Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Market Size (2025) | USD 125.71 Billion |

| Market Size (2030) | USD 162.90 Billion |

| Growth Rate (2025 - 2030) | 5.32% CAGR |

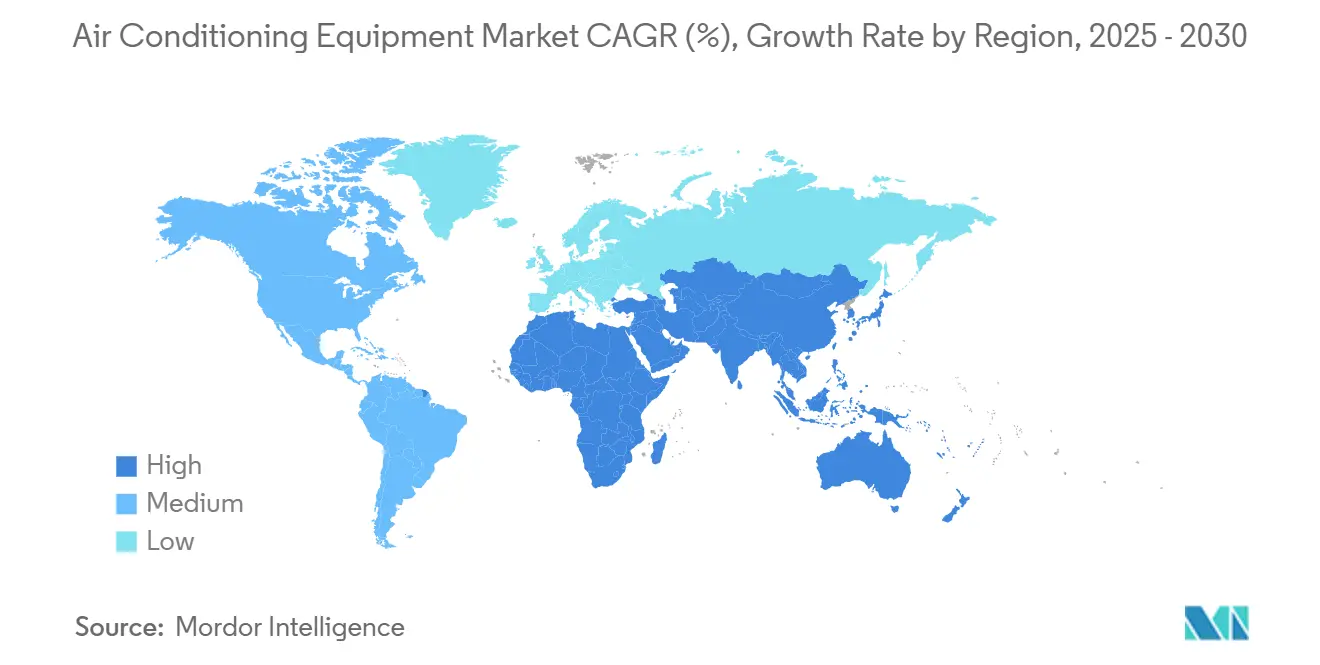

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia Pacific |

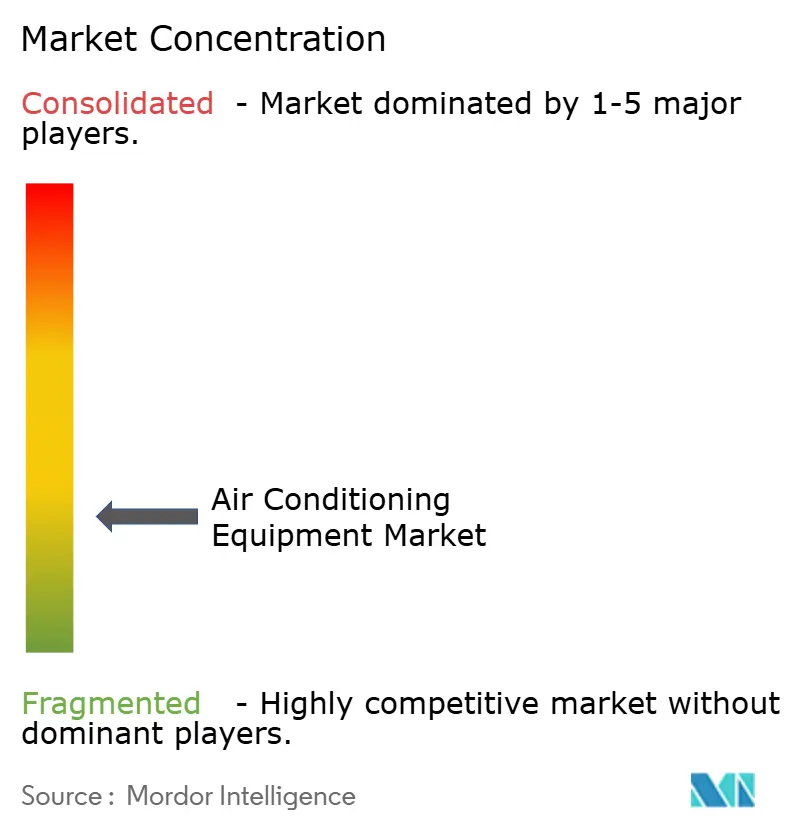

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Air Conditioning Equipment Market Analysis by Mordor Intelligence

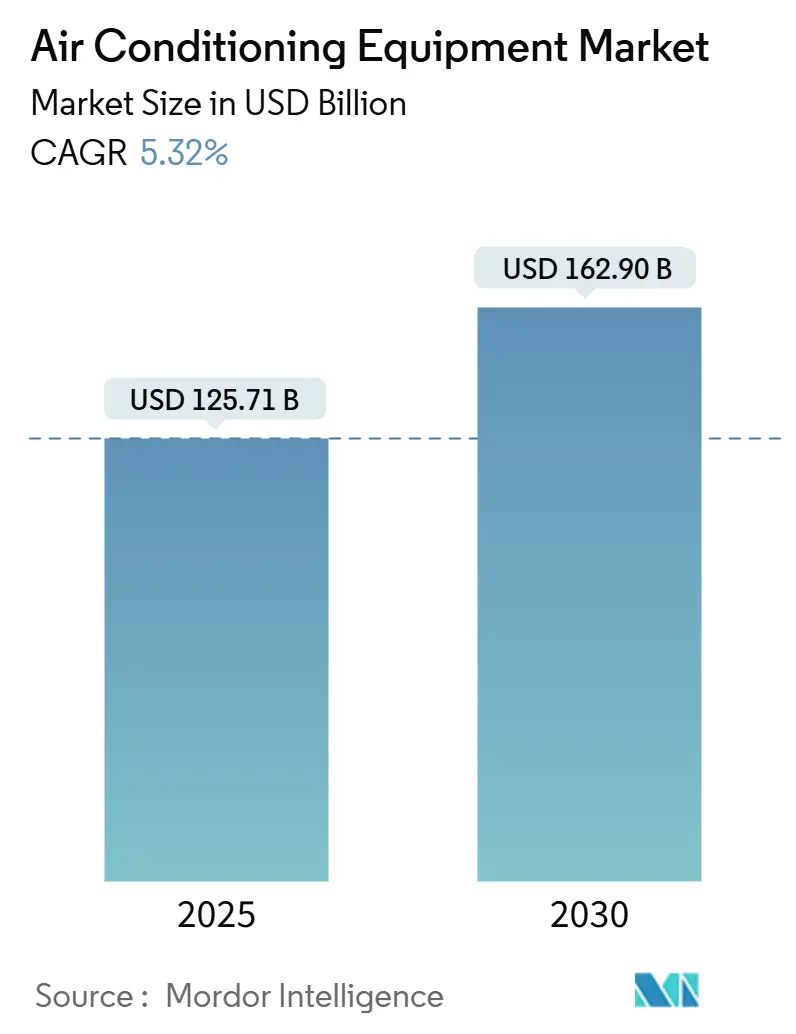

The air conditioning equipment market size reached USD 125.71 billion in 2025 and is projected to rise to USD 162.9 billion by 2030, registering a 5.32% CAGR during the forecast period. Sustained demand stems from hotter summers, accelerating urban construction, and faster replacement cycles toward inverter- and heat-pump-based systems. Manufacturers continue to expand its capacity in the Asia-Pacific region, where domestic incentives and export demand align. Component supply chains are regionalizing to mitigate freight costs and trade risks, while digital monitoring tools improve service profitability. At the same time, data center build-outs create a high-margin precision-cooling niche that outpaces overall volume growth.

