Africa Cold Chain Logistics Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

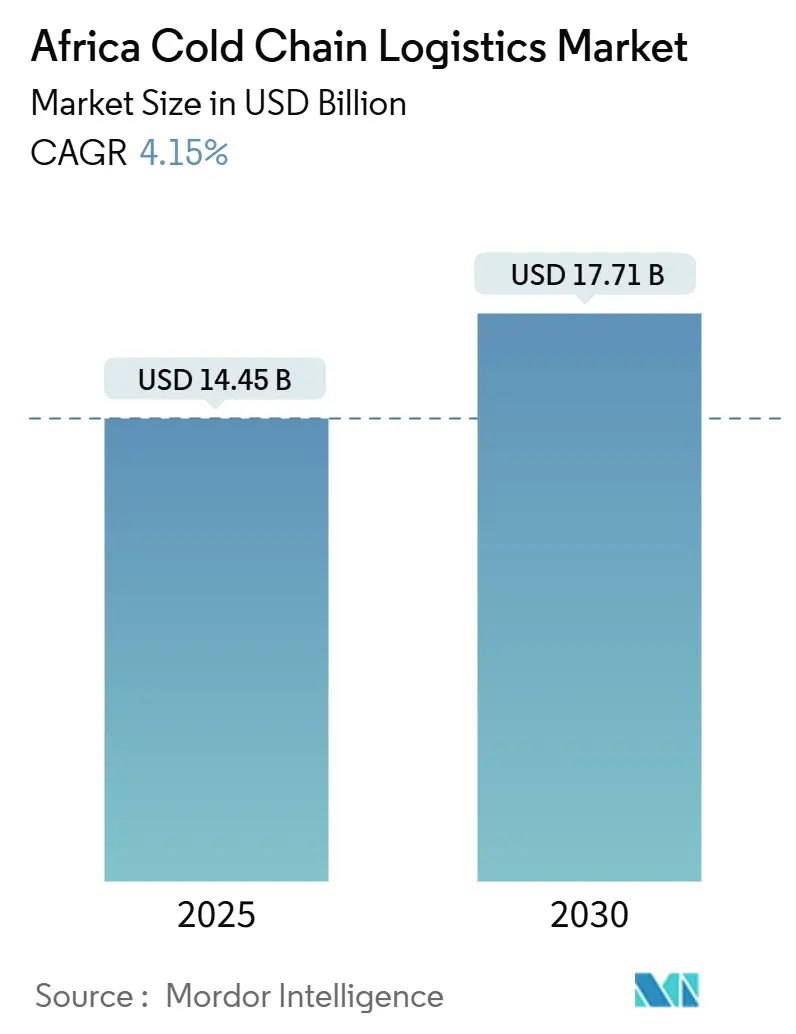

| Market Size (2025) | USD 14.45 Billion |

| Market Size (2030) | USD 17.71 Billion |

| Growth Rate (2025 - 2030) | 4.15% CAGR |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Africa Cold Chain Logistics Market Analysis by Mordor Intelligence

The Africa Cold Chain Logistics Market size is estimated at USD 14.45 billion in 2025, and is expected to reach USD 17.71 billion by 2030, at a CAGR of 4.15% during the forecast period (2025-2030).

Rising urbanization, local vaccine manufacturing targets, and the African Continental Free Trade Area (AfCFTA) are amplifying demand for temperature-controlled infrastructure across food and pharma supply chains. Cross-border trade corridors now carry more high-value perishables, while solar-powered micro cold rooms and IoT-enabled monitoring are cutting spoilage, especially in underserved rural zones. Consolidation among global and regional logistics providers is creating end-to-end service offerings, yet high energy tariffs and grid instability continue to push operators toward renewable power and natural refrigerants. Competitive differentiation now hinges on data-driven capacity planning, compliance with GDP standards, and the ability to navigate diverse regulatory frameworks across 54 countries.

