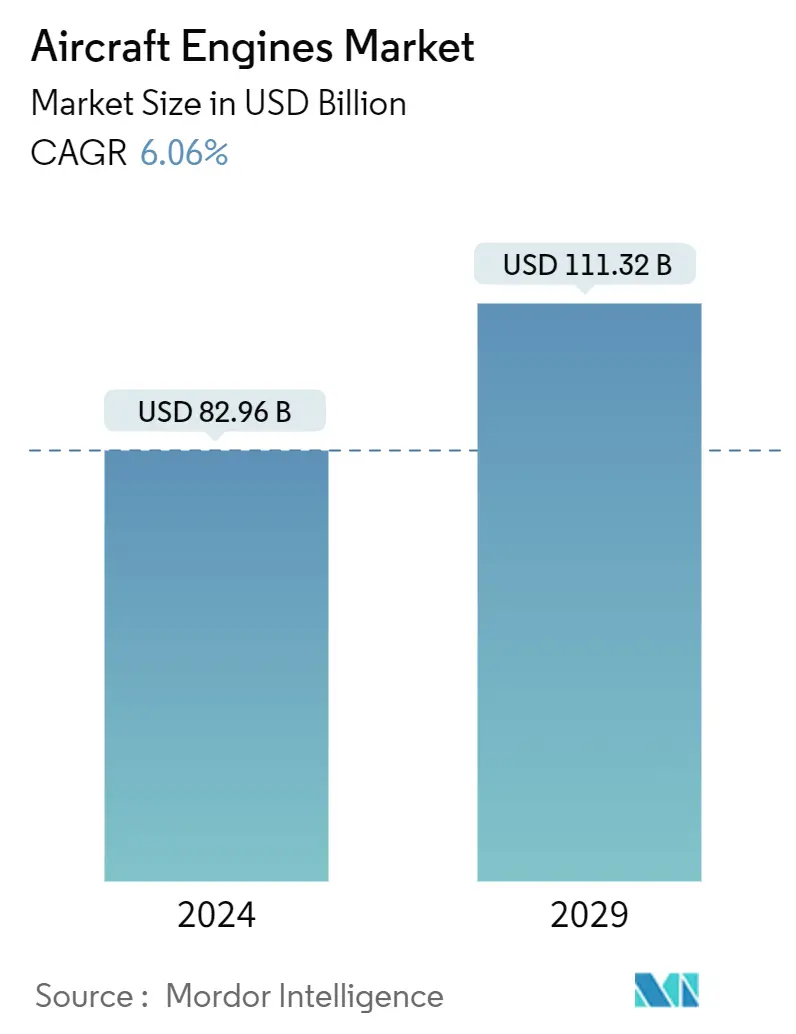

Market Size of Aircraft Engines Industry

| Study Period | 2019 - 2029 |

| Market Size (2024) | USD 82.96 Billion |

| Market Size (2029) | USD 111.32 Billion |

| CAGR (2024 - 2029) | 6.06 % |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

Major Players

*Disclaimer: Major Players sorted in no particular order |

Aircraft Engine Market Analysis

The Aircraft Engines Market size is estimated at USD 82.96 billion in 2024, and is expected to reach USD 111.32 billion by 2029, growing at a CAGR of 6.06% during the forecast period (2024-2029).

The industry growth is also driven by the demand for new-generation engines with low emissions and lower weight, which will likely enhance aircraft fuel efficiency. Due to this trend, the largest companies in the market are investing in research and development of new engine models utilizing the latest technologies, like additive manufacturing and composite technologies.

However, growing concerns over the failure of aircraft engines during operation and delays in deliveries are some of the factors hampering the industry growth.

Aircraft OEMs and engine manufacturers are engaging in extensive integration efforts to enhance performance and extend the range of aircraft. The investments towards the R&D of such technologies are anticipated to bolster the market prospects during the forecast period. The manufacturing cycle of aircraft engine OEMs is expected to undergo rapid transformation due to the increasing use of 3D printing and ceramic matrix composites to construct critical components of an aircraft engine. Furthermore, emerging industry trends such as a hybrid-electric jet engine are anticipated to enhance the current business opportunities for the market players.

Aircraft Engine Industry Segmentation

The industry analysis of the aircraft engines market includes all the new engines installed on fixed and rotary-wing aircraft that are used in military, commercial, and general aviation aircraft. The aftermarket sales of the engine and its parts and sales of auxiliary power units (APUs) are excluded from the study.

An aircraft engine is a component of the aircraft's advanced propulsion system that generates mechanical power. Based on the engine type, the market is segmented into turbofan, turboprop, turboshaft, and piston. The aircraft engine market is also segmented based on aircraft type into commercial aviation, military aviation, and general aviation. Commercial aviation is further segmented into narrow-body aircraft, wide-body aircraft, and regional aircraft. Military aviation is further segmented into combat aircraft and non-combat aircraft. General aviation is further segmented into business jets, helicopters, turboprop aircraft, and piston-engine aircraft. The report also covers the market share, size, and forecasts for the aircraft engine market in major countries across different regions (North America, Europe, Asia-Pacific, Latin America, and the Middle East and Africa).

