Market Overview

| Study Period | 2017 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

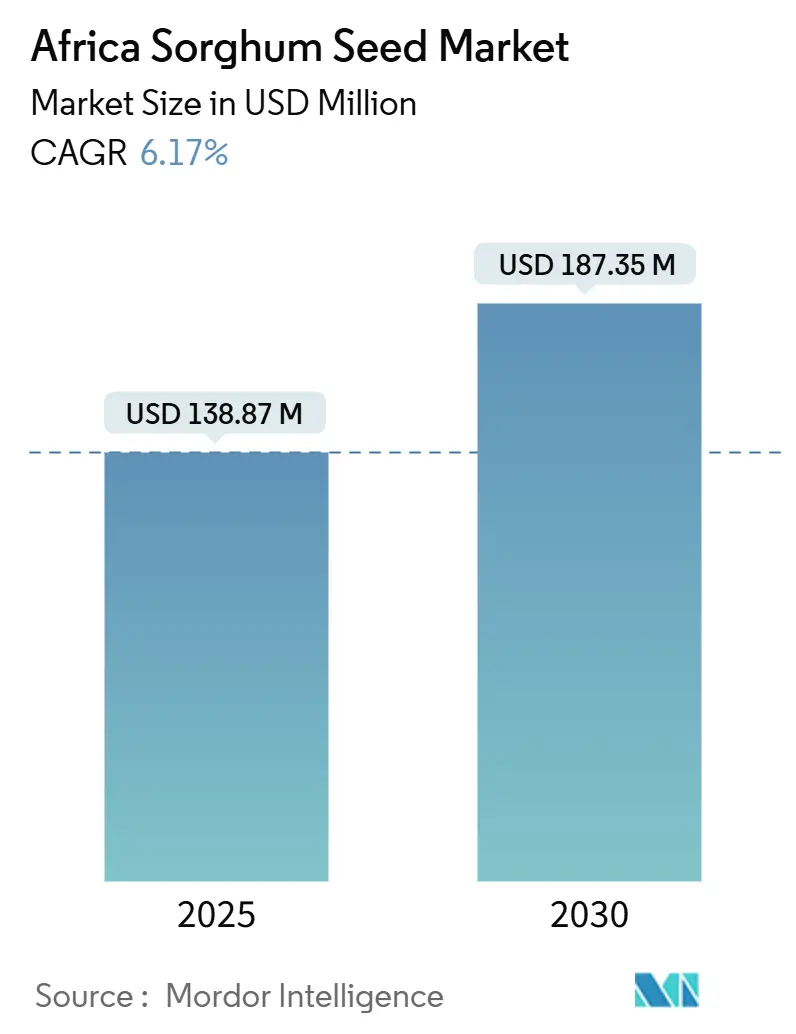

| Market Size (2025) | USD 138.87 Million |

| Market Size (2030) | USD 187.35 Million |

| Growth Rate (2025 - 2030) | 6.17% CAGR |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Africa Sorghum Seed Market Analysis by Mordor Intelligence

The Africa sorghum seed market size stands at USD 138.87 million in 2025 and is forecast to reach USD 187.35 million by 2030, advancing at a 6.17% CAGR. Demand rises as policymakers and farmers adopt drought-tolerant crops to cope with erratic rainfall, while brewing companies expand local sourcing contracts that guarantee price premiums for malting-quality grain. Formal seed channels gain traction through subsidy programs that offset the price gap between certified and farmer-saved seed. Hybrid breeding breakthroughs using genomic selection shorten variety-development cycles, enabling rapid release of Striga- and drought-resistant lines. Nigeria's National Agricultural Technology and Innovation Policy 2022-2027 specifically prioritizes sorghum value chain development, while Kenya's seed certification frameworks increasingly support hybrid variety registration. Regional seed firms retain distribution power, yet multinationals deepen their presence through joint ventures and local facilities.

