Market Trends of Aircraft Actuators Industry

The Linear Actuators Segment is Anticipated to Show the Highest Growth During the Forecast Period

The linear actuators segment is poised for significant growth during the forecast period. Electric linear actuators, known for their precision, outshine their hydraulic and pneumatic counterparts. These actuators are versatile and cater to a wide range of force requirements. Notably, electric linear actuators are the top choice for many aircraft manufacturers. Their ease of networking and swift programmability sets electric linear actuators apart. They offer real-time diagnostics and maintenance feedback. Moreover, these actuators grant precise motion control, allowing for tailored speeds, stroke lengths, and applied forces. In addition, they operate more quietly than their hydraulic and pneumatic counterparts. Recognizing these benefits, companies increasingly join forces to harness technology and bolster their market reach.

For example, in July 2022, Parker Aerospace unveiled a collaboration to advance electric flight. Partnering with Aviation Aircraft, Parker Aerospace spearheaded the development of six technology system packages for the groundbreaking 'Alice' commuter aircraft. These packages featured cutting-edge electromechanical actuators, electronic control units, and position sensors. With a global uptick in commercial and defense aircraft production, manufacturers are increasingly turning to linear actuators for their myriad benefits. Given these trends, the linear actuator segment is poised for robust growth over the forecast period.

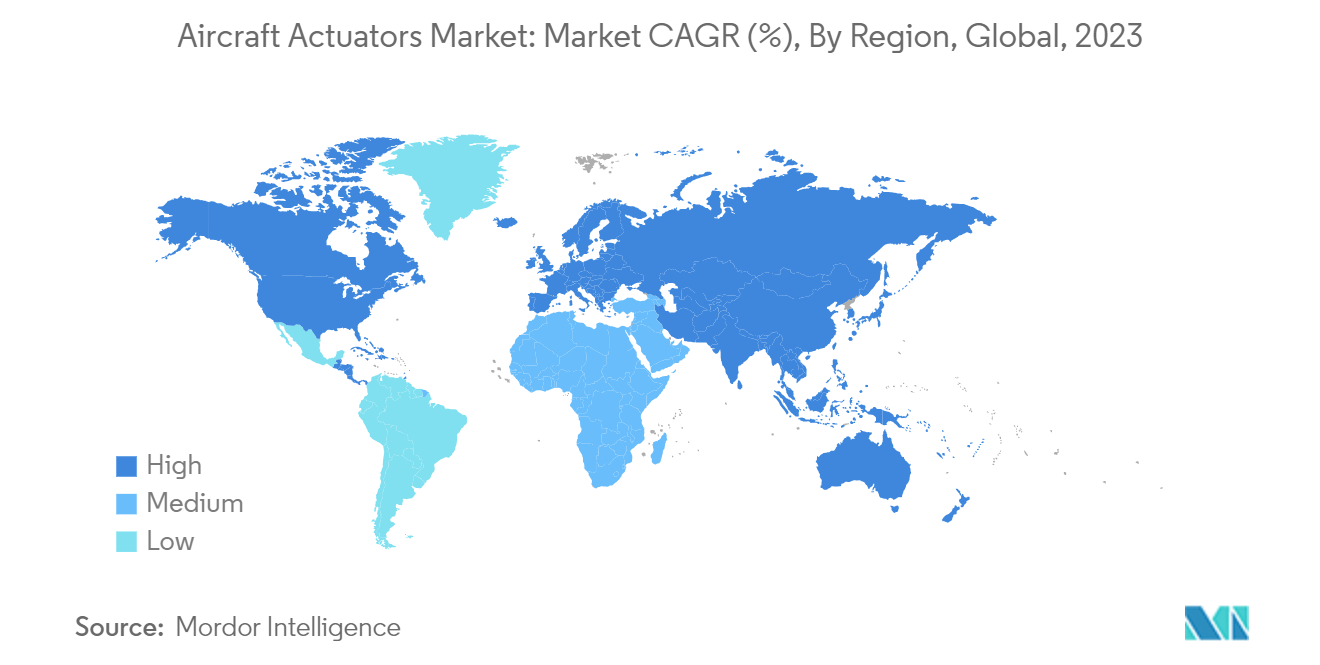

Asia-Pacific is Projected to Record Significant Growth During the Forecast Period

In recent years, Asia-Pacific has witnessed significant growth in the aviation industry due to escalating investments from India and China. This surge is further fueled by the mounting demand for commercial aircraft, a response to the region's burgeoning air traffic. Notably, in 2020, China surpassed the United States to become the world's largest aviation market regarding seating capacity, a shift largely magnified by the United States cutting nearly 30% of its seating capacity amid the pandemic.

Highlighting China's aviation industry's vigor, in November 2022, China Aviation Supplies (CASC) inked a significant deal with Airbus, securing 140 jets in a USD 17 billion agreement, encompassing CASC's existing orders. Moreover, in July 2022, Airbus further solidified its position in the Chinese market by finalizing orders with major carriers like Air China, China Eastern, China Southern, and Shenzhen Airlines for a collective 292 A320 family aircraft. Such robust orders underscore China's aviation market's rebound and point toward a heightened demand for aircraft actuators, promising substantial market growth in the coming years.

Shifting focus to India, the nation is actively bolstering its military capabilities. With a military budget of USD 76 billion, India ranks as the world's fourth-largest spender, trailing only the United States, China, and Russia. A significant portion of this budget is earmarked for advancements in military aircraft, setting the stage for notable developments in the industry. In a testament to this commitment, in October 2022, the Tata-Airbus consortium, a pioneering private venture in India's military landscape, commenced the construction of a manufacturing facility. This facility is dedicated to producing the C-295 medium transport aircraft to modernize the Indian Air Force's transportation fleet.