Air Ambulance Service Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

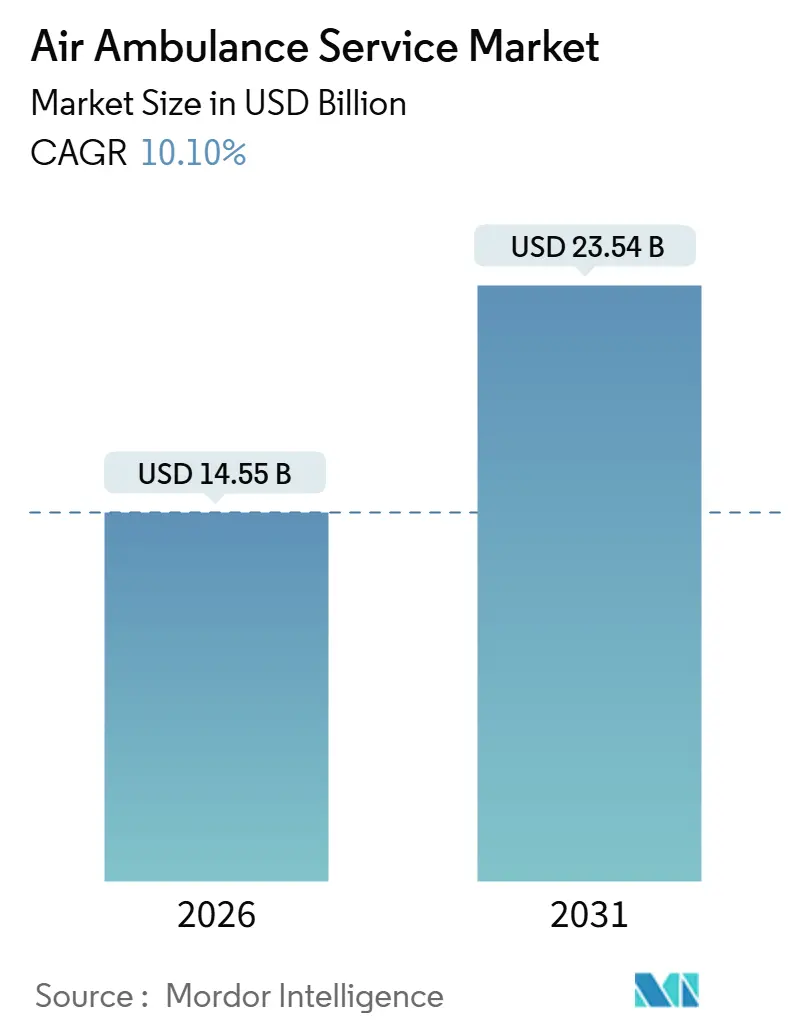

| Market Size (2026) | USD 14.55 Billion |

| Market Size (2031) | USD 23.54 Billion |

| Growth Rate (2026 - 2031) | 10.10% CAGR |

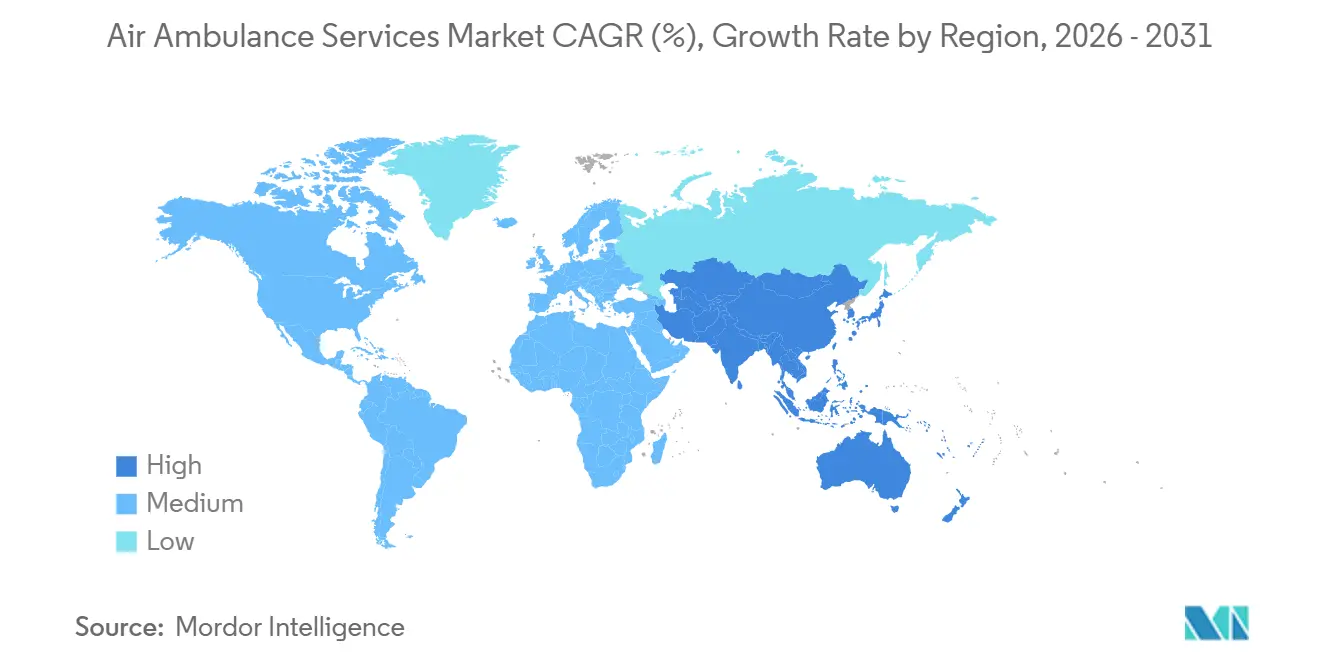

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

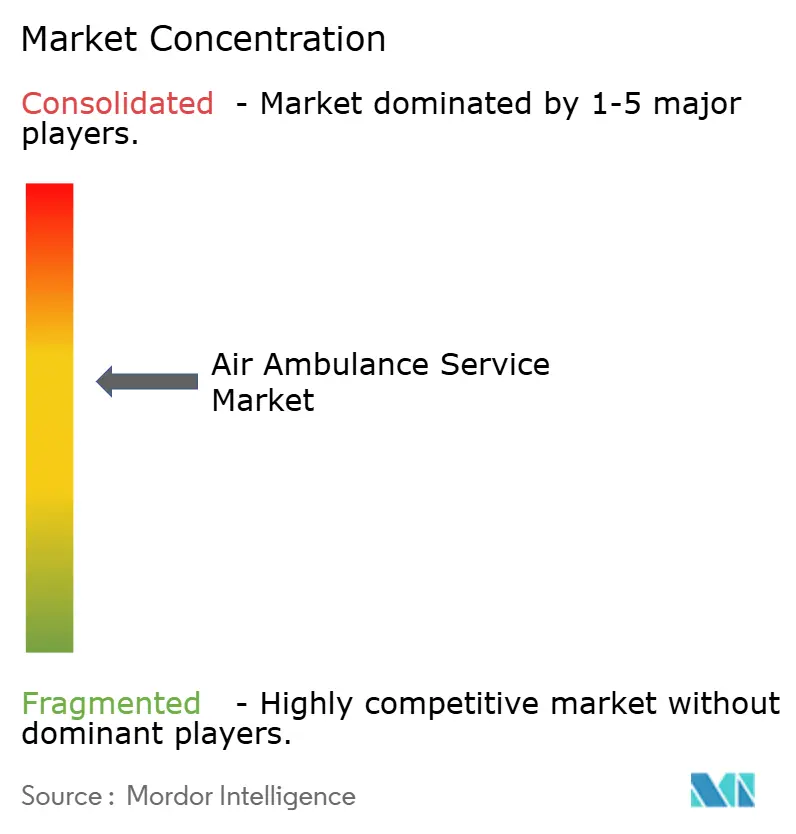

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Air Ambulance Service Market Analysis by Mordor Intelligence

The air ambulance service market is expected to grow from USD 14.55 billion in 2026 to USD 23.54 billion by 2031, registering a CAGR of 10.10%. This growth is driven by the increasing need for rapid transport in cardiovascular and trauma emergencies, improved insurance reimbursements under the No Surprises Act, and the expansion of integrated health systems establishing in-house fleets to retain high-acuity cases within their networks. Fleet modernization is progressing as operators invest in IFR-capable helicopters and explore electric vertical takeoff and landing (eVTOL) aircraft, which can reduce per-flight costs by up to 50%. Government initiatives, such as the USD 50 billion CMS Rural Health Transformation program, are enhancing cash flow for low-volume routes, while AI-based dispatch tools are enabling quicker launches and better asset utilization. Although competitive intensity remains moderate, recent trends in debt refinancing and market consolidation indicate that achieving scale is increasingly critical to manage high operating costs effectively.