Key Report Takeaways

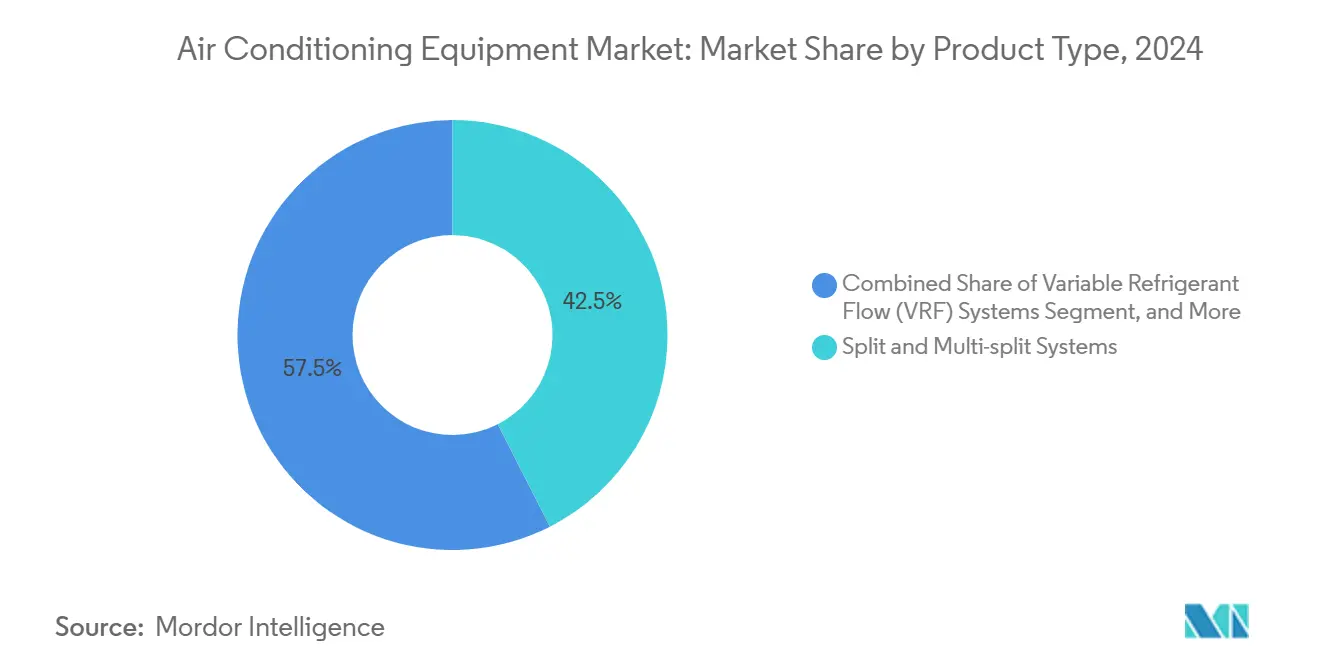

- By product type, split and multi-split units led with 42.53% revenue share in 2024; variable refrigerant flow systems are forecast to expand at a 6.73% CAGR to 2030.

- By technology, inverter platforms captured 68.86% of the 2024 air conditioning equipment market share and are projected to advance at a 6.53% CAGR through 2030.

- By end-user, residential applications accounted for 64.12% of the air conditioning equipment market size in 2024; commercial demand is projected to grow at a 7.85% CAGR between 2025-2030.