For each segment, the market size is provided in terms of value (USD).

| Engine Type | |

| Turbofan | |

| Turboprop | |

| Turboshaft | |

| Piston |

| Aircraft Type | ||||||

| ||||||

| ||||||

|

| Geography | ||||||||||||||||||||||

| ||||||||||||||||||||||

| ||||||||||||||||||||||

| ||||||||||||||||||||||

| ||||||||||||||||||||||

|

Aircraft Engines Market Size Summary

The aircraft engine market is poised for significant growth, driven by the increasing demand for new-generation engines that offer low emissions and enhanced fuel efficiency. This demand is prompting substantial investments in research and development, with companies leveraging advanced technologies such as additive manufacturing and composite materials. Despite challenges like concerns over engine reliability and delivery delays, the market is expected to benefit from extensive integration efforts between aircraft OEMs and engine manufacturers. These efforts aim to improve performance and extend aircraft range, with emerging technologies like hybrid-electric jet engines presenting new business opportunities. The commercial aircraft segment currently leads the market, supported by a robust backlog of aircraft deliveries, with a faster recovery anticipated for narrow-body aircraft due to rising domestic travel demand.

The Asia-Pacific region is expected to experience the highest growth, fueled by strong domestic air travel demand and fleet modernization plans by low-cost airlines. Geopolitical tensions are also driving investments in advanced aircraft procurement, as seen in agreements like the one between India and GE Aerospace for fighter jet engines. The market is consolidated, with major players such as General Electric, RTX Corporation, Rolls-Royce, Safran, and Honeywell dominating both commercial and military segments. These companies are actively partnering with aircraft manufacturers to develop sustainable, low-weight, and low-emission engine solutions. Regional collaborations, such as those involving India's DRDO and Safran, are also on the rise, aiming to enhance local manufacturing capabilities and expand geographical presence.

Aircraft Engines Market Size - Table of Contents

-

1. MARKET DYNAMICS

-

1.1 Market Overview

-

1.2 Market Drivers

-

1.3 Market Restraints

-

1.4 Porter's Five Forces Analysis

-

1.4.1 Bargaining Power of Suppliers

-

1.4.2 Bargaining Power of Buyers/Consumers

-

1.4.3 Threat of New Entrants

-

1.4.4 Threat of Substitute Products

-

1.4.5 Intensity of Competitive Rivalry

-

-

-

2. MARKET SEGMENTATION

-

2.1 Engine Type

-

2.1.1 Turbofan

-

2.1.2 Turboprop

-

2.1.3 Turboshaft

-

2.1.4 Piston

-

-

2.2 Aircraft Type

-

2.2.1 Commercial Aviation

-

2.2.1.1 Narrow-body Aircraft

-

2.2.1.2 Wide-body Aircraft

-

2.2.1.3 Regional Aircraft

-

-

2.2.2 Military Aviation

-

2.2.2.1 Combat Aircraft

-

2.2.2.2 Non-combat Aircraft

-

-

2.2.3 General Aviation

-

2.2.3.1 Business Jets

-

2.2.3.2 Helicopters

-

2.2.3.3 Turboprop Aircraft

-

2.2.3.4 Piston Engine Aircraft

-

-

-

2.3 Geography

-

2.3.1 North America

-

2.3.1.1 United States

-

2.3.1.1.1 Engine Type

-

2.3.1.1.2 Aircraft Type

-

-

2.3.1.2 Canada

-

2.3.1.2.1 Engine Type

-

2.3.1.2.2 Aircraft Type

-

-

-

2.3.2 Europe

-

2.3.2.1 United Kingdom

-

2.3.2.1.1 Engine Type

-

2.3.2.1.2 Aircraft Type

-

-

2.3.2.2 Germany

-

2.3.2.2.1 Engine Type

-

2.3.2.2.2 Aircraft Type

-

-

2.3.2.3 France

-

2.3.2.3.1 Engine Type

-

2.3.2.3.2 Aircraft Type

-

-

2.3.2.4 Rest of Europe

-

2.3.2.4.1 Engine Type

-

2.3.2.4.2 Aircraft Type

-

-

-

2.3.3 Asia-Pacific

-

2.3.3.1 China

-

2.3.3.1.1 Engine Type

-

2.3.3.1.2 Aircraft Type

-

-

2.3.3.2 India

-

2.3.3.2.1 Engine Type

-

2.3.3.2.2 Aircraft Type

-

-

2.3.3.3 Japan

-

2.3.3.3.1 Engine Type

-

2.3.3.3.2 Aircraft Type

-

-

2.3.3.4 South Korea

-

2.3.3.4.1 Engine Type

-

2.3.3.4.2 Aircraft Type

-

-

2.3.3.5 Rest of Asia-Pacific

-

2.3.3.5.1 Engine Type

-

2.3.3.5.2 Aircraft Type

-

-

-

2.3.4 Latin America

-

2.3.4.1 Brazil

-

2.3.4.1.1 Engine Type

-

2.3.4.1.2 Aircraft Type

-

-

2.3.4.2 Rest of Latin America

-

2.3.4.2.1 Engine Type

-

2.3.4.2.2 Aircraft Type

-

-

-

2.3.5 Middle-East and Africa

-

2.3.5.1 United Arab Emirates

-

2.3.5.1.1 Engine Type

-

2.3.5.1.2 Aircraft Type

-

-

2.3.5.2 Saudi Arabia

-

2.3.5.2.1 Engine Type

-

2.3.5.2.2 Aircraft Type

-

-

2.3.5.3 Qatar

-

2.3.5.3.1 Engine Type

-

2.3.5.3.2 Aircraft Type

-

-

2.3.5.4 Rest of Middle-East and Africa

-

2.3.5.4.1 Engine Type

-

2.3.5.4.2 Aircraft Type

-

-

-

-

Aircraft Engines Market Size FAQs

How big is the Aircraft Engines Market?

The Aircraft Engines Market size is expected to reach USD 82.96 billion in 2024 and grow at a CAGR of 6.06% to reach USD 111.32 billion by 2029.

What is the current Aircraft Engines Market size?

In 2024, the Aircraft Engines Market size is expected to reach USD 82.96 billion.