Market Overview

| Study Period | 2020 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

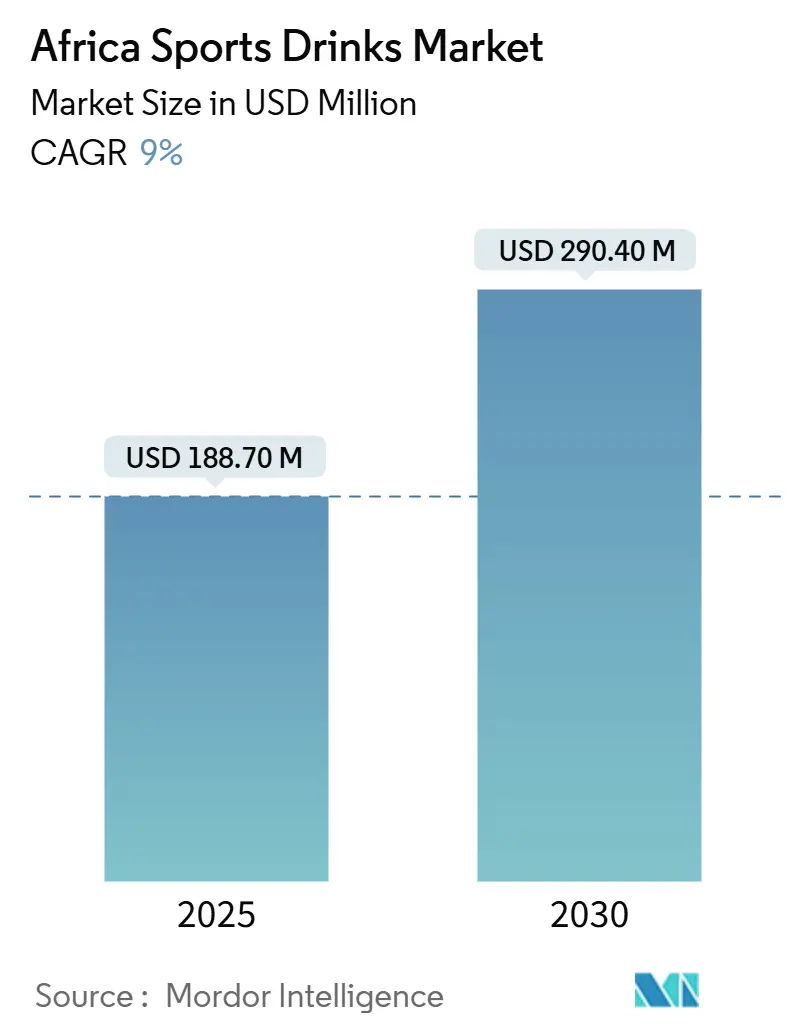

| Market Size (2025) | USD 188.70 Million |

| Market Size (2030) | USD 290.40 Million |

| Growth Rate (2025 - 2030) | 9.00% CAGR |

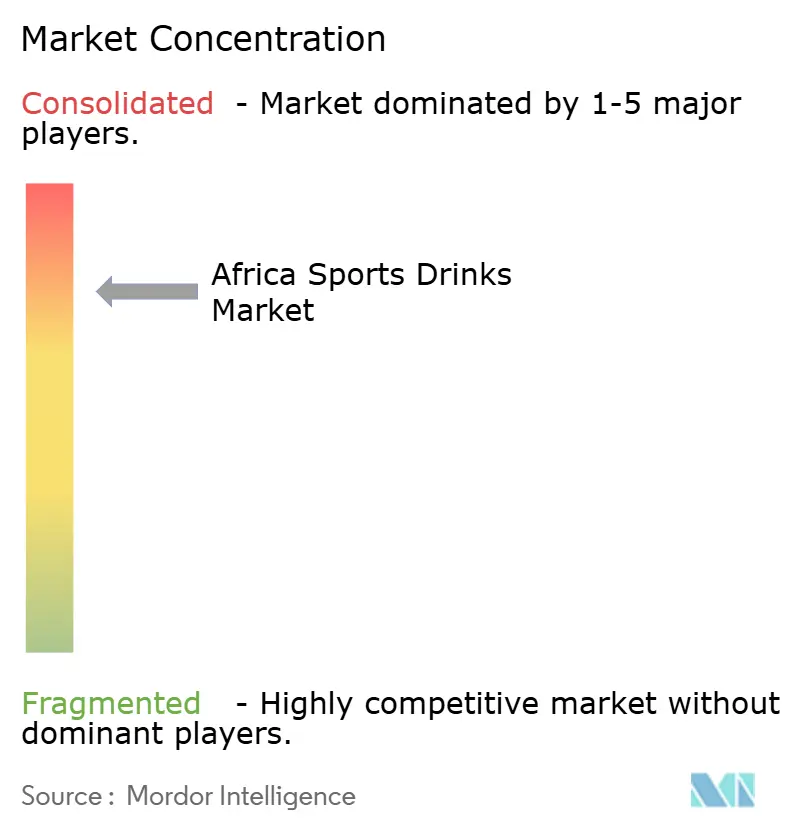

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Africa Sports Drinks Market Analysis by Mordor Intelligence

The Africa Sports Drink Market was valued at USD 188.70 million in 2025 and is projected to grow to USD 290.40 million by 2030, registering a compound annual growth rate (CAGR) of 9.00% during the forecast period. This growth reflects a significant shift driven by urbanization, increasing disposable incomes, and the development of fitness infrastructure, which are collectively transforming functional hydration from a niche product for athletes into a mainstream wellness trend across the continent. In South Africa, the implementation of a sugar tax in 2018 has had a notable impact on consumer behavior. Researchers analyzed nutritional data from the purchases of over 3,000 households before and after the tax's introduction to assess changes in daily sugar intake, calorie consumption, and the volume of taxed and non-taxed beverages purchased. The analysis revealed a 52% reduction in calorie consumption, a 51% decrease in sugar intake, and a 29% decline in the volume of beverages purchased per person per day following the enactment of the tax [1]Source: Gillings School of Global Public Health, “South African beverage tax has reduced purchases of sugar-sweetened beverages,” sph.unc.edu.

Key Report Takeaway

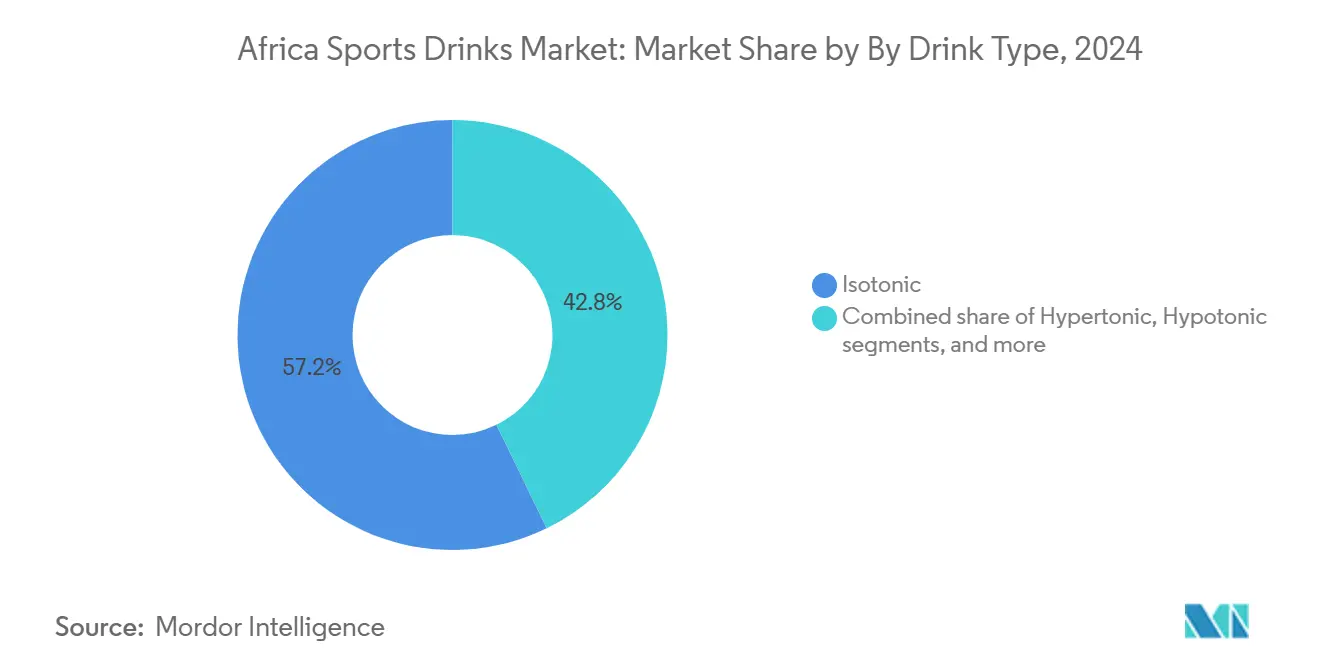

- By drink type, isotonic products commanded 57.23% of the Africa sports drink market share in 2024, and hypotonic sports drinks are forecast to grow at an 11.56% CAGR through 2030.

- By functionality, post-workout beverages led with 45.15% share in 2024, while pre-workout lines are set to register the fastest 10.89% CAGR between 2025-2030.

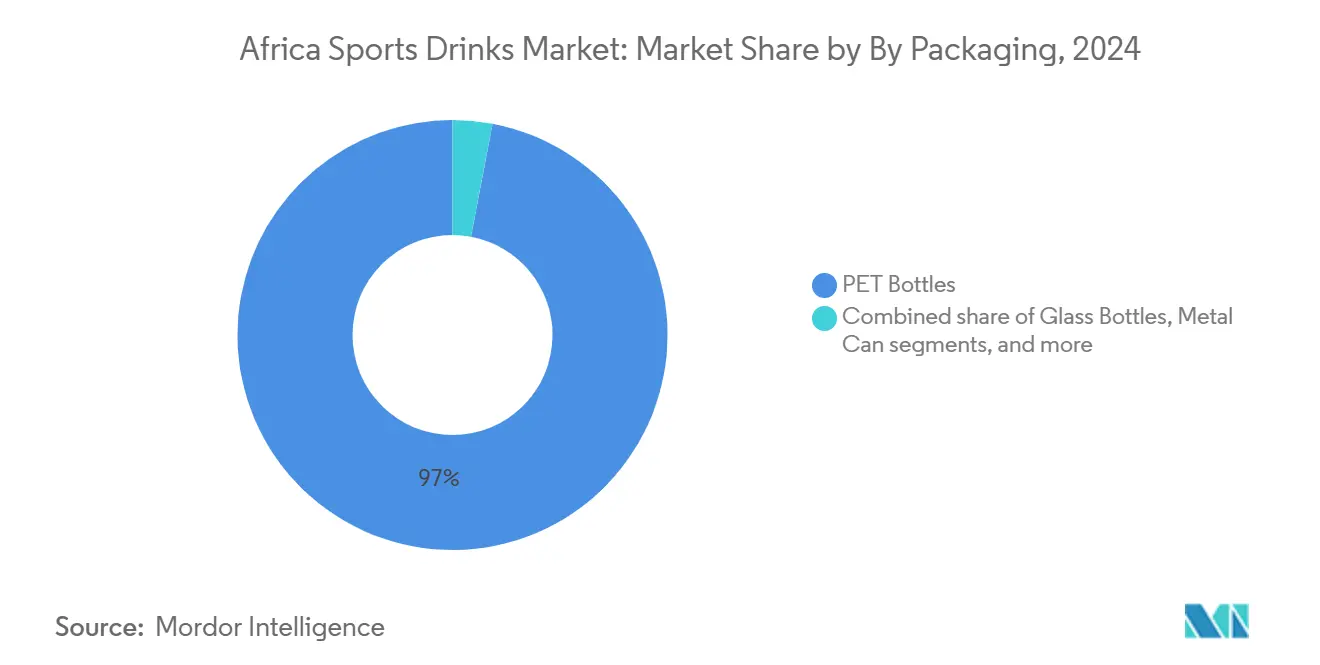

- By packaging, PET bottles dominated with 97.02% share in 2024; metal cans are expected to record an 11.76% CAGR, the quickest among formats.

- By distribution, off-trade channels held 82.09% of 2024 revenue, whereas on-trade outlets should advance at a 10.94% CAGR over the outlook period.

- By geography, South Africa captured 84.22% of 2024 value, yet Nigeria is poised for the strongest 11.38% CAGR to 2030.

Africa Sports Drinks Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in fitness activities and gym participation | +2.1% | South Africa, Kenya, Nigeria (urban centers: Lagos, Nairobi, Johannesburg, Cape Town) | Medium term (2-4 years) |

| Health consciousness promoting hydration and recovery products | +1.8% | Global, with early adoption in South Africa and Egypt | Short term (≤ 2 years) |

| Innovation in local taste-adapted formulations | +1.3% | South Africa, Nigeria, Kenya (regional flavor preferences) | Medium term (2-4 years) |

| Partnerships with sports events and teams | +1.5% | South Africa (Comrades Marathon), Kenya (rugby, athletics), Nigeria (football leagues) | Short term (≤ 2 years) |

| Youth engagement in competitive sports | +1.2% | Nigeria, Kenya, Egypt (youth population >50% under 25) | Long term (≥ 4 years) |

| Wellness trends favoring functional hydration | +1.4% | South Africa, Kenya, Egypt (emerging middle class) | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Understand The Key Trends Shaping This Market

Download PDF

Surge in fitness activities and gym participation

Boutique fitness studios and gym chains experienced significant growth across African urban centers in 2024. In Kenya, the fitness industry expanded with the addition of several new facilities in Nairobi and Mombasa, catering to an increasing number of health-conscious professionals. This expansion has created dedicated distribution channels for sports drinks, as gym-goers reportedly consume approximately 120-180 mL of hydration beverages every 15 minutes during intense exercise, based on guidelines from peer-reviewed sports science research. Strategically, positioning sports drinks as pre-workout hydration solutions, rather than solely for post-exercise recovery, offers an opportunity to capture market share from energy drinks by focusing on sustained hydration instead of short-term caffeine boosts. Sponsorship initiatives within gyms, such as sampling programs and branded hydration stations, have proven more effective in converting trials into regular purchases compared to retail promotions. For instance, South African brands like MoFaya and Knox Hydrate have successfully utilized celebrity endorsements to enhance visibility and engagement within fitness-focused environments.

Health consciousness promoting hydration and recovery product

Public health campaigns and rising awareness of non-communicable diseases have elevated hydration from a performance concern to a daily wellness imperative across Africa. The National Library of Mecicine data published on September 2025 revealed that only 20% of African adolescents meet recommended physical activity guidelines, with girls significantly less active than boys, creating a latent demand pool as governments and NGOs invest in youth sports programs [2]Source: National Library of Medicine, “Promoting Adolescent and Youth Health Through Physical Activity Initiatives and Interventions in Sub-Saharan Africa: The ARISE-NUTRINT and DASH Initiatives,” pmc.ncbi.nlm.nih.gov. The transition from reactive (post-workout) to proactive (daily) hydration habits is influencing product positioning. Electrolyte-enhanced water and hypotonic formulations are increasingly being marketed as all-day beverages rather than exercise-specific products. Brands that focus on educating consumers about the science of osmolality and the role of sodium in fluid retention, supported by systematic meta-analyses demonstrating the superiority of hypotonic drinks over isotonic options for central hydration during continuous exercise, can justify premium pricing by positioning sports drinks as targeted wellness solutions.

Innovation in local taste-adapted formulations

African consumers exhibit strong preferences for regionally familiar flavors, and brands that localize formulations capture disproportionate loyalty. Tiger Brands' Score sports drink incorporated umhlonyane, a traditional South African herb, into its flavor profile, differentiating it from multinational offerings and contributing to the brand's above-expectation performance in fiscal 2024. Peer-reviewed research on isotonic drink formulation highlights the viability of natural ingredients, diluted fruit juices (pineapple, apple, banana), coconut water, and honey-based concentrates, as alternatives to synthetic flavoring, with several formulations achieving target osmolality ranges (260-330 mOsm/kg) while delivering culturally resonant taste profiles. The formulation challenge lies in balancing local flavor preferences with scientifically validated hydration efficacy: excessive fructose (common in tropical fruit juices) slows gastric emptying and can cause gastrointestinal distress, while optimal carbohydrate concentrations for rapid hydration fall between 1-3%, requiring dilution of most natural juices. Brands that invest in food science partnerships to optimize local-ingredient formulations, such as using maltodextrin from cassava or maize to lower osmolality while maintaining energy density, can achieve both authenticity and performance.

Partnerships with sports events and teams

High-visibility sponsorships enhance brand recognition and provide opportunities for product trials, contributing to sustained market share growth. THIRSTI Water renewed its 4-year partnership as the Official Hydration Partner of the Comrades Marathon in 2024, supplying 2 million water sachets and 600,000 THIRSTI+ electrolyte sports drink sachets to participants and spectators. PepsiCo announced a multi-year partnership with Formula 1 starting in 2025, designating Gatorade as the official sports drink and Sting Energy as the official energy drink of the racing series, with activation planned in African markets where F1 viewership is expanding. In Kenya, Safaricom entered a 5-year partnership with the Kenya Rugby Union (KRU), while TotalEnergies extended its sponsorship of the Confederation of African Football (CAF) through 2028, creating opportunities for beverage brands to negotiate co-marketing rights. The strategic value of event partnerships goes beyond brand visibility, offering real-world product testing environments where athletes and consumers experience hydration benefits under physical stress, generating credible testimonials and social media content. However, the success of these partnerships relies on effective execution; brands must ensure product availability at retail immediately after events to convert trials into purchases, a challenge in markets with fragmented distribution networks.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Competition from water and natural alternatives | -1.4% | South Africa and Kenya (high coconut water adoption) | Short term (≤ 2 years) |

| Regulatory variations on ingredient claims | -0.9% | Nigeria (NAFDAC), South Africa (SAHPRA, sugar tax), Egypt (EDA) | Medium term (2-4 years) |

| Competition from energy drinks and other functional beverages | -1.2% | South Africa, Nigeria, Kenya (energy drinks CAGR 11.55%) | Short term (≤ 2 years) |

| High production costs for specialized formulas | -0.8% | Nigeria, Egypt (import dependencies, currency volatility) | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Competition from water and natural alternatives

Plain water and coconut water serve as low-cost substitutes that significantly impact sports drink volumes, particularly among casual exercisers who view electrolyte replenishment as unnecessary for short-duration activities. Coconut water and plant-based hydration beverages are marketed as natural electrolyte sources free from synthetic additives. In South Africa, where health consciousness is prominent, and sugar taxes have heightened consumer awareness of beverage ingredient profiles, natural alternatives benefit from a favorable perception. In contrast, sports drinks are often viewed as high in sugar and containing artificial colors, which poses a challenge to their acceptance. From a physiological perspective, water alone is inadequate for rehydration during prolonged exercise exceeding 60 minutes. Sodium losses through sweat, typically ranging from 20-80 mmol/L, must be replaced to maintain plasma volume and prevent hyponatremia, as supported by peer-reviewed sports science research. However, consumer awareness regarding osmolality, the role of sodium in fluid retention, and the limitations of water for exercise lasting over an hour remains limited. This knowledge gap allows natural alternatives to gain market share based on perception rather than proven performance. Brands can address this challenge by reformulating products with natural ingredients, such as using coconut water as a base and incorporating natural fruit flavors, while ensuring scientifically validated electrolyte concentrations. Additionally, investing in educational marketing to inform consumers about the specific scenarios where sports drinks outperform water can help counter the growing competition from natural alternatives.

Regulatory variations on ingredient claims

Regulatory differences across African markets result in increased compliance costs and hinder the scalability of regional product launches. For instance, Nigeria's National Agency for Food and Drug Administration and Control (NAFDAC) requires detailed labeling, including product name, ingredient list, net content, manufacturer details, production and expiration dates, storage conditions, batch number, NAFDAC registration number, and English-language text [3]Source: Nigeria's National Agency for Food and Drug Administration and Control, “GUIDE TO FOOD LABELLING,” nafdac.gov.ng. This adds complexity to packaging and extends registration timelines. In Egypt, regulatory authority for food supplements has shifted from the National Food Safety Authority to the Egypt Medicines Agency (EDA), mandating the registration of all supplements, including sports drinks with functional claims, and adherence to maximum vitamin and mineral levels (e.g., vitamin A limited to 10,000 IU per day). These regulatory discrepancies compel multinational brands to manage multiple SKU formulations and packaging designs, whereas local companies focusing on single-country markets can align with domestic regulations and achieve cost efficiencies. A strategic approach involves developing modular formulations that comply with the strictest regional standards, such as South Africa's sugar threshold, enabling broader market deployment with minimal adjustments. Additionally, lobbying through industry associations to harmonize labeling and health claim regulations under frameworks like the African Continental Free Trade Area (AfCFTA) could further streamline operations.

Segment Analysis

By Drink Type: Hypotonic Formulations Challenge Isotonic Dominance

Isotonic drinks captured 57.23% market share in 2024, and hypotonic sports drinks are forecast to grow at 11.56% CAGR through 2030, reflecting their established positioning as the gold standard for exercise hydration. Hypotonic carbohydrate-electrolyte drinks provide superior central hydration during continuous exercise compared to isotonic and hypertonic formulations, with hypotonic drinks attenuating plasma volume decline by 2.3 percentage points more than isotonic. This evidence gap between scientific consensus and market share suggests that consumer education and product innovation lag behind sports science, creating an opportunity for brands that reformulate toward hypotonic profiles and educate consumers on osmolality's impact on absorption.

Hypertonic drinks, typically used for post-exercise glycogen replenishment due to higher carbohydrate concentrations (>8%), serve niche endurance athletes but risk gastrointestinal distress and delayed gastric emptying, limiting mass-market appeal. Electrolyte-enhanced water occupies a growing middle ground, appealing to wellness consumers who seek hydration benefits without the calories and artificial flavors of traditional sports drinks; this segment is likely under-counted in current market share data as it straddles bottled water and sports drink categories. Protein-based sports drinks, which combine hydration with muscle recovery, are emerging in South Africa and Kenya, targeting gym-goers and CrossFit enthusiasts who prioritize post-workout protein synthesis; these formulations typically use whey or casein, which slow gastric emptying and enhance fluid retention but are unsuitable for intra-exercise consumption.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Functionality: Pre-Workout Gains as Timing Awareness Grows

Post-workout formulations commanded 45.15% market share in 2024, reflecting the historical positioning of sports drinks as recovery beverages consumed after exercise to replenish fluids and glycogen. However, pre-workout products are forecast to grow at 10.89% CAGR through 2030, the fastest rate among functionality segments, as consumer education on hydration timing improves and brands emphasize proactive rather than reactive consumption. Pre-workout drinks typically contain lower carbohydrate concentrations to accelerate gastric emptying and sodium to promote voluntary fluid intake and plasma volume expansion, positioning them as hydration primers rather than energy sources.

Intra-workout products, consumed during exercise, balance hydration and energy delivery with 6% carbohydrate formulations and multiple transportable carbohydrates to sustain exogenous carbohydrate oxidation during prolonged activity. The "Others" category is expanding as sports drinks reposition from niche athletic products to mainstream functional beverages consumed at work, during commutes, and in social settings. Brands that invest in consumer education, through packaging labels explaining usage timing, partnerships with fitness trainers and sports medicine professionals, and digital content demonstrating performance benefits, capture disproportionate share in the fast-growing pre-workout segment.

By Packaging Type: Sustainability Pressures Accelerate Metal Can Adoption

PET bottles accounted for a 97.02% market share in 2024, driven by their cost efficiency, lightweight nature, and compatibility with existing filling lines and distribution infrastructure. However, metal cans are expected to grow at a CAGR of 11.76% through 2030, marking the fastest growth rate among packaging formats. This growth is attributed to sustainability mandates, premium positioning, and increased on-premise consumption. While investments in recycling infrastructure aim to reduce virgin plastic usage and enhance the environmental profile of PET, consumer perception has not kept pace with technical advancements. In contrast, metal cans benefit from a perceived sustainability advantage, despite requiring higher energy for production and transport.

Glass bottles, aseptic packages, and disposable cups serve specific niche applications: glass bottles are used for premium positioning and returnable formats, aseptic packages cater to shelf-stable products that do not require refrigeration, and disposable cups are utilized for on-premise consumption at sports venues and events. The strategic opportunity lies in format innovation. For example, sachets, rovide portion control and lower per-unit costs, appealing to price-sensitive consumers and encouraging product trials. Additionally, dispensed formats, such as fountain machines in gyms, offices, and universities, help reduce packaging waste while creating recurring revenue streams.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Distribution Channel: On-Trade Revival Driven by Experience Economy

Off-trade channels captured 82.09% market share in 2024, reflecting the dominance of supermarkets, hypermarkets, convenience stores, and online retail in daily beverage purchases. However, on-trade is forecast to grow at a 10.94% CAGR through 2030, driven by experiential consumption, event partnerships, and the premiumization of out-of-home occasions. Tiger Brands expanded its general trade footprint to 91,000 stores in South Africa by fiscal 2024, targeting 130,000 by fiscal 2029, illustrating the infrastructure investment required to maintain off-trade dominance.

On-trade growth is concentrated in gyms, sports clubs, and event venues where consumption is immediate, and price sensitivity is lower, allowing brands to charge premiums and build loyalty through experiential marketing. THIRSTI's 4-year partnership renewal with the Comrades Marathon as Official Hydration Partner, supplying 2 million water sachets and 600,000 electrolyte sports drink sachets in 2024, exemplifies on-trade activation that converts trial into brand preference. Moreover, specialty stores (health food shops, sports nutrition retailers) and convenience stores serve distinct roles: specialty stores cater to informed consumers seeking specific formulations, while convenience stores capture impulse purchases and immediate consumption occasions. The strategic implication is that brands must adopt omnichannel strategies.

Geography Analysis

South Africa held 84.22% market share in 2024, reflecting its status as the continent's most developed sports drink market, with established retail infrastructure, high brand awareness, and a mature fitness culture. However, Nigeria is forecast to grow at 11.38% CAGR through 2030, the fastest rate among geographic segments, driven by demographics, urbanization, and rising disposable incomes. Coca-Cola's USD 1 billion investment commitment in Nigeria over 5 years, announced in September 2024, signals confidence in the country's long-term growth trajectory.

Egypt's food and beverage market is characterized by high inflation and significant growth potential, presenting opportunities for sports drinks within the broader functional nutrition trend. The nutritional supplements market, which encompasses sports drinks, is growing due to factors such as a large population, improving healthcare infrastructure, and strategic geopolitical advantages, including the Suez Canal's role in facilitating imports. Regulatory oversight for food supplements has transitioned from the National Food Safety Authority to the Egypt Medicines Agency (EDA), mandating the registration of all supplements and adherence to specified maximum vitamin and mineral levels. This regulatory shift has introduced compliance costs, benefiting established players with expertise in navigating regulatory requirements.

The strategic opportunity lies in establishing local manufacturing to circumvent import duties, cater to local flavor preferences, and generate employment. However, this approach necessitates significant capital investment and involves lengthy regulatory approval processes. The rest of Africa, including markets such as Kenya, Ghana, and Morocco, presents growth opportunities influenced by specific country dynamics: Kenya's fitness culture and athletics heritage, Ghana's expanding middle class, and Morocco's geographical proximity to European markets.

Competitive Landscape

The Africa sports drink market is concentrated, characterized by the presence of multinational companies such as Coca-Cola, PepsiCo, and Suntory, alongside agile local competitors and celebrity-backed entrants. Multinational companies utilize regional bottling networks, cold-chain infrastructure, and established brand equity to maintain their market share. However, their large-scale operations can lead to organizational inertia, which local players capitalize on through rapid product innovation, culturally relevant formulations, and technology-driven distribution strategies.

Opportunities exist in hypotonic formulations, which are scientifically proven to enhance hydration but are underrepresented in product portfolios. These formulations are designed to quickly replenish fluids and electrolytes, making them particularly suitable for athletes and individuals engaged in high-intensity activities. Additional potential lies in natural-ingredient sports drinks, such as those using coconut water or fruit juice bases. These beverages appeal to health-conscious consumers seeking clean-label products with fewer artificial additives.

Furthermore, protein-based recovery beverages aimed at gym-goers and CrossFit participants present a growing market. These products cater to the increasing demand for functional beverages that support muscle recovery and overall fitness goals. Emerging disruptors utilize celebrity endorsements, digital-first marketing strategies, and technology-driven distribution methods to bypass traditional retail channels. For example, companies employing micro-distribution platforms demonstrate how social media influence combined with advanced logistics technology can drive demand and access fragmented markets without relying on traditional bottling infrastructure.

Africa Sports Drinks Industry Leaders

PepsiCo, Inc.

Suntory Holdings Limited

The Coca-Cola Company

Tiger Brands Ltd.

Kingsley Beverages Ltd.

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- March 2025: iPRO Hydrate, a leading functional hydration brand, launched in South Africa, representing a key milestone in its global expansion strategy. This launch is supported by an exclusive partnership with Gordon Sweets, a reputable distributor serving independent retailers and the impulse sector. Based in Cape Town's Western Province, Gordon Sweets offers nationwide distribution, ensuring iPRO Hydrate's accessibility to consumers throughout the country.

- February 2025: BigTree Beverages Ltd, an independent subsidiary of the Trade Kings Group, introduced FIT by Vatra, a sports drink designed to support the fitness goals of athletes and enthusiasts in Zambia. This launch represents an important addition to the company’s beverage portfolio, emphasizing its focus on wellness and sports development in the region. FIT by Vatra is formulated to provide optimal hydration and replenishment, offering a balanced combination of essential minerals, carbohydrates, and electrolytes, with a controlled sugar content to enhance performance.

- December 2024: PRIME Hydration, a US-based energy drink brand, entered the West African market with its launch in Ghana and Nigeria. This expansion is facilitated through a strategic partnership with TradeDepot, a B2B buying platform recognized for its extensive retail network and distribution expertise.

Africa Sports Drinks Market Report Scope

Electrolyte-Enhanced Water, Hypertonic, Hypotonic, Isotonic, Protein-based Sport Drinks are covered as segments by Soft Drink Type. Aseptic packages, Metal Can, PET Bottles are covered as segments by Packaging Type. Convenience Stores, Online Retail, Specialty Stores, Supermarket/Hypermarket, Others are covered as segments by Sub Distribution Channel. Egypt, Nigeria, South Africa are covered as segments by Country.By Drink Type

| Isotonic |

| Hypertonic |

| Hypotonic |

| Electrolyte-Enhanced Water |

| Protein-based Sport Drinks |

By Functionality

| Pre-Workout |

| Intra-Workout |

| Post-Workout |

| Others |

By Packaging Type

| PET Bottles |

| Glass Bottles |

| Metal Can |

| Aseptic packages |

| Disposable Cups |

By Distribution Channel

| On-Trade | |

| Off-Trade | Supermarket/Hypermarket |

| Convenience Stores | |

| Specialty Stores | |

| Online Retail | |

| Other Distribution Channels |

By Country

| South Africa |

| Egypt |

| Nigeria |

| Rest of Africa |

| By Drink Type | Isotonic | |

| Hypertonic | ||

| Hypotonic | ||

| Electrolyte-Enhanced Water | ||

| Protein-based Sport Drinks | ||

| By Functionality | Pre-Workout | |

| Intra-Workout | ||

| Post-Workout | ||

| Others | ||

| By Packaging Type | PET Bottles | |

| Glass Bottles | ||

| Metal Can | ||

| Aseptic packages | ||

| Disposable Cups | ||

| By Distribution Channel | On-Trade | |

| Off-Trade | Supermarket/Hypermarket | |

| Convenience Stores | ||

| Specialty Stores | ||

| Online Retail | ||

| Other Distribution Channels | ||

| By Country | South Africa | |

| Egypt | ||

| Nigeria | ||

| Rest of Africa | ||

Need A Different Region or Segment?

Customize Now

Market Definition

- Carbonated Soft Drinks (CSDs) - Carbonated soft drinks (CSDs) refer to non-alcoholic beverages that are carbonated and typically flavored, containing dissolved carbon dioxide to create effervescence. These beverages commonly include cola, lemon-lime, orange, and various fruit-flavored sodas. Marketed in cans, bottles, or fountain dispense.

- Juices - We have considered packaged juices which encompass non-alcoholic beverages derived from fruits, vegetables, or a combination thereof, processed and sealed in various packaging formats such as bottles, cartons, or pouches. Excluding fresh juices, this market segment involves commercially prepared and preserved juices, often with added preservatives and flavors.

- Ready-to-Drink (RTD) Tea and RTD Coffee - Ready-to-Drink (RTD) tea and RTD coffee are pre-packaged, non-alcoholic beverages that are brewed and prepared for consumption without further dilution. RTD tea typically includes various tea varieties, infused with flavors and sweeteners, and comes in bottles, cans, or cartons. Similarly, RTD coffee involves pre-brewed coffee formulations, often mixed with milk, sugar, or flavorings, and is conveniently packaged for on-the-go consumption.

- Energy Drinks - Energy drinks are non-alcoholic beverages formulated to provide a quick boost of energy and alertness. Whereas, sports drinks are beverages designed to hydrate and replenish electrolytes, particularly after physical exertion, exercise, or intense activity

| Keyword | Definition |

|---|---|

| Carbonated Soft Drinks | Carbonated soft drinks (CSDs) are a combination of carbonated water and flavouring, sweetened by sugar or a non-sugar sweeteners. |

| Standard Cola | Standard Cola is defined as the original flavor of cola soda. |

| Diet Cola | A cola-based soft drink containing no or low amounts of sugar |

| Fruit Flavored Carbonates | A carbonated beverage prepared from fruit juice/fruit flavor with carbonated water and containing sugar, dextrose, invert sugar or liquid glucose either singly or in combination. It may contain peel oil and fruit essences. |

| Juice | Juice is a drink made from the extraction or pressing of the natural liquid contained in fruit and vegetables. |

| 100% Juice | Fruit/vegetable juice made from fruit in the form of its juice with no water added to make up the volume. It is not permitted to add sugars, sweeteners, preservatives, flavourings or colourings to fruit juice. |

| Juice Drinks (up to 24% Juice) | Fruit/vegetable juice drinks with up to 24% fruits/vegetable extract. |

| Nectars (25-99% Juice) | Juices that can have between 25 and 99% of fruit, with the minimum legal limits defined depending on the type of fruit |

| Juice concentrates | Juice Concentrates are those form of juices when most of this liquid is removed resulting in a thick, syrupy product known as juice concentrate. |

| RTD Coffee | Packaged coffee beverages that are sold in a prepared form and are ready for consumption at the time of purchase. |

| Iced Coffee | An iced coffee is a cold version of coffee, usually a combination of hot espresso and milk with ice added to it. |

| Cold Brew Coffee | Cold brew also called cold water extraction or cold pressing is made by steeping ground coffee in room-temperature water for several hours. |

| RTD Tea | Ready-to-drink (RTD) tea is a packaged tea product ready for immediate consumption without brewing or preparation |

| Iced Tea | Ice tea or iced tea is a drink made from tea without milk but with sugar and sometimes fruit flavourings, drunk cold. |

| Green Tea | Green tea is a tea beverage which promotes mental alertness, relieving digestive symptoms and promoting weight loss. |

| Herbal Tea | Herbal tea beverages are made from the infusion or decoction of herbs, spices, or other plant material in hot water. |

| Energy Drink | A type of drink containing stimulant compounds, usually caffeine, which is marketed as providing mental and physical stimulation. They may or may not be carbonated and may also contain sugar, other sweeteners, or herbal extracts, among numerous possible ingredients. |

| Sugar-free or Low-calories Energy Drinks | Sugar-free or Low-calories Energy Drinks are sugar-free, artificially sweetened energy drinks with few or no calories. |

| Traditional Energy Drink | Traditional Energy Drinks are functional soft drinks containing ingredients designed to boost the consumer's energy. |

| Natural/Oraganic Energy Drinks | Natural/Organic energy drinks are energy drinks free of artificial sweeteners and synthetic colorings. Instead, they contain naturally derived ingredients such as green tea, yerba mate, and botanical extracts. |

| Energy Shots | A small but highly concentrated energy drink that contains large amounts of caffeine and/or other stimulants. The quantity is comparatively smaller compared to energy drinks. |

| Sports Drink | Sports drinks are beverages designed specifically for the rapid supply of fluid, carbohydrates, and electrolytes before, during or after exercise. |

| Isotonic | Isotonic drinks contain similar concentrations of salt and sugar as in the human body, and are designed to quickly replace fluids lost during exercise but with an increase of carbohydrate. |

| Hypertonic | Hypertonic drinks have a higher concentration of salt and sugar than the human body. They are best drunk after exercise as it is important to replace glycogen levels quickly after exercise. |

| Hypotonic | Hypotonic drinks are designed to quickly replace fluids lost during exercise. They have very low carbohydrate content and a lower concentration of salt and sugar than the human body. |

| Electrolyte-Enhanced Water | Electrolyte water is water infused with electrically-charged minerals, such as sodium, potassium, calcium, and magnesium. |

| Protein-based Sport Drinks | Protein-based sports drinks are those sports drinks which has added protein in it that will improve performance and reduce muscle protein breakdown. |

| On-Trade | The on-trade refers to places that sell beverages for immediate consumption on the premises like bars, restaurants, and pubs |

| Off-Trade | Off-trade usually means places like liquor stores, supermarkets and other places where you don't consume the beverage right away. |

| Convenience Store | A retail business that provides the public with a convenient location to quickly purchase a wide variety of consumable products and services, generally food and gasoline. |

| Specialty store | A specialty store is a shop/store that carries a deep assortment of brands, styles, or models within a relatively narrow category of goods |

| Online Retail | Online retail is a type of eCommerce whereby a business sells goods or services directly to consumers from a website. |

| Aseptic Packaging | Aseptic packaging refers to the filling of a cold, commercially sterile product under sterile conditions into a presterilized container and closure under sterile conditions to form a seal that effectively excludes microorganisms. These includes tetra packs, cartons, pouches etc. |

| PET Bottle | PET bottle means a bottle made of polyethylene terephthalate. |

| Metal Cans | Metal containers made of aluminum or tin- plated or zinc-plated steel, which are commonly used for packaging food, beverages or other products. |

| Disposable Cups | Disposable Cup means a cup or other container designed for single use to serve beverages, such as water, cold drinks, hot drinks and alcoholic beverages. |

| Gen Z | A way of referring to the group of people who were born in the late 1990s and early 2000s. |

| Millenial | Anyone born between 1981 and 1996 (ages 23 to 38 in 2019) is considered a Millennial |

| Taurine | Taurine is an amino acid that supports immune health and nervous system function. |

| Bars & Pubs | It is a drinking establishment licensed to serve alcoholic drinks for consumption on the premises. |

| Café | It is a foodservice establishment serving refreshments (mainly coffee) and light meals. |

| On the go | It means doing / dealing with while busily engaged with something and not diverting plans in order to accommodate. |

| Internet Penetration | The Internet Penetration Rate corresponds to the percentage of the total population of a given country or region that uses the Internet. |

| Vending Machine | A machine that dispenses small articles such as food, drinks, or cigarettes when a coin or token is inserted |

| Discount store | A discount store or discounter offers a retail format in which products are sold at prices that are in principle lower than an actual or supposed "full retail price". Discounters rely on bulk purchasing and efficient distribution to keep down costs. |

| Clean Label | Clean label on the beverage market are drinks that are made from few ingredients of natural origin and are not or only slightly processed. |

| Caffeine | An alkaloid compound which is a stimulant of the central nervous system. It is mainly used recreationally, as a mild cognitive enhancer to increase alertness and attentional performance. |

| Extreme sport | Action sports, adventure sports or extreme sports are activities perceived as involving a high degree of risk. |

| High-intensity interval training | It incorporates several rounds that alternate between several minutes of high intensity movements to significantly increase the heart rate to at least 80% of one's maximum heart rate, followed by short periods of lower intensity movements. |

| Shelf life | The length of time for which an item remains usable, fit for consumption, or saleable. |

| Cream Soda | Cream soda is a sweet soft drink. Generally flavored with vanilla and based on the taste of an ice cream float |

| Root Beer | Root beer is a sweet North American soft drink traditionally made using the root bark of the sassafras tree Sassafras albidum or the vine of Smilax ornata as the primary flavor. Root beer is typically, but not exclusively, non-alcoholic, caffeine-free, sweet, and carbonated. |

| Vanilla Soda | A carbonated soft drink flavoured with vanilla. |

| Dairy-Free | A product that does not contain any milk or milk products from cows, sheep or goats. |

| Caffeine-Free Energy Drinks | Caffeine-free energy drinks rely on other ingredients to boost the energy. Popular choices include amino acids, B vitamins, and electrolytes. |

Need More Details on Market Definition?

Ask a Question

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: IDENTIFY KEY VARIABLES: In order to build a robust forecasting methodology, the variables and factors identified in Step 1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set, and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market-size estimations for the forecast years are in nominal terms. Inflation is not a part of the pricing, and the average selling price (ASP) is kept constant throughout the forecast period for each country.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables, and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated reports, custom consulting assignments, databases & subscription platforms

Get More Details On Research Methodology

Download PDF