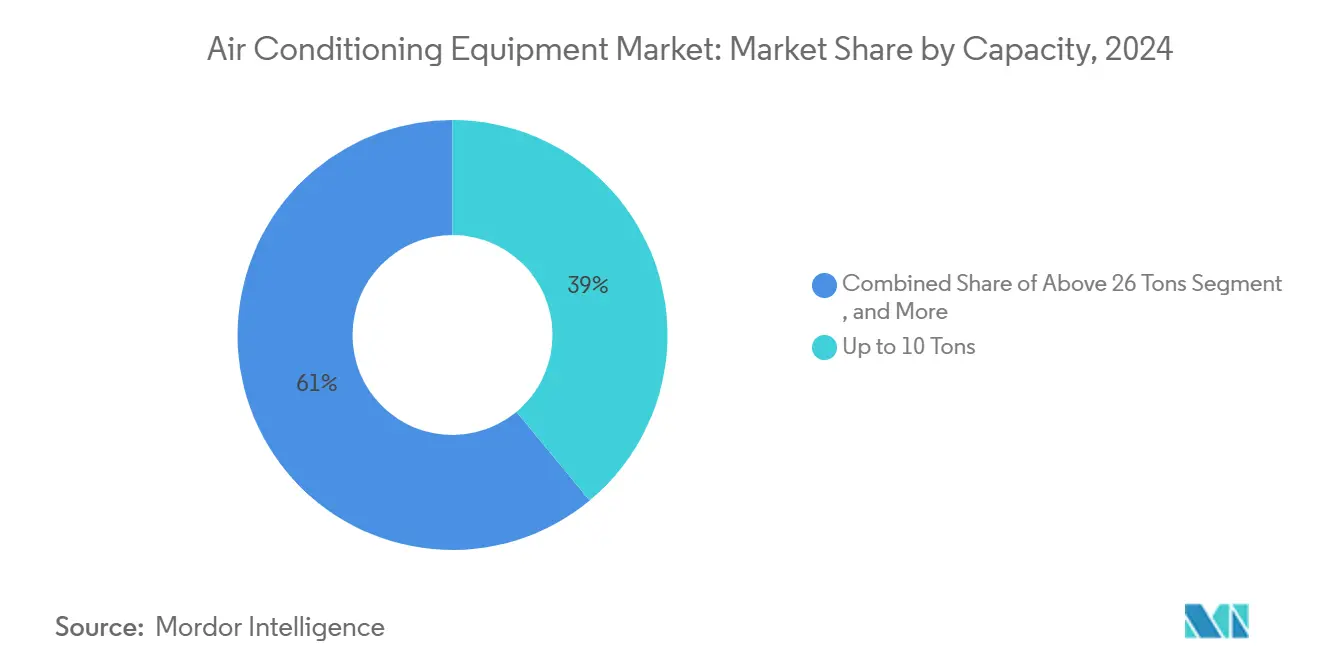

- By capacity, above-26-ton systems represented the fastest-growing segment, with an 8.01% CAGR to 2030, although units with a capacity of ≤ 10 tons dominated the volume at 38.97% in 2024.

- By distribution channel, dealer and retail stores captured 42.12% of 2024 revenue, while direct sales are projected to post the highest 7.58% CAGR through 2030.

- By geography, Asia-Pacific commanded 40.32% of 2024 sales and is expected to post an 8.43% CAGR through 2030.

Global Air Conditioning Equipment Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising global temperatures and heat-wave frequency | +1.2% | Global, with acute effects in Middle East, South Asia, Southern US | Medium term (2-4 years) |

| Government energy-efficiency mandates and incentive programs | +1.8% | North America, Europe, China, Japan | Short term (≤ 2 years) |

| Urbanisation-led construction boom in emerging economies | +1.5% | Asia-Pacific core, spill-over to Latin America, Africa | Long term (≥ 4 years) |

| Replacement demand for ageing AC stock with inverter and VRF units | +1.1% | Global, with early gains in developed markets | Medium term (2-4 years) |

| Data-centre build-outs escalating precision-cooling demand | +0.9% | North America, Europe, select Asia-Pacific hubs | Short term (≤ 2 years) |

| Cold-chain and vertical-farming expansion requiring dedicated HVAC | +0.7% | Global, concentrated in food-importing regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Government Energy-Efficiency Mandates Drive Market Transformation