Key Report Takeaways

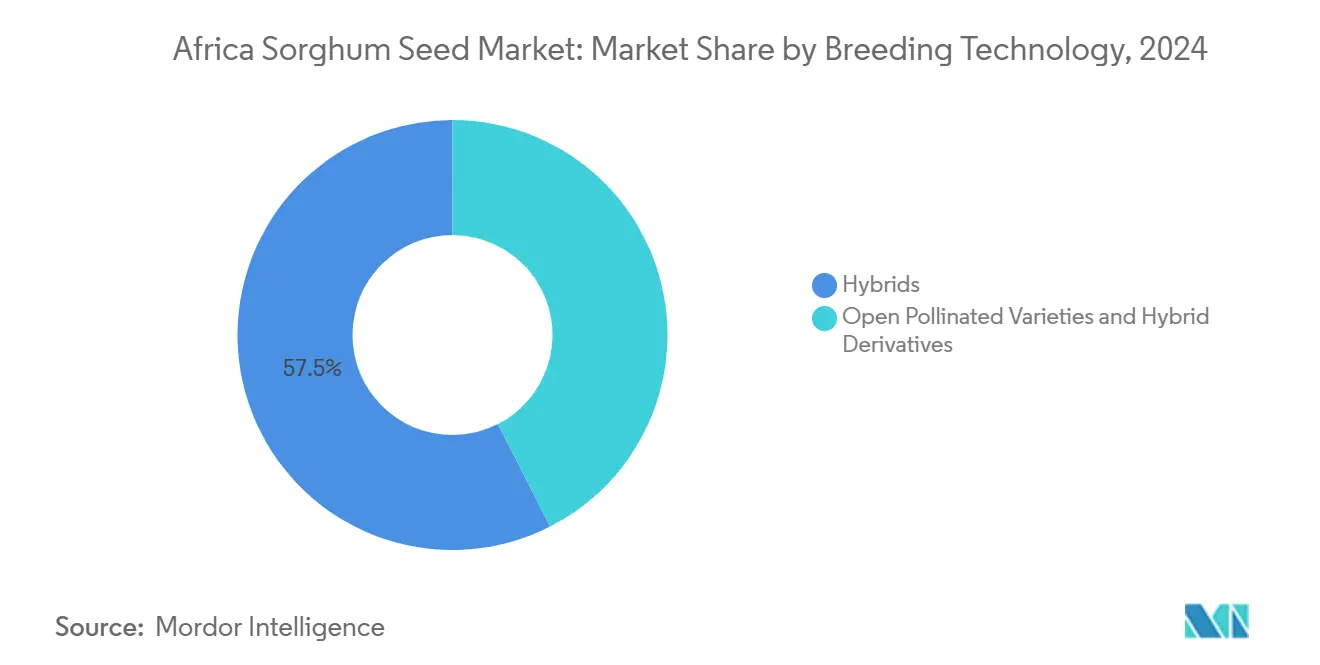

- By breeding technology, hybrids led with 57.5% of the Africa sorghum seed market size in 2024 and are projected to expand at a 6.66% CAGR through 2030.

- By geography, Nigeria accounted for 50.8% of the Africa sorghum seed market share in 2024, while Ghana records the fastest growth at 7.93% CAGR to 2030.

Africa Sorghum Seed Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for drought-tolerant hybrids | +1.8% | Nigeria, Ghana, Kenya, Ethiopia, and Tanzania | Medium term (2-4 years) |

| Government seed-subsidy programs | +1.2% | Nigeria, Kenya, Ghana, and South Africa | Short term (≤ 2 years) |

| Breweries' malt-sorghum pull | +0.9% | Kenya, Tanzania, Uganda, and Cameroon | Medium term (2-4 years) |

| Expansion of community seed enterprises | +0.7% | Ethiopia, Mali, Burkina Faso, and Senegal | Long term (≥ 4 years) |

| Genomic-selection acceleration | +0.6% | Global, with early gains in Kenya and Nigeria | Long term (≥ 4 years) |

| Climate-smart agriculture finance | +0.5% | Sub-Saharan Africa core, spill-over to North Africa | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Drought-Tolerant Hybrids

Climate variability drives unprecedented demand for drought-resilient sorghum varieties as rainfall patterns become increasingly unpredictable across Africa's semi-arid regions. Traditional sorghum cultivation areas now experience more frequent drought stress periods compared to historical averages, forcing farmers to seek varieties that maintain productivity under water-limited conditions. International Crops Research Institute for the Semi-Arid Tropics' (ICRISAT) genomic selection programs have accelerated the development of climate-adapted varieties, reducing breeding cycles from 10-12 years to 6-8 years through marker-assisted selection techniques[1]Source: International Crops Research Institute for the Semi-Arid Tropics, “Sorghum Research Programs,” Icrisat.org. This convergence of agronomic innovation and genetic improvement creates sustained demand for hybrid seed technologies across drought-prone African regions.

Government Seed-Subsidy Programs

National agricultural policies increasingly prioritize seed system strengthening through targeted subsidy mechanisms that reduce farmer adoption barriers for improved varieties. Nigeria's National Agricultural Technology and Innovation Policy 2022-2027 allocates substantial resources to sorghum value chain development, including seed multiplication and distribution support for smallholder farmers[2]Source: Federal Ministry of Agriculture and Rural Development, “National Agricultural Technology and Innovation Policy 2022-2027,” Fmard.gov.ng. Kenya's agricultural input subsidy programs provide cost reductions for certified seeds, significantly improving access to hybrid varieties among resource-constrained farmers. The effectiveness of these programs depends on coordination between seed certification agencies, agricultural extension services, and farmer organizations to ensure proper variety selection and agronomic support.

Breweries’ Malt-Sorghum Pull

Industrial demand from brewing companies creates premium market opportunities for sorghum producers, driving the adoption of specific varieties optimized for malting characteristics. Brewing industry expansion across Africa, driven by rising consumer incomes and urbanization, creates sustained demand for malting-quality sorghum that traditional food markets cannot provide. Companies like Guinness Nigeria and SABMiller's African operations increasingly source local sorghum to reduce import dependencies and support local agriculture. This industrial demand channel requires consistent quality standards and traceability systems that favor formal seed varieties over farmer-saved alternatives.

Expansion of Community Seed Enterprises

Community-based seed production models emerge as sustainable mechanisms for improving seed access while building local capacity and reducing distribution costs. These enterprises typically involve farmer groups or cooperatives that multiply certified seeds under technical supervision, then distribute them within their communities at reduced costs compared to commercial channels. Senegal's Senegal's PRODAC (Programme des Domaines Agricoles Communautaires) program demonstrates this model's effectiveness, where community agricultural domains combine modern farming techniques with local seed multiplication, enabling participating farmers to achieve double or triple their previous incomes.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Informal seed-system dominance | -1.5% | Sub-Saharan Africa, particularly rural areas | Long term (≥ 4 years) |

| Limited extension and credit | -1.1% | Nigeria, Ethiopia, Tanzania, and Mali | Medium term (2-4 years) |

| Slow GMO/CRISPR (Clustered Regularly Interspaced Short Palindromic Repeats) regulatory pathways | -0.8% | Most African countries, except Kenya and Nigeria | Long term (≥ 4 years) |

| Severe bird damage in the Savanna belts | -0.6% | Sahel region, East Africa savannas | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Informal Seed-System Dominance

Traditional seed-saving practices continue to supply 80-90% of smallholder seed requirements across Africa, creating structural barriers to formal seed market expansion and technology adoption. Farmers prefer saved seeds due to familiarity, cultural practices, and immediate cost advantages, despite potential yield penalties from genetic deterioration and disease accumulation. This preference reflects rational economic behavior, given that certified seeds often cost 3-5 times more than saved alternatives, while extension support for proper variety management remains limited. The informal system's resilience stems from its integration with local knowledge systems, social networks, and risk management strategies that formal seed channels struggle to replicate.

Limited Extension and Credit

Agricultural extension services reach fewer than 30% of smallholder farmers across most African countries, constraining technology transfer and proper agronomic support for improved seed varieties. Credit access remains equally limited, with formal financial institutions serving less than 20% of rural farmers, forcing reliance on informal lending at prohibitive interest rates. This dual constraint creates adoption barriers even when improved seeds are available and affordable, as farmers lack both technical knowledge and financial resources for complementary inputs like fertilizers and pest control measures. Digital extension platforms show promise for scaling technical support, but require significant infrastructure investments and farmer training programs. Mobile money systems and agricultural insurance products gradually improve financial inclusion, though coverage remains patchy across rural areas [3]Source: World Bank Group, “Agricultural Finance and Insurance,” Worldbank.org.

Segment Analysis

By Breeding Technology: Hybrids Drive Market Transformation

Hybrids captured 57.5% of the Africa sorghum seed market share in 2024 and are growing at 6.66% CAGR through 2030. This dominant position reflects superior stress tolerance and the rising affordability of hybrid seed as cytoplasmic male-sterility systems boost production efficiency. Hybrid traits such as Corteva’s Pioneer Protector stack drought tolerance with pest resistance, extending performance under variable rainfall. S&W Seed Company’s PF Trait eliminates prussic acid risk, opening forage segments previously restricted during drought.

Open-pollinated varieties remain prevalent where annual seed purchase budgets are limited, yet their share declines as climate events intensify and financing options expand. The Africa sorghum seed market size for hybrid derivatives is projected to climb steadily as researchers integrate nutritional enrichment traits into commercial seed lots. This technological differentiation supports premium pricing and strengthens hybrid varieties' competitive position against saved seed alternatives.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

Geography Analysis

Nigeria held 50.8% of the Africa sorghum seed market size in 2024 due to its grain output and policy priority for sorghum within the National Agricultural Technology and Innovation Policy. Strong domestic demand from breweries and food processors underpins seed replacement volumes. West Africa remains the core market. Nigeria’s leadership is reinforced by subsidy-backed seed distribution, and Ghana showcases a scalable public-private model linking growers to brewing conglomerates. Community seed hubs in Mali and Burkina Faso foster decentralized multiplication, though transport and storage infrastructure still curtail rapid growth.

Ghana posts the fastest 7.93% CAGR as modernization reforms and brewery contracts stimulate formal seed use. Ethiopia, Kenya, and Tanzania present sizable adoption potential where hybrid uptake hinges on extension coverage and credit. South Africa’s commercial farms provide high-value segments for trait-rich hybrids, while Egypt explores sorghum rotations to mitigate water scarcity. East Africa displays regulatory maturity. Kenya’s rigorous seed certification and partial subsidy scheme improve smallholder access. Ethiopia’s vast cultivation area commands volume, yet informal channels dominate.

Tanzania leverages cross-border trade routes to capture regional demand, and Uganda’s malt-grade initiatives echo Kenyan success. Southern Africa centers on South Africa’s commercialized system where premium hybrids target yield maximization. Zambia and Zimbabwe gain from Seed Co’s and other regional firms’ dealer networks that blend input finance with grain marketing. Trade protocols under the Southern African Development Community ease varietal movement, lowering unit cost and enhancing choice diversity.

Competitive Landscape

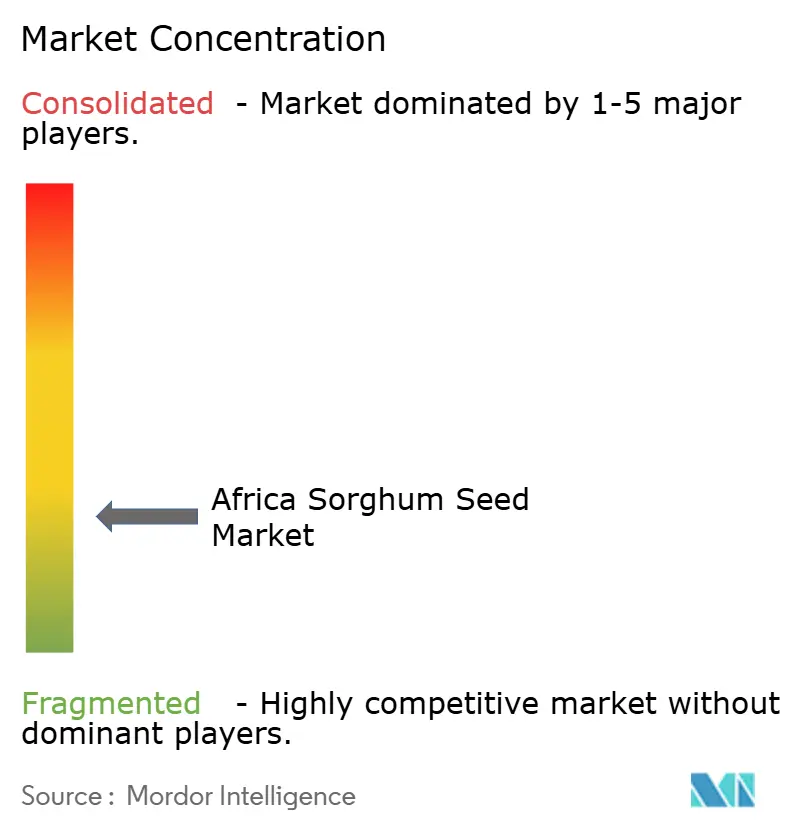

The Africa sorghum seed market exhibits fragmentation, with regional players dominating distribution networks while multinational companies expand through strategic partnerships and local facility investments. Seed Co Limited maintains the strongest regional presence across Southern and Eastern Africa, leveraging established dealer networks and local variety development capabilities to serve diverse market segments from commercial farmers to smallholder cooperatives.

International companies like Corteva Agriscience and Syngenta pursue market entry through technology licensing agreements and joint ventures rather than direct competition, recognizing the importance of local knowledge and distribution relationships in African seed markets. Technology differentiation increasingly drives competitive positioning as companies invest in genomic selection capabilities and trait development programs. UPL's Advanta Seeds division focuses on drought-tolerant varieties optimized for African growing conditions, while S&W Seed Company leverages proprietary traits like PF Trait for forage safety applications

Bayer's maize seed facility investment in Zambia signals a multinational commitment to African market development, though sorghum applications remain secondary to maize focus. Emerging opportunities exist in digital agriculture platforms and integrated pest management solutions that address bird damage challenges, with quelea control representing a significant unmet need across savanna production zones.

Africa Sorghum Seed Industry Leaders

-

FICA SEEDS

-

Seed Co Limited

-

Victoria Seeds Limited

-

Zambia Seed Company Limited (Zamseed)

-

Capstone Seeds Pty Ltd.

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- June 2025: Green 2000 and Senegal’s PRODAC scaled community agricultural domains across Kaolack, Kolda, and Saint-Louis, pairing improved sorghum seed with mechanization and market links.

- April 2025: S&W Seed Company, in collaboration with Purdue University, has developed the PF Trait, a non-GMO trait that creates prussic acid-free forage sorghum. This will eliminate prussic acid risk under drought and cold stress.

Africa Sorghum Seed Market Report Scope

Hybrids, Open Pollinated Varieties & Hybrid Derivatives are covered as segments by Breeding Technology. Egypt, Ethiopia, Ghana, Kenya, Nigeria, South Africa, Tanzania are covered as segments by Country.

Breeding Technology

| Hybrids | Non-Transgenic Hybrids |

| Open Pollinated Varieties & Hybrid Derivatives |

Geography

| Egypt |

| Ethiopia |

| Ghana |

| Kenya |

| Nigeria |

| South Africa |

| Tanzania |

| Rest of Africa |

| Breeding Technology | Hybrids | Non-Transgenic Hybrids |

| Open Pollinated Varieties & Hybrid Derivatives | ||

| Geography | Egypt | |

| Ethiopia | ||

| Ghana | ||

| Kenya | ||

| Nigeria | ||

| South Africa | ||

| Tanzania | ||

| Rest of Africa |

Need A Different Region or Segment?

Customize Now

Market Definition

- Commercial Seed - For the purpose of this study, only commercial seeds have been included as part of the scope. Farm-saved Seeds, which are not commercially labeled are excluded from scope, even though a minor percentage of farm-saved seeds are exchanged commercially among farmers. The scope also excludes vegetatively reproduced crops and plant parts, which may be commercially sold in the market.

- Crop Acreage - While calculating the acreage under different crops, the Gross Cropped Area has been considered. Also known as Area Harvested, according to the Food & Agricultural Organization (FAO), this includes the total area cultivated under a particular crop across seasons.

- Seed Replacement Rate - Seed Replacement Rate is the percentage of area sown out of the total area of crop planted in the season by using certified/quality seeds other than the farm-saved seed.

- Protected Cultivation - The report defines protected cultivation as the process of growing crops in a controlled environment. This includes greenhouses, glasshouses, hydroponics, aeroponics, or any other cultivation system that protects the crop against any abiotic stress. However, cultivation in an open field using plastic mulch is excluded from this definition and is included under open field.

| Keyword | Definition |

|---|---|

| Row Crops | These are usually the field crops which include the different crop categories like grains & cereals, oilseeds, fiber crops like cotton, pulses, and forage crops. |

| Solanaceae | These are the family of flowering plants which includes tomato, chili, eggplants, and other crops. |

| Cucurbits | It represents a gourd family consisting of about 965 species in around 95 genera. The major crops considered for this study include Cucumber & Gherkin, Pumpkin and squash, and other crops. |

| Brassicas | It is a genus of plants in the cabbage and mustard family. It includes crops such as carrots, cabbage, cauliflower & broccoli. |

| Roots & Bulbs | The roots and bulbs segment includes onion, garlic, potato, and other crops. |

| Unclassified Vegetables | This segment in the report includes the crops which don’t belong to any of the above-mentioned categories. These include crops such as okra, asparagus, lettuce, peas, spinach, and others. |

| Hybrid Seed | It is the first generation of the seed produced by controlling cross-pollination and by combining two or more varieties, or species. |

| Transgenic Seed | It is a seed that is genetically modified to contain certain desirable input and/or output traits. |

| Non-Transgenic Seed | The seed produced through cross-pollination without any genetic modification. |

| Open-Pollinated Varieties & Hybrid Derivatives | Open-pollinated varieties produce seeds true to type as they cross-pollinate only with other plants of the same variety. |

| Other Solanaceae | The crops considered under other Solanaceae include bell peppers and other different peppers based on the locality of the respective countries. |

| Other Brassicaceae | The crops considered under other brassicas include radishes, turnips, Brussels sprouts, and kale. |

| Other Roots & Bulbs | The crops considered under other roots & bulbs include Sweet Potatoes and cassava. |

| Other Cucurbits | The crops considered under other cucurbits include gourds (bottle gourd, bitter gourd, ridge gourd, Snake gourd, and others). |

| Other Grains & Cereals | The crops considered under other grains & cereals include Barley, Buck Wheat, Canary Seed, Triticale, Oats, Millets, and Rye. |

| Other Fibre Crops | The crops considered under other fibers include Hemp, Jute, Agave fibers, Flax, Kenaf, Ramie, Abaca, Sisal, and Kapok. |

| Other Oilseeds | The crops considered under other oilseeds include Ground nut, Hempseed, Mustard seed, Castor seeds, safflower seeds, Sesame seeds, and Linseeds. |

| Other Forage Crops | The crops considered under other forages include Napier grass, Oat grass, White clover, Ryegrass, and Timothy. Other forage crops were considered based on the locality of the respective countries. |

| Pulses | Pigeon peas, Lentils, Broad and horse beans, Vetches, Chickpeas, Cowpeas, Lupins, and Bambara beans are the crops considered under pulses. |

| Other Unclassified Vegetables | The crops considered under other unclassified vegetables include Artichokes, Cassava Leaves, Leeks, Chicory, and String beans. |

Need More Details on Market Definition?

Ask a Question

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: IDENTIFY KEY VARIABLES: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market-size estimations for the forecast years are in nominal terms. Inflation is not a part of the pricing, and the average selling price (ASP) is kept constant throughout the forecast period.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases, and Subscription Platforms

Get More Details On Research Methodology

Download PDF