South Africa Agriculture Market Analysis by Mordor Intelligence

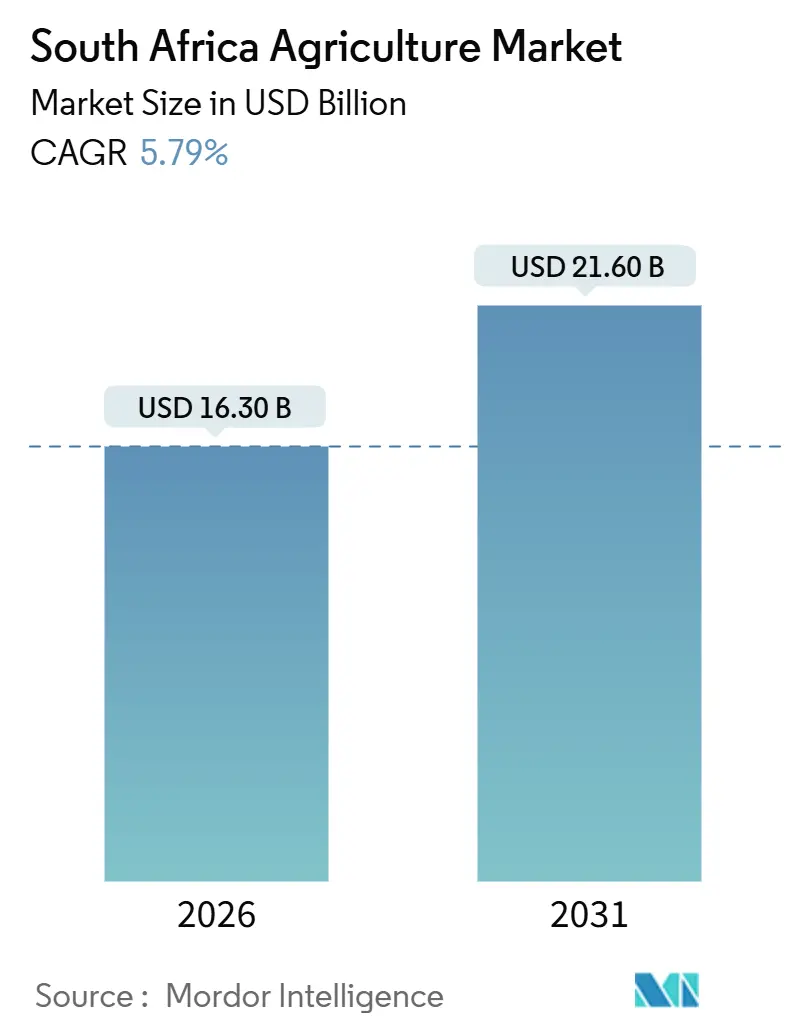

South Africa's agriculture market size stood at USD 16.3 billion in 2026 and is projected to reach USD 21.6 billion by 2031, advancing at a 5.79% CAGR during the forecast period. Structural gains stem from export-oriented horticulture, rapid deployment of precision-agriculture tools, and expanded value-chain finance rather than pure acreage growth. Commercial farms lifted yield per hectare through satellite-guided fertilization, drone-based pest scouting, and soil-moisture sensors embedded in variable-rate irrigation rigs. Policy support under the Agriculture and Agro-processing Master Plan (AAMP) has unlocked USD 64 million for irrigation upgrades and packhouse expansion, resulting in a 15% reduction in post-harvest losses since 2024. Significant agricultural exports in 2024 highlighted the sector's dual role as a generator of foreign exchange and a cornerstone of domestic food security.

Key Report Takeaways

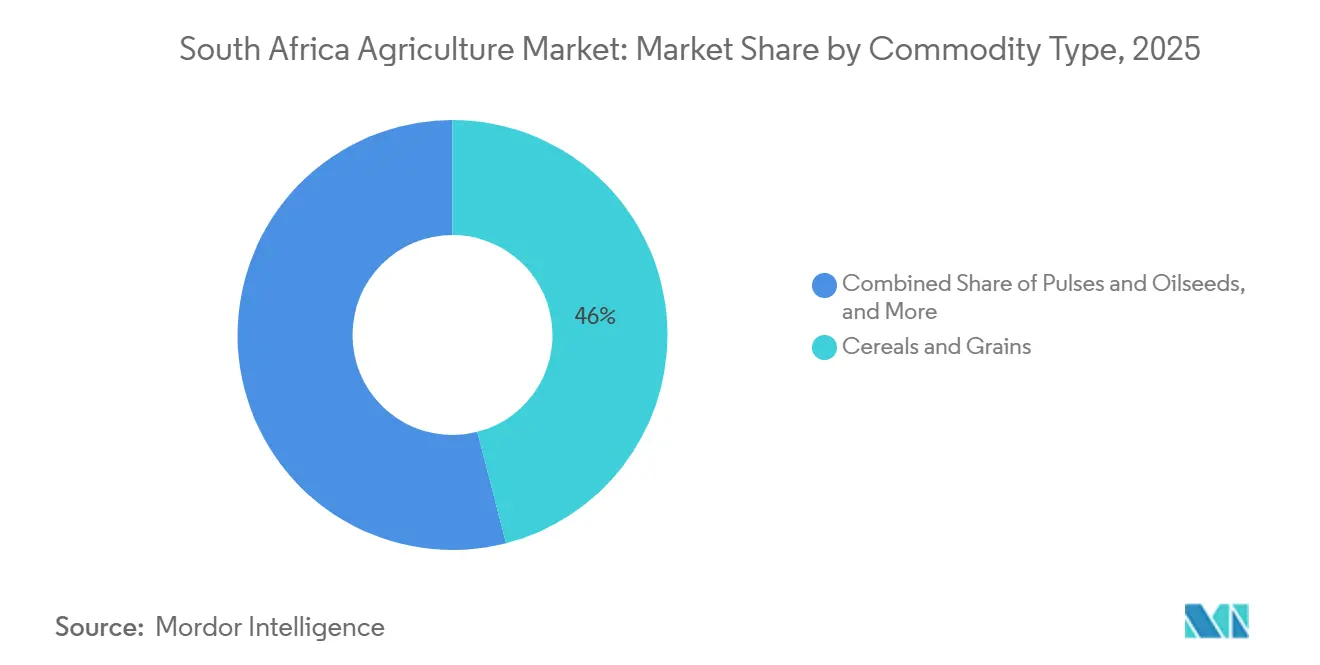

- By commodity type, cereals and grains led with 46% of South Africa agriculture market share in 2025, while vegetables are forecast to grow at a 6.9% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

South Africa Agriculture Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High demand for food crops with a rising population | +1.8% | National, with concentration in Gauteng, Western Cape urban centers | Long term (≥ 4 years) |

| Adoption of advanced ag technologies | +1.2% | Western Cape, Mpumalanga, Free State commercial farming areas | Medium term (2-4 years) |

| Government support via the Agriculture and Agro-processing Master Plan | +0.9% | National, with priority focus on Eastern Cape, Limpopo transformation zones | Long term (≥ 4 years) |

| Surge in horticulture exports | +1.5% | Western Cape, Limpopo citrus regions, KwaZulu-Natal subtropical zones | Short term (≤ 2 years) |

| Expansion of carbon-credit revenue streams for regenerative practices | +0.7% | Free State, Northwest, Mpumalanga grain production areas | Medium term (2-4 years) |

| Corporate off-take agreements with retailers | +0.5% | National, with early adoption in the Western Cape, KwaZulu-Natal | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Demand for Food Crops With a Rising Population

South Africa agriculture market benefits from a population that is projected to reach 62 million by 2030, lifting urban demand for cereals, pulses, and fresh produce [1]Source: Statistics South Africa, “Population Projections 2030,” statssa.gov.za. Maize consumption, which supplies more than 60% of caloric intake, has remained near 11 million metric tons annually, while wheat-based foods are increasingly popular in metropolitan regions. Regional food-security mandates divert surplus cereals to Botswana, Namibia, and Zimbabwe, helping to stabilize producer cash flow during bumper harvests. Quarterly climate-adjusted yield forecasts have sharpened grain-reserve management, reducing import spikes in drought years. Rising disposable income is shifting plates toward higher-value proteins and greenhouse vegetables, generating downstream demand for fodder crops and protected cultivation infrastructure.

Adoption of Advanced Ag Technologies

Precision-agriculture platforms reached scale, as the Council for Scientific and Industrial Research (CSIR) mapped 450,000 hectares on its decision-support system by 2025. Variable-rate irrigation reduced water use by 18% to 25% on citrus and avocado estates in Limpopo, a critical step in a province prone to drought. Multispectral drones enabled early pest detection, reducing pesticide volumes by 12% and aligning farms with the Department of Forestry, Fisheries, and the Environment (DFFE) stewardship codes[2]Source: Council for Scientific and Industrial Research, “Precision Agriculture Information System,” csir.co.za. According to the International Soil Reference and Information Centre (ISRIC) Report, GPS-guided planters, now installed on 70% of large grain farms, have improved seed placement and increased maize and soybean yields by 5% to 8% since 2024. Data analytics, combined with agronomic advice, generated recurring revenue for equipment dealers. The flow of farm-level data is also improving credit risk assessment, thereby widening access to working capital lines.

Government Support Via the Agriculture and Agro-processing Master Plan

The AAMP, steered by the Department of Agriculture, Land Reform, and Rural Development (DALRRD), deployed ZAR 1.2 billion (approximately USD 64 million) in 2024 for irrigation canals, cold storages, and skills hubs. Twenty-two new refrigerated depots added 85,000 metric tons of capacity, halving spoilage in berries and stone fruit. Streamlined phytosanitary clearance now requires only seven days, down from fourteen, accelerating avocado and blueberry shipments to Europe. Preferential procurement earmarks have brought ZAR 800 million (USD 43 million) in institutional contracts to black-owned producers, although the provincial rollout remains uneven. The plan’s monitoring dashboard, updated quarterly, flags bottlenecks in licensing, export certification, and logistics, enabling rapid policy tweaks.

Surge in Horticulture Exports

According to the Citrus Growers’ Association (CGA), citrus exports experienced year-over-year growth following the adoption of new market protocols with China, Japan, and South Korea. Avocado volumes reached record levels, supported by packhouse upgrades that reduced shipping lead times by three days. Table grapes, apples, and pears benefited from preferential tariffs under the European Partnership Agreement. Transnet increased refrigerated rail slots, and the Cape Town port significantly expanded its reefer-container capacity. However, congestion at the Durban port led to cargo being redirected through Maputo and Walvis Bay. Since 2024, private equity funds have planted 8,500 hectares of blueberries and macadamias in Limpopo and Mpumalanga, capitalizing on higher export margins.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Low land productivity and soil degradation | -1.1% | Eastern Cape communal areas, Free State marginal lands | Long term (≥ 4 years) |

| Limited access to affordable finance for smallholders | -0.8% | Rural areas across Limpopo, Eastern Cape, KwaZulu-Natal | Medium term (2-4 years) |

| Risk of losing duty-free access | -0.9% | Western Cape citrus regions, automotive manufacturing zones | Short term (≤ 2 years) |

| Increasing water licensing compliance costs | -0.6% | Commercial farming areas in the Western Cape, Mpumalanga | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Low Land Productivity and Soil Degradation

Roughly one-third of cropland suffers moderate to severe soil degradation marked by erosion, nutrient depletion, and declining organic matter. Maize yields in the Free State and North West average 4.5 metric tons per hectare, 35% below hybrid potential, primarily due to low soil pH and compaction. A national survey identified 2.1 million hectares that require lime application, at a cost of ZAR 1,800 to ZAR 2,500 (USD 97 to USD 135) per hectare, a burden that most smallholders cannot afford. Erosion on Eastern Cape communal lands exceeds 10 metric tons per hectare annually, stripping the topsoil and reducing the water-holding capacity. Pilot rehabilitation on 18,000 hectares shows promise but needs sustained extension support and subsidized inputs to scale.

Limited Access to Affordable Finance for Smallholders

The Land Bank’s loan book decreased from ZAR 48 billion (USD 2.6 billion) in 2021 to ZAR 29 billion (USD 1.6 billion) by 2024, resulting in a funding gap for smallholders[3]Source: Land Bank, “Annual Financial Statements 2024,” landbank.co.za. Commercial banks demand collateral and audited accounts, criteria that exclude three-quarters of applicants. Agricultural loan rates averaged 11.5% to 13.5% in 2025, which was between 2 and 4 percentage points above the prime rate, reflecting weather-related credit risk. Concessional vehicles, such as the Industrial Development Corporation’s agro-processing fund, disbursed ZAR 1.8 billion (USD 97 million) between 2023 and 2025. Demand outstripped supply threefold. Microfinance caps of ZAR 50,000 (USD 3,700) are inadequate for machinery or irrigation pivots, limiting technology diffusion.

Segment Analysis

By Commodity Type: Cereals Anchor, Horticulture Accelerates

Cereals and grains maintained dominance with 46% of South Africa agriculture market share in 2025, supported by maize that leveraged favorable rainfall and drought-tolerant hybrids. Sorghum and barley trails remain niche, but feed the growing craft-beer industry. The climatic reliability of the maize belt underpins domestic food security while generating surpluses for Southern African Customs Union neighbors, stabilizing regional grain prices. Precision planters and variable-rate fertilizer systems on large grain estates further embedded economic yield growth without acreage expansion, a trend that keeps cereals critical to the South Africa agriculture market.

Vegetables, projecting a 6.9% CAGR through 2031, exploit international appetite for vitamin-rich produce and extend South Africa agriculture market size in higher-margin categories. Limpopo, Mpumalanga, and Western Cape estates added 12,500 hectares of citrus, avocado, and blueberry orchards between 2023 and 2025. Controlled-atmosphere cold storage now prolongs shelf life by up to 14 days, enabling containerized exports to East Asia without requiring layovers in ripening rooms. Pulses and oilseeds are reducing protein-meal imports and improving feed-processing margins. Cash crops are primarily driven by sugarcane, with cane-based cogeneration contributing baseload renewable electricity through utility power-purchase agreements. Tobacco acreage has declined due to stricter health regulations, although small areas in Limpopo continue to produce specialty grades for premium cigar leaf.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

Geography Analysis

The South Africa agriculture market spreads across diverse agro-climatic zones that dictate regional specialization. The Free State, North West, and Mpumalanga maize triangle contributed significantly to the national grain output in 2025, benefiting from deep vertisol soils, mechanized operations, and silage infrastructure that reduce harvest losses. Farms embedded near rail sidings optimize bulk export flows to Richards Bay and Mozambique’s Maputo port, reducing inland logistics costs. Limpopo is the fastest-growing agricultural region in the country, with avocado plantations expanding by 4,200 hectares between 2023 and 2025, and citrus estates increasing by 3,800 hectares. This growth is supported by access to the Olifants River irrigation scheme and the region's proximity to the Port of Durban, which facilitates export logistics. The short distance to Durban harbor reduces transit time to Middle Eastern supermarkets, helping maintain pulp firmness within retailer specifications.

The Western Cape dominates the production of deciduous fruit, table grapes, and premium wine grapes, accounting for 72% of national apple and pear exports and 95% of wine production in 2025. Growers employ netting, drip irrigation, and predictive disease scouting to mitigate the effects of the Cape Doctor wind and shifts in Mediterranean drought. Peri-urban greenhouses surrounding Cape Town and Johannesburg have added 850 hectares of hydroponic lettuce and tomatoes since 2024, reducing reliance on Spanish winter glasshouse vegetables for imports.

KwaZulu-Natal diversifies beyond cane, replacing low-margin fields with macadamia orchards that fetched USD 12 per kilogram kernel price in 2025. The province’s dual-purpose Noodsberg cogeneration plant now supplies 18 megawatts of bagasse-derived electricity to the national grid, enhancing mill economics. According to the Eastern Cape Rural Development Agency (ECRDA), the Eastern Cape faces challenges such as fragmented land tenure and soil erosion, resulting in maize yields that are 40% below the national average. However, the region's 3.2 million cattle present opportunities in the red meat market, provided veterinary services and feedlot capacities are expanded. Northern Cape growers exploit the Orange River’s regulated flow to irrigate 22,000 hectares of raisins and table grapes, exporting 65 million cartons to European and Asian buyers despite long overland routes to port.

Competitive Landscape

South Africa's agriculture market exhibits concentration as cooperatives, multinational subsidiaries, and vertically integrated exporters compete with thousands of smallholders. Grain cooperatives Senwes, VKB, and NWK command 55% of on-farm silo capacity and 40% of fertilizer distribution, enabling preferential freight rates and pooled procurement that suppress input costs. The February 2023 VKB-GWK merger formed a ZAR 18 billion (USD 970 million) giant spanning Free State, North West, and Northern Cape, illustrating consolidation aimed at economies of scale. Export specialists, such as Westfalia Fruit, Capespan, and Dutoit, integrate orchards, packhouses, and overseas subsidiaries to capture margins from the farm gate to the retail shelf. Westfalia secured a USD 300 million credit line in 2023 for cold-room automation and the rollout in the Asian market.

Technology is a discriminator. ZZ2’s internet-of-things greenhouse-control system optimized climate variables and increased tomato yields by 9% while reducing water use by 14% in 2025. Blockchain pilots led by the Lona Group, in collaboration with the University of Pretoria, record citrus harvest data, packhouse handling, and reefer temperatures on a distributed ledger, thereby reducing customs disputes and expediting border inspections. Agri-fintech startups embed invoice discounting and weather-indexed insurance within produce-procurement apps, widening smallholder liquidity and hedging rainfall risk. Regenerative-agriculture specialists monetize soil-carbon credits, selling offsets to retailers that pledge net-zero supply chains.

Value-added niches remain underdeveloped. Pulses, oilseed meals, and indigenous botanicals such as rooibos tea still register less than 5% global share despite favorable agro-ecology and protected designation of origin status. Proposed investments in extruders, solvent-extraction plants, and herbal-tea processing could diversify export baskets and stabilize farm revenues against commodity cycles. Competitive intensity will likely increase as private-equity ownership grows, fostering managerial discipline and capital access but also heightening pressure on small growers to keep pace with certifications and traceability requirements.

Recent Industry Developments

- September 2025: Tiger Brands has transitioned its Langeberg and Ashton Foods operations into a standalone business unit, focusing on its core grain-based and agricultural product lines. This initiative aims to enhance operational efficiency and align strategically within its food and agriculture portfolio, thereby improving competitiveness in South Africa's agro-processing market. The restructuring aligns with industry trends emphasizing portfolio optimization and a stronger focus on high-growth agricultural segments.

- April 2025: The Department of Agriculture (DOA), the Provincial Department of Agriculture and Rural Development (DARD), and Unilever South Africa, in collaboration with provincial agricultural authorities, initiated a smallholder support program in Jozini, KwaZulu-Natal. This program trained 100 farmers in herb and spice cultivation and integrated them into Unilever’s supplier localization chain, contributing to the development of South Africa's agricultural sector by enhancing smallholder participation and promoting sustainable farming practices.

- March 2024: Vergelegen Wine Estate has partnered with SkyBugs to conduct drone-delivered biological pest control trials. These trials aim to address mealybugs and grape leafroll disease using predatory wasps and ladybug beetles, showcasing a sustainable alternative to chemical treatments. This initiative showcases the increasing adoption of innovative and eco-friendly pest management solutions, which can improve crop health and productivity while minimizing environmental impact in the South African agricultural market. The cost of this approach ranges from ZAR 650 to 1,500 (USD 37–85.4) per hectare.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

According to Mordor Intelligence, the South African agriculture market covers the on-farm production and first-sale value of food and industrial crops, field and protected horticulture, and livestock derived at the farm gate; downstream agro-processing, forestry, and fisheries are outside scope.

Scope exclusion: forestry, aquaculture, and commercial timber plantations fall beyond this study's boundary.

Segmentation Overview

- By Commodity Type

- Grains and Cereals

- Production Analysis (Volume)

- Overview

- Area Harvested and Yield

- Consumption Analysis (Value and Volume)

- Trade Analysis (Value and Volume)

- Import Market Analysis

- Overview

- Key Supplying Markets

- Export Market Analysis

- Overview

- Key Destinations Markets

- Import Market Analysis

- Wholesale Price Trend Analysis and Forecast

- Seasonality Analysis

- Production Analysis (Volume)

- Pulses and Oilseeds

- Production Analysis (Volume)

- Overview

- Area Harvested and Yield

- Consumption Analysis (Value and Volume)

- Trade Analysis (Value and Volume)

- Import Market Analysis

- Overview

- Key Supplying Markets

- Export Market Analysis

- Overview

- Key Destinations Markets

- Import Market Analysis

- Wholesale Price Trend Analysis and Forecast

- Seasonality Analysis

- Production Analysis (Volume)

- Fruits

- Production Analysis (Volume)

- Overview

- Area Harvested and Yield

- Consumption Analysis (Value and Volume)

- Trade Analysis (Value and Volume)

- Import Market Analysis

- Overview

- Key Supplying Markets

- Export Market Analysis

- Overview

- Key Destinations Markets

- Import Market Analysis

- Wholesale Price Trend Analysis and Forecast

- Seasonality Analysis

- Production Analysis (Volume)

- Vegetables

- Production Analysis (Volume)

- Overview

- Area Harvested and Yield

- Consumption Analysis (Value and Volume)

- Trade Analysis (Value and Volume)

- Import Market Analysis

- Overview

- Key Supplying Markets

- Export Market Analysis

- Overview

- Key Destinations Markets

- Import Market Analysis

- Wholesale Price Trend Analysis and Forecast

- Seasonality Analysis

- Production Analysis (Volume)

- Cash Crops

- Production Analysis (Volume)

- Overview

- Area Harvested and Yield

- Consumption Analysis (Value and Volume)

- Trade Analysis (Value and Volume)

- Import Market Analysis

- Overview

- Key Supplying Markets

- Export Market Analysis

- Overview

- Key Destinations Markets

- Import Market Analysis

- Wholesale Price Trend Analysis and Forecast

- Seasonality Analysis

- Production Analysis (Volume)

- Grains and Cereals

Detailed Research Methodology and Data Validation

Primary Research

Structured interviews with commercial farmers, co-op managers, commodity-board economists, agritech integrators, and export agents across Gauteng, Western Cape, KwaZulu-Natal, and Limpopo helped confirm harvested area shifts, average selling prices, technology adoption rates, and bio-security cost impacts. These conversations validated desk findings and filled data gaps on informal market channels.

Desk Research

Mordor analysts began with official datasets such as Statistics South Africa crop census, SAGIS grain flow sheets, National Agricultural Marketing Council trade dashboards, Department of Agriculture quarterly conditions bulletins, and USDA-FAS country PS&D files. Macro inputs, including CPI, producer price indices, and rand-dollar trends, were taken from the South African Reserve Bank and World Bank. Company filings and provincial agriculture department reports provided cost curves and yield benchmarks, while paid access to D&B Hoovers and Dow Jones Factiva allowed verification of farm-gate revenue disclosures. This list is illustrative; many other open and subscription sources informed intermediate assumptions.

Market-Sizing & Forecasting

We anchor the 2025 baseline with a top-down build that reconciles agricultural gross value added, crop-specific production volumes, and average farm-gate prices; subsequently, cross-checked through bottom-up roll-ups of sampled large-scale farm revenues. Key variables include seeded area, five-year average yields, livestock slaughter weights, export parity pricing, and input-cost inflation. Missing bottom-up pieces, most notably for smallholder volumes, are bridged with calibrated shadow multipliers derived from census ratios. Forecasts to 2030 apply multivariate regression linking planted area and yield to rainfall anomalies (SPI index), fertilizer affordability, and real exchange-rate shifts; before scenario stress-testing with maize-soy price spreads and phytosanitary trade alerts.

Data Validation & Update Cycle

Outputs pass multi-layer variance, peer, and senior-analyst reviews; anomalies over ±5% trigger a re-run of assumptions. Models refresh each year, with in-cycle updates after material events such as drought declarations or sudden tariff changes, ensuring clients receive the latest vetted view.

Why Mordor's South Africa Agriculture Baseline Commands Reliability

Published market values often diverge.

Differences in crop baskets, price assumptions, and refresh cadence typically drive the spread.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 17.30 B (2025) | Mordor Intelligence | - |

| USD 14.98 B (2024) | Regional Consultancy A | Omits informal livestock sales and uses 2020 yield constants |

| USD 15.04 B (2023) | Global Consultancy B | Excludes horticulture under shade nets; currency fixed at 2023 average FX |

Because Mordor aligns crop-level volumes with current season surveys, applies rolling three-year average prices, and refreshes annually, our baseline balances realism with traceability and offers a dependable starting point for strategic planning.

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the estimated value of the South Africa agriculture market in 2026?

It is USD 16.3 billion with a trajectory to reach USD 21.6 billion by 2031.

Which commodity held the largest share in 2025?

Cereals and grains led with 46% of South Africa agriculture market share.

Which segment is projected to grow fastest through 2031?

Vegetables are forecast to post a 6.9% CAGR, outpacing other commodities.

How will AGOA expiry affect exporters?

A lapse could impose tariffs of 5% to 15% on shipments worth USD 1.1 billion, eroding citrus and wine margins.

Which province is the fastest-growing horticulture hub?

Limpopo records the quickest expansion, adding 8,000 plus hectares of citrus and avocado orchards since 2023.

What role do carbon credits play for farmers?

Verified regenerative practices generated USD 3.2 million in carbon-credit revenue in 2025, bolstering income diversification.