Market Trends of Aircraft Turbine Engine Industry

Commercial Segment to Dominate Market Share During the Forecast Period

The commercial segment holds the largest aircraft turbine engine market share due to several compelling drivers. The rise in global air passenger travel, attributed to rising incomes, the growth of the middle class, and urbanization, provides a strong foundation for the commercial aircraft engine industry. This growth trend is expected to continue, with many people joining the global middle class, especially from countries like India and China.

The industry perspective emphasizes the rise of single-aisle aircraft, driven by cost and convenience factors for air travelers. This shift is reflected in the increasing usage of aircraft like Airbus’ A320 and Boeing’s B737, comprising a significant portion of the global passenger jet fleet. Single-aisle aircraft are expected to dominate the market, offering commercial aircraft turbine manufacturers opportunities. Additionally, the stringent regulatory and compliance standards imposed on commercial turbine engines create a unique barrier to entry for other segments. Meeting these requirements necessitates substantial research, development, and manufacturing investments, which often only established commercial engine manufacturers can undertake.

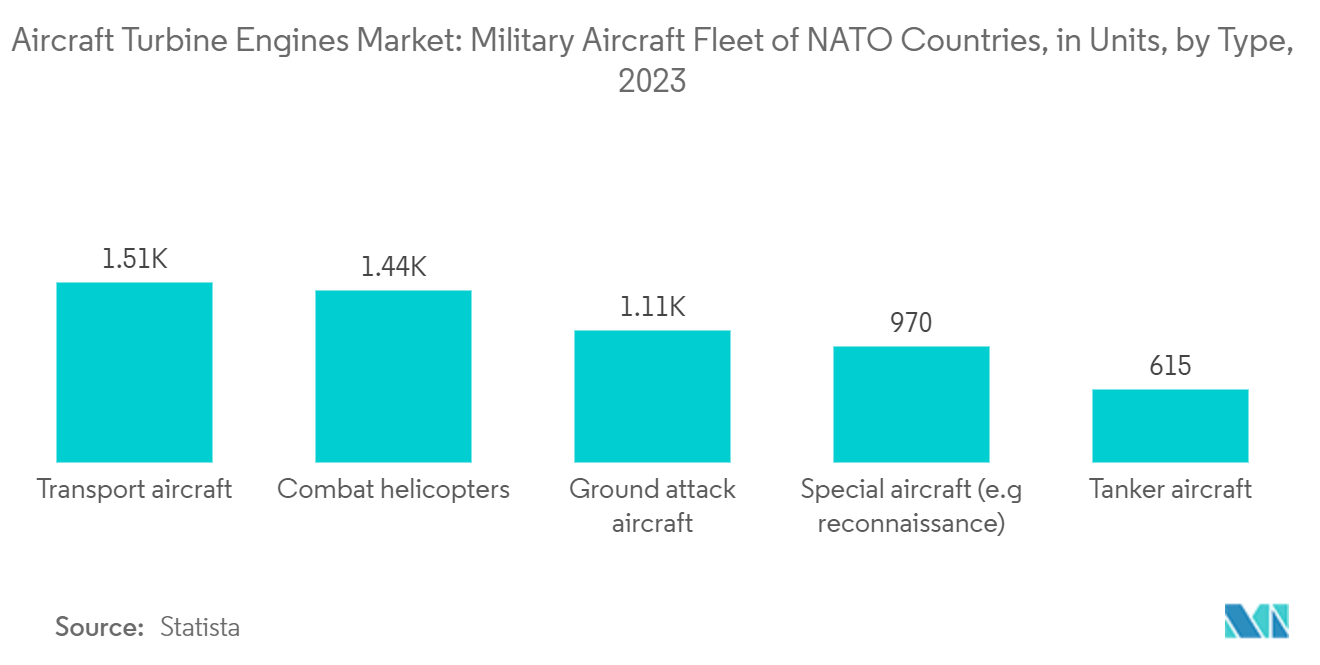

Military engines are designed to last for decades, withstanding the rigors of combat and extensive use. Consequently, governments are heavily invested in their maintenance, repair, and upgrade, resulting in a continuous revenue stream for manufacturers and service providers. For instance, in July 2022, Rolls-Royce plc entered the final build stage for the world’s largest aero-engine technology demonstrator, UltraFan, offering technologies to support sustainable air travel in the future. The demonstrator engine has a fan diameter of 140 inches and runs on 100% Sustainable Aviation Fuel. The new engine offers a 25% fuel efficiency improvement compared with the first generation of the Trent engine. In the longer term, the UltraFan engine’s scalable technology from 25,000 to 100,000 lb. thrust offers the potential to power new wide-body and narrow-body commercial aircraft.

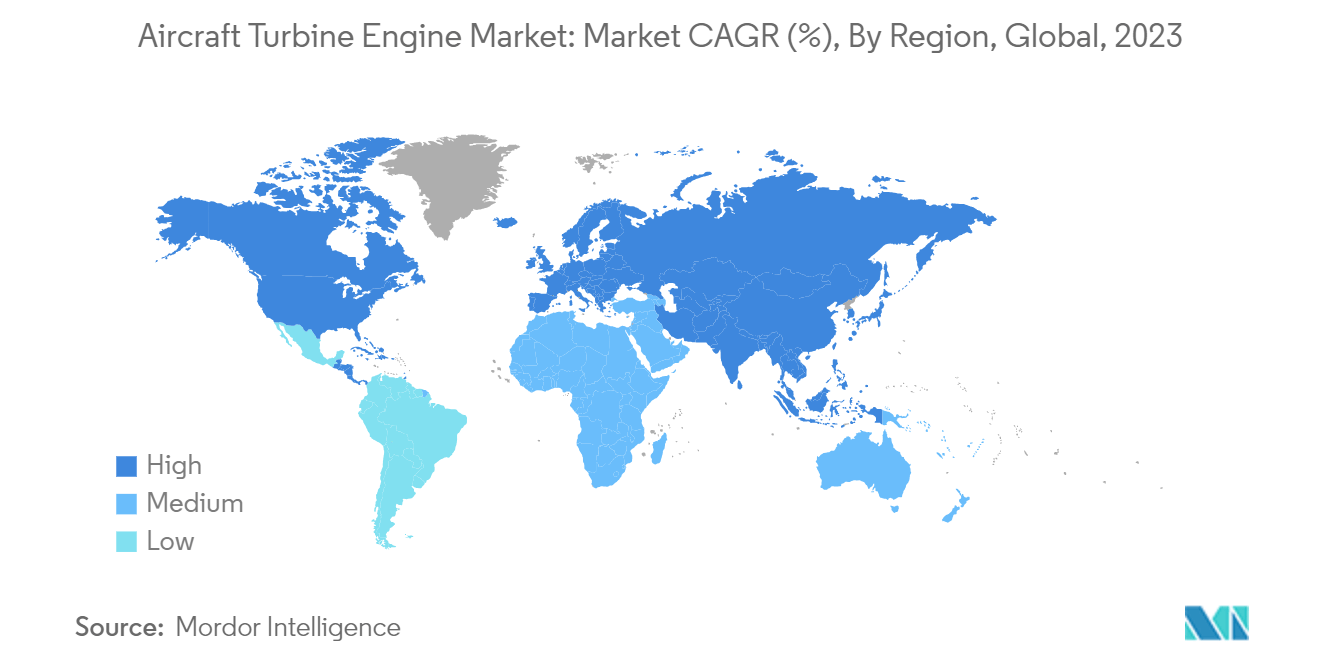

Asia-Pacific to Dominate the Market Share During the Forecast Period

The ongoing success of the LCC model has contributed to steady growth in passenger traffic in Asia-Pacific. It has also created significant opportunities for developing regional aircraft and engine manufacturers by stimulating various companies to invest in aircraft manufacturing activities. The rise in demand for newer and improved aircraft versions has resulted in a simultaneous requirement for aircraft gas turbine engines. Numerous airline operators are trying to collaborate with engine OEMs to receive superior MRO and after-services. For instance, Airbus has already realized the potential of the MRO market and has put in efforts to accelerate its presence in Asia-Pacific through acquisitions, joint ventures (JVs), and partnerships.

Other international engine suppliers will be required to maintain an adequate supply of engines and associated components, as these developments will promote the regional market during the forecast period. For instance, In June 2023, India and the US announced the agreement between Hindustan Aeronautics Limited (HAL) and GE Aerospace to produce fighter jet engines for the Indian Air Force (IAF). The deal takes place in the context of efforts by the IAF to improve its capabilities and capacities. The IAF procures 114 multi-role fighter jets (MRFA), acquiring additional Light Combat Aircraft (LCA) Mk1A and LCA Mk2. GE's F404 engines power India's only indigenous fighter jet, LCA Tejas. GE has manufactured 75 F404 engines, and another 99 are on order with LCA Mk1A. In the ongoing development program for LCA Mk2, 8 F414 engines have been supplied.