Rules restricting high-GWP refrigerants and boosting seasonal efficiency ratings accelerate turnover toward heat-pump-based products and inverter compressors. [1]California Energy Commission, “Building Energy Efficiency Standards,” energy.ca.gov California’s 2025 code requires heat pumps in new homes, while the EPA AIM Act cuts HFC production 40% by 2024. Similar phase-downs in the European Union shrink supplies of R-410A, making R-32 and R-454B the mainstream choices. These measures encourage builders and homeowners to adopt higher SEER units, thereby shortening payback periods in regions with high electricity costs. Brands that already produce low-GWP refrigerant equipment gain a first-mover advantage and protect margins despite metal price inflation. Utility rebates and tax credits further stimulate early replacement, especially in states that track greenhouse-gas targets.

Urbanization-Led Construction Boom Expands Market Addressability

Emerging economies add millions of new urban residents annually, channeling infrastructure funds into multi-family housing and commercial complexes. [2]Asian Development Bank, “Urbanization in Asia,” adb.org China’s urbanization rate is nearing 70%, while India’s urban population is set to surpass 600 million by 2030, increasing the baseline load for room air conditioners and packaged units. Local building codes now integrate green-building requirements, driving architects toward centralized VRF systems that meet both energy and comfort goals. Governments link smart-city grants to high-efficiency HVAC installations, enabling suppliers to bundle IoT sensors, demand-response controls, and onsite renewable integration. As a result, the installed base of obsolete fixed-speed compressors declines steadily in Tier 2 and Tier 3 cities.

Data Center Build-Outs Create High-Value Precision-Cooling Segment

The global shift to AI and cloud services raises rack densities above 20 kW, necessitating purpose-built computer-room air handlers that maintain temperature within ±0.5 °C. [3]AAON, “AAON expands production,” climatecontrolnews.com.au AAON’s new 787,000 ft² Memphis facility, set to bring 828 skilled jobs online in 2025, targets this exacting niche. Daikin Applied’s USD 121 million Tijuana plant will supply custom systems for hyperscale campuses. Precision-cooling equipment yields margins several points above those of standard commercial rooftop units, encouraging incumbents to lock in long-term service contracts that include remote diagnostics and refrigerant leak alerts.

Replacement Demand Accelerates Technology Transitions

Equipment installed during the early 2000s construction boom nears the end of its life, opening opportunities to swap fixed-speed R-410A models for inverter-driven units using R-454B. Johnson Controls invested USD 3 million in Izmir, Turkey, tripling YORK heat-pump output to serve European retrofits. [4]Johnson Controls, “Expansion of Izmir Plant,” johnsoncontrols.com Higher energy prices in Europe compress paybacks to under five years, while utility rebates in Japan and the U.S. Southeast further shorten the cycles. Installers promote connected thermostats as a bundled upsell, reducing callbacks through predictive maintenance software.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront equipment and installation costs | -1.4% | Global, acute in price-sensitive emerging markets | Short term (≤ 2 years) |

| Raw-material and refrigerant price volatility | -0.8% | Global, with manufacturing hubs in Asia-Pacific most affected | Medium term (2-4 years) |

| Stringent refrigerant phase-down compliance costs | -0.6% | North America, Europe, developed Asia-Pacific markets | Short term (≤ 2 years) |

| Skilled-technician shortage for advanced system installation | -1.1% | North America, Europe, developed Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Skilled-Technician Shortage Constrains Market Expansion

The sector employs 425,200 technicians against future demand of 459,700 by 2034, leaving an 80,000-worker gap and requiring 40,100 openings each year. More than half of the current workforce is older than 45, so retirements are expected to spike as systems become increasingly complex. VRF charging and inverter diagnostics demand new skills that three-year apprenticeships seldom cover, forcing contractors to ration jobs and raise wages. Training centers scramble to add simulator-based curricula, yet pipeline growth lags equipment demand. Project delays in the data center and hospitality segments push some owners to accept less efficient interim solutions, muting near-term revenue potential.