Key Report Takeaways

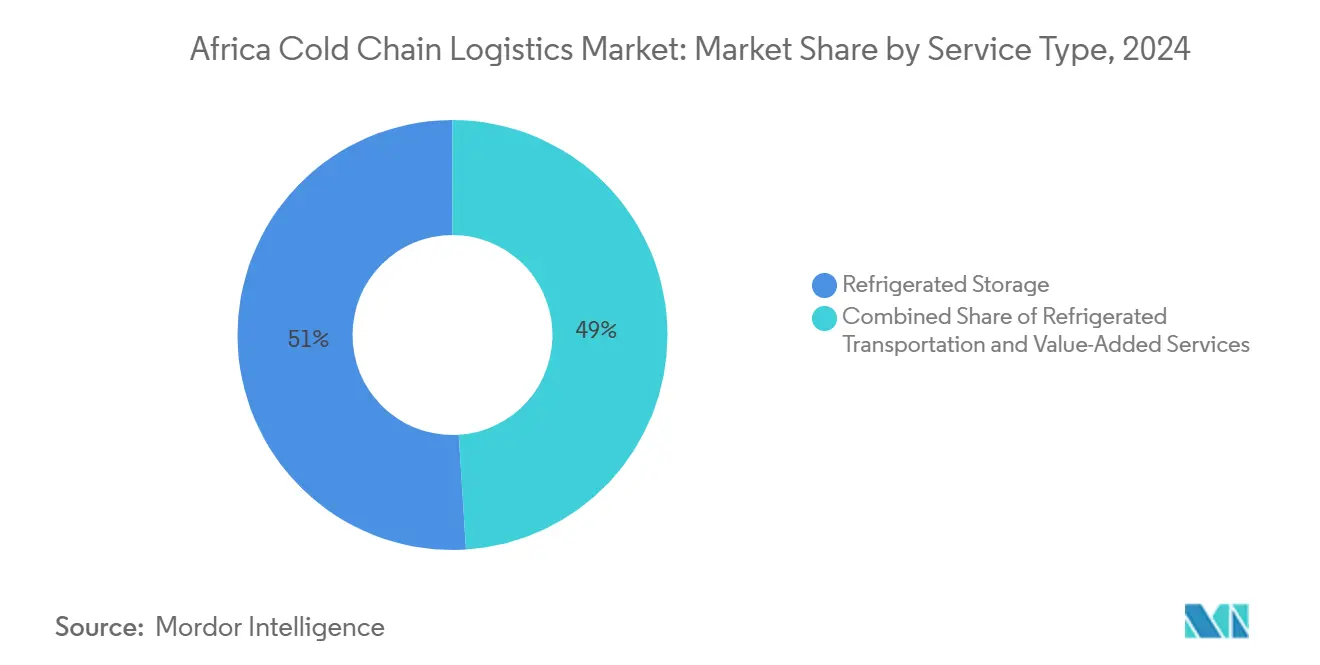

- By service type, refrigerated storage led with 51% of the Africa cold chain logistics market share in 2024; value-added services are projected to expand at a 4.3% CAGR to 2030.

