Market Size of Africa CNG And LPG Vehicle Industry

| Study Period | 2019 - 2029 |

| Base Year For Estimation | 2023 |

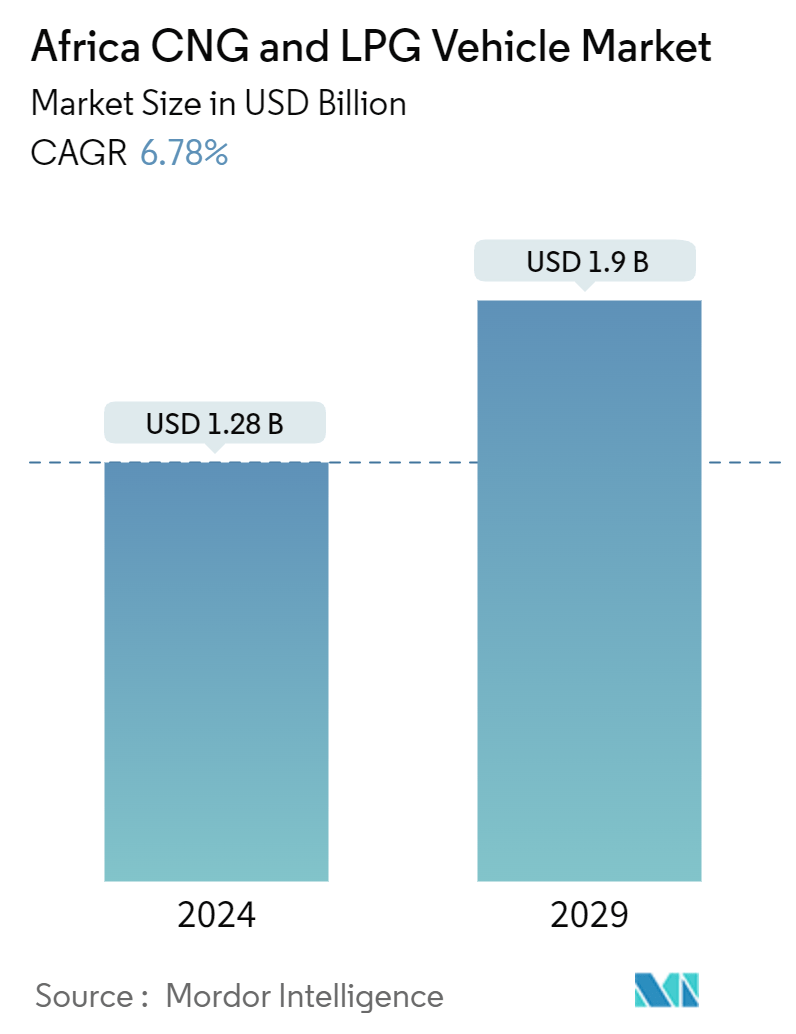

| Market Size (2024) | USD 1.28 Billion |

| Market Size (2029) | USD 1.9 Billion |

| CAGR (2024 - 2029) | 6.78 % |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order |

Africa CNG and LPG Vehicle Market Analysis

The Africa CNG And LPG Vehicle Market size is estimated at USD 1.28 billion in 2024, and is expected to reach USD 1.9 billion by 2029, growing at a CAGR of 6.78% during the forecast period (2024-2029).

Africa's transportation sector is undergoing a gradual shift toward cleaner and more sustainable fuels, primarily driven by a focus on environmental concerns and the reduction on the dependence on traditional fossil fuels and government policies that promote cleaner energy sources. Thus, the market for CNG and LPG vehicles is gaining traction as viable alternatives to conventional gasoline and diesel vehicles.

While the adoption of CNG and LPG vehicles in Africa is still relatively modest compared to other regions, there is a growing interest and investment in these alternative fuel technologies. The market size varies across different countries within the continent with some regions experiencing faster growth rates due to supportive regulatory frameworks and infrastructure development.

The increasing awareness about the environmental impact of conventional vehicles, including air pollution and greenhouse gas emissions, is prompting consumers and policymakers to seek cleaner alternatives. CNG and LPG typically offer cost advantages over gasoline and diesel, making them attractive options for fleet operators and individual vehicle owners seeking to lower fuel expenses.

Many African governments are implementing policies and incentives to encourage the adoption of alternative fuels, including tax incentives, subsidies, and regulatory measures such as emissions standards and fuel mandates.

Investment in expanding refueling infrastructure, including CNG/LPG stations and distribution networks, presents a significant opportunity for private investors and government agencies.

Considering these factors, demand for CNG and LPG vehicles is expted to witness positive growth rate during the forecast period.

Africa CNG and LPG Vehicle Industry Segmentation

Motor vehicles powered with alternative fuels including liquified petroleum gas and compressed natural gas in order to reduce greenhouse emissions are referred to as CNG and LPG vehicles.

The Africa CNG and LPG vehicle market is segmented by fuel type, vehicle type, sales channel, and country. By fuel type, the market is segmented into compressed natural gas (CNG) and liquefied petroleum gas (LPG). By vehicle type, the market is segmented into passenger cars and commercial vehicles. By sales channel, the market is segmented into OEM and aftermarket, and on the basis of country, the market is segmented into Egypt, Nigeria, South Africa, Northern Africa, Morocco, Ethiopia, and the Rest of Africa. For each segment, the market sizing and forecasting are based on value (USD).

| Fuel Type | |

| Compressed Natural Gas | |

| Liquified Petroleum Gas |

| Vehicle Type | |

| Passenger Cars | |

| Commercial Vehicles |

| Sales Channel | |

| OEM | |

| Aftermarket |

| Country | |

| Egypt | |

| Nigeria | |

| South Africa | |

| Morocco | |

| Ethiopia | |

| Rest of Africa |

Africa CNG And LPG Vehicle Market Size Summary

The Africa CNG and LPG vehicle market is experiencing a transformative shift as the continent moves towards cleaner and more sustainable fuel alternatives. This transition is driven by increasing environmental concerns and government policies aimed at reducing reliance on traditional fossil fuels. The market is gaining momentum as CNG and LPG vehicles emerge as viable substitutes for conventional gasoline and diesel vehicles. Although the adoption rate in Africa is still modest compared to other regions, there is a growing interest and investment in these alternative fuel technologies. The market's growth is uneven across the continent, with some countries benefiting from supportive regulatory frameworks and infrastructure development. The cost advantages of CNG and LPG over traditional fuels make them attractive options for both fleet operators and individual vehicle owners looking to reduce fuel expenses.

Egypt is poised to lead the African CNG and LPG vehicle market, supported by significant government initiatives and investments in infrastructure. The country's proactive approach includes incentives such as tax breaks and subsidies, which create a favorable environment for market growth. Egypt's extensive network of refueling stations and conversion centers facilitates higher adoption rates compared to other African nations. The presence of local industry players and partnerships with international manufacturers further bolster the market's development in Egypt. The fragmented nature of the African market sees numerous players investing in research and development to enhance CNG and LPG vehicle offerings. Recent developments, such as the introduction of dedicated natural gas trucks in South Africa and the establishment of CNG facilities in Tanzania, highlight the ongoing efforts to expand the market across the continent.

Africa CNG And LPG Vehicle Market Size - Table of Contents

-

1. MARKET DYNAMICS

-

1.1 Market Drivers

-

1.1.1 Investments in Refueling Infrastructure Is Driving the Market Growth

-

-

1.2 Market Restraints

-

1.2.1 Inadequate Regulatory Frameworks is Anticipated to Restrain the Market Growth

-

-

1.3 Porters Five Forces Analysis

-

1.3.1 Threat of New Entrants

-

1.3.2 Bargaining Power of Buyers/Consumers

-

1.3.3 Bargaining Power of Suppliers

-

1.3.4 Threat of Substitute Products

-

1.3.5 Intensity of Competitive Rivalry

-

-

-

2. MARKET SEGMENTATION

-

2.1 Fuel Type

-

2.1.1 Compressed Natural Gas

-

2.1.2 Liquified Petroleum Gas

-

-

2.2 Vehicle Type

-

2.2.1 Passenger Cars

-

2.2.2 Commercial Vehicles

-

-

2.3 Sales Channel

-

2.3.1 OEM

-

2.3.2 Aftermarket

-

2.3.3

-

-

2.4 Country

-

2.4.1 Egypt

-

2.4.2 Nigeria

-

2.4.3 South Africa

-

2.4.4 Morocco

-

2.4.5 Ethiopia

-

2.4.6 Rest of Africa

-

2.4.7

-

-

Africa CNG And LPG Vehicle Market Size FAQs

How big is the Africa CNG And LPG Vehicle Market?

The Africa CNG And LPG Vehicle Market size is expected to reach USD 1.28 billion in 2024 and grow at a CAGR of 6.78% to reach USD 1.9 billion by 2029.

What is the current Africa CNG And LPG Vehicle Market size?

In 2024, the Africa CNG And LPG Vehicle Market size is expected to reach USD 1.28 billion.