Key Report Takeaways

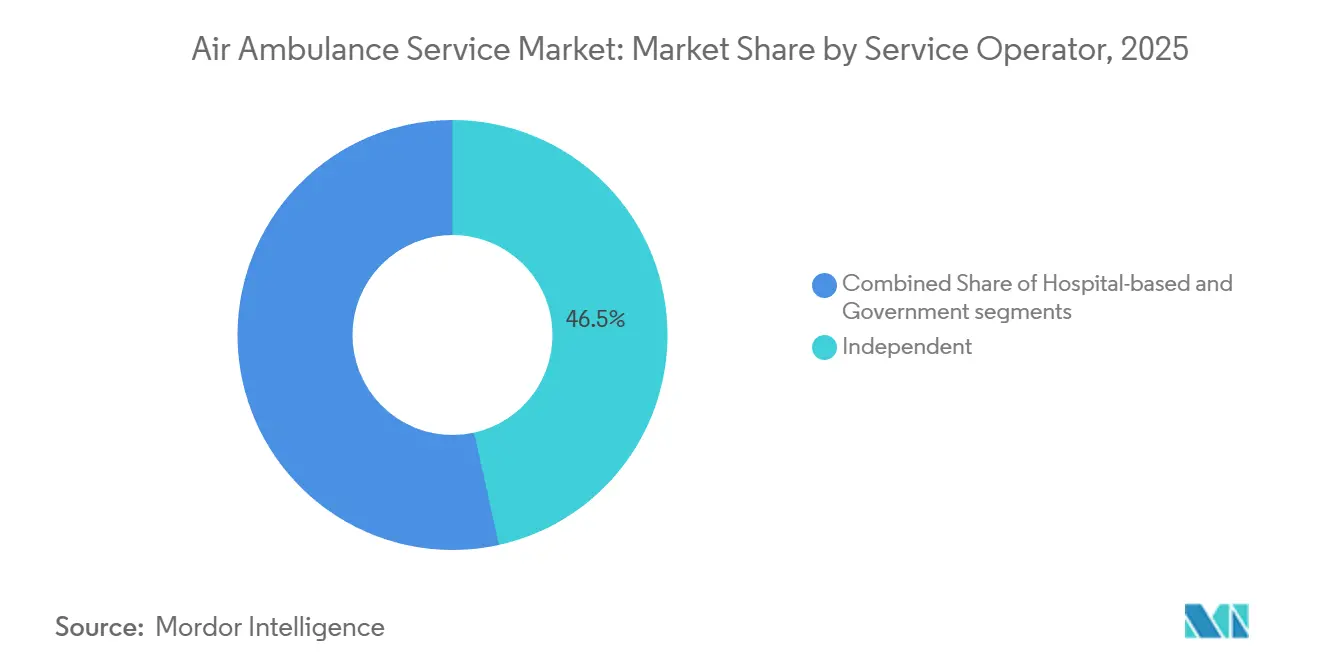

- By service operator, independent operators held 46.53% of the air ambulance service market share in 2025, while hospital-based models are forecasted to grow at the fastest rate, with a 11.89% CAGR through 2031.

- By aircraft type, fixed-wing platforms led the air ambulance service market, accounting for 53.59% of the market size in 2025; rotary-wing units are expanding at a 10.68% CAGR, driven by the implementation of IFR upgrades.

- By service type, domestic missions accounted for 58.49% of global revenue in 2025; international repatriation is poised to accelerate at a 12.01% CAGR to 2031.

- By geography, North America accounted for 38.9% of the 2025 revenue, while the Asia-Pacific region is projected to record the highest CAGR at 11.95% over the forecast horizon.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Air Ambulance Service Market Trends and Insights

Drivers Impact Analysis

| Driver | (%) Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing prevalence of cardiovascular and trauma emergencies | +1.8% | Global with higher impact in aging populations of North America and Europe | Medium term (2-4 years) |

| Expansion of private medical insurance coverage | +1.5% | Asia-Pacific core, spill-over to South America | Medium term (2-4 years) |

| Government subsidies for rural critical-care access | +1.2% | North America and Australia, emerging in India and Brazil | Long term (≥ 4 years) |

| eVTOL integration accelerating rapid response times | +0.9% | North America and EU pilot programs, expanding globally | Long term (≥ 4 years) |

| Cross-border tele-ICU network partnerships | +0.7% | Europe and North America, expanding to Asia-Pacific | Medium term (2-4 years) |

| AI-driven flight-route optimization reducing response time | +0.6% | Global with early adoption in developed markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Growing Prevalence of Cardiovascular and Trauma Emergencies

Cardiac and trauma cases account for the majority of helicopter emergency medical service missions, with 385,366 patients transported in 2023, primarily for these conditions.[1]Federal Aviation Administration, “FAA Reauthorization Act of 2024,” faa.gov Survival rates for rural cardiac arrest are 30% lower than urban averages, making reduced transport times critical. Air transport can cut travel time from 60 minutes by ground to 15 minutes by air, significantly improving outcomes. In England, helicopters achieved a median cardiac arrest response time of 19 minutes, compared to 28 minutes for ground units, resulting in an increase in return-of-spontaneous-circulation rates. Peer-reviewed studies indicate a 12% reduction in mortality when trauma patients are transported by air instead of ground. Aging populations in developed regions are expected to sustain demand through 2031.

Expansion of Private Medical Insurance Coverage

The No Surprises Act, effective January 2022, reduced balance billing, lowering out-of-pocket costs for patients and enabling more covered air ambulance flights. In 2024, CMS introduced the Air Ambulance Data Collection program, enhancing cost transparency for payers and operators. Major insurers, including UnitedHealthcare, Cigna, Anthem, and Blue Cross Blue Shield, now provide clear clinical criteria for flight authorization, covering conditions such as hemodynamic instability and airway compromise. A 50% Medicare rural add-on payment further supports operator economics in frontier areas. Upcoming standards from the CMS–DOT advisory committee are expected to improve reimbursement predictability.

Government Subsidies for Rural Critical-care Access

In 2022, federal grants totaling USD 42.90 million supported rural providers in building helipads and acquiring necessary equipment. The FY2026 budget allocates USD 50 billion over five years to enhance emergency coverage in underserved US counties. Additional grant programs from the US Department of Agriculture provide funding for helipads and crew training. Similar initiatives in Saudi Arabia funded seven helicopters around Mecca to serve 2 million Hajj pilgrims in 2024. These subsidies enable carriers to maintain operations on low-volume routes that would otherwise be unprofitable.

eVTOL Integration Accelerating Rapid Response Times

Archer Aviation and the Cleveland Clinic plan to introduce eVTOL medical flights by 2025, offering five-minute dispatch times for 50-mile missions. Beta Technologies is testing battery-powered aircraft with Air Methods to validate endurance and payload capabilities. Eve Air Mobility and Joby Aviation are progressing toward FAA approvals, potentially opening North American corridors by 2027. Electric propulsion reduces fuel and maintenance costs while adhering to strict urban noise regulations.

Restraints Impact Analysis

| Restraint | (%) Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High operating and maintenance costs | -1.3% | Global with higher impact in cost-sensitive emerging markets | Short term (≤ 2 years) |

| Shortage of trained aero-medical professionals | -1.1% | North America and Europe, expanding to Asia-Pacific | Medium term (2-4 years) |

| Stringent aviation regulatory approvals | -0.8% | Global with varying intensity by jurisdiction | Long term (≥ 4 years) |

| Spectrum congestion hampering in-flight telemedicine | -0.5% | Urban areas globally, particularly dense metropolitan regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Operating and Maintenance Costs

Annual helicopter operating costs range from USD 2.9 million to USD 6.5 million, with fuel expenses accounting for up to 35% of the total operating costs.[2]Journal of Emergency Medical Services, “Air Ambulance Operating Costs Analysis,” jems.com Turbine overhauls can exceed USD 500,000, while rising insurance premiums and multi-crew staffing further increase costs. Low-volume rural bases struggle to achieve economies of scale, prompting smaller providers to consider consolidation or exit from the market.

Shortage of Trained Aero-medical Professionals

Employment growth for EMTs and paramedics is projected at only 5% through 2033, falling short of the expected double-digit growth in air ambulance missions.[3]U.S. Bureau of Labor Statistics, “EMT and Paramedic Employment Projections,” bls.gov Flight crews require specialized certifications, such as critical-care paramedic and advanced airway management, as well as 2,000 flight hours for pilots, limiting the candidate pool. While earn-while-you-learn programs have been introduced, significant workforce relief is not expected for another three to five years.

Segment Analysis

By Service Operator: Hospital Systems Deepen Integration

Hospital systems represent the fastest-growing segment in the air ambulance service market, with an expected CAGR of 11.89%. This growth is driven by their ability to transport high-acuity cases directly to owned intensive-care units, ensuring downstream revenue. The Cleveland Clinic–Archer eVTOL project exemplifies this approach. Independent operators, while maintaining a projected 46.53% market share by 2025, face challenges such as rising fuel costs, labor expenses, and negotiations with payers. Global Medical Response’s USD 5.4 billion refinancing positions it to expand into underserved rural areas where hospital-operated fleets are absent. Government-run services, such as Australia’s Royal Flying Doctor Service, address service gaps with taxpayer funding, shielding them from fluctuations in reimbursement.

Hospital ownership facilitates cross-functional scheduling, data sharing, and the negotiation of bundled payment contracts with insurers, thereby reducing per-patient transport costs. Independent operators, such as GMR with its 387 US bases, offer extensive geographic coverage but are more vulnerable to regulatory and fuel price changes. Air Methods’ 2023 restructuring, which reduced USD 1 billion in debt, highlights the financial challenges faced by standalone operators. Looking ahead, hybrid joint ventures where hospitals take minority stakes in established operators could combine financial stability with operational expertise, reshaping competition in the air ambulance service market.

Note: Segment shares of all individual segments available upon report purchase

By Aircraft Type: Helicopters Close the Gap

Fixed-wing aircraft are projected to account for 53.59% of 2025 revenue, driven by their suitability for long-haul repatriation and pressurized cabins capable of carrying ECMO or incubators on intercontinental routes. This segment benefited significantly from the post-pandemic rebound in international volumes. However, rotary-wing aircraft are expected to grow at a 10.68% CAGR, supported by the introduction of IFR-capable models like the Bell 407GXi and Bell 429, which enhance operational capabilities in adverse weather conditions. Airbus’ H140 order from STAT MedEvac further reflects demand for helicopters with quiet, spacious cabins.

Helicopters remain critical for scene pickups and rooftop landings, particularly within 150-mile radii of level-I trauma centers. Fixed-wing operators are modernizing their fleets with Pilatus PC-24 jets and King Air 350i turboprops to improve fuel efficiency. The emergence of eVTOL aircraft is expected to impact short-haul helicopter missions while complementing fixed-wing operations on longer routes. Overall, rotary-wing aircraft are anticipated to continue narrowing the market share gap with fixed-wing aircraft through 2031.

By Service Type: International Travel Accelerates

Domestic flights are projected to account for 58.49% of 2025 revenue, but international repatriation services are expected to grow at a faster CAGR of 12.01%. This growth is driven by increasing demand for bedside-to-bedside transfers from medical tourism and expatriate communities. Partnerships like International SOS and SAF Aerogroup’s tele-ICU initiative reduce the need for onboard physicians, lowering costs and expanding accessibility. Transatlantic ICU jet services start at approximately USD 25,000, with providers like Brasil Vida and AirMed offering global coverage that reassures insurers.

Domestic growth is expected to moderate as expanded ground EMS capabilities absorb some short-haul transfers, and payer scrutiny limits reimbursement increases. However, rural areas with challenging topography and long travel times ensure the continued necessity of air transport. Consequently, international routes are poised to contribute significantly to incremental revenue, prompting operators to strategically position aircraft in hubs such as Dubai, Singapore, and Miami to support the growing demand in the air ambulance service market.

Geography Analysis

North America is expected to generate 38.9% of global sales in 2025, supported by Medicare’s 50% rural add-on and the No Surprises Act, which simplifies payer settlements. GMR’s extensive network of 387 bases across all 50 states, combined with its commitment to acquiring 53 new aircraft, strengthens its domestic presence. In Canada, provincial programs like Ornge ensure coverage in remote northern regions. Mexico, however, remains underserved, presenting opportunities for new entrants willing to navigate regulatory challenges.

The Asia-Pacific region is projected to achieve the fastest CAGR of 11.95% through 2031, driven by the liberalization of helicopter EMS in China and India. Japan’s Doctor Helicopter system serves as a model for public-private collaboration, while Saudi Arabia’s Mecca fleet demonstrates targeted government investment to address episodic demand surges. Dubai’s strategic positioning as a hub for Eurasian medical tourism further enhances the region’s growth potential.

In Europe, state-funded HEMS programs, such as Germany’s DRF network with 52 helicopters, coexist with charity-funded operations in the UK, France, Turkey, and South Africa, which also contribute to the regional landscape. In Africa, political instability and low insurance penetration limit the expansion of the broader market. However, niche opportunities exist in sectors such as mining, oil, and safari tourism, which require critical-care transport services.

Competitive Landscape

The air ambulance service market exhibits moderate concentration, with the top three US carriers, GMR, Air Methods, and PHI Health, dominating domestic operations. However, the European and Asia-Pacific markets remain fragmented. GMR leverages its scale to negotiate insurance contracts and invest in AI-driven dispatch systems and tele-ICU retrofits, illustrating how larger players can benefit from technological advancements. Following its restructuring, Air Methods has reduced its operational footprint, creating opportunities for competitors to enter its former markets. Additionally, Toll Group’s planned 2024 acquisition of Pel-Air’s fixed-wing assets highlights the growing interest of logistics companies in aeromedical transport as a complementary service.

eVTOL manufacturers are forming joint ventures with hospital systems, introducing new competition and reducing entry barriers in urban areas. Accreditation from the Commission on Accreditation of Medical Transport Systems has become essential for securing premium contracts, prompting smaller operators to either invest in upgrades or pursue mergers. Regulatory changes under the FAA and CMS quality committees favor companies capable of funding advanced avionics, safety systems, and evidence-based clinical protocols. Overall, strategic alliances, refinancing efforts, and technological advancements are expected to continue reshaping the air ambulance service market through 2031.

Air Ambulance Service Industry Leaders

Air Methods Corporation

Global Medical Response, Inc.

PHI Health, LLC

REVA Inc.

Avincis Aviation Group, S.A.U.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: International SOS and SAF Aerogroup formed a strategic alliance to incorporate tele-ICU capabilities into their intercontinental air ambulance services. This collaboration allows ground-based critical care specialists to deliver real-time clinical oversight during long-distance medical transport, aiming to reduce costs and clinical risks for corporate clients and insurers.

- March 2025: Global Medical Response entered into an agreement with Airbus for the procurement of up to 15 H140 helicopters for emergency medical services, including 10 firm orders and five optional units.

- November 2024: Global Medical Response placed an order for 28 Airbus helicopters, comprising H125s, H130s, H135s, and H145s, to enhance its North American fleet, which currently includes nearly 200 Airbus rotorcraft.

- June 2024: Med-Trans Corporation and Med-Force Aeromedical Transport collaborated to expand 24/7 H135 and EC135 helicopter coverage in the Quad Cities region.

- February 2024: DRF Luftrettung placed an order for up to 10 additional Airbus H145 helicopters, with seven firm orders and three optional units, to strengthen its life-saving fleet across multiple European countries.

Global Air Ambulance Service Market Report Scope

Air ambulances are a special type of aircraft designed to provide emergency medical services to patients. They include rotary-wing and fixed-wing aircraft equipped with medical facilities designed to provide medical services in remote areas where land-based ambulance services are not easily available.

The air ambulance service market is segmented by service operator, aircraft type, service type, and geography. By service operator, the market is segmented into hospital-based, independent, and government. By aircraft type, the market is segmented into fixed-wing and rotary-wing. By service type, the market is categorized into domestic and international services. The report also covers the market sizes and forecasts for the air ambulance service market in major countries across different regions. For each segment, the market size is provided in terms of value (USD).

| Hospital-based |

| Independent |

| Government |

| Fixed-Wing |

| Rotary-Wing |

| Domestic |

| International |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| France | ||

| Germany | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Rest of South America | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Africa | South Africa | |

| Egypt | ||

| By Service Operator | Hospital-based | ||

| Independent | |||

| Government | |||

| By Aircraft Type | Fixed-Wing | ||

| Rotary-Wing | |||

| By Service Type | Domestic | ||

| International | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | United Kingdom | ||

| France | |||

| Germany | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Rest of South America | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Africa | South Africa | ||

| Egypt | |||

Key Questions Answered in the Report

How large is the air ambulance service market in 2026?

The air ambulance service market stands at USD 14.55 billion and is set to grow at a 10.10% CAGR to 2031.

Which aircraft type dominates current revenue?

Fixed-wing aircraft hold 53.59% of 2025 revenue because of their role in long-distance repatriation.

What region will grow fastest through 2031?

Asia-Pacific is forecasted to post an 11.95% CAGR thanks to helicopter EMS rollouts in China and India.

Why are hospital systems investing in their own fleets?

They aim to keep high-acuity cases inside their networks, generating inpatient revenue while improving clinical continuity.

How will eVTOL technology affect air medical transport?

EVTOL aircraft should cut per-flight operating costs by up to 50%, enabling rapid urban response with less noise.

What is the key restraint facing operators today?

High operating costs, USD 2.9 million to USD 6.5 million per helicopter per year, press margins, especially on low-volume rural routes.