High Upfront Equipment and Installation Costs Limit Market Penetration

Premium inverter systems and heat pumps can double total installed cost compared with legacy split units, especially when electrical upgrades are required. Metal costs add pressure: copper averaged USD 4.20 per lb and aluminum gained 2% in 2024. Wage inflation exceeds 23.5% compared to pre-COVID levels, prompting contractors to pass costs directly to end-users. Although rebates and low-interest green loans mitigate the impacts in developed markets, budget-constrained households in Southeast Asia often defer upgrades, thereby slowing the adoption curves.

Segment Analysis

By Product Type: Variable Refrigerant Flow Systems Gain Ground

Split and multi-split units maintained the largest slice of the air conditioning equipment market at 42.53% in 2024 as their plug-and-play design suits mass housing and small offices. Commercial builders, however, are specifying VRF solutions that deliver up to 30% energy savings and zone-level climate control. VRF’s 6.73% CAGR reflects rising retrofit activity in educational campuses and healthcare facilities that operate around the clock. Manufacturers differentiate through modular outdoor units, longer piping runs, and integrated building-management system interfaces. The air conditioning equipment market size attributable to packaged rooftops remains meaningful in supermarkets and light industrial facilities, yet their share slips as designers prioritize higher SEER2 ratings.

VRF adoption influences installer skill requirements, spurring OEMs to offer factory commissioning services. Supply-side integration is deepening as compressor plants open closer to major markets, lowering logistical carbon footprints. Still, split systems retain volume leadership because retail chains and online platforms promote standardized capacities with immediate availability. Chillers anchor district cooling and large process lines, where redundancy is essential; their specification cycle is lengthy, but revenue per project is sizeable, helping suppliers offset price competition in commodity splits.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Technology: Inverter Platforms Anchor Efficiency Leadership

Inverter technology accounted for 68.86% of 2024 revenue and continues to outpace fixed-speed alternatives at a 6.53% CAGR. Variable-speed compressors align cooling output with load, trimming energy usage by up to 50%. Mitsubishi Electric’s USD 143.5 million Kentucky compressor plant, with an annual capacity of 1 million units from 2027, demonstrates how localized component supply secures a share in the air conditioning equipment market. Connectivity upgrades now bundle Wi-Fi modules, enabling demand-response programs that utilities reward. Fixed-speed units remain prevalent in low-tariff regions and informal markets, but stricter minimum-efficiency codes are curbing their distribution.

Non-inverter production is consolidating in lower-cost countries as brands redeploy capacity toward high-value DC-motor lines. Component standardization narrows cost differences, making inverter paybacks attractive even in moderate-climate zones. Early mover advantages accrue to firms with proprietary drive electronics, enabling software tweaks that refine part-load performance and reduce acoustic signatures in premium residential towers.

By End-User: Commercial Applications Accelerate

The residential segment accounted for 64.12% of 2024 shipments, driven by urban middle-class households upgrading from fans and evaporative coolers. E-commerce promotions and installment financing sustain unit sales in Latin America and South Asia. The commercial segment, however, posts a 7.85% CAGR as offices, hotels, and retail complexes reopen and add IoT-ready VRF systems that support predictive maintenance contracts. Edge data centers in suburban locations further expand the market size for precision air handlers.

Industrial buyers demand 24-hour reliability; pharmaceutical plants and cold-storage depots require validated temperature mapping. Compliance with OSHA indoor air quality rules strengthens demand for higher fresh air ratios and advanced filtration. Vendors upsell services that guarantee uptime, bundling monitoring subscriptions into equipment leases. This service-oriented model boosts lifetime margins even if upfront hardware revenue moderates.

By Capacity: Large-Tonnage Systems Capture Growth

Units of ≤10 tons represented 38.97% of the 2024 volume, primarily favored in single-family homes and small shops. The midrange 11-18 ton categories are suitable for malls and mid-rise offices. Above-26-ton systems clock the fastest 8.01% CAGR as data halls and district cooling networks proliferate. These large units dominate the air conditioning equipment market share in new industrial parks, where central plants are replacing dispersed rooftop units for lower maintenance costs.

High-capacity orders often involve bespoke heat-exchanger geometries and multiple refrigeration circuits. Extended lead times give suppliers pricing power that partially offsets raw-material inflation. Energy-performance contracts tie payments to verified kilowatt-hour (kWh) savings, aligning OEM incentives with building owner targets. Standards such as ASHRAE 90.1 encourage designers to adopt magnetic-bearing chillers and adiabatic condensers, further differentiating premium lines.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Distribution Channel: Direct Engagement Rises in Complex Projects

Dealer and retail outlets still handled 42.12% of 2024 shipments, offering immediate stock and familiar warranties to homeowners. Yet direct sales into design-build contracting firms are rising at 7.58% CAGR. Large project stakeholders want early-stage modeling and lifecycle-cost analysis, roles that manufacturers can fulfill more effectively than resellers. Haier’s Thailand hub will focus on direct exports to regional EPC contractors once its 3 million-unit capacity is operational by 2027.

Online marketplaces grow in retrofit splits and portable units, offering transparent pricing and user reviews. Regulatory oversight requires licensed installers to finalize hookups, so click-to-ship models include installation vouchers. Some OEMs pilot subscription bundles that combine hardware, service, and energy-savings guarantees, potentially changing how the air conditioning equipment industry measures sales.

Geography Analysis

Asia-Pacific held 40.32% of 2024 revenue and is projected to advance at 8.43% CAGR through 2030, thanks to large housing programs and aggressive manufacturing expansion. Daikin’s new Indonesia plant cost Rp3.3 trillion (USD 211.5 million) and targets 1.5 million units annually, while Midea’s Cikarang factory required IDR 650 billion (USD 41.7 million) to reach 1 million units by 2026. Government subsidies for heat pumps and evolving building codes lift regional conversion rates from window units to inverter splits.

North America is a mature replacement market shaped by SEER2 standards and state-level electrification drives. Precision cooling for hyperscale campuses and office retrofits sustains volume, yet technician shortages stretch installation timelines. Energy-efficiency tax credits keep premium products competitive even as metal costs climb. Europe simultaneously pushes for refrigerant phase-downs and heat-pump adoption to meet climate-neutrality goals, thereby elevating unit value, although volume is sensitive to housing renovation funding.

The Middle East and Africa experience hot-climate-driven baseline demand; however, currency volatility and limited financing hinder the large-scale adoption of inverter systems. Gulf states invest in district cooling to reduce peak power loads, presenting opportunities for chiller suppliers. Latin America experiences mid-single-digit growth driven by urbanization in Brazil and Mexico, where energy-efficiency labeling has begun to sway consumer choices. Import tariffs protect local assemblers, prompting multinationals to scale regional plants.

Get Analysis on Important Geographic Markets

Download PDF

Competitive Landscape

The market remains moderately concentrated. Daikin, Carrier, Trane Technologies, and Mitsubishi Electric leverage proprietary compressor lines and long-standing dealer networks to defend share. Capacity expansions such as Mitsubishi Electric’s USD 143.5 million Kentucky factory and Daikin’s USD 121 million Tijuana site highlight a trend toward near-shore production that cushions forex swings and meets Buy-American preferences. Brand strategies converge on inverter technology, smart-connectivity ecosystems, and low-GWP refrigerant readiness.

Vertical integration extends from designing BLDC motors to owning cloud analytics platforms that manage fault detection. Service revenue grows as OEMs bundle extended warranties and subscription-based monitoring. Yet white-space entrants focusing on edge-AI diagnostics threaten to disintermediate repair networks. Established firms respond by acquiring minority stakes in software start-ups or entering into joint development agreements.

Raw-material price swings and logistics costs compress commodity-split margins, prompting incumbents to shift toward premium segments, such as data-center precision cooling and cold-chain equipment. Customized offerings fetch higher ASPs and lock customers into multi-year maintenance contracts. Competitive intensity also reflects environmental credentials, with top brands racing to declare net-zero operations and recyclable packaging, factors now appearing in government tenders.

Air Conditioning Equipment Industry Leaders

-

Daikin Industries, Ltd.

-

Bosch Thermotechnology GmbH

-

Mitsubishi Electric Corporation

-

LG Electronics Inc.

-

Carrier Global Corporation

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- December 2024: Mitsubishi Electric Corporation announced a USD 143.5 million investment to build twin-rotary variable-speed compressor capacity in Maysville, Kentucky, aimed at producing 1 million units annually from Oct 2027.

- December 2024: Daikin Industries Indonesia opened a full-scale air-conditioner plant in Cikarang after spending Rp3.3 trillion (USD 211.5 million), targeting 1.5 million units per year and 40% local content by 2025.

- November 2024: Midea Electronics Indonesia completed a new Cikarang AC factory with IDR 650 billion (USD 41.7 million) initial outlay, planning 1 million split and window units by 2026.

- September 2024: Haier committed THB 10 billion (USD 289.9 million) to establish a 3 million-unit facility in Thailand by 2027.

Global Air Conditioning Equipment Market Report Scope

Air conditioning equipment is designed to regulate temperatures and provide fresh air in rooms experiencing high temperatures and humidity, ensuring a comfortable indoor environment. The market study analyzes the trends and opportunities for different types of air conditioning equipment, including split systems, variable refrigerant flow, air handling units, chillers, fan coils, indoor packaged units, and rooftop units, used in various end-user industry applications. Furthermore, the study examines the influence of macroeconomic factors on the market.

The Air Conditioning Equipment Market Report is Segmented by Product Type (Split and Multi-split Systems, Variable Refrigerant Flow Systems, Packaged and Rooftop Units, and Chillers), Technology (Inverter Systems, and Non-inverter Systems), End-user (Residential, Commercial, and Industrial), Capacity (Up to 10 Tons, 11-18 Tons, 19-26 Tons, and Above 26 Tons), Distribution Channel (Direct Sales, Dealer/Retail Stores, and Online), and Geography (North America, South America, Europe, Asia-Pacific, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

By Product Type

| Split and Multi-split Systems |

| Variable Refrigerant Flow (VRF) Systems |

| Packaged and Rooftop Units |

| Chillers |

By Technology

| Inverter Systems |

| Non-inverter Systems |

By End-user

| Residential |

| Commercial |

| Industrial |

By Capacity (Tons of Refrigeration)

| Up to 10 Tons |

| 11 - 18 Tons |

| 19 - 26 Tons |

| Above 26 Tons |

By Distribution Channel

| Direct Sales |

| Dealer / Retail Stores |

| Online |

By Geography

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Nigeria | ||

| Rest of Africa | ||

| By Product Type | Split and Multi-split Systems | ||

| Variable Refrigerant Flow (VRF) Systems | |||

| Packaged and Rooftop Units | |||

| Chillers | |||

| By Technology | Inverter Systems | ||

| Non-inverter Systems | |||

| By End-user | Residential | ||

| Commercial | |||

| Industrial | |||

| By Capacity (Tons of Refrigeration) | Up to 10 Tons | ||

| 11 - 18 Tons | |||

| 19 - 26 Tons | |||

| Above 26 Tons | |||

| By Distribution Channel | Direct Sales | ||

| Dealer / Retail Stores | |||

| Online | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| France | |||

| United Kingdom | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Nigeria | |||

| Rest of Africa | |||

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

How large is the air conditioning equipment market in 2025?

It stands at USD 125.71 billion, with a projected rise to USD 162.9 billion by 2030.

What is driving demand for VRF systems?

Commercial building retrofits and energy-efficiency codes push VRF adoption, resulting in a 6.73% CAGR through 2030.

Which region is growing fastest?

Asia-Pacific leads with an 8.43% CAGR, fueled by urbanization and local manufacturing expansions.

Why are inverter compressors gaining share?

Variable-speed operation lowers energy use by up to 50% and meets tighter SEER2 and F-Gas regulations.

What challenges does the industry face?

Technician shortages and high upfront costs restrict installation capacity and slow uptake of premium systems.

How will refrigerant phase-downs impact equipment choices?

Regulations favor low-GWP refrigerants like R-32 and R-454B, accelerating replacement of legacy R-410A units.

Page last updated on: