| Study Period | 2019 - 2030 |

| Market Size (2025) | USD 55.73 Billion |

| Market Size (2030) | USD 82.65 Billion |

| CAGR (2025 - 2030) | 8.20 % |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

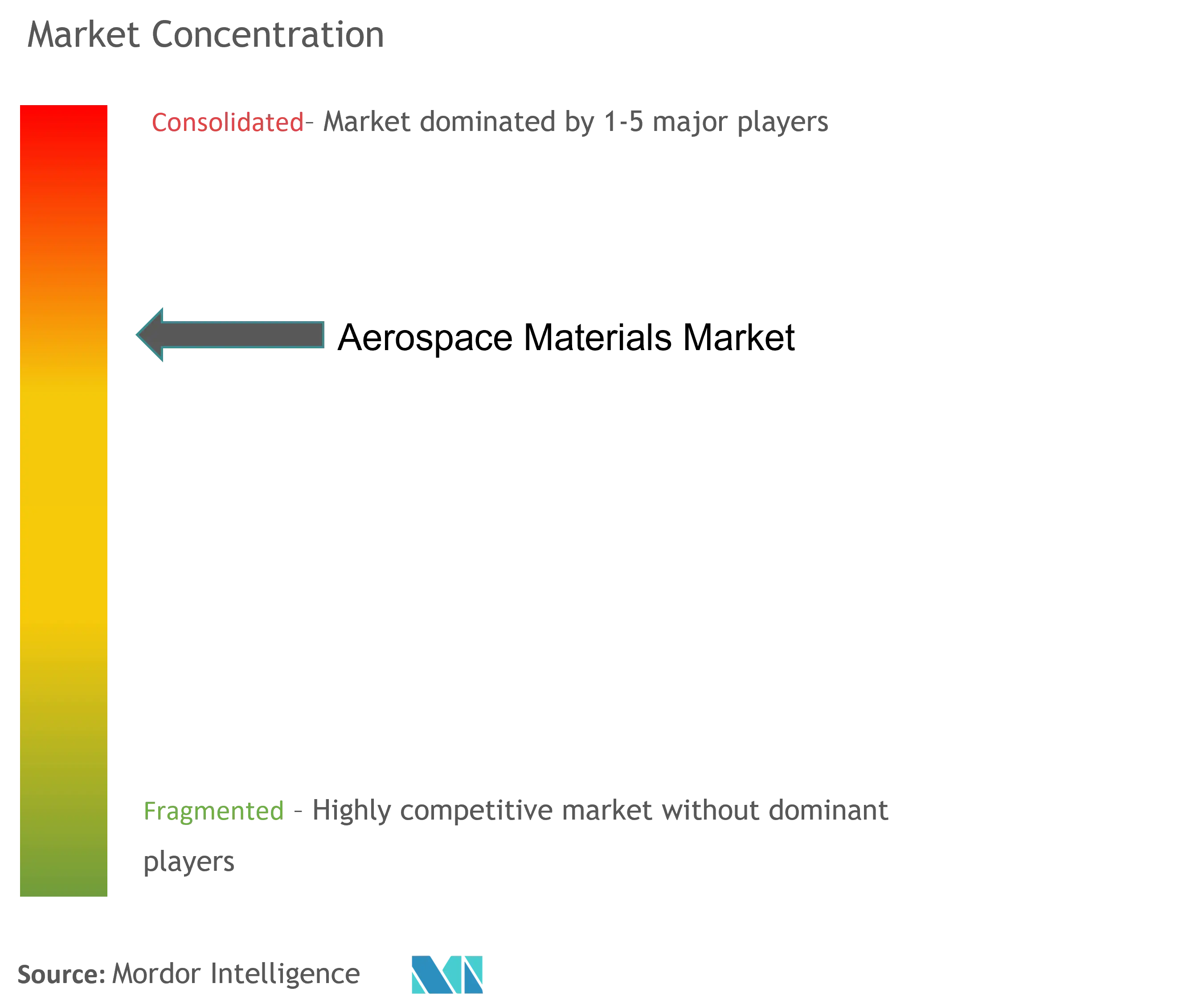

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order |

Aerospace Materials Market Analysis

The Aerospace Materials Market size is estimated at USD 55.73 billion in 2025, and is expected to reach USD 82.65 billion by 2030, at a CAGR of greater than 8.2% during the forecast period (2025-2030).

The aerospace materials industry is undergoing a significant transformation driven by technological advancements and changing market demands. Aircraft manufacturers are increasingly focusing on developing more fuel-efficient and environmentally sustainable aircraft, leading to innovations in material science and engineering. According to Boeing's latest forecast, the worldwide commercial fleet is expected to exceed 49,000 planes by 2040, with Asian economies accounting for approximately 40% of the long-term global demand for new airplanes. This shift has catalyzed investments in research and development of advanced materials, particularly in the areas of composite materials and lightweight alloys.

The defense sector continues to be a major driver of aerospace industry growth and innovation. Global defense spending reached USD 2,113 billion in 2021, marking a significant 6.77% increase from the previous year. This surge in defense expenditure has led to increased demand for high-performance materials capable of meeting stringent military specifications. The industry is witnessing a notable shift towards materials that offer enhanced durability, stealth capabilities, and resistance to extreme conditions, particularly in applications for next-generation military aircraft and unmanned aerial vehicles.

Commercial aviation has emerged as a key growth catalyst for the aerospace industry market, with airlines focusing on fleet modernization and expansion. The space industry has demonstrated remarkable growth, reaching a record $469 billion in annual global spending in 2021, with projections suggesting it could reach USD 1 trillion by 2040. This expansion has driven demand for specialized materials capable of withstanding the extreme conditions of space travel, particularly in applications for satellites, launch vehicles, and space exploration equipment.

The industry is experiencing significant consolidation through strategic partnerships and collaborations between material manufacturers and aerospace companies. For instance, in October 2022, the government-run Mishra Dhatu Nigam Limited (MIDHANI) and Boeing India announced a collaboration to develop raw materials for aerospace parts and components in India. Similarly, in November 2022, VoltAero signed an agreement with Italian aerospace supplier TESI to manufacture airframes for its Cassio 330 aircraft. These partnerships are fostering innovation in material development and manufacturing processes, while also addressing supply chain challenges and promoting localization of aerospace material production.

Aerospace Materials Market Trends

INCREASING USE OF COMPOSITES IN AIRCRAFT MANUFACTURING

The aerospace materials industry is witnessing a significant shift toward composite materials in aircraft manufacturing, driven by the critical need for fuel efficiency and performance optimization. Major aircraft manufacturers are increasingly incorporating carbon fiber-reinforced plastics (CFRPs) and other composite materials in their newest models, with the Airbus A350 XWB and Boeing 787 both utilizing approximately 50% composite materials in their construction. These advanced materials offer superior strength-to-weight ratios, corrosion resistance, and improved fatigue properties compared to traditional metallic materials, enabling manufacturers to create lighter and more efficient aircraft structures while maintaining structural integrity and safety standards.

The adoption of composites extends beyond primary structures to include various aircraft components such as wing assemblies, helicopter rotor blades, seat propellers, and instrument enclosures. Aramid fibers, for instance, are being extensively used in these applications due to their exceptional impact resistance and damage tolerance properties. The integration of composite materials has demonstrated remarkable benefits in weight reduction, with each kilogram saved contributing to lower fuel consumption, reduced operating costs, and decreased environmental impact. Furthermore, carbon composites offer manufacturing advantages through their moldability, allowing multiple simple metal parts to be replaced with a single complex composite piece, significantly reducing the total number of components required in aircraft construction. This trend is a key driver in the commercial aircraft materials market.

Understand The Key Trends Shaping This Market

Download PDF

GROWING SPACE INDUSTRY

The global space industry is experiencing unprecedented growth, driven by increasing private sector participation and technological advancements. The space economy demonstrated remarkable resilience and expansion, reaching a record $469.3 billion in annual global spending in 2021, with commercial space products and services accounting for nearly 48% of total turnover. This growth is supported by ambitious space exploration programs, increasing satellite deployments, and rising investments in space infrastructure development. Private companies are revolutionizing the industry through innovative approaches to spacecraft design and launch services, while government space agencies continue to push the boundaries of exploration and scientific research.

The industry's expansion is further evidenced by the growing number of satellite launches and space missions. As of January 2022, there were 4,852 active artificial satellites in orbit, with the United States, China, and Russia leading in satellite deployment capabilities. Space agencies worldwide are undertaking ambitious projects, such as NASA's Artemis program, which aims to return humans to the Moon and establish a sustainable lunar presence. Additionally, countries like China are making significant strides in their space capabilities, with plans to conduct more than 50 space launches annually, demonstrating the industry's robust growth trajectory and increasing global participation in space exploration activities. This expansion is a significant facet of aerospace market growth.

INCREASING GOVERNMENT SPENDING ON DEFENSE IN THE UNITED STATES AND EUROPEAN COUNTRIES

Defense spending in the United States and European countries has witnessed substantial growth, driven by modernization initiatives and evolving security challenges. The United States government allocated $768.2 billion for national defense programs in 2022, representing a 2% increase from the previous budget request. This increased funding supports various aerospace defense programs, including aircraft procurement, research and development, and maintenance operations. Major defense contracts continue to drive innovation and production in the aerospace sector, as exemplified by Boeing's recent contract modification for KC-46A Air Force Production Lot 8 aircraft, valued at $886.2 million for foreign military sales to Israel.

European nations have significantly increased their defense budgets in response to regional security concerns. Germany announced a substantial increase in defense spending, pledging €130 billion through 2030 for defense equipment, while committing to increase overall defense spending by €3-4 billion annually for the next 15 years. Similarly, countries like Belgium have approved legislation to increase defense budgets by more than €10 billion by 2030, and Romania has committed to raising its defense budget from 2% to 2.5% of GDP. These investments are driving demand for advanced aerospace materials and technologies, particularly in military aircraft manufacturing and modernization programs. The increased focus on defense capabilities has led to numerous procurement programs and technological developments, creating sustained demand for aerospace materials across the region, highlighting trends in the aerospace materials market.

Segment Analysis: Type

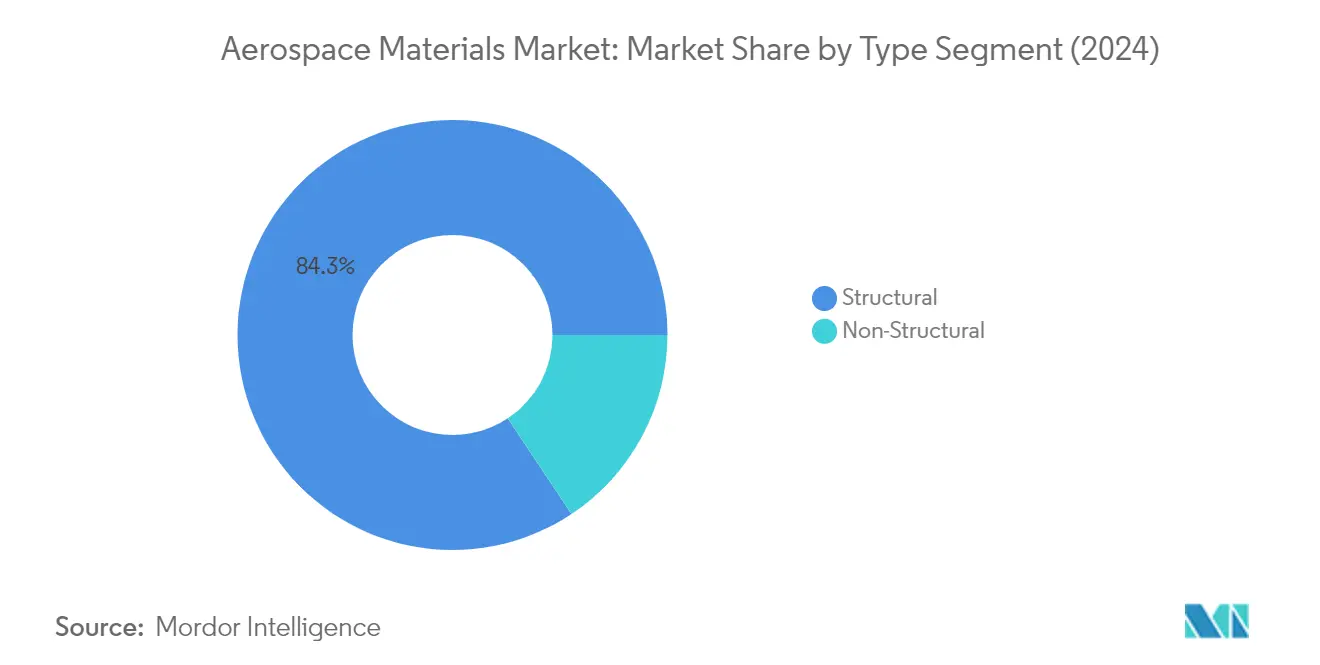

Structural Segment in Aerospace Materials Market

The aerospace materials structural segment dominates the aerospace materials market, commanding approximately 84% of the total market share in 2024. This segment encompasses critical materials like composites, plastics, and various alloys, including titanium, aluminum, steel, and magnesium, which are essential for manufacturing primary and secondary aircraft structures. The segment's dominance can be attributed to the increasing use of advanced composites in modern aircraft manufacturing, particularly in commercial aviation, where manufacturers are focusing on lightweight materials to improve fuel efficiency. The structural materials segment is also experiencing the fastest growth trajectory, projected to grow at around 8% from 2024 to 2029, driven by the rising demand for carbon fiber composites in next-generation aircraft and the growing space industry. The segment's growth is further supported by increasing government spending on defense in the United States and European countries, where structural materials play a crucial role in military aircraft manufacturing and space vehicle development.

Non-Structural Segment in Aerospace Materials Market

The non-structural segment plays a vital role in the aerospace materials market, encompassing essential materials such as coatings, adhesives and sealants, foams, and seals. These materials are crucial for aircraft protection, maintenance, and operational efficiency, despite holding a smaller market share. The segment's significance lies in its diverse applications, from protective coatings that shield aircraft surfaces from environmental damage to specialized adhesives that ensure structural integrity. Non-structural materials are particularly important in the commercial aviation sector, where they contribute to aircraft longevity and safety through applications such as thermal insulation, vibration dampening, and corrosion protection. The segment's growth is driven by technological advancements in coating materials, increasing focus on aircraft maintenance and repair operations, and the development of environmentally friendly aerospace materials.

Segment Analysis: Aircraft Type

General and Commercial Segment in Aerospace Materials Market

The General and Commercial segment continues to dominate the global aerospace materials market, holding approximately 56% of the market share in 2024. This significant market position is driven by the robust recovery in commercial aviation post-pandemic, with passenger travel demand strengthening across major regions. The segment's growth is further supported by the substantial backlog of new aircraft orders and the resurgence of business aircraft demand. The implementation of the Open Skies Agreement has been instrumental in extending liberalization in the commercial airline industry, contributing to the segment's dominance. Additionally, the increasing demand for private travel, driven by the growing number of high-net-worth individuals globally, has led to increased procurement of helicopters and business jets with improved cabin interiors. The expansion of charter operators and tourism businesses, coupled with their plans to increase fleet sizes by introducing new piston-engine aircraft and turboprop aircraft, has further solidified this segment's market leadership.

Space Vehicles Segment in Aerospace Materials Market

The Space Vehicles segment is emerging as the fastest-growing segment in the aerospace materials market, projected to grow at approximately 10% annually from 2024 to 2029. This remarkable growth trajectory is primarily driven by increasing investments in space exploration programs and satellite deployments across both government and private sectors. The segment's expansion is further fueled by the growing commercial space industry, with numerous private companies entering the market with innovative space technologies and solutions. The development of reusable launch vehicles, increasing satellite constellations for global connectivity, and the emergence of space tourism have created new opportunities for advanced aerospace materials. The segment is also benefiting from the rising number of countries developing their space capabilities and the increasing focus on deep space exploration missions, driving the demand for specialized materials that can withstand extreme space conditions.

Remaining Segments in Aircraft Type

The Military and Defense segment represents a crucial component of the aerospace materials market, driven by increasing global defense budgets and modernization programs across major military powers. This segment's significance is underscored by the growing emphasis on developing advanced military aircraft with multi-mission capabilities, particularly in response to evolving security challenges and territorial disputes. The segment benefits from continuous technological advancements in military aviation, including the development of next-generation fighter aircraft, military transport planes, and advanced unmanned aerial vehicles. The increasing focus on lightweight, high-performance materials for military applications, coupled with the growing demand for stealth capabilities and enhanced operational efficiency, continues to drive innovation in aerospace materials within this segment.

Aerospace Materials Market Geography Segment Analysis

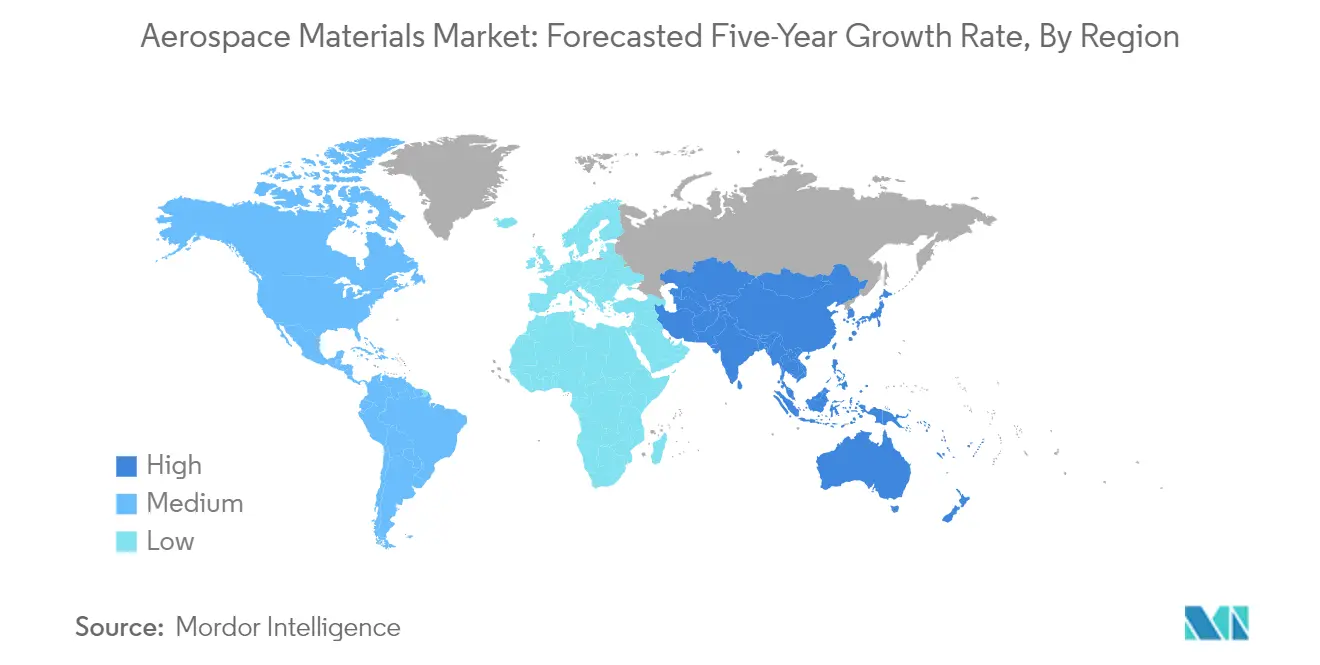

Aerospace Materials Market in Asia-Pacific

The aerospace materials market in Asia-Pacific demonstrates significant diversity across its key markets, including China, India, Japan, and South Korea. The region's aerospace sector is characterized by rapid industrialization, increasing defense spending, and growing commercial aviation demands. Countries in this region are actively developing their domestic aerospace manufacturing capabilities, with several nations implementing favorable policies to attract investments in aerospace material production and aircraft manufacturing. The presence of major aircraft manufacturers and their supply chains has created a robust ecosystem for aerospace materials, while increasing military modernization programs across the region continue to drive demand.

Aerospace Materials Market in China

China dominates the Asia-Pacific aerospace materials market, holding approximately 52% market share in the region. The country's aerospace sector benefits from substantial government support and strategic initiatives aimed at developing domestic aerospace capabilities. China's aerospace industry encompasses a comprehensive supply chain, from raw material production to final aircraft assembly. The country has made significant strides in developing its commercial aircraft manufacturing capabilities, exemplified by its domestic aircraft programs. The nation's robust space program and military modernization efforts further contribute to the demand for advanced aerospace materials, while its growing civil aviation sector continues to drive market expansion.

Aerospace Materials Market in India

India emerges as the fastest-growing market in the Asia-Pacific region, with a projected growth rate of around 9% from 2024-2029. The country's aerospace materials market is driven by increasing investments in domestic aerospace manufacturing capabilities and rising defense expenditure. India's growing focus on indigenous aircraft production and space exploration programs has created new opportunities for aerospace material suppliers. The government's push for self-reliance in aerospace manufacturing, coupled with initiatives to develop aerospace manufacturing clusters, has attracted significant investments in the sector. The country's expanding maintenance, repair, and overhaul (MRO) sector also contributes to the growing demand for aerospace materials.

Aerospace Materials Market in North America

North America represents the largest regional market for aerospace materials globally, characterized by the presence of major aircraft manufacturers, advanced technological capabilities, and robust aerospace research and development activities. The region's market is primarily driven by the United States, Canada, and Mexico, with each country contributing uniquely to the aerospace materials ecosystem. The presence of leading aircraft manufacturers, extensive military programs, and a well-established space industry creates sustained demand for advanced aerospace materials. The region's focus on developing next-generation aircraft and spacecraft continues to drive innovation in aerospace materials.

Aerospace Materials Market in United States

The United States maintains its position as the dominant force in the North American aerospace materials market, commanding approximately 93% of the regional market share. The country's aerospace sector benefits from extensive military and commercial aviation programs, supported by significant government defense spending and the presence of major aerospace manufacturers. The U.S. maintains leadership in aerospace innovation through advanced research facilities and strong collaboration between industry and academic institutions. The nation's robust space exploration programs, including both government and private sector initiatives, further strengthen the demand for specialized aerospace materials.

Aerospace Materials Market in Mexico

Mexico demonstrates the highest growth potential in North America, with an expected growth rate of around 8% from 2024-2029. The country has emerged as an important aerospace manufacturing hub, attracting significant foreign investment in aerospace component production. Mexico's strategic geographical location, competitive labor costs, and favorable trade agreements have contributed to its growing importance in the aerospace supply chain. The country's aerospace industry benefits from increasing investments in manufacturing facilities and the expansion of aerospace clusters. The government's supportive policies and focus on developing a skilled workforce continue to enhance Mexico's position in the aerospace materials market.

Aerospace Materials Market in Europe

Europe maintains a strong position in the global aerospace market size, supported by its well-established aerospace industry and significant research and development capabilities. The region's market encompasses key countries, including Germany, France, the United Kingdom, Italy, Spain, and Russia, each contributing to the diverse aerospace ecosystem. The presence of major aircraft manufacturers, extensive defense programs, and collaborative European space initiatives drives the demand for advanced aerospace materials. The region's focus on sustainable aviation and technological innovation continues to shape the development of new aerospace materials.

Aerospace Materials Market in France

France stands as the largest market for aerospace materials in Europe, supported by its robust aerospace manufacturing sector and strong presence in both commercial and military aviation. The country's aerospace industry benefits from the presence of major aircraft manufacturers and their extensive supply chains. France's leadership in European space programs and significant investments in aerospace research and development further strengthen its position. The nation's commitment to developing next-generation aircraft and sustainable aviation technologies continues to drive innovation in aerospace materials.

Aerospace Materials Market in Germany

Germany emerges as the fastest-growing market in Europe, driven by its strong focus on technological innovation and manufacturing excellence in the aerospace sector. The country's aerospace industry benefits from extensive research and development activities and strong collaboration between industry and academic institutions. Germany's expertise in specialized aerospace components and materials manufacturing contributes to its growth trajectory. The nation's increasing investments in sustainable aviation technologies and space programs further support market expansion.

Aerospace Materials Market in Rest of World

The Rest of World region, encompassing South America and the Middle East & Africa, represents an emerging market for aerospace materials with significant growth potential. These regions are characterized by increasing investments in aerospace infrastructure and growing demand for commercial aviation services. In South America, Brazil emerges as the largest market, driven by its established aircraft manufacturing industry and growing defense sector. The Middle East demonstrates strong growth potential, particularly in the UAE and Saudi Arabia, supported by expanding commercial aviation sectors and increasing defense modernization programs. The regions' focus on developing domestic aerospace capabilities and increasing military modernization efforts continues to drive demand for aerospace materials.

Get Analysis on Important Geographic Markets

Download PDF

Aerospace Materials Industry Overview

Top Companies in Aerospace Materials Market

The aerospace materials market is characterized by intense innovation and strategic developments among key players like Toray Industries, BASF SE, Precision Castparts Corp, and PPG Industries. Companies are heavily investing in research and development to create advanced composite materials, high-performance alloys, and sustainable coating solutions that meet stringent aerospace requirements. Operational agility is demonstrated through vertical integration strategies, allowing manufacturers to control raw material supply and maintain quality standards. Strategic partnerships with aircraft manufacturers and long-term supply contracts have become crucial for maintaining market position. Geographic expansion, particularly in emerging aerospace hubs, and capacity enhancement through new manufacturing facilities represent key growth strategies. Companies are also focusing on developing environmentally sustainable materials and processes to align with industry-wide sustainability goals.

Consolidated Market with Strong Regional Players

The aerospace materials market exhibits a moderately consolidated structure with a mix of global chemical conglomerates and specialized aerospace materials companies. Global players leverage their extensive research capabilities, broad product portfolios, and established relationships with major aircraft manufacturers to maintain market dominance. Regional specialists have carved out strong positions in specific product categories like composites, alloys, or coatings, often serving local aerospace manufacturing clusters. The market has witnessed significant vertical integration, with major players acquiring smaller specialized manufacturers to enhance their technological capabilities and market reach.

Merger and acquisition activity in the sector is driven by the need to acquire advanced technologies, expand geographic presence, and strengthen product portfolios. Companies are particularly interested in acquiring firms with proprietary technologies in composite materials and high-performance coatings. The trend of consolidation is expected to continue as manufacturers seek to achieve economies of scale and enhance their ability to serve global aerospace manufacturers. Strategic alliances and joint ventures, especially in emerging markets, have become common approaches for market expansion and technology sharing.

Innovation and Sustainability Drive Future Success

Success in the aerospace materials industry increasingly depends on developing innovative, lightweight materials that enhance aircraft performance and fuel efficiency. Incumbent players must continue investing in research and development while maintaining strong relationships with key aerospace manufacturers through long-term supply agreements. Market leaders are focusing on developing sustainable materials and manufacturing processes to address growing environmental concerns in the aviation industry. The ability to provide comprehensive material solutions, including technical support and customization capabilities, has become crucial for maintaining competitive advantage.

New entrants and smaller players can gain aerospace market share by focusing on specialized niches within the aerospace materials sector, particularly in emerging technologies like advanced composites or sustainable materials. The high concentration of aerospace manufacturers and strict qualification requirements create significant barriers to entry, making strategic partnerships and certifications crucial for market success. Regulatory requirements, particularly regarding safety and environmental impact, continue to shape product development and market strategies. The risk of substitution remains relatively low due to the highly specialized nature of aerospace materials and stringent certification requirements, though innovation in alternative materials could impact specific market segments.

Aerospace Materials Market Leaders

-

BASF SE

-

Toray Industries Inc.

-

Hexcel Corporation

-

Solvay

-

Huntsman International LLC

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competiters?

Download PDF

Aerospace Materials Market News

- December 2023: Teijin Limited announced the manufacturing and sale of TenaxTM Carbon Fiber, produced from sustainable acrylonitrile (AN) waste and leftover materials from biomass products. The product finds applications in various industries, including aerospace.

- June 2023: Toray Industries highlighted its Next-generation Composite Material Solutions at the 2023 Paris Air Show. The company showcased TORAYCA carbon fiber, thermoset materials, and thermoplastic composites. Toray enabled the large-scale adoption of composites in commercial and general aviation and continues to pave the way for next-generation programs through valued new product launches.

- October 2022: Toray Composite Materials America partnered with SpecialityMaterials, a boron fiber manufacturer, to develop advanced next-generation aerospace materials with functional properties. This move will strengthen Toray's position in the aerospace materials market.

Aerospace Materials Market Report - Table of Contents

1. INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET DYNAMICS

-

4.1 Drivers

- 4.1.1 Increasing Use of Composites in Aircraft Manufacturing

- 4.1.2 Growing Space Industry

- 4.1.3 Increasing Government Spending on Defense in the United States and European Countries

-

4.2 Restraints

- 4.2.1 High Manufacturing Cost of Carbon Fibers

- 4.2.2 Declining Usage of Alloys

- 4.3 Industry Value Chain Analysis

-

4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5. MARKET SEGMENTATION (Market Size by Value)

-

5.1 Type

- 5.1.1 Structural

- 5.1.1.1 Composites

- 5.1.1.1.1 Glass Fiber

- 5.1.1.1.2 Carbon Fiber

- 5.1.1.1.3 Aramid Fiber

- 5.1.1.1.4 Other Composites

- 5.1.1.2 Plastics

- 5.1.1.3 Alloys

- 5.1.1.3.1 Titanium

- 5.1.1.3.2 Aluminium

- 5.1.1.3.3 Steel

- 5.1.1.3.4 Super

- 5.1.1.3.5 Magnesium

- 5.1.1.3.6 Other Alloys

- 5.1.2 Non-structural

- 5.1.2.1 Coatings

- 5.1.2.2 Adhesives and Sealants

- 5.1.2.2.1 Epoxy

- 5.1.2.2.2 Polyurethane

- 5.1.2.2.3 Silicone

- 5.1.2.2.4 Other Adhesives and Sealants

- 5.1.2.3 Foams

- 5.1.2.3.1 Polyethylene

- 5.1.2.3.2 Polyurethane

- 5.1.2.3.3 Other Foams

- 5.1.2.4 Seals

-

5.2 Aircraft Type

- 5.2.1 General and Commercial

- 5.2.2 Military and Defense

- 5.2.3 Space Vehicles

-

5.3 Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Spain

- 5.3.3.6 Russia

- 5.3.3.7 Rest of Europe

- 5.3.4 Rest of the World

- 5.3.4.1 South America

- 5.3.4.2 Middle East and Africa

6. COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

-

6.4 Company Profiles

- 6.4.1 3M

- 6.4.2 Acerinox SA (VