| Study Period | 2019 - 2030 |

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

| CAGR | 11.70 % |

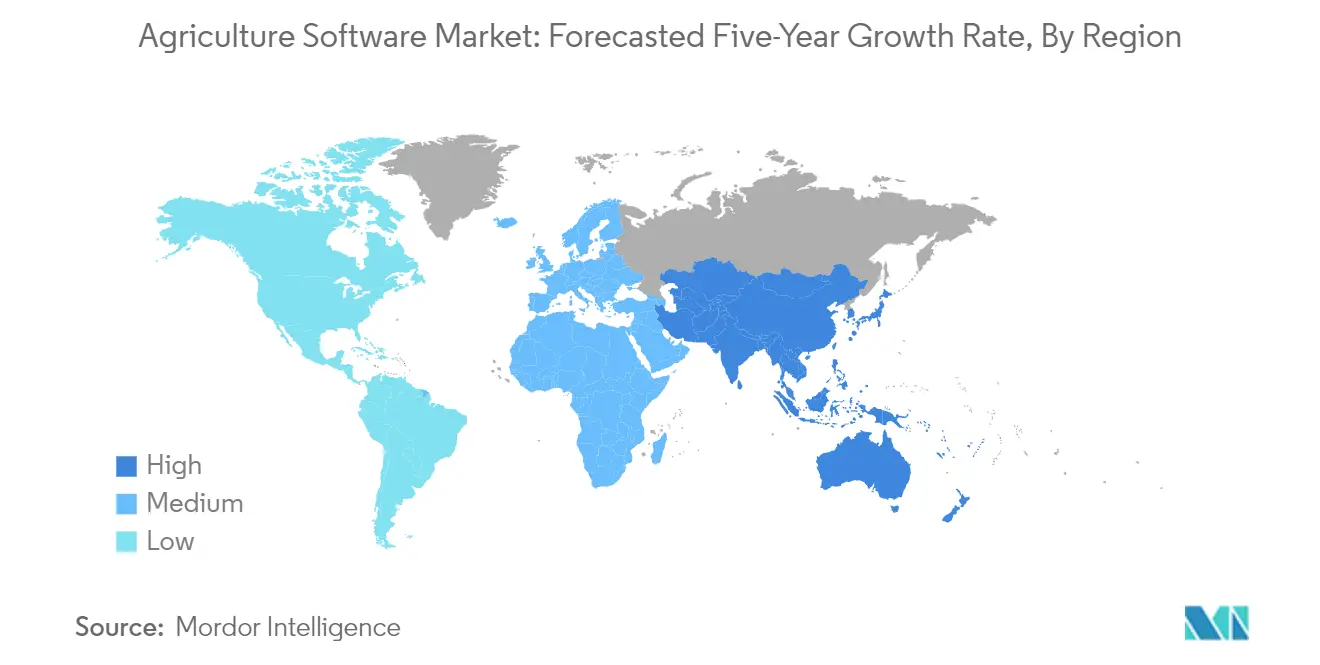

| Fastest Growing Market | North America |

| Largest Market | Asia Pacific |

| Market Concentration | Low |

Major Players*Disclaimer: Major Players sorted in no particular order |

Agriculture Software Market Analysis

The Agriculture Software Market is expected to register a CAGR of 11.7% during the forecast period.

The agricultural software industry is experiencing transformative changes driven by global macroeconomic factors and technological advancement. The United Nations estimates that the world's population will reach 9.6 billion by 2050, creating unprecedented pressure on agricultural systems to increase food production efficiency. This demographic shift, coupled with rapid urbanization and climate change challenges, has accelerated the adoption of digital solutions in farming practices. The Food and Agriculture Organization (FAO) emphasizes that food production must double between 2014 and 2050 to meet growing demand, highlighting the critical need for technological intervention in agricultural practices.

The integration of advanced technologies such as artificial intelligence, the Internet of Things, and cloud computing is revolutionizing traditional farming methods. Agricultural exports have shown remarkable growth, with the United States reaching USD 196.4 billion in 2022, demonstrating the sector's increasing reliance on agricultural technology-driven solutions. The emergence of precision farming techniques, incorporating data analytics and automated systems, has enabled farmers to optimize resource utilization and improve crop yields. These technological advancements are particularly evident in the rising adoption of smart greenhouse systems and vertical farming solutions, which address the challenges of limited arable land and climate variability.

The digital transformation of agriculture is reflected in the growing online agricultural commerce sector. In China, online sales of farm products increased by 9.2% year-over-year to CNY 531.38 billion (approximately USD 78.58 billion) in 2022, indicating a significant shift towards digital platforms in agricultural trade. This digital revolution extends beyond mere commerce, encompassing farm management systems, crop monitoring solutions, and precision agriculture tools. The integration of digital farming software and agriculture data management solutions has enabled real-time data management and decision-making capabilities, fundamentally changing how farmers approach crop planning and resource allocation.

The industry is witnessing a notable trend towards sustainable and precision agriculture practices. According to a survey by the Brazilian Association of Precision and Digital Agriculture (AsBraAP), the adoption rate of precision agriculture reached 66% for cotton and 34% for soy cultivation in Brazil, highlighting the growing acceptance of technology-driven farming methods. This shift towards precision farming is characterized by the implementation of sophisticated smart farming software solutions that enable precise monitoring of soil conditions, weather patterns, and crop health. The trend is further supported by the increasing deployment of autonomous systems and smart sensors, which provide farmers with actionable insights for optimizing agricultural operations while minimizing environmental impact.

Agriculture Software Market Trends

Growing Adoption of Smart Greenhouse and Precision Farming Technologies

The increasing integration of Internet of Things (IoT) and advanced sensor technologies in agricultural operations is driving significant demand for precision agriculture software solutions. Smart greenhouse systems are being equipped with sophisticated sensor networks that monitor crucial parameters including light, humidity, temperature, and soil moisture, enabling automated irrigation systems and precise environmental control. This technological advancement is exemplified by recent developments such as the December 2022 partnership between Astrocast and Avirtech, where satellite IoT network solutions were integrated into farm control systems to enhance monitoring capabilities and reduce operational costs.

The adoption of precision farming technologies has been accelerated by the integration of multiple data sources, including GPS, satellite imagery, and internet-connected devices. These technologies enable farmers to implement data-driven decision-making processes for optimal resource utilization and improved crop yields. For instance, in February 2023, University of Georgia researchers developed an internet-connected greenhouse lighting system that demonstrated potential electricity savings of up to 33% through predictive lighting control systems, highlighting the tangible benefits of smart agricultural technologies.

Understand The Key Trends Shaping This Market

Download PDF

Government Support and Investments in Agricultural Technology

Government initiatives and investments are playing a crucial role in accelerating the adoption of farm management software solutions across various regions. This is evidenced by significant funding allocations, such as the May 2023 investment of USD 8 million by the U.S. Department of Agriculture (USDA) in four collaborations focused on soil carbon measurement and monitoring on working agricultural lands. These investments demonstrate the growing governmental focus on leveraging technology to enhance agricultural productivity while promoting sustainable practices.

The support extends beyond direct funding to include policy frameworks and research programs that encourage technological adoption in agriculture. For instance, in March 2023, the National Institute of Food and Agriculture (NIFA) of the USDA announced a USD 70 million investment in sustainable agriculture programs that combine Extension, research, and educational activities. These initiatives are designed to establish robust, adaptable, and climate-smart food and agricultural systems, creating a favorable environment for the adoption of agricultural software solutions.

Rising Need for Resource Optimization and Sustainable Agriculture

The agricultural sector faces mounting pressure to optimize resource utilization while maintaining productivity, particularly in water management and soil health. Agriculture resource management software solutions are becoming essential tools in addressing these challenges by enabling precise monitoring and control of resource usage. These systems provide real-time data analytics and automated control mechanisms that help farmers implement more efficient irrigation practices and optimize input utilization, leading to significant resource savings while maintaining or improving crop yields.

The focus on sustainable agriculture practices has intensified with the growing emphasis on climate-smart farming techniques. Software solutions are increasingly being integrated with advanced monitoring systems to track and optimize various environmental parameters. For example, in February 2023, the Department of Science and Technology (DOST 4-A) of the Philippines collaborated with Bukidamara Agri Farm to implement automated systems for drip irrigation, climate monitoring, and nutritional solution dosing, demonstrating the global push towards resource-efficient farming practices through technology adoption.

Cloud Computing and Data Management Requirements

The agricultural sector's growing reliance on data-driven decision-making has elevated the importance of robust cloud computing and data management solutions. Cloud-based farm management software offers enhanced reliability, accessibility, and scalability, enabling farmers to access and analyze critical farm data from any location. These solutions facilitate real-time monitoring of field conditions, crop health, and environmental parameters, allowing for immediate response to changing conditions and potential issues.

The integration of advanced analytics and artificial intelligence capabilities in cloud-based agricultural software is transforming farm management practices. These systems can process vast amounts of data from multiple sources, including IoT sensors, weather stations, and satellite imagery, to provide actionable insights for farm operations. The software's ability to deliver automated alerts and recommendations for any detected anomalies in smart greenhouses or field conditions has become particularly valuable for modern farming operations, enabling proactive management and improved operational efficiency.

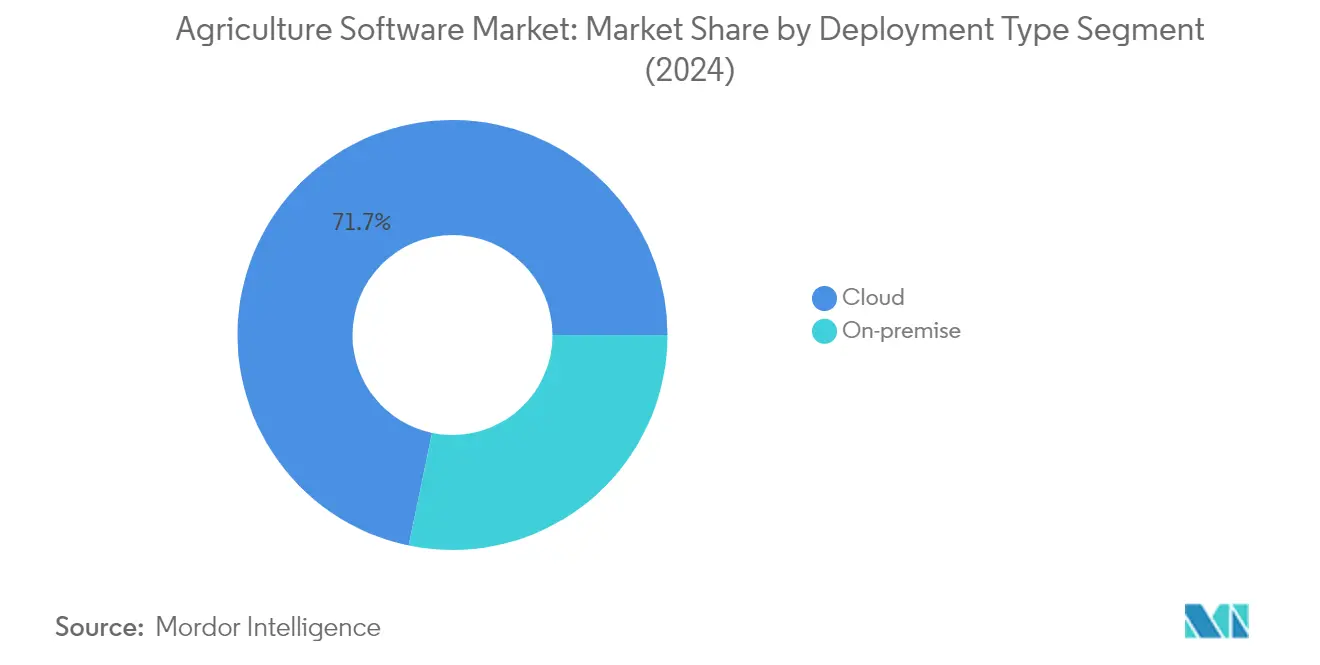

Segment Analysis: By Deployment Type

Cloud Segment in Agriculture Software Market

The cloud segment has emerged as the dominant force in the agriculture software market, commanding approximately 72% of the total market share in 2024. This substantial market presence is driven by the widespread adoption of cloud-based solutions in precision farming and smart greenhouse applications. The segment's growth is fueled by several key advantages, including enhanced data management capabilities, real-time monitoring features, and seamless integration with IoT devices in agricultural operations. Cloud-based agriculture software solutions, particularly Software-as-a-Service (SaaS) and Platform-as-a-Service (PaaS) offerings, are witnessing increased adoption due to their scalability, cost-effectiveness, and ability to provide remote access to critical farming data. The segment is experiencing robust growth with a projected growth rate of nearly 13% from 2024 to 2029, driven by the increasing demand for real-time data management through cloud computing and the strengthening of intellectual property protections for agricultural discoveries. The integration of advanced technologies such as AI and machine learning in cloud-based agricultural solutions is further accelerating market expansion, enabling farmers to make data-driven decisions and optimize their agricultural operations effectively. The adoption of farm management software in cloud platforms is enhancing the overall efficiency of agricultural practices.

On-premise Segment in Agriculture Software Market

The on-premise segment continues to maintain its significance in the agriculture software market, particularly among organizations that prioritize data security and direct control over their agricultural software systems. This deployment type offers farmers and agricultural enterprises greater customization capabilities and enhanced control over their data and software configuration. On-premise solutions provide more reliability and performance for farm operations as they don't depend on internet connectivity or bandwidth availability. These solutions are particularly valuable in regions with limited internet infrastructure or where data sovereignty is a crucial concern. The segment is witnessing steady adoption among large-scale agricultural operations and enterprises that require specialized customization and integration with existing on-premise systems. The ability to implement personalized backup and recovery plans, coupled with the option to optimize software performance using local hardware and network resources, continues to drive the adoption of on-premise solutions in specific agricultural scenarios. The use of agriculture ERP systems in on-premise deployments ensures comprehensive management of farm resources and operations.

Segment Analysis: By Application

Precision Farming Segment in Agriculture Software Market

Precision farming dominates the agriculture software market, commanding approximately 91% market share in 2024, driven by the increasing adoption of data-driven agricultural practices worldwide. This segment leverages various technologies, including GPS guidance systems, remote sensing, and variable rate technology, to optimize farming operations. The widespread adoption is primarily attributed to its ability to help farmers make data-driven decisions, improve resource efficiency, reduce costs, and increase yields through sophisticated analytics and real-time monitoring capabilities. The segment's dominance is further strengthened by the integration of artificial intelligence and machine learning algorithms that provide predictive insights for crop management, pest control, and resource optimization. The growing focus on sustainable agriculture practices and the need for efficient resource utilization has made precision farming software an essential tool for modern agricultural operations. The use of crop management software is pivotal in enhancing the precision farming approach, allowing for better yield predictions and resource allocation.

Smart Greenhouse Segment in Agriculture Software Market

The smart greenhouse segment is emerging as the fastest-growing application in the agriculture software market, with an expected growth rate of approximately 17% during 2024-2029. This remarkable growth is driven by the increasing need for controlled environment agriculture and year-round crop production capabilities. Smart greenhouse software solutions are revolutionizing traditional greenhouse operations by incorporating advanced sensors, automation systems, and data analytics to optimize temperature, humidity, lighting, and irrigation parameters. The segment's growth is further accelerated by the rising adoption of IoT-based monitoring systems and climate control technologies that enable precise microclimate management. The integration of cloud computing and mobile technologies has made these solutions more accessible and user-friendly, allowing farmers to monitor and control their greenhouse operations remotely while ensuring optimal growing conditions for high-value crops. The implementation of farm planning software in smart greenhouses aids in strategic planning and resource management, ensuring maximum productivity.

Agriculture Software Market Geography Segment Analysis

Agriculture Software Market in North America

North America represents a dominant force in the global agriculture software market, driven by extensive adoption of advanced farming technologies and strong government support for agricultural digitization. The United States and Canada form the key markets in this region, with both countries showing significant momentum in precision farming and smart greenhouse applications. The region's leadership is attributed to its robust technological infrastructure, high awareness of digital farming solutions, and substantial investments in agricultural innovation. The presence of major agriculture software companies and extensive research and development activities further strengthens North America's position in the global market.

Agriculture Software Market in United States

The United States stands as the largest market for agri software in North America, commanding approximately 87% of the regional market share in 2024. The country's dominance is driven by its extensive agricultural land, sophisticated farming practices, and strong emphasis on technological innovation in agriculture. The US market is characterized by widespread adoption of precision farming techniques, particularly in large-scale farming operations. The country's robust agricultural exports and strong focus on increasing rural economies through technological advancement continue to drive market growth. The integration of advanced technologies such as GPS, satellite imagery, and internet-connected devices in farming practices has become increasingly common among American farmers.

Agriculture Software Market in Canada

Canada emerges as the fastest-growing market in North America, with a projected growth rate of approximately 15% during 2024-2029. The country's remarkable growth is fueled by increasing government efforts to boost precision farming and a growing trend toward sustainable agricultural practices. Canadian farmers are increasingly embracing sophisticated analytics and monitoring systems to manage their operations with high precision. The country's agriculture sector is actively addressing challenges such as farmer and labor shortages through increased investment in technology and automation. Cloud-based farm software solutions are gaining particular traction in Canada, offering enhanced reliability, flexibility, and scalability for both large agribusinesses and small-to-medium farmers.

Agriculture Software Market in Europe

Europe represents a significant market for ag software, characterized by strong technological adoption and innovative farming practices. The region's market is primarily driven by countries like Germany, France, and the United Kingdom, each contributing significantly to the overall market dynamics. European farmers are increasingly embracing digital solutions to enhance productivity and sustainability in agricultural operations. The region's focus on sustainable farming practices and environmental conservation has been a key driver for the adoption of advanced agricultural technologies. The European Union's Common Agricultural Policy (CAP) continues to play a crucial role in promoting the digitalization of farming practices across member states.

Agriculture Software Market in Germany

Germany leads the European agtech software market, holding approximately 24% of the regional market share in 2024. The country's leadership position is supported by its strong agricultural sector, which ranks among the four largest producers in the European Union. German farmers are actively embracing modern production practices and new technologies, particularly in precision farming applications. The country's emphasis on sustainable farming practices and environmental protection has led to increased adoption of digital solutions in agriculture. The presence of major agricultural technology companies and strong research institutions further strengthens Germany's position in the market.

Agriculture Software Market in United Kingdom

The United Kingdom demonstrates significant growth potential in the agriculture software market, with a projected growth rate of approximately 13% during 2024-2029. The country's agricultural sector is undergoing a significant transformation driven by the adoption of renewable technology and digital solutions. British farmers are increasingly embracing precision farming techniques and smart greenhouse technologies to optimize their operations and achieve better agronomic results. The UK's commitment to achieving net-zero emissions in agriculture has been a key driver for the adoption of digital farming solutions. The country's focus on innovation and development across the AgTech industry continues to create new opportunities for market growth.

Agriculture Software Market in Asia Pacific

The Asia Pacific region represents a rapidly evolving market for agriculture software, characterized by diverse agricultural practices and increasing technological adoption. Countries like China, Australia and New Zealand, and Thailand are at the forefront of agricultural innovation in the region. The market is driven by the growing need to enhance agricultural productivity, address food security concerns, and promote sustainable farming practices. Government initiatives supporting agricultural modernization and digital transformation are playing a crucial role in market development across the region.

Agriculture Software Market in Australia and New Zealand

Australia and New Zealand together represent the largest market for farm software in the Asia Pacific region. These countries have demonstrated strong adoption of advanced farming technologies, particularly in precision agriculture and farm management systems. The agricultural sector in these countries is characterized by large-scale farming operations and a strong focus on export-oriented production. The adoption of cloud-based farm management solutions and precision farming technologies has been particularly strong, driven by the need to optimize resource utilization and improve productivity.

Agriculture Software Market in China

China emerges as one of the fastest-growing markets in the Asia Pacific region for ag software solutions. The country's agricultural sector is undergoing rapid modernization with increasing adoption of digital technologies and smart farming practices. The Chinese government's strong support for agricultural technology innovation and modernization has been a key driver for market growth. The focus on improving agricultural productivity while ensuring sustainable practices has led to increased adoption of precision farming and smart greenhouse technologies across the country.

Agriculture Software Market in Latin America

Latin America represents a growing market for agriculture software solutions, with Brazil, Mexico, and Argentina emerging as key markets in the region. Brazil stands as the largest market in the region, while Argentina shows the fastest growth potential. The region's agricultural sector is characterized by large-scale farming operations and increasing adoption of precision farming techniques. Government initiatives supporting agricultural modernization and the need to enhance productivity while ensuring sustainable practices are driving market growth. The adoption of cloud-based solutions and precision farming technologies is particularly strong among large agricultural enterprises in the region.

Agriculture Software Market in Middle East & Africa

The Middle East & Africa region presents unique opportunities in the agriculture software market, driven by the need to address water scarcity and food security challenges. The region's agricultural sector is witnessing increasing adoption of advanced farming technologies, particularly in precision irrigation and smart greenhouse applications. Countries in the region are focusing on developing sustainable agricultural practices through technological innovation. The adoption of agriculture software solutions is supported by government initiatives aimed at modernizing the agricultural sector and reducing dependence on food imports. Mobile-based applications and digital tools are gaining particular traction among farmers in the region, providing valuable insights and decision-making support.

Get Analysis on Important Geographic Markets

Download PDF

Agriculture Software Industry Overview

Top Companies in Agriculture Software Market

The agriculture software companies market features established players like Trimble Inc., AGRIVI Ltd, Oracle Corporation, Conservis, Farmbrite, Deere & Company, and others who are driving innovation through advanced technological solutions. Companies are increasingly focusing on developing cloud-based platforms and integrated solutions that combine precision farming capabilities with data analytics and automation features. Strategic partnerships and collaborations with agricultural equipment manufacturers and technology providers have become a key trend to enhance product offerings and market reach. The industry is witnessing significant investment in research and development to incorporate emerging technologies like AI, IoT, and machine learning into farm management solutions. Companies are also expanding their geographical presence through strategic acquisitions and establishing strong distribution networks to serve diverse agricultural markets globally.

Fragmented Market with Growing Consolidation Trends

The agriculture software market exhibits a fragmented structure with a mix of global technology conglomerates and specialized agriculture software companies competing for market share. Large agricultural equipment manufacturers like Deere & Company have leveraged their established presence to integrate software solutions into their product ecosystem, while specialized players like AGRIVI and Conservis focus on developing comprehensive farm management platforms. The market is characterized by increasing consolidation through mergers and acquisitions, as larger companies seek to acquire innovative startups and smaller players to enhance their technological capabilities and expand their solution portfolio.

The competitive dynamics are shaped by the presence of both international players with extensive resources and regional specialists with deep local market understanding. Companies are increasingly pursuing strategic partnerships and joint ventures to combine their strengths in hardware, software, and agricultural expertise. The market has witnessed a surge in investment activities, particularly in startups developing innovative agricultural software solutions, leading to increased competition and technological advancement in the sector.

Innovation and Customer Focus Drive Success

Success in the farm management software industry increasingly depends on providers' ability to deliver comprehensive, user-friendly solutions that address specific farming challenges while integrating seamlessly with existing agricultural equipment and practices. Companies must focus on developing scalable platforms that can accommodate various farm sizes and types while ensuring data security and privacy. The ability to provide real-time insights, predictive analytics, and automated decision-making capabilities has become crucial for gaining a competitive advantage. Providers must also establish strong customer support networks and offer training programs to help farmers maximize the benefits of their software solutions.

Market players need to consider the growing influence of environmental regulations and sustainability requirements in agricultural practices. Companies that can demonstrate a clear value proposition through improved efficiency, reduced input costs, and enhanced yield optimization are better positioned to gain market share. The ability to build and maintain strong relationships with agricultural cooperatives, equipment manufacturers, and technology partners is becoming increasingly important. Future success will depend on providers' capacity to adapt to evolving farmer needs, technological advancements, and changing regulatory landscapes while maintaining competitive pricing strategies and robust support infrastructure. The farm management software market size is expected to grow as these trends continue to evolve.

Agriculture Software Market Leaders

-

Trimble Inc.

-

AGRIVI Ltd

-

Oracle Corporation

-

Conservis

-

Farmbrite

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Agriculture Software Market News

- April 2023: CropX, a provider of decision and planning tools, secured a Series C financing round with USD 30 million to advance its farm management system, integrating data from the earth and the sky to provide soil and crop intelligence.

- February 2023: The Topcon Corporation launched a solution for specialized farmers called Transplanting Control. The growers of permanent and perennial trees, fruits, and vegetable crops can profit from this system, which provides GNSS-based guiding, autosteering, and control, which has been designed to reduce labor costs, boost productivity, and increase efficiency.

Agriculture Software Market Market Report - Table of Contents

1. INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET INSIGHTS

- 4.1 Market Overview

-

4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Consumers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitutes

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Assessment of Impact of Macro Economic Trends

- 4.4 Case Studies

- 4.5 Ecosystem Analysis

5. MARKET SEGMENTATION

-

5.1 By Deployment Type

- 5.1.1 Cloud

- 5.1.1.1 Software-as-a-service (SAAS)

- 5.1.1.2 Platform-as-a-service (PAAS)

- 5.1.2 On-premise

-

5.2 By Application

- 5.2.1 Precision Farming

- 5.2.2 Livestock Tracking and Monitoring

- 5.2.3 Smart Greenhouse

- 5.2.4 Precision Forestry

- 5.2.5 Other Applications

-

5.3 By Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.2 Europe

- 5.3.2.1 United Kingdom

- 5.3.2.2 Germany

- 5.3.2.3 France

- 5.3.2.4 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 Australia and New Zealand

- 5.3.3.3 Thailand

- 5.3.3.4 Rest of Asia-Pacific

- 5.3.4 Latin America

- 5.3.4.1 Brazil

- 5.3.4.2 Mexico

- 5.3.4.3 Argentina

- 5.3.4.4 Rest of Latin America

- 5.3.5 Middle East & Africa

6. COMPETITIVE LANDSCAPE

-

6.1 Company Profiles

- 6.1.1 Trimble Inc.

- 6.1.2 AGRIVI Ltd

- 6.1.3 Oracle Corporation

- 6.1.4 Conservis

- 6.1.5 Farmbrite

- 6.1.6 Deere & Company

- 6.1.7 Ag Leader Technology Incorporated

- 6.1.8 AgJunction Inc.

- 6.1.9 AGCO Corporation

- 6.1.10 Raven Industries Inc.

- 6.1.11 Topcon Corporation

- *List Not Exhaustive

7. INVESTMENT ANALYSIS

8. FUTURE OPPORTUNITIES

**Subject to Availability

You Can Purchase Parts Of This Report. Check Out Prices For Specific Sections

Get Price Break-up Now

Agriculture Software Industry Segmentation

The agriculture software market study tracks the revenue accrued through the sale of subscriptions and licensing of agriculture software, specifically in agricultural applications such as precision farming and smart greenhouse across the globe. The analysis is based on the market insights captured through secondary research and the primaries. The market also covers the major factors impacting the growth of the market in terms of drivers and restraints.

The agriculture software market is segmented by deployment type (cloud (software-as-a-service (SaaS), platform-as-a-service (PaaS)) and on-premise), application (precision farming, livestock tracking and monitoring, smart greenhouse, precision forestry, and other applications), geography (North America (United States, Canada), Europe (United Kingdom, France, Germany, Rest of Europe), Asia-Pacific (China, Australia and New Zealand, Thailand, Rest of Asia-Pacific), Latin America (Brazil, Mexico, Argentina, Rest of Latin America), Middle East & Africa). The market sizes and forecasts are provided in terms of value (USD ) for all the segments.

| By Deployment Type | Cloud | Software-as-a-service (SAAS) | |

| Platform-as-a-service (PAAS) | |||

| On-premise | |||

| By Application | Precision Farming | ||

| Livestock Tracking and Monitoring | |||

| Smart Greenhouse | |||

| Precision Forestry | |||

| Other Applications | |||

| By Geography | North America | United States | |

| Canada | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Australia and New Zealand | |||

| Thailand | |||

| Rest of Asia-Pacific | |||

| Latin America | Brazil | ||

| Mexico | |||

| Argentina | |||

| Rest of Latin America | |||

| Middle East & Africa | |||

Need A Different Region or Segment?

Customize Now

Agriculture Software Market Market Research Faqs

What is the current Agriculture Software Market size?

The Agriculture Software Market is projected to register a CAGR of 11.70% during the forecast period (2025-2030)

Who are the key players in Agriculture Software Market?

Trimble Inc., AGRIVI Ltd, Oracle Corporation, Conservis and Farmbrite are the major companies operating in the Agriculture Software Market.

Which is the fastest growing region in Agriculture Software Market?

North America is estimated to grow at the highest CAGR over the forecast period (2025-2030).

Which region has the biggest share in Agriculture Software Market?

In 2025, the Asia Pacific accounts for the largest market share in Agriculture Software Market.

What years does this Agriculture Software Market cover?

The report covers the Agriculture Software Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Agriculture Software Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Our Best Selling Reports

Agriculture Software Market Research

Mordor Intelligence provides a comprehensive analysis of the agriculture software market. We leverage our extensive experience in agricultural technology research to deliver valuable insights. Our detailed report examines the evolving landscape of digital farming software and smart farming software. It includes crucial segments like farm management software and agriculture mobile app solutions. The analysis also covers precision agriculture software, crop management software, and livestock management software. These insights reveal how agriculture business management is being transformed through technology.

Stakeholders across the agricultural software industry benefit from our thorough examination of agriculture ERP systems and agriculture data management solutions. The report PDF, available for download, offers an in-depth analysis of agriculture supply chain software implementations and farm operations software developments. Our research covers emerging trends in agriculture resource management, farm planning software, and agtech software. This provides valuable insights for agriculture software companies and industry participants. The comprehensive coverage includes a detailed analysis of digital farming initiatives and farm management software market size. This enables informed decision-making for industry stakeholders.