Market Size of Aircraft Turbine Engine Industry

| Study Period | 2019 - 2029 |

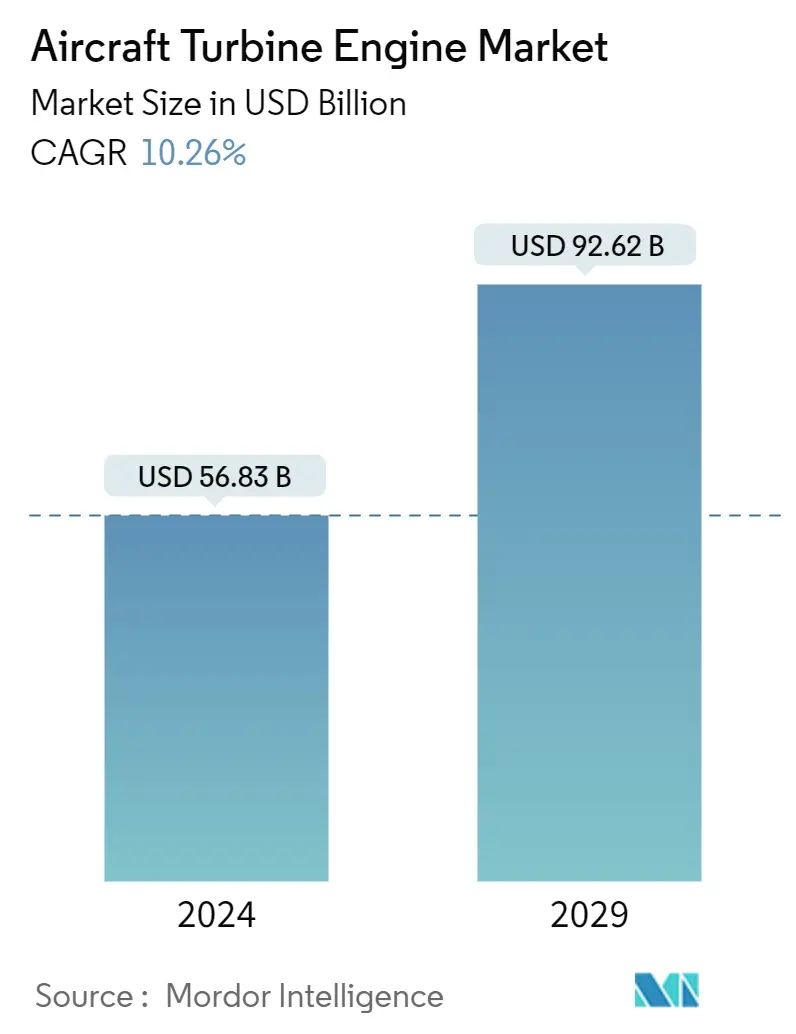

| Market Size (2024) | USD 56.83 Billion |

| Market Size (2029) | USD 92.62 Billion |

| CAGR (2024 - 2029) | 10.26 % |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order |

Aircraft Turbine Engine Market Analysis

The Aircraft Turbine Engine Market size is estimated at USD 56.83 billion in 2024, and is expected to reach USD 92.62 billion by 2029, growing at a CAGR of 10.26% during the forecast period (2024-2029).

The demand for aircraft engines is driven primarily by either an increase in the order book of aircraft (business jet, commercial, or military aircraft) or a replacement for the engines for the existing aircraft fleet. Aircraft OEMs and engine manufacturers are engaging in extensive integration efforts to enhance performance and extend the range of aircraft. Investments in the R&D of such technologies are anticipated to bolster the market prospects during the forecast period.

Since modern-day airlines operate on a merged profit model, the profit margins are relatively low. This scenario makes it challenging for operators to procure a new fleet and pay significant cash to complete the transaction. However, due to the emerging dynamics of the aircraft and engine leasing business, airlines have access to the comfort of opting for lease agreements from aircraft financing entities, providing financial relief to airlines and granting them temporary access to increased capacity.

The manufacturing cycle of aircraft engine OEMs is expected to undergo rapid transformation due to the increasing use of 3D printing and ceramic matrix composites to construct critical components of an aircraft engine. Furthermore, emerging technologies such as a hybrid-electric jet engine are anticipated to enhance the current business opportunities for the market players.

Aircraft Turbine Engine Industry Segmentation

The scope of the study encompasses the turbine engines designed and integrated into both commercial and military aircraft and helicopters. Though the market projections exclude the sales of aftermarket parts and components, replacement sales of engines have been considered within the report's purview.

The aircraft turbine engine market is segmented by end-user, aircraft type, and geography. By end-user, the market is segmented into civil and commercial aviation and military aviation. By aircraft type, the market is segmented into fixed-wing and rotorcraft. The report also covers the market sizes and forecasts for the aircraft turbine engine market in major countries across different regions. For each segment, the market size is provided in terms of value (USD).

| End-user | |

| Civil and Commercial Aviation | |

| Military Aviation |

| Aircraft Type | |

| Fixed-wing | |

| Rotorcraft |

| Geography | ||||||||

| ||||||||

| ||||||||

| ||||||||

| ||||||||

|

Aircraft Turbine Engine Market Size Summary

The aircraft turbine engine market is poised for significant growth, driven by increasing demand for both new aircraft and engine replacements within existing fleets. This demand is fueled by the expansion of global air travel, particularly in the commercial segment, where rising incomes and urbanization are contributing to a burgeoning middle class. The market is characterized by a semi-consolidated structure with major players like CFM International, General Electric Company, Pratt & Whitney, Rolls-Royce plc, and Safran competing on various fronts such as technology, quality, and price. The commercial segment holds the largest market share, with single-aisle aircraft like Airbus’ A320 and Boeing’s B737 leading the charge due to their cost-effectiveness and convenience for travelers. The industry is also witnessing a shift towards advanced manufacturing techniques, including 3D printing and ceramic matrix composites, which are expected to transform the production cycle of aircraft engines.

The market landscape is further shaped by the evolving dynamics of aircraft and engine leasing, providing financial flexibility to airlines amidst low profit margins. Technological advancements, such as hybrid-electric jet engines, are opening new avenues for market players, while stringent regulatory standards in the commercial segment create barriers that favor established manufacturers. Military engines, designed for longevity and resilience, ensure a steady revenue stream through maintenance and upgrades. The Asia-Pacific region is experiencing steady growth, driven by the success of low-cost carriers and increased passenger traffic, prompting investments in regional aircraft manufacturing. Collaborative efforts between airlines and engine OEMs are enhancing maintenance, repair, and overhaul services, with significant partnerships and agreements, such as those between Hindustan Aeronautics Limited and GE Aerospace, bolstering regional market prospects. The competitive environment is expected to intensify with ongoing technological innovations, mergers, and acquisitions, making it a pivotal period for adopting new-generation aircraft and engines.

Aircraft Turbine Engine Market Size - Table of Contents

-

1. MARKET DYNAMICS

-

1.1 Market Overview

-

1.2 Market Drivers

-

1.3 Market Restraints

-

1.4 Porter's Five Forces Analysis

-

1.4.1 Bargaining Power of Buyers/Consumers

-

1.4.2 Bargaining Power of Suppliers

-

1.4.3 Threat of New Entrants

-

1.4.4 Threat of Substitute Products

-

1.4.5 Intensity of Competitive Rivalry

-

-

-

2. MARKET SEGMENTATION

-

2.1 End-user

-

2.1.1 Civil and Commercial Aviation

-

2.1.2 Military Aviation

-

-

2.2 Aircraft Type

-

2.2.1 Fixed-wing

-

2.2.2 Rotorcraft

-

-

2.3 Geography

-

2.3.1 North America

-

2.3.1.1 United States

-

2.3.1.2 Canada

-

-

2.3.2 Europe

-

2.3.2.1 United Kingdom

-

2.3.2.2 France

-

2.3.2.3 Germany

-

2.3.2.4 Russia

-

2.3.2.5 Rest of Europe

-

-

2.3.3 Asia-Pacific

-

2.3.3.1 China

-

2.3.3.2 India

-

2.3.3.3 Japan

-

2.3.3.4 South Korea

-

2.3.3.5 Singapore

-

2.3.3.6 Rest of Asia-Pacific

-

-

2.3.4 Latin America

-

2.3.4.1 Brazil

-

2.3.4.2 Rest of Latin America

-

-

2.3.5 Middle-East and Africa

-

2.3.5.1 Saudi Arabia

-

2.3.5.2 Egypt

-

2.3.5.3 Israel

-

2.3.5.4 South Africa

-

2.3.5.5 Rest of Middle-East and Africa

-

-

-

Aircraft Turbine Engine Market Size FAQs

How big is the Aircraft Turbine Engine Market?

The Aircraft Turbine Engine Market size is expected to reach USD 56.83 billion in 2024 and grow at a CAGR of 10.26% to reach USD 92.62 billion by 2029.

What is the current Aircraft Turbine Engine Market size?

In 2024, the Aircraft Turbine Engine Market size is expected to reach USD 56.83 billion.