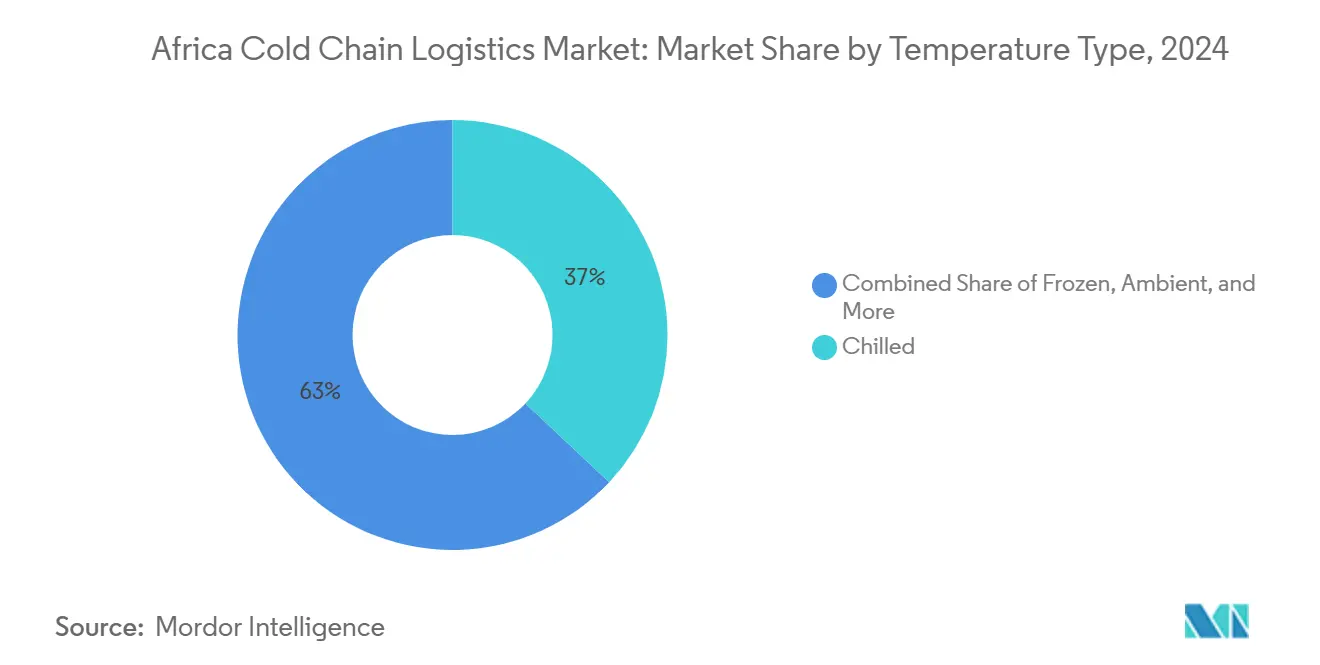

- By temperature type, chilled storage accounted for 37% of the Africa cold chain logistics market size in 2024, while frozen storage is tracking the fastest 4.8% CAGR through 2030.

- By application, fruits & vegetables retained a 28% share of the Africa cold chain logistics market size in 2024 and is advancing at a 4.1% CAGR through 2030.

- By geography, South Africa held a 31% share of the Africa cold chain logistics market in 2024; Nigeria records the highest 4.5% CAGR through 2030.

Africa Cold Chain Logistics Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for perishable foods | +1.2% | Nigeria, Kenya, Ghana | Medium-term (2-4 years) |

| Pharmaceutical cold-chain expansion | +0.8% | Egypt, Morocco, South Africa, Nigeria | Long-term (≥ 4 years) |

| Modern retail & e-commerce growth | +0.7% | Urban centers continent-wide | Short-term (≤ 2 years) |

| AfCFTA-driven intra-Africa trade | +0.6% | West and East Africa corridors | Long-term (≥ 4 years) |

| Solar-powered micro cold rooms uptake | +0.5% | Rural Nigeria, Kenya, Ghana | Medium-term (2-4 years) |

| AI/ML capacity-planning adoption | +0.3% | South Africa, Egypt, Morocco, Kenya | Short-term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Perishable Foods

Urban migration is adding 40 million new city consumers each year, prompting retailers to secure temperature-controlled networks that reduce the 40–50% post-harvest loss rate in fruits and vegetables. Supermarket chains such as Shoprite are rolling out track-and-trace platforms that give growers real-time feedback on shipment temperatures, improving shelf life and cutting rejection rates. Nigeria’s middle class is expanding by 8% annually, supporting premium pricing for fresh produce and justifying investment in public cold stores near wholesale markets. Supply chain digitization now allows freight brokers to match small-holder output with refrigerated truck space, shrinking empty backhaul mileage. Solar-powered micro cold rooms further anchor rural collection hubs, enabling growers to aggregate shipments into larger, more economical loads.

Pharmaceutical Cold-Chain Expansion

The African Vaccine Manufacturing Accelerator is targeting 60% local vaccine production by 2040, necessitating validated storage at 2-8 °C, -20 °C, and -70 °C ranges. Rwanda and Morocco are commissioning GMP-certified facilities that feed regional distribution through CEIV Pharma-accredited air-cargo terminals. Health ministries are tightening GDP compliance, obligating warehouse operators to implement temperature mapping and redundant power systems. Energy-efficient R290 refrigeration is gaining traction as operators pursue both cost savings and compliance with HFC phasedown rules. Stakeholders view robust pharma cold chains as critical to reducing antimicrobial resistance linked to degraded medicines stored in hot climates.

Modern Retail & E-commerce Growth

Mobile money transactions reached USD 701 billion in 2024, supporting an e-grocery wave that pressures distributors to guarantee cold integrity during two-hour delivery windows. Retail majors are piloting dark stores fitted with high-density chilled pick-faces to shorten fulfillment paths. Kenyan startup Keep IT Cool links its solar-powered cube stores to a B2B app, allowing small grocers to restock fresh items daily without owning refrigeration. Post-pandemic click-and-collect models in South Africa now rely on cross-docking hubs that consolidate mixed-temperature orders, cutting last-mile costs by 12%. Electric refrigerated vans are emerging for short-haul routes, supported by battery-swap stations that keep asset utilization high.

AfCFTA-Driven Intra-Africa Perishables Trade

Tariff removal on 90% of goods lifted intra-African trade by 7.2% in 2024. Blockchain-based certificates of origin now clear customs in under four hours on the Northern Corridor, trimming typical dwell times by two days. Port operators at Tema expanded reefer plugs by 40% to handle citrus and pineapple exports to West Africa. Harmonized SPS standards among COMESA, EAC, and SADC reduce duplication of lab tests, encouraging operators to route perishables via land corridors rather than higher-cost sea trans-shipment. Donor-funded trade finance is lowering risk premiums on multi-country cold chain projects, accelerating investment decisions for regional distribution centers.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High infrastructure & energy costs | -1.1% | Sub-Saharan Africa | Long-term (≥ 4 years) |

| Inadequate road & grid networks | -0.9% | Continental | Long-term (≥ 4 years) |

| Load-shedding-induced spoilage risk | -0.6% | South Africa, Nigeria, Ghana | Short-term (≤ 2 years) |

| HFC phase-down retrofit burden | -0.4% | Established facilities | Medium-term (2-4 years) |

| Source: Mordor Intelligence | |||

High Infrastructure & Energy Costs

Industrial power tariffs average USD 0.20-0.35 per kWh in 2024, more than double rates in developed markets, pushing cold storage energy bills to USD 50-80 per m³ annually[1]African Development Bank, “Energy Sector in Africa Overview 2024,” afdb.org. Refrigeration makes up 60-80% of total facility electricity use, and operators often face capital-intensive grid connection fees. Private equity funds hesitate to back greenfield builds due to 10-year payback horizons. Subsidy regimes rarely cover commercial refrigeration, compelling firms to seek carbon credits to offset renewable investments. Government infrastructure bonds remain oversubscribed, indicating unmet demand for lower-cost financing instruments targeted at cold chain projects.

Inadequate Road & Grid Networks

Only 28% of African roads are paved, and average outage duration exceeds 100 hours per year, forcing logistics companies to factor generator fuel into standard operating costs[2]International Energy Agency, “Cooling Emissions and Policy Synthesis Report 2024,” iea.org. Rural connectivity is worst in Central Africa, where unpaved feeder roads delay produce collection beyond optimal harvest windows, elevating spoilage. Border posts lack dedicated refrigerated inspection bays, adding 8-15 hours to transit for chilled cargo. Broadband constraints hinder the deployment of IoT trackers, leading to visibility gaps during multi-country hauls. Climate-induced flooding damages roads and substations, prompting insurers to hike premiums for temperature-sensitive cargo.

Segment Analysis

By Service Type: Storage Dominates Despite Transport Innovation

Refrigerated storage captures 51% of the Africa cold chain logistics market share in 2024, underscoring the region’s focus on reducing post-harvest losses through centralized facilities. Public warehouses leverage shared-cost models that attract cooperatives of smallholder farmers, while private stores cater to pharmaceutical and food multinationals with tailored certification needs. Road freight continues to dominate the transport sub-segment, yet service gaps for mid-distance hauls spur investment in insulated rail wagons on corridors such as Ethiopia-Djibouti. Value-added services—temperature monitoring, specialized packaging, and phytosanitary inspections—post a 4.3% CAGR as clients seek full-service contracts that consolidate compliance and logistics under one roof.

Logistics providers embed AI dashboards that forecast storage capacity and trigger dynamic pricing, lifting utilization rates. ColdHubs expands a hub-and-spoke trucking fleet that aggregates village-level loads into urban distribution centers, shortening dwell times. Sea freight operators install controlled-atmosphere reefer containers, prolonging fruit shelf life during Atlantic crossings. Air-cargo lanes handle high-value vaccines and floriculture shipments, with Ethiopia Cargo upgrading tarmac cold rooms to meet CEIV Fresh standards. Investment in bonded refrigeration zones near land borders facilitates AfCFTA trade flows, easing duty suspensions and accelerating customs clearance[3]International Institute of Refrigeration, “Cooling as-a-Service in Nigeria,” iifiir.org.

Note: Segment shares of all individual segments available upon report purchase

By Temperature Type: Frozen Growth Outpaces Chilled Dominance

Chilled facilities at 0-5 °C serve fresh produce and dairy, holding 37% of the Africa cold chain logistics market size in 2024. Pack-house upgrades in Kenya and Ghana integrate pre-cooling tunnels that drop field heat within 90 minutes, protecting vitamin content and texture. Frozen storage at -18 °C to 0 °C grows fastest at 4.8% CAGR, propelled by rising meat processing and expanded frozen entrée ranges in modern retail freezers. Pharma demand for -20 °C bulk vaccine storage intensifies as local fill-finish plants scale up output.

Ultra-low warehouses below -20 °C remain a niche but attract donor funding linked to pandemic preparedness plans. Operators trial transcritical CO₂ systems, balancing higher energy draw in hot climates against lower refrigerant costs. Ambient facilities complement active cooling by staging goods during palletization, mitigating condensation. Kigali-driven technology shifts spur suppliers to design modular natural refrigerant racks suited to variable load profiles typical of African warehouses.

Note: Segment shares of all individual segments available upon report purchase

By Application: Fruits & Vegetables Lead Dual Growth-Share Matrix

Fruits & vegetables command 28% share of the Africa cold chain logistics market in 2024 and is expected to grow at a 4.1% CAGR from 2025-2030, buoyed by export programs in citrus, avocado, and berries. Multilayer breathable liners and ethylene scrubbers inside reefer containers extend shelf life on 25-day Europe sailings. Meat & poultry growth mirrors protein demand in West Africa’s urban centers, where quick-service restaurants stipulate documented chill chains. Fish & seafood investments cluster along Senegal’s coastline, featuring brine-freeze tunnels that support EU-compliant exports.

Pharmaceuticals & biologics, though lower in tonnage, offer premium yields due to stringent handling protocols. WHO GDP guidelines require continuous data logging and route risk assessments, raising service barriers to entry. Dairy & frozen desserts expand in Tanzania and Uganda, driven by youth preference for convenient portion packs. Ready-to-eat meal demand rises among dual-income households, spurring investments in multi-temperature last-mile vans outfitted with Bluetooth probes that certify delivery compliance.

Geography Analysis

South Africa retains a 31% share of the Africa cold chain logistics market in 2024, underpinned by advanced retail networks and export-oriented horticulture. Policy incentives support solar rooftop retrofits on cold warehouses, partially offsetting load-shedding risk. Nigeria posts the highest 4.5% CAGR to 2030 as population growth surpasses 2% annually. ColdHubs’ solar units near Kano wholesale markets and Expeditors’ new Lagos facility signal rising investor confidence.

Egypt leverages USD 3.88 billion in pharma sales to justify GDP-compliant depots feeding MENA markets. Morocco’s Tanger-Med port offers fast transshipment into Mediterranean grocery chains, stimulating hinterland citrus pack-houses. Rest-of-Africa markets such as Ethiopia tap geothermal power for cost-effective refrigeration. Kenya’s flower export industry upgrades vacuum coolers and invests in air-cargo pods to maintain petal rigidity on Amsterdam routes.

Competitive Landscape

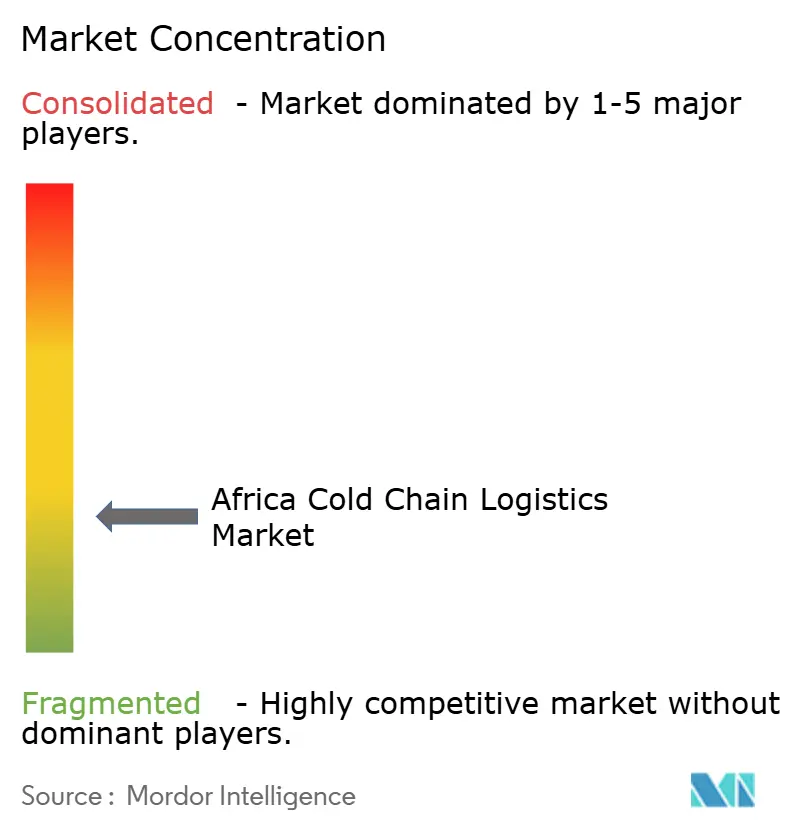

The Africa cold chain logistics market is fragmented, with global integrators, regional champions, and impact-driven startups co-existing. DP World’s acquisition of Imperial Logistics unlocks seamless door-to-door flows from berth to inland depot, strengthening vertical integration across African trade arteries[4]Seatrade Maritime, “DP World Acquisition of Imperial Logistics,” seatrade-maritime.com. DHL earmarks EUR 2 billion (USD 2.08 billion) for its Health Logistics division, including GDP-compliant sites in Egypt, Kenya, and South Africa. Kuehne+Nagel’s purchase of Morgan Cargo enhances perishables expertise, bridging farm-gates with EU retail distribution.

Solar-first disruptors such as ColdHubs and Africa GreenTec capitalize on decentralized energy to serve rural areas neglected by grid-reliant operators. Cross-border mergers accelerate as South African 3PLs seek scale in West Africa, with transaction rationales anchored in market access and portfolio diversification. Technology stacks combining AI capacity forecasts, IoT temperature loggers, and blockchain traceability become baseline client requirements, raising entry barriers for smaller incumbents.

Investors target facilities capable of switching from high-GWP refrigerants to natural alternatives with minimal downtime, viewing compliance readiness as a proxy for asset longevity. Competitive advantage now hinges on turnkey services covering import documentation, multi-temperature transport, and last-mile distribution tailored to e-commerce growth. Joint ventures with local SME truckers enable multinationals to navigate cabotage rules while expanding geographic reach.

Africa Cold Chain Logistics Industry Leaders

-

Imperial Logistics (Subsidiary of DP World)

-

Kuehne + Nagel

-

DHL Group

-

Trans-Nationwide Express (TRANEX)

-

Kennie-O Cold Chain Logistics

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: DHL Group closed its purchase of CRYOPDP, adding more than 600,000 temperature-controlled shipments a year to its network and deepening pharmaceutical logistics coverage across 15 countries, including key African markets.

- February 2025: DP World completed its USD 1.6 billion buyout of Imperial Logistics, combining extensive road fleets with port assets to offer Africa-wide end-to-end cold chain services staffed by 11,000 employees across 25 countries.

- February 2025: Kuehne+Nagel take over South Africa’s Morgan Cargo, gaining 40,000 tonnes of annual perishables airlift and 20,000 TEU of refrigerated sea freight capacity, along with 450 specialists who strengthen routes linking South Africa, the United Kingdom, and Kenya.

- January 2025: Ethiopian Cargo & Logistics Services partnered with cargo.one to launch real-time digital booking for temperature-sensitive freight on its network of more than 130 African destinations, improving visibility for pharmaceutical and fresh-produce shippers

Africa Cold Chain Logistics Market Report Scope

The process of transporting, holding, and managing temperature-sensitive products in a controlled environment is referred to as cold chain logistics. For industries dealing with products that are sensitive to temperature variations, including both positive and negative temperature ranges, this is essential.

A complete background analysis of the African cold chain logistics market, including the assessment of the economy and contribution of sectors in the economy, market overview, market size estimation for key segments, and emerging trends in the market segments, market dynamics, and geographical trends, and COVID-19 impact, is covered in the report.

Africa's cold chain logistics market is segmented by service (storage, transportation, and value-added services (blast freezing, labeling, inventory management, etc.)), temperature (ambient, chilled, and frozen), application (horticulture (fresh fruits and vegetables), dairy products (milk, ice-cream, butter, etc.), meats and fish, processed food products, pharma, life sciences, and chemicals, and other applications), and country (Egypt, Morocco, Nigeria, South Africa, and Rest of Africa). The report offers market size and forecasts for the above-mentioned segments in value (USD).

| Refrigerated Storage | Public Warehousing |

| Private Warehousing | |

| Refrigerated Transportation | Road |

| Rail | |

| Sea | |

| Air | |

| Value-Added Services |

| Chilled (0–5 °C) |

| Frozen (-18–0 °C) |

| Ambient |

| Deep-Frozen / Ultra-Low (less than-20 °C) |

| Fruits & Vegetables |

| Meat & Poultry |

| Fish & Seafood |

| Dairy & Frozen Desserts |

| Bakery & Confectionery |

| Ready-to-Eat Meals |

| Pharmaceuticals & Biologics |

| Vaccines & Clinical Trial Materials |

| Chemicals & Specialty Materials |

| Other Perishables |

| Egypt |

| Morocco |

| Nigeria |

| South Africa |

| Rest of Africa |

| By Service Type | Refrigerated Storage | Public Warehousing |

| Private Warehousing | ||

| Refrigerated Transportation | Road | |

| Rail | ||

| Sea | ||

| Air | ||

| Value-Added Services | ||

| By Temperature Type | Chilled (0–5 °C) | |

| Frozen (-18–0 °C) | ||

| Ambient | ||

| Deep-Frozen / Ultra-Low (less than-20 °C) | ||

| By Application | Fruits & Vegetables | |

| Meat & Poultry | ||

| Fish & Seafood | ||

| Dairy & Frozen Desserts | ||

| Bakery & Confectionery | ||

| Ready-to-Eat Meals | ||

| Pharmaceuticals & Biologics | ||

| Vaccines & Clinical Trial Materials | ||

| Chemicals & Specialty Materials | ||

| Other Perishables | ||

| By Country | Egypt | |

| Morocco | ||

| Nigeria | ||

| South Africa | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current value of the Africa cold chain logistics market?

The market stands at USD 14.45 billion in 2025, with a forecast to reach USD 17.71 billion by 2030.

How fast is demand for frozen storage growing?

Frozen storage capacity is expanding at a 4.8% CAGR through 2030, the fastest among temperature segments.

Which country leads the continent in cold chain capacity?

South Africa holds the largest share at 31% because of its mature retail and export networks.

Why are solar-powered micro cold rooms important?

They provide off-grid, pay-as-you-store solutions that cut spoilage in rural areas lacking reliable electricity.

How is AfCFTA influencing refrigerated logistics?

Tariff removal and digital trade facilitation have raised intra-African perishables trade by 7.2%, boosting cross-border cold chain demand.

What technologies are logistics firms adopting for compliance?

Operators are integrating IoT temperature sensors, AI capacity-planning tools, and GDP-certified processes to meet food and pharma regulations.

Page last updated on: