North America Pet Nutraceuticals Market Size

| Icons | Lable | Value |

|---|---|---|

|

|

Study Period | 2017 - 2029 |

|

|

Market Size (2024) | USD 2.27 Billion |

|

|

Market Size (2029) | USD 2.99 Billion |

|

|

Largest Share by Pets | Dogs |

|

|

CAGR (2024 - 2029) | 5.66 % |

|

|

Largest Share by Country | United States |

|

|

Market Concentration | Medium |

Major Players |

||

|

|

||

|

*Disclaimer: Major Players sorted in alphabetical order. |

North America Pet Nutraceuticals Market Analysis

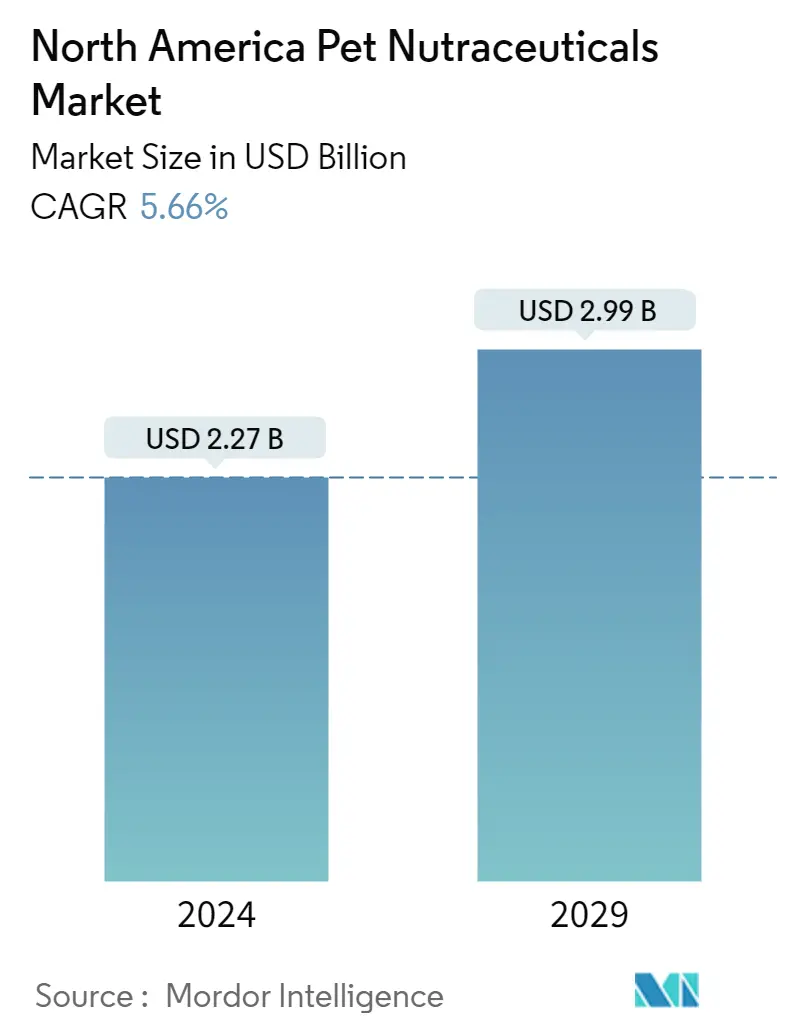

The North America Pet Nutraceuticals Market size is estimated at USD 2.27 billion in 2024, and is expected to reach USD 2.99 billion by 2029, growing at a CAGR of 5.66% during the forecast period (2024-2029).

2.27 Billion

Market Size in 2024 (USD)

2.99 Billion

Market Size in 2029 (USD)

2.42 %

CAGR (2017-2023)

5.66 %

CAGR (2024-2029)

Largest Market by Sub product

26.17 %

value share, Vitamins and Minerals, 2022

Rising pet health concerns have boosted the demand for vitamins and minerals in the region, as these supplements help promote metabolism and immunity in pets.

Largest Market by Country

88.71 %

value share, United States, 2022

Increasing pet ownership and growing interest among pet owners in natural and functional products, such as vitamins, minerals, and probiotics, have boosted the US market.

Fastest-growing Market by Sub Product

6.35 %

Projected CAGR, Vitamins and Minerals, 2023-2029

Rising pet populations and the ability of vitamins and minerals to regulate pet body functions and increase disease resistance will likely bolster their demand during the forecast period.

Fastest-growing Market by Country

9.42 %

Projected CAGR, Mexico, 2023-2029

Rising pet ownership rates, the growing trend of urbanization, and the increasing demand for high-quality and custom-made nutraceuticals have boosted the market in the country.

Leading Market Player

24.04 %

market share, Nestle (Purina), 2022

Nestle (Purina) is the market leader, as the company has focused on innovating new specific pet health products and expanding its manufacturing facilities in the region.

Dogs are the major consumers of nutraceuticals as they are susceptible to many health problems, such as joint problems and digestive issues

- Pet nutraceuticals are supplements that are specifically formulated to improve the health and well-being of pets. In 2022, they accounted for 2.8% of the North American pet food market. The share of nutraceuticals increased by 9.9% in 2022 compared to 2017, mainly due to the increasing awareness among pet owners about the importance of preventive healthcare. In 2021, a study revealed that four in 10 cat and dog owners in the United States had paid more attention to their pet's health since the start of the pandemic.

- Dogs accounted for the majority of the nutraceuticals market, valued at USD 1.24 billion, followed by cats and other pet animals at USD 581.4 million and USD 226 million, respectively. The larger share of dogs is mainly due to their larger population compared to other pets. In 2022, there were 144 million dogs in the region, while cats and other pet animals accounted for 96.5 million and 104.9 million, respectively. The United States has the largest pet population in the region, accounting for 69% (239 million). Additionally, dogs are known to suffer from a wider range of health issues, such as joint problems, skin allergies, and digestive issues, which has led to increased demand for nutraceuticals in the region. Joint/mobility, vitamin deficiency, general health, skin coat, and immunity are among the most popular conditions where pet owners are spending money on both dogs and cats.

- The growing trend of humanization among pet owners, the aging pet population, growing specialized needs, and the rise of e-commerce channels are the major factors driving the market, and it is projected to register a CAGR of 5.0% during the forecast period.

The United States dominated the nutraceutical market, with vitamins and minerals as major nutraceuticals

- The North American pet nutraceuticals market has witnessed significant growth and is expected to continue this trend over the forecast period. One of the primary drivers of this growth is the increasing pet humanization trend, where pet owners are increasingly treating their pets as family members and focusing on their overall health and well-being.

- The United States dominated the market, and it accounted for 88.7% of the North American pet nutraceutical market value in 2022. The dominance of the United States is mainly due to its higher pet population in the country, with 239.1 million pets in 2022, which is about 69.2% of the North American pet population. With this huge pet population, the US pet nutraceuticals market value is anticipated to record a CAGR of 5.0% during the forecast period.

- Canada has the second-largest market share, accounting for USD 126.4 million in 2022. It has the second-largest share because of lower households adopting pets than the pets adopted in the United States. The country is expected to record a CAGR of 9.0% during the forecast period as there is an increase in awareness about pet health and growing pet expenditure. For instance, the pet population in Canada was 28.3 million in 2022.

- Mexico accounted for about 3.8% of the market share in 2022. The limited market share of the country is mainly due to the limited pet population in the country. However, with the rising trend in pet humanization, it is anticipated to register a CAGR of 9.4% during the forecast period.

- The pet nutraceuticals market in Rest of North America is anticipated to record a CAGR of 10.5% during the forecast period. The growing focus of pet owners on pet health and well-being is anticipated to boost the market during the forecast period.

North America Pet Nutraceuticals Market Trends

The increasing adoption of cats by young adults and millennials is driving the cat food market

- There is an increase in the adoption of cats as pets in North America owing to the high demand for companionship and lesser expenditure on pet food for cats than dogs. In the region, cats as pets increased by 13.6% between 2017 and 2022 due to a rise in pet humanization and because cats require less area to live than dogs. For instance, in the United States, households owning a cat as a pet was 26% in 2020, which increased to 53.5% in 2022.

- The United States, Canada, and Mexico witnessed higher adoption of cats as pets during the pandemic because of the work-from-home culture leading to a demand for companionship and a higher number of pet owners being millennials. For instance, in 2022, millennials amounted to 33% of pet parents in the United States. In 2020, 40% of the pet cat population was adopted from animal shelters in the United States. Additionally, pet parents purchased cats from pet stores due to high income, and in 2020, 43% of cat parents in the United States purchased cats from pet stores. Therefore, cats as pets in the region increased by 5.34% between 2020 and 2022.

- Young cats are being adopted more than adult cats in the region, with the United States leading in terms of that number. For instance, in 2021, the adopted cat population in the United States was 684,144, and young cats accounted for 53.5% of the cats adopted. The higher population of young cats and millennials being pet parents is expected to help in the growth of pet food products during the forecast period. An increase in the adoption and purchase of cats and an increase in pet humanization are expected to help in the growth of the pet population.

Dogs accounted for higher expenditure as they consume a larger quantity of food than cats and have higher susceptibility to digestive issues

- Pet expenditure is increasing in North America. The rise in pet expenditure is due to the availability of different types of pet food and the growing premiumization of pet food products in the United States and Canada. Pet expenditure is projected to increase as pet parents increasingly treat their pets as family members and the awareness about specialized pet food rises. In 2020, there was a rise in pet supplement sales by about 200% as pet parents wanted their pets to have higher immunity and improved digestive systems, in line with greater awareness about pet health needs.

- The highest expenses of pet parents are on pet food, which is estimated to increase during the forecast period. For instance, pet food accounted for 42.4% of pet expenses in the United States in 2022. The expenditure share of dog food is higher than that of cats because the dog population is higher and because they consume a larger quantity of food than cats. Pet parents provide premium pet food to their pets and use services such as pet grooming and pet daycare in the region as they consider them as family members. In the United States, about 40% of pet parents purchased premium pet food, and USD 11.4 billion was spent on services such as pet grooming and pet walking in 2022.

- Pet parents purchase pet food through online retailers, supermarkets, and pet stores. Higher pet food sales are generated through online retailers as a variety of pet food products are available on e-commerce sites; also, the pandemic increased the number of online orders. In the United States, online sales of pet care products, including food, increased from 32% in 2020 to 40% in 2022. Premiumization and rising awareness about the benefits of quality food are factors anticipated to boost pet expenditure in the region.

OTHER KEY INDUSTRY TRENDS COVERED IN THE REPORT

- Growing acquisition of dogs from animal shelters and the evolving pet ecosystem are boosting the market growth

- Low maintenance and comfort are driving the adoption of other pets

North America Pet Nutraceuticals Industry Overview

The North America Pet Nutraceuticals Market is moderately consolidated, with the top five companies occupying 56.78%. The major players in this market are ADM, Mars Incorporated, Nestle (Purina), Schell & Kampeter Inc. (Diamond Pet Foods) and Vetoquinol (sorted alphabetically).

North America Pet Nutraceuticals Market Leaders

ADM

Mars Incorporated

Nestle (Purina)

Schell & Kampeter Inc. (Diamond Pet Foods)

Vetoquinol

Other important companies include Alltech, Clearlake Capital Group, L.P. (Wellness Pet Company Inc.), Dechra Pharmaceuticals PLC, Nutramax Laboratories Inc., Virbac.

*Disclaimer: Major Players sorted in alphabetical order.

North America Pet Nutraceuticals Market News

- February 2023: ADM opened its new probiotics and postbiotics production facility in Spain. The facility will supply these supplements to North America, EMEA, and Asia-Pacific.

- January 2023: Wellness Pet Company Inc., a subsidiary of Clearlake Capital Group LP, launched a fresh range of supplements designed for dogs, which prioritize providing daily health advantages to promote overall well-being. These products help meet the proactive approach of pet parents for long-term health and well-being.

- January 2023: Mars Incorporated partnered with the Broad Institute to create an open-access database of dog and cat genomes to advance preventive pet care. It is aimed at developing more effective precision medicines and diets that lead to scientific breakthroughs for the future of pet health.

Free with this Report

We provide a complimentary and exhaustive set of data points on regional and country-level metrics that present the fundamental structure of the industry. Presented in the form of 90+ free charts, the section covers difficult-to-find data from various countries regarding the expenditure on different pet food products including food, treats, veterinary diets, and nutraceuticals/supplements.

North America Pet Nutraceuticals Market Report - Table of Contents

EXECUTIVE SUMMARY & KEY FINDINGS

REPORT OFFERS

1. INTRODUCTION

1.1. Study Assumptions & Market Definition

1.2. Scope of the Study

1.3. Research Methodology

2. KEY INDUSTRY TRENDS

2.1. Pet Population

2.1.1. Cats

2.1.2. Dogs

2.1.3. Other Pets

2.2. Pet Expenditure

2.3. Regulatory Framework

2.4. Value Chain & Distribution Channel Analysis

3. MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2029 and analysis of growth prospects)

3.1. Sub Product

3.1.1. Milk Bioactives

3.1.2. Omega-3 Fatty Acids

3.1.3. Probiotics

3.1.4. Proteins and Peptides

3.1.5. Vitamins and Minerals

3.1.6. Other Nutraceuticals

3.2. Pets

3.2.1. Cats

3.2.2. Dogs

3.2.3. Other Pets

3.3. Distribution Channel

3.3.1. Convenience Stores

3.3.2. Online Channel

3.3.3. Specialty Stores

3.3.4. Supermarkets/Hypermarkets

3.3.5. Other Channels

3.4. Country

3.4.1. Canada

3.4.2. Mexico

3.4.3. United States

3.4.4. Rest of North America

4. COMPETITIVE LANDSCAPE

4.1. Key Strategic Moves

4.2. Market Share Analysis

4.3. Company Landscape

4.4. Company Profiles

4.4.1. ADM

4.4.2. Alltech

4.4.3. Clearlake Capital Group, L.P. (Wellness Pet Company Inc.)

4.4.4. Dechra Pharmaceuticals PLC

4.4.5. Mars Incorporated

4.4.6. Nestle (Purina)

4.4.7. Nutramax Laboratories Inc.

4.4.8. Schell & Kampeter Inc. (Diamond Pet Foods)

4.4.9. Vetoquinol

4.4.10. Virbac

5. KEY STRATEGIC QUESTIONS FOR PET FOOD CEOS

6. APPENDIX

6.1. Global Overview

6.1.1. Overview

6.1.2. Porter’s Five Forces Framework

6.1.3. Global Value Chain Analysis

6.1.4. Market Dynamics (DROs)

6.2. Sources & References

6.3. List of Tables & Figures

6.4. Primary Insights

6.5. Data Pack

6.6. Glossary of Terms

List of Tables & Figures

- Figure 1:

- PET POPULATION OF CATS, NUMBER, NORTH AMERICA, 2017 - 2022

- Figure 2:

- PET POPULATION OF DOGS, NUMBER, NORTH AMERICA, 2017 - 2022

- Figure 3:

- PET POPULATION OF OTHER PETS, NUMBER, NORTH AMERICA, 2017 - 2022

- Figure 4:

- PET EXPENDITURE PER CAT, USD, NORTH AMERICA, 2017 - 2022

- Figure 5:

- PET EXPENDITURE PER DOG, USD, NORTH AMERICA, 2017 - 2022

- Figure 6:

- PET EXPENDITURE PER OTHER PET, USD, NORTH AMERICA, 2017 - 2022

- Figure 7:

- VOLUME OF PET NUTRACEUTICALS/SUPPLEMENTS, METRIC TON, NORTH AMERICA, 2017 - 2029

- Figure 8:

- VALUE OF PET NUTRACEUTICALS/SUPPLEMENTS, USD, NORTH AMERICA, 2017 - 2029

- Figure 9:

- VOLUME OF PET NUTRACEUTICALS/SUPPLEMENTS BY SUB PRODUCT CATEGORIES, METRIC TON, NORTH AMERICA, 2017 - 2029

- Figure 10:

- VALUE OF PET NUTRACEUTICALS/SUPPLEMENTS BY SUB PRODUCT CATEGORIES, USD, NORTH AMERICA, 2017 - 2029

- Figure 11:

- VOLUME SHARE OF PET NUTRACEUTICALS/SUPPLEMENTS BY SUB PRODUCT CATEGORIES, %, NORTH AMERICA, 2017 VS 2023 VS 2029

- Figure 12:

- VALUE SHARE OF PET NUTRACEUTICALS/SUPPLEMENTS BY SUB PRODUCT CATEGORIES, %, NORTH AMERICA, 2017 VS 2023 VS 2029

- Figure 13:

- VOLUME OF MILK BIOACTIVES, METRIC TON, NORTH AMERICA, 2017 - 2029

- Figure 14:

- VALUE OF MILK BIOACTIVES, USD, NORTH AMERICA, 2017 - 2029

- Figure 15:

- VALUE SHARE OF MILK BIOACTIVES BY DISTRIBUTION CHANNEL, %, NORTH AMERICA, 2022 AND 2029

- Figure 16:

- VOLUME OF OMEGA-3 FATTY ACIDS, METRIC TON, NORTH AMERICA, 2017 - 2029

- Figure 17:

- VALUE OF OMEGA-3 FATTY ACIDS, USD, NORTH AMERICA, 2017 - 2029

- Figure 18:

- VALUE SHARE OF OMEGA-3 FATTY ACIDS BY DISTRIBUTION CHANNEL, %, NORTH AMERICA, 2022 AND 2029

- Figure 19:

- VOLUME OF PROBIOTICS, METRIC TON, NORTH AMERICA, 2017 - 2029

- Figure 20:

- VALUE OF PROBIOTICS, USD, NORTH AMERICA, 2017 - 2029

- Figure 21:

- VALUE SHARE OF PROBIOTICS BY DISTRIBUTION CHANNEL, %, NORTH AMERICA, 2022 AND 2029

- Figure 22:

- VOLUME OF PROTEINS AND PEPTIDES, METRIC TON, NORTH AMERICA, 2017 - 2029

- Figure 23:

- VALUE OF PROTEINS AND PEPTIDES, USD, NORTH AMERICA, 2017 - 2029

- Figure 24:

- VALUE SHARE OF PROTEINS AND PEPTIDES BY DISTRIBUTION CHANNEL, %, NORTH AMERICA, 2022 AND 2029

- Figure 25:

- VOLUME OF VITAMINS AND MINERALS, METRIC TON, NORTH AMERICA, 2017 - 2029

- Figure 26:

- VALUE OF VITAMINS AND MINERALS, USD, NORTH AMERICA, 2017 - 2029

- Figure 27:

- VALUE SHARE OF VITAMINS AND MINERALS BY DISTRIBUTION CHANNEL, %, NORTH AMERICA, 2022 AND 2029

- Figure 28:

- VOLUME OF OTHER NUTRACEUTICALS, METRIC TON, NORTH AMERICA, 2017 - 2029

- Figure 29:

- VALUE OF OTHER NUTRACEUTICALS, USD, NORTH AMERICA, 2017 - 2029

- Figure 30:

- VALUE SHARE OF OTHER NUTRACEUTICALS BY DISTRIBUTION CHANNEL, %, NORTH AMERICA, 2022 AND 2029

- Figure 31:

- VOLUME OF PET NUTRACEUTICALS/SUPPLEMENTS BY PET TYPE, METRIC TON, NORTH AMERICA, 2017 - 2029

- Figure 32:

- VALUE OF PET NUTRACEUTICALS/SUPPLEMENTS BY PET TYPE, USD, NORTH AMERICA, 2017 - 2029

- Figure 33:

- VOLUME SHARE OF PET NUTRACEUTICALS/SUPPLEMENTS BY PET TYPE, %, NORTH AMERICA, 2017 VS 2023 VS 2029

- Figure 34:

- VALUE SHARE OF PET NUTRACEUTICALS/SUPPLEMENTS BY PET TYPE, %, NORTH AMERICA, 2017 VS 2023 VS 2029

- Figure 35:

- VOLUME OF PET CAT NUTRACEUTICALS/SUPPLEMENTS, METRIC TON, NORTH AMERICA, 2017 - 2029

- Figure 36:

- VALUE OF PET CAT NUTRACEUTICALS/SUPPLEMENTS, USD, NORTH AMERICA, 2017 - 2029

- Figure 37:

- VALUE SHARE OF PET CAT NUTRACEUTICALS/ SUPPLEMENTS BY PET NUTRACEUTICALS/ SUPPLEMENTS CATEGORIES, %, NORTH AMERICA, 2022 AND 2029

- Figure 38:

- VOLUME OF PET DOG NUTRACEUTICALS/SUPPLEMENTS, METRIC TON, NORTH AMERICA, 2017 - 2029

- Figure 39:

- VALUE OF PET DOG NUTRACEUTICALS/SUPPLEMENTS, USD, NORTH AMERICA, 2017 - 2029

- Figure 40:

- VALUE SHARE OF PET DOG NUTRACEUTICALS/ SUPPLEMENTS BY PET NUTRACEUTICALS/ SUPPLEMENTS CATEGORIES, %, NORTH AMERICA, 2022 AND 2029

- Figure 41:

- VOLUME OF OTHER PETS NUTRACEUTICALS/SUPPLEMENTS, METRIC TON, NORTH AMERICA, 2017 - 2029

- Figure 42:

- VALUE OF OTHER PETS NUTRACEUTICALS/SUPPLEMENTS, USD, NORTH AMERICA, 2017 - 2029

- Figure 43:

- VALUE SHARE OF OTHER PETS NUTRACEUTICALS/ SUPPLEMENTS BY PET NUTRACEUTICALS/ SUPPLEMENTS CATEGORIES, %, NORTH AMERICA, 2022 AND 2029

- Figure 44:

- VOLUME OF PET NUTRACEUTICALS/SUPPLEMENTS SOLD VIA DISTRIBUTION CHANNELS, METRIC TON, NORTH AMERICA, 2017 - 2029

- Figure 45:

- VALUE OF PET NUTRACEUTICALS/SUPPLEMENTS SOLD VIA DISTRIBUTION CHANNELS, USD, NORTH AMERICA, 2017 - 2029

- Figure 46:

- VOLUME SHARE OF PET NUTRACEUTICALS/SUPPLEMENTS SOLD VIA DISTRIBUTION CHANNELS, %, NORTH AMERICA, 2017 VS 2023 VS 2029

- Figure 47:

- VALUE SHARE OF PET NUTRACEUTICALS/SUPPLEMENTS SOLD VIA DISTRIBUTION CHANNELS, %, NORTH AMERICA, 2017 VS 2023 VS 2029

- Figure 48:

- VOLUME OF PET NUTRACEUTICALS/SUPPLEMENTS SOLD VIA CONVENIENCE STORES, METRIC TON, NORTH AMERICA, 2017 - 2029

- Figure 49:

- VALUE OF PET NUTRACEUTICALS/SUPPLEMENTS SOLD VIA CONVENIENCE STORES, USD, NORTH AMERICA, 2017 - 2029

- Figure 50:

- VALUE SHARE OF PET NUTRACEUTICALS/ SUPPLEMENTS SOLD VIA CONVENIENCE STORES BY SUB PRODUCT CATEGORIES, %, NORTH AMERICA, 2022 AND 2029

- Figure 51:

- VOLUME OF PET NUTRACEUTICALS/SUPPLEMENTS SOLD VIA ONLINE CHANNEL, METRIC TON, NORTH AMERICA, 2017 - 2029

- Figure 52:

- VALUE OF PET NUTRACEUTICALS/SUPPLEMENTS SOLD VIA ONLINE CHANNEL, USD, NORTH AMERICA, 2017 - 2029

- Figure 53:

- VALUE SHARE OF PET NUTRACEUTICALS/ SUPPLEMENTS SOLD VIA ONLINE CHANNEL BY SUB PRODUCT CATEGORIES, %, NORTH AMERICA, 2022 AND 2029

- Figure 54:

- VOLUME OF PET NUTRACEUTICALS/SUPPLEMENTS SOLD VIA SPECIALTY STORES, METRIC TON, NORTH AMERICA, 2017 - 2029

- Figure 55:

- VALUE OF PET NUTRACEUTICALS/SUPPLEMENTS SOLD VIA SPECIALTY STORES, USD, NORTH AMERICA, 2017 - 2029

- Figure 56:

- VALUE SHARE OF PET NUTRACEUTICALS/ SUPPLEMENTS SOLD VIA SPECIALTY STORES BY SUB PRODUCT CATEGORIES, %, NORTH AMERICA, 2022 AND 2029

- Figure 57:

- VOLUME OF PET NUTRACEUTICALS/SUPPLEMENTS SOLD VIA SUPERMARKETS/HYPERMARKETS, METRIC TON, NORTH AMERICA, 2017 - 2029

- Figure 58:

- VALUE OF PET NUTRACEUTICALS/SUPPLEMENTS SOLD VIA SUPERMARKETS/HYPERMARKETS, USD, NORTH AMERICA, 2017 - 2029

- Figure 59:

- VALUE SHARE OF PET NUTRACEUTICALS/ SUPPLEMENTS SOLD VIA SUPERMARKETS/HYPERMARKETS BY SUB PRODUCT CATEGORIES, %, NORTH AMERICA, 2022 AND 2029

- Figure 60:

- VOLUME OF PET NUTRACEUTICALS/SUPPLEMENTS SOLD VIA OTHER CHANNELS, METRIC TON, NORTH AMERICA, 2017 - 2029

- Figure 61:

- VALUE OF PET NUTRACEUTICALS/SUPPLEMENTS SOLD VIA OTHER CHANNELS, USD, NORTH AMERICA, 2017 - 2029

- Figure 62:

- VALUE SHARE OF PET NUTRACEUTICALS/ SUPPLEMENTS SOLD VIA OTHER CHANNELS BY SUB PRODUCT CATEGORIES, %, NORTH AMERICA, 2022 AND 2029

- Figure 63:

- VOLUME OF PET NUTRACEUTICALS/SUPPLEMENTS BY COUNTRY, METRIC TON, NORTH AMERICA, 2017 - 2029

- Figure 64:

- VALUE OF PET NUTRACEUTICALS/SUPPLEMENTS BY COUNTRY, USD, NORTH AMERICA, 2017 - 2029

- Figure 65:

- VOLUME SHARE OF PET NUTRACEUTICALS/SUPPLEMENTS BY COUNTRY, %, NORTH AMERICA, 2017 VS 2023 VS 2029

- Figure 66:

- VALUE SHARE OF PET NUTRACEUTICALS/SUPPLEMENTS BY COUNTRY, %, NORTH AMERICA, 2017 VS 2023 VS 2029

- Figure 67:

- VOLUME OF PET NUTRACEUTICALS/SUPPLEMENTS, METRIC TON, CANADA, 2017 - 2029

- Figure 68:

- VALUE OF PET NUTRACEUTICALS/SUPPLEMENTS, USD, CANADA, 2017 - 2029

- Figure 69:

- VALUE SHARE OF PET NUTRACEUTICALS/ SUPPLEMENTS BY SUB PRODUCT, %, CANADA, 2022 AND 2029

- Figure 70:

- VOLUME OF PET NUTRACEUTICALS/SUPPLEMENTS, METRIC TON, MEXICO, 2017 - 2029

- Figure 71:

- VALUE OF PET NUTRACEUTICALS/SUPPLEMENTS, USD, MEXICO, 2017 - 2029

- Figure 72:

- VALUE SHARE OF PET NUTRACEUTICALS/ SUPPLEMENTS BY SUB PRODUCT, %, MEXICO, 2022 AND 2029

- Figure 73:

- VOLUME OF PET NUTRACEUTICALS/SUPPLEMENTS, METRIC TON, UNITED STATES, 2017 - 2029

- Figure 74:

- VALUE OF PET NUTRACEUTICALS/SUPPLEMENTS, USD, UNITED STATES, 2017 - 2029

- Figure 75:

- VALUE SHARE OF PET NUTRACEUTICALS/ SUPPLEMENTS BY SUB PRODUCT, %, UNITED STATES, 2022 AND 2029

- Figure 76:

- VOLUME OF PET NUTRACEUTICALS/SUPPLEMENTS, METRIC TON, REST OF NORTH AMERICA, 2017 - 2029

- Figure 77:

- VALUE OF PET NUTRACEUTICALS/SUPPLEMENTS, USD, REST OF NORTH AMERICA, 2017 - 2029

- Figure 78:

- VALUE SHARE OF PET NUTRACEUTICALS/ SUPPLEMENTS BY SUB PRODUCT, %, REST OF NORTH AMERICA, 2022 AND 2029

- Figure 79:

- MOST ACTIVE COMPANIES BY NUMBER OF STRATEGIC MOVES, COUNT, NORTH AMERICA, 2017 - 2023

- Figure 80:

- MOST ADOPTED STRATEGIES, COUNT, NORTH AMERICA, 2017 - 2023

- Figure 81:

- VALUE SHARE OF MAJOR PLAYERS, %, NORTH AMERICA, 2022

North America Pet Nutraceuticals Industry Segmentation

Milk Bioactives, Omega-3 Fatty Acids, Probiotics, Proteins and Peptides, Vitamins and Minerals are covered as segments by Sub Product. Cats, Dogs are covered as segments by Pets. Convenience Stores, Online Channel, Specialty Stores, Supermarkets/Hypermarkets are covered as segments by Distribution Channel. Canada, Mexico, United States are covered as segments by Country.

- Pet nutraceuticals are supplements that are specifically formulated to improve the health and well-being of pets. In 2022, they accounted for 2.8% of the North American pet food market. The share of nutraceuticals increased by 9.9% in 2022 compared to 2017, mainly due to the increasing awareness among pet owners about the importance of preventive healthcare. In 2021, a study revealed that four in 10 cat and dog owners in the United States had paid more attention to their pet's health since the start of the pandemic.

- Dogs accounted for the majority of the nutraceuticals market, valued at USD 1.24 billion, followed by cats and other pet animals at USD 581.4 million and USD 226 million, respectively. The larger share of dogs is mainly due to their larger population compared to other pets. In 2022, there were 144 million dogs in the region, while cats and other pet animals accounted for 96.5 million and 104.9 million, respectively. The United States has the largest pet population in the region, accounting for 69% (239 million). Additionally, dogs are known to suffer from a wider range of health issues, such as joint problems, skin allergies, and digestive issues, which has led to increased demand for nutraceuticals in the region. Joint/mobility, vitamin deficiency, general health, skin coat, and immunity are among the most popular conditions where pet owners are spending money on both dogs and cats.

- The growing trend of humanization among pet owners, the aging pet population, growing specialized needs, and the rise of e-commerce channels are the major factors driving the market, and it is projected to register a CAGR of 5.0% during the forecast period.

| Sub Product | |

| Milk Bioactives | |

| Omega-3 Fatty Acids | |

| Probiotics | |

| Proteins and Peptides | |

| Vitamins and Minerals | |

| Other Nutraceuticals |

| Pets | |

| Cats | |

| Dogs | |

| Other Pets |

| Distribution Channel | |

| Convenience Stores | |

| Online Channel | |

| Specialty Stores | |

| Supermarkets/Hypermarkets | |

| Other Channels |

| Country | |

| Canada | |

| Mexico | |

| United States | |

| Rest of North America |

Market Definition

- FUNCTIONS - Pet foods are usually intended to provide complete and balanced nutrition to the pet but are primarily used as functional products. The scope includes the food and supplements consumed by pets including veterinary diets. Supplements/nutraceuticals that are directly supplied to pets are considered within the scope.

- RESELLERS - Companies engaged in reselling of pet food without value addition have been excluded from the market scope, in order to avoid double counting.

- END CONSUMERS - Pet owners are considered to be the end-consumers in the market studied.

- DISTRIBUTION CHANNELS - Supermarkets/hypermarkets, specialty stores, convenience stores, online channels and other channels are considered within the scope. The stores which are exclusively providing pet related basic and custom products are considered within the scope of specialty stores.

| Keyword | Definition |

|---|---|

| Pet Food | The scope of pet food includes the food that is eatable by pets including food, treats, veterinary diets, and nutraceuticals/supplements. |

| Food | Food is animal feed intended for consumption by pets. It is formulated to provide essential nutrients and meet the dietary needs of various types of pets, including dogs, cats, and other animals. These are generally segmented into dry and wet pet foods. |

| Dry Pet Food | Dry pet foods may be extruded/baked (kibbles) or flaked. They have a lower moisture content, typically around 12-20%. |

| Wet Pet Food | Wet pet food, also known as canned pet food or moist pet food, generally has a higher moisture content compared to dry pet food, often ranging from 70-80%. |

| Kibbles | Kibbles are dry, processed pet food in small, bite-sized pieces or pellets. They are specifically formulated to provide balanced nutrition for various domestic animals, such as dogs, cats, and other animals. |

| Treats | Pet Treats are special food items or rewards given to pets, to show affection, and encourage good behavior. They are especially used during training. Pet treats are made from various combinations of meat or meat-derived materials with other ingredients. |

| Dental Treats | Pet dental treats are specialized treats that are formulated to promote good oral hygiene in pets. |

| Crunchy Treats | It is a type of pet treat that has a firm and crispy texture which can be a good source of nutrition for pets. |

| Soft and chewy treats | Soft and Chewy pet treats are a type of pet food product that is formulated to be easy to chewy and digest. They are usually made from soft and pliable ingredients, such as meat, poultry, or vegetables, that have been blended and formed into bite-sized pieces or strips. |

| Freeze-dried & Jerky Treats | Freeze-dried and jerky treats are snacks given to pets, that are prepared through a special preservation process, without damaging the nutritional content, resulting in long-lasting, nutrient-rich treats. |

| Urinary Tract Disease Diets | These are commercial diets that are specifically formulated to promote urinary health and reduce the risk of urinary tract infections and other urinary problems. |

| Renal Diets | These are specialized pet foods formulated to support the health of pets with kidney disease or renal insufficiency. |

| Digestive Sensitivity Diets | Digestive-sensitive diets are specially formulated to meet the nutritional needs of pets with digestive issues such as food intolerances, allergies, and sensitivities. These diets are designed to be easily digestible and to reduce the symptoms of digestive problems in pets. |

| Oral Care Diets | Oral care diets for pets are specially formulated diets produced to promote oral health and hygiene in pets. |

| Grain-Free Pet Food | Pet food that does not contain common grains like wheat, corn, or soy. Grain-free diets are often preferred by pet owners seeking alternative options or if their pets have specific dietary sensitivities. |

| Premium Pet Food | High-quality pet food formulated with superior ingredients often offers additional nutritional benefits compared to standard pet food. |

| Natural Pet Food | Pet food made from natural ingredients, with minimal processing and without artificial preservatives. |

| Organic Pet Food | Pet food is produced using organic ingredients, free from synthetic pesticides, hormones, and genetically modified organisms (GMOs). |

| Extrusion | A manufacturing process used to produce dry pet food, where ingredients are cooked, mixed, and shaped under high pressure and temperature. |

| Other Pets | Other pets include birds, fish, rabbits, hamsters, ferrets, and reptiles. |

| Palatability | The taste, texture, and aroma of pet food influence its appeal and acceptance by pets. |

| Complete and Balanced Pet Food | Pet food that provides all essential nutrients in appropriate proportions to meet the nutritional needs of pets without additional supplementation. |

| Preservatives | These are the substances that are added to pet food to extend its shelf life and prevent spoilage. |

| Nutraceuticals | Food products that offer health benefits beyond basic nutrition, often contain bioactive compounds with potential therapeutic effects. |

| Probiotics | Live beneficial bacteria that promote a healthy balance of gut flora, supporting digestive health and immune function in pets. |

| Antioxidants | Compounds that help neutralize harmful free radicals in the body, promoting cellular health and supporting the immune system in pets. |

| Shelf-Life | The duration of which pet food remains safe and nutritionally viable for consumption after its production date. |

| Prescription diet | Specialized pet food formulated to address specific medical conditions under veterinary supervision. |

| Allergen | A substance that can cause allergic reactions in some pets, leading to food allergies or sensitivities. |

| Canned food | Wet pet food that is packed in cans and contains higher moisture content than dry food. |

| Limited ingredient diet (LID) | Pet food formulated with a reduced number of ingredients to minimize potential allergens. |

| Guaranteed Analysis | The minimum or maximum levels of certain nutrients present in pet food. |

| Weight management | Pet food designed to help pets maintain a healthy weight or support weight loss efforts. |

| Other Nutraceuticals | It includes prebiotics, antioxidants, digestive fiber, enzymes, essential oils and herbs. |

| Other Veterinary Diets | It includes weight management diets, skin and coat health, cardiac care, and joint care. |

| Other Treats | It includes rawhides, mineral blocks, lickables, and catnips. |

| Other Dry Foods | It includes cereal flakes, mixers, meal toppers, freeze-dried foods, and air-dried foods. |

| Other Animals | It includes birds, fish, reptiles, and small animals (rabbits, ferrets, hamsters). |

| Other Distribution Channels | It includes veterinary clinics, local unregulated stores, and feed and farm stores. |

| Proteins and Peptides | Proteins are large molecules composed of basic units called amino acids which help in the growth and development of pets. Peptides are the short string of 2 to 50 amino acids. |

| Omega-3 fatty acids | Omega-3 fatty acids are essential polyunsaturated fats that play a crucial role in the overall health and well-being of Pets |

| Vitamins | Vitamins are the essential organic compounds that are essential for vital physiological functioning. |

| Minerals | Minerals are naturally occurring inorganic substances that are essential for various physiological functions in pets. |

| CKD | Chronic Kidney Disease |

| DHA | Docosahexaenoic Acid |

| EPA | Eicosapentaenoic Acid |

| ALA | Alpha-linolenic Acid |

| BHA | Butylated Hydroxyanisol |

| BHT | Butylated Hydroxytoluene |

| FLUTD | Feline Lower Urinary Tract Disease |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: IDENTIFY KEY VARIABLES: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market-size estimations for the forecast years are in nominal terms. Inflation is not a part of the pricing, and the average selling price (ASP) is kept constant throughout the forecast period.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms