Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

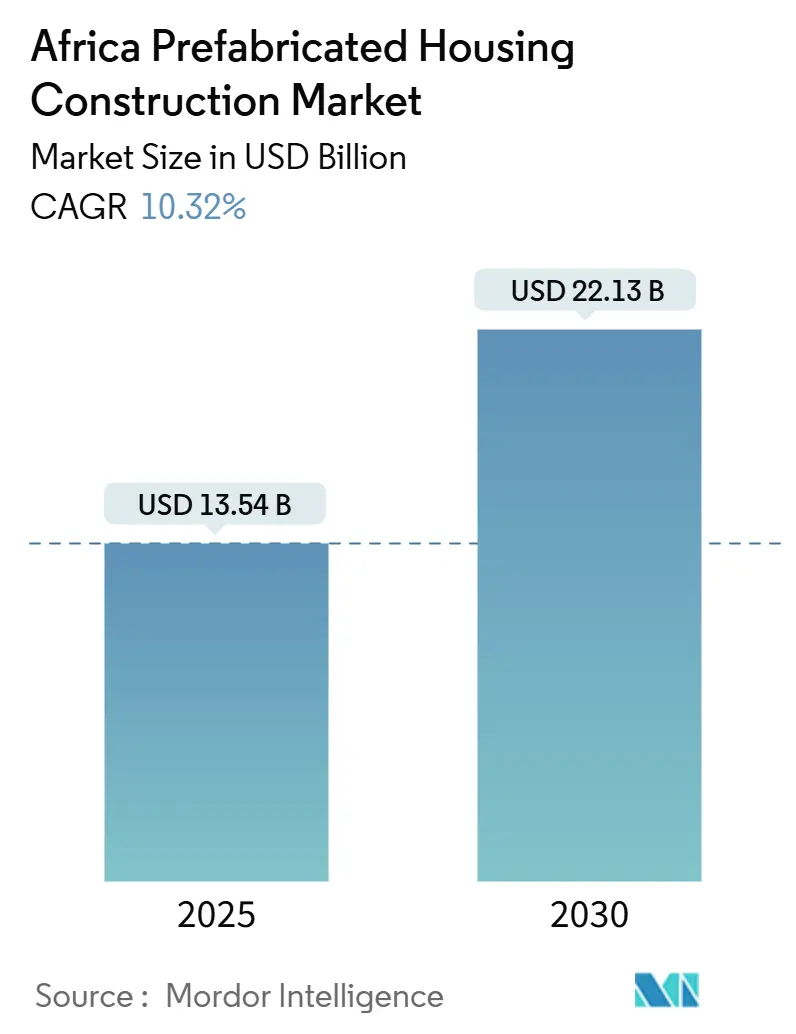

| Market Size (2025) | USD 13.54 Billion |

| Market Size (2030) | USD 22.13 Billion |

| Growth Rate (2025 - 2030) | 10.32% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Africa Prefabricated Housing Construction Market Analysis by Mordor Intelligence

The Africa prefabricated housing construction market size stands at USD 13.54 billion in 2025 and is on track to reach USD 22.13 billion by 2030, reflecting a robust 10.32% CAGR over the forecast period. A decisive shift from informal, labor-intensive site work to factory-produced modular and panelized systems is shortening build times, improving quality control, and offsetting chronic shortages of skilled trades. Concrete-based systems retained the largest 44.5% revenue share in 2024, yet timber and engineered-wood solutions are gaining traction as governments embed embodied-carbon caps in public tenders, while multi-family projects in Lagos, Cairo, and Johannesburg accelerate amid surging land prices. Competition is intensifying as Chinese state-owned enterprises (SOEs) export modular integrated construction expertise, European hire specialists expand rental fleets into healthcare and education, and domestic manufacturers tap Africa Finance Corporation (AFC) special-economic-zone financing to localize panel production. Currency volatility, fragmented permitting, and import-driven cost premiums remain near-term headwinds; however, blended-finance structures from the International Finance Corporation (IFC) and sovereign affordable-housing funds are widening the addressable pool of bankable projects.

Key Report Takeaways

- By material, concrete led with 44.5% of Africa's prefabricated housing construction market share in 2024, while timber solutions are forecast to expand at an 11.12% CAGR through 2030.

- By housing type, single-family formats commanded 56.1% of Africa's prefabricated housing construction market size in 2024, whereas multi-family deliveries are projected to grow at an 11.67% CAGR to 2030.

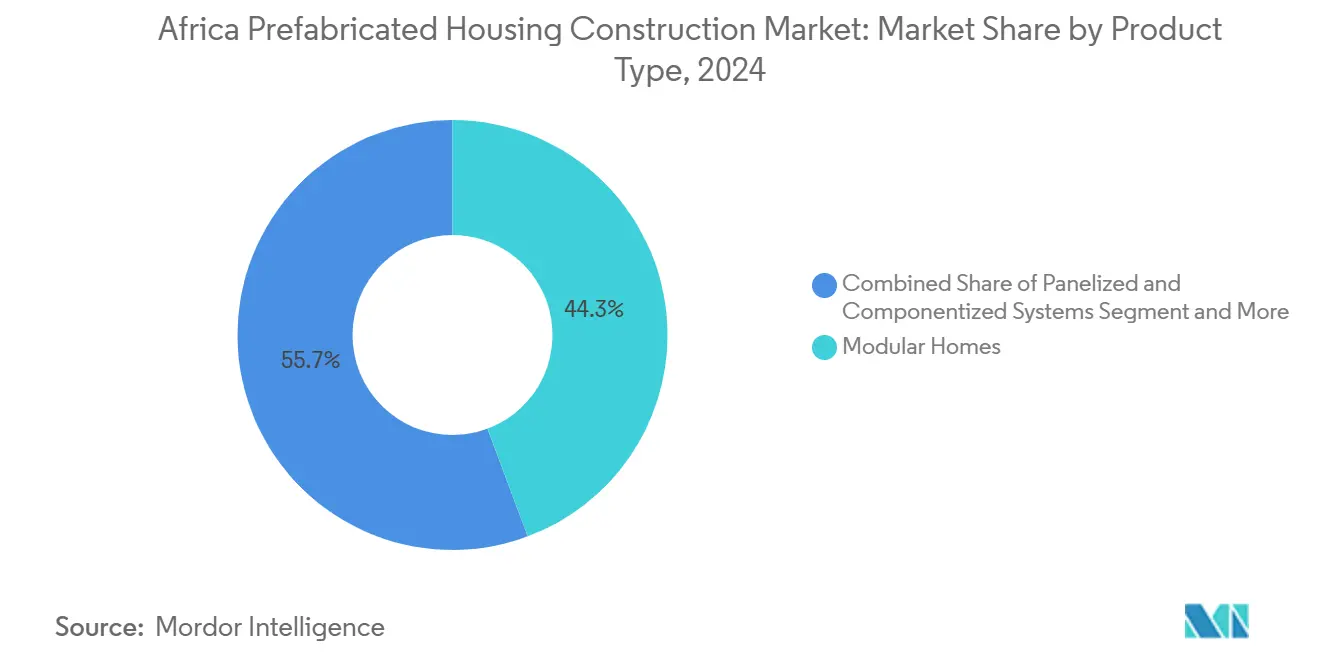

- By product, modular homes held 44.3% revenue share in 2024 and are set to advance at a 12.03% CAGR, the fastest among all prefab formats.

- By geography, Nigeria generated 29.2% of 2024 revenue, yet Egypt is poised for the highest national growth at a 12.44% CAGR between 2025 and 2030.

Africa Prefabricated Housing Construction Market Trends and Insights

Drivers Impact Analysis

| Drivers | (~) % IMPACT ON CAGR FORECAST | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid urbanization and housing deficits in major cities creating demand for fast, scalable delivery | 2.8% | Nigeria, Egypt, Kenya, South Africa; spillover to Ethiopia, DRC, Tanzania | Medium term (2-4 years) |

| Government affordable housing programs and PPPs opening pipelines for standardized prefab units | 2.4% | Nigeria (FHFL, MOFI), Egypt (SHMFF), Kenya (Affordable Housing Levy), Côte d'Ivoire, Senegal | Short term (≤ 2 years) |

| Offsite construction shortening build times and reducing costs amid skilled labor constraints | 1.9% | Global; acute in South Africa, Nigeria, Ghana, Kenya where informality exceeds 80% | Medium term (2-4 years) |

| Disaster relief, conflict resettlement, and climate adaptation needs favoring modular, relocatable homes | 1.3% | Sahel (Mali, Niger, Burkina Faso), Horn of Africa (Somalia, South Sudan), coastal zones (Mozambique, Madagascar) | Long term (≥ 4 years) |

| Growing investor interest in rental, staff housing, and student accommodation using industrialized methods | 1.2% | South Africa (mining belts), Nigeria (Lagos, Port Harcourt oil sector), Kenya (Nairobi student housing), Egypt (New Administrative Capital) | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid Urbanization And Housing Deficits In Major Cities Creating Demand For Fast, Scalable Delivery

Africa’s urban population is projected to hit 1.4 billion by 2050, with just four countries—Nigeria, Egypt, Ethiopia, and the Democratic Republic of Congo—contributing one-third of that growth. Nigeria alone faces a 28-million-unit housing shortfall, and the continent collectively needs 53 million additional dwellings, widening a USD 1 trillion financing gap. Densities above 50,000 people per square kilometer in Lagos, Cairo, and Johannesburg have pushed land values to levels where modular systems that require lighter foundations and minimal excavation deliver decisive cost savings. Governments now favor suppliers able to complete projects within 60-90 days and guarantee repeatability at scale, positioning factories with bulk off-take agreements to outcompete project-by-project contractors.

Government Affordable Housing Programs And PPPs Opening Pipelines For Standardized Prefab Units

Kenya’s Affordable Housing Act of 2024 imposes a 1.5% payroll levy matched by employers, creating a ring-fenced fund empowered to award transparent turnkey contracts[1]Clyde & Co LLP, “A Highlight of Kenya’s Affordable Housing Act, 2024,” clydeco.com. Nigeria channels capital through Federal Housing Finance Limited, while Egypt’s Social Housing and Mortgage Finance Fund has delivered 840,000 units to date. Côte d’Ivoire, backed by IFC transaction advisory, targets 150,000 units by 2025, and Senegal has published a World Bank-reviewed procurement plan inviting prefab bids. These initiatives de-risk factory investment by ensuring multi-year demand, though local-content thresholds and technology-transfer clauses require foreign entrants to adopt joint-venture or licensing models. Collectively, they add 2.8% to the Africa prefabricated housing construction market CAGR forecast by guaranteeing predictable volume for standardized designs.

Offsite Construction Shortening Build Times And Reducing Costs Amid Skilled-Labor Constraints

Informality covers 82% of Africa’s construction workforce, eroding productivity and safety. Offsite fabrication shifts value into controlled factories, cutting on-site labor requirements by up to 70% and enabling quality audits before shipment. China State Construction Engineering Corporation (CSCEC) achieved 92% prefabrication on a Beijing project, trimming six months from schedule, and is transplanting that modular integrated construction approach to Egypt’s New Administrative Capital. Holcim’s 14Trees venture printed a Malawi school and the first 10 units of the Mvule Gardens project in Kenya in half the traditional timeframe, securing EDGE Advanced certification. In South Africa, suppliers with Agrément approvals bypass repetitive on-site inspections, further compressing cycle times. These demonstrations validate time and cost savings, reinforcing adoption curves and contributing 2.1% to the CAGR outlook.

Disaster Relief, Conflict Resettlement, And Climate Adaptation Needs Favoring Modular, Relocatable Homes

Seventy percent of refugees originate from climate-vulnerable nations, creating structural demand for rapidly deployable shelters. Red Sea Housing’s factory in Accra manufactures modular units that humanitarian agencies can redeploy between crises, reducing life-cycle costs by up to 40% compared with single-use tents. Cyclone-prone Mozambique and Madagascar require elevated foundations and reinforced anchoring, adding 10-15% to unit costs yet allowing specialist suppliers to carve out premium niches. Dual-use designs that comply with UNHCR and mining-camp standards enable manufacturers to diversify revenue streams and smooth commodity-cycle volatility. These factors lift the market growth trajectory by an additional 1.5% over the long term.

Restraints Impact Analysis

| Restraints | (~) % IMPACT ON CAGR FORECAST | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited local manufacturing depth and imported component reliance raising delivered costs and lead times | -1.6% | Nigeria, Kenya, Tanzania, Ghana; less acute in South Africa, Egypt with established precast industries | Short term (≤ 2 years) |

| Fragmented regulations, permitting variability, and building-code gaps slowing approvals and uptake | -1.2% | Pan-African; acute in Francophone West Africa, Lusophone markets with limited code enforcement | Medium term (2-4 years) |

| Financing barriers—low mortgage penetration, high rates, and limited developer capital—constraining scale | -1.4% | Nigeria (0.6% penetration), WAEMU (<2% of GDP), Kenya, Tanzania; less acute in South Africa, Egypt with established mortgage markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Limited Local Manufacturing Depth And Imported Component Reliance Raising Delivered Costs And Lead Times

Precision components—insulated panels, welded mesh, and high-spec joinery—remain largely imported, inflating landed costs by 15-25% relative to brick-and-mortar in Nigeria and Kenya[2]Africa Finance Corporation, “ARISE IIP and AFC Launch USD 100M Capital Pool for African Entrepreneurs,” africafc.org. Kenya’s National Housing Corporation opened an EPS plant to feed its 110,000-unit pipeline, yet capacity shortfalls still necessitate freighted panels from Asia at more than USD 200 per cubic meter. South Africa’s mature precast sector lessens exposure, but even certified suppliers import sealants and fasteners from Europe. AFC’s USD 100 million special-economic-zone program finances new panel lines, although commissioning typically takes 18-24 months. These structural gaps shave 1.8% off forecast growth until meaningful localization gains momentum after 2026.

Fragmented Regulations, Permitting Variability, And Building-Code Gaps Slowing Approvals And Uptake

Fifty-four national jurisdictions enforce disparate building codes; Kenya still references a 2009 framework, Ghana rolled out a 2018 edition, and Rwanda applies 2015 standards, while cross-border recognition is scant. ARSO is drafting continental guidelines, and ISO released a working document on prefab terminology, yet adoption lags procurement schedules. Inspectors unfamiliar with modular systems often reject non-traditional designs, adding 6-12 months to approvals. South Africa’s Agrément certification reduces this to four to six weeks, providing a model other nations could emulate, but legislative amendments and training budgets are thin. Resultant delays strip an estimated 1.3% from the Africa prefabricated housing construction market CAGR through 2029.

Segment Analysis

By Material Type: Concrete Retains Leadership While Timber Gains Sustainable Momentum

Concrete accounted for 44.5% of Africa's prefabricated housing construction market share in 2024, favored for fire resistance, affordability, and code familiarity. Holcim’s ECOPact low-carbon mix delivered EDGE-certified units in Kenya’s Mvule Gardens, showing concrete can meet green mandates without sacrificing structural integrity. The segment benefits from widespread cement capacity, local aggregates, and established supply chains that dampen currency risk. However, engineered-wood products—cross-laminated timber (CLT) and glue-laminated beams—are set to log an 11.12% CAGR, the fastest in the category, as carbon-pricing pilots and municipal incentives spread to Johannesburg and Nairobi. Mass Timber Technology’s precision-cut CLT panels already qualify for South African tax rebates that trim property levies by up to 15%.

Growing environmental scrutiny and rapid installation advantages are driving pilot adoptions in mid-rise residential blocks. Arup’s East Africa study confirms CLT offers 40-50% lower embodied carbon than reinforced concrete, and local plantation pine sources in Tanzania could enable price parity by 2027. Concrete is expected to defend its dominance through incremental innovation, such as geopolymer blends, while timber’s upside will hinge on scaling kiln capacity, fire-testing regimes, and third-party certifications analogous to Agrément. Combined, these dynamics keep concrete ahead on volume, yet position timber as the sustainability-led growth engine within the Africa prefabricated housing construction market.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Housing Type: Single-Family Still Commands Bulk Volume, Yet Multi-Family Surges

Single-family homes captured 56.1% of Africa's prefabricated housing construction market size in 2024, driven by rural and peri-urban plots where land remains inexpensive, and buyers value privacy. Egypt’s Social Housing and Mortgage Finance Fund nonetheless channels most new deliveries into 4- to 6-story walk-ups that maximize density within subsidized land envelopes. Multi-family formats are forecast to grow at an 11.67% CAGR—the fastest in the category—propelled by plots in central Nairobi already priced above USD 500 per square meter and Lagos districts where site preparation alone can top USD 50 per square meter.

Developers exploit factory repetition advantages: a 100-unit block requires only eight to ten module types, trimming tooling changeovers and slashing lead times to around 14 weeks. Kenya’s EPS panels reduce foundation loads by up to 40%, enabling builds on marginal soils without costly pilings. South Africa’s N2 Gateway demonstrates that densities of 80-100 units per hectare are feasible while meeting SANS 10400 fire-safety norms. As urban density climbs, government procurement is expected to concentrate on multi-family typologies, reducing per-unit subsidy requirements and accelerating volume gains in the Africa prefabricated housing construction market.

By Product Type: Modular Homes Deliver Speed and Reusability

Modular systems held 44.3% of revenue in 2024, underpinned by turnkey interiors shipped directly from the factory. CSCEC’s MiC towers in Egypt’s New Administrative Capital prove the model scales to six-story heights and cuts six months off conventional timelines. The format is projected to expand at a 12.03% CAGR, outpacing panelized and manufactured-home alternatives. Rental specialist Kwikspace keeps 170-plus units circulating among mining and infrastructure sites, showing that reusability offsets the 15-20% rental premium many customers pay for rapid deployment.

Panelized kits carve out a flexible middle ground, with Robust Structures’ expanded-metal core wall panels certified by Agrément and Miami-Dade, weighing just 3.6 kg/m²—light enough for manual handling yet strong enough for cyclone regions. Manufactured homes remain constrained by financing rules that classify them as personal property, limiting mortgage support. Hybrid timber-steel and 3D-printed variants sit at the pilot stage; nonetheless, Holcim’s TectorPrint ink in Malawi indicates promising routes to mass-customizable façades. Overall, modularity’s proven schedule gains and relocation economics keep it the centerpiece of growth strategies across the Africa prefabricated housing construction market.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

Geography Analysis

Egypt will post the fastest national growth at a 12.44% CAGR through 2030, buoyed by the Ministry of Housing’s standardized typologies and 840,000 units already delivered under the Social Housing and Mortgage Finance Fund. In February 2025, the government offered another 400,000 units, including a USD 2.3 billion first-phase project in Hadayek October, locking in significant volume for prefab suppliers[3]Egypt Ministry of Housing, “Housing for All Egyptians Initiative,” moh.gov.eg. Chinese SOEs are erecting modular towers in the New Administrative Capital, while domestic manufacturers still import precision joinery that lifts delivered costs 15-25%, a gap the AFC’s special-economic-zone program aims to close by 2027.

Nigeria retained 29.2% of the 2024 Africa prefabricated housing construction market revenue on the back of a 28-million-unit deficit and federal funding channeled through FHFL and the Real Estate Investment Fund. Lafarge Africa’s partnership with Shelter Afrique underpins steady cement demand, yet mortgage penetration stuck at 0.6% compels developers to rely on equity or high-interest short-term loans, eroding returns. EPS and plastic-formwork pilots are proving cost-competitive at USD 250 per square meter, but forex volatility and port congestion continue to weigh on project schedules.

South Africa benefits from a transparent regulatory environment anchored by the National Home Builders Registration Council and Agrément pathways. Robust Structures, BHC Steel, and Concor Buildings possess pre-approved systems that cut permitting to six weeks, a key edge in public tenders. The Housing Development Agency’s N2 Gateway handed over 12,000 units, and the private Barlow Park redevelopment houses more than 1,000 residents after a USD 11 million investment. Elsewhere, Kenya, Ghana, and Senegal are rolling out payroll levies, PPP frameworks, and IFC-structured transactions, yet still wrestle with code fragmentation and component import dependencies that may ease only after local panel lines come online post-2026.

Competitive Landscape

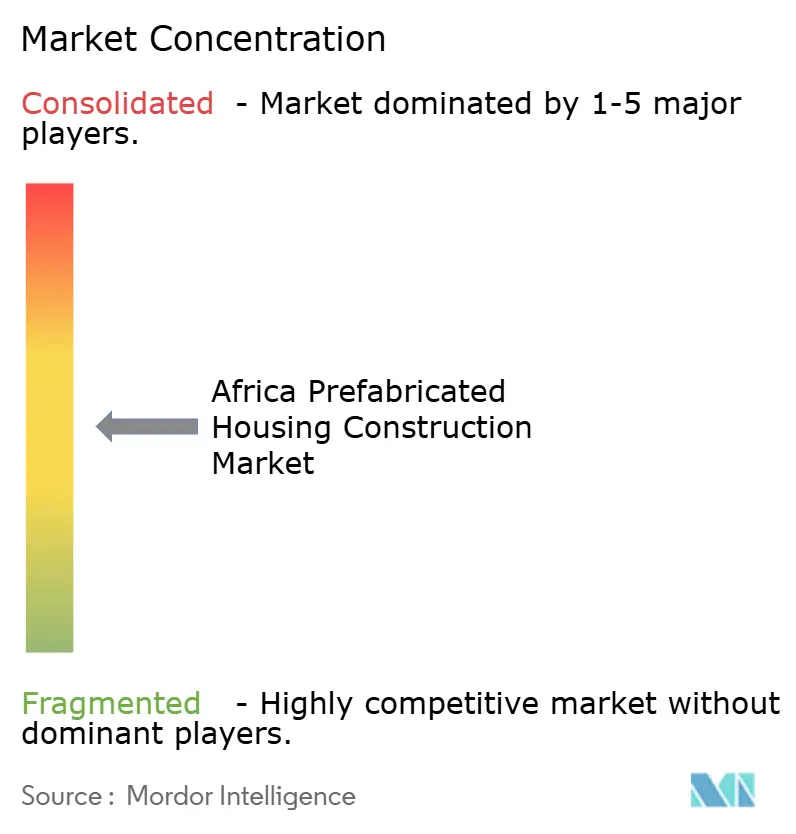

Competition in the Africa prefabricated housing construction market is moderate, with more than 20 active firms jockeying for multi-year affordable-housing contracts, mining-camp fleets, and humanitarian tenders. European hire specialists such as Algeco are leveraging their Moduflex design, which claims 73% lower embodied carbon and 96% recyclability, to win education and healthcare bids requiring rapid, code-compliant deployment. Chinese SOEs—chiefly CSCEC—bring deep R&D budgets (USD 6.5 billion in 2023) and 68,000-plus patents that translate into turnkey EPC offerings, transferring technical risk away from ministries poorly staffed with engineers.

Domestic capacity is rising as AFC financing incentivizes panel production within special economic zones. Robust Structures continues to license its expanded-metal cores across Zimbabwe, Zambia, and Namibia, while Kenya’s National Housing Corporation’s new EPS factory expands its role from developer to component supplier. Hire-fleet models, typified by Kwikspace’s operations in South Africa, Mozambique, and Zambia, offer asset-light flexibility and high utilization rates, contrasting with capital-heavy factories betting on government pipeline certainty. Certification remains a battleground: firms securing Agrément or equivalent approvals compress approvals to 4-6 weeks, accelerating cash conversion and raising barriers for late entrants.

Strategic alliances are proliferating. Holcim’s 14Trees venture marries low-carbon concrete with COBOD printers, producing EDGE Advanced-certified structures that appeal to donor-funded schools and climate-resilient pilot programs. Red Sea Housing leverages its Ghana facility to serve both humanitarian agencies and extractive-sector clients, balancing cyclical demand. Meanwhile, start-ups focusing on CLT and hybrid timber-steel systems are courting city governments keen on embodied-carbon reductions. Against this backdrop, scale economics, certification speed, and financing links to PPP programs are emerging as the decisive levers for long-term share capture.

Africa Prefabricated Housing Construction Industry Leaders

-

Moladi

-

Red Sea Housing Services

-

Karmod Prefabricated Technologies

-

Algeco (Modulaire Group)

-

Portakabin

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- January 2025: China State Construction Engineering Corporation executives visited the Central Business District project in Egypt's New Administrative Capital, inspecting progress on modular residential towers that apply the company's Modular Integrated Construction (MiC) techniques, which achieved 92% prefabrication in Beijing projects and reduce build time by 6 months.

- January 2025: The World Bank published a procurement plan for Senegal's Affordable Housing Program (Project P174759), detailing procurement schedules, goods/works/services, prior review thresholds, and contractual modalities for prefabricated housing suppliers and contractors seeking opportunities in the West Africa region.

- January 2025: Innovative Modular Concepts received Agrément South Africa approval for its container-based modular building system, validating the design for commercial deployment and compressing permitting timelines from 6-9 months to 4-6 weeks in South African markets.

- July 2024: ARISE IIP and Africa Finance Corporation signed a memorandum of understanding to create a USD 100 million capital pool to finance African entrepreneurs establishing operations within ARISE IIP Special Economic Zones across 11 countries (Benin, Togo, Gabon, Côte d'Ivoire, Nigeria, Republic of Congo, DRC, Sierra Leone, Malawi, Rwanda, Chad), with AFC mobilizing additional financing from Export Credit Agencies and providing equipment financing, market-entry support, and technical partnerships.

Africa Prefabricated Housing Construction Market Report Scope

Prefabricated homes, often called prefab homes, are primarily manufactured in advance off-site, then delivered and assembled on-site. The report covers a complete assessment of the Africa Prefabricated Housing Market. It includes an assessment of the economy market overview, market size estimation for key segments, and emerging trends in the market segments. The report sheds light on the market trends like growth factors, restraints, and opportunities in this sector. The competitive landscape of the Africa Prefabricated Housing Market is depicted through the profiles of active key players. The report also covers the impact of COVID-19 on the market and future projections.

The Africa Prefabricated Housing Market is segmented by type (single-family and multi-family) and country (Nigeria, Egypt, South Africa, and the Rest of Africa). The report offers market sizes and forecasts in value (USD) for all the above segments.

By Material Type

| Concrete |

| Glass |

| Metal |

| Timber |

| Other Materials |

By Housing Type

| Single-Family |

| Multi-Family |

By Product Type

| Modular Homes |

| Panelized & Componentized Systems |

| Manufactured Homes |

| Other Prefab Types |

By Country

| Nigeria |

| Egypt |

| South Africa |

| Rest of Africa |

| By Material Type | Concrete |

| Glass | |

| Metal | |

| Timber | |

| Other Materials | |

| By Housing Type | Single-Family |

| Multi-Family | |

| By Product Type | Modular Homes |

| Panelized & Componentized Systems | |

| Manufactured Homes | |

| Other Prefab Types | |

| By Country | Nigeria |

| Egypt | |

| South Africa | |

| Rest of Africa |

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the current value of the Africa prefabricated housing construction market and its expected growth?

The Africa prefabricated housing construction market size is USD 13.54 billion in 2025 and is projected to reach USD 22.13 billion by 2030, registering a 10.32% CAGR.

Which material dominates prefabricated housing across Africa?

Concrete leads with 44.5% 2024 market share, though timber systems are the fastest-growing on an 11.12% CAGR path.

Which country is forecast to grow the fastest for prefab housing?

Egypt is expected to expand at 12.44% CAGR through 2030, driven by large-scale government programs and modular tower projects.

Why are modular homes gaining popularity over panelized variants?

Modular units arrive factory-finished, cut schedules by up to six months, and can be redeployed or stacked, giving them the highest projected CAGR at 12.03%.

What are the biggest hurdles slowing prefab adoption?

Imported components raise costs 15-25%, and fragmented building codes add 6-12 months to permitting in many markets, trimming growth potential.

How are governments supporting local prefab manufacturing?

Programs such as AFC’s USD 100 million special-economic-zone fund and Kenya’s EPS panel factory financing aim to localize production and reduce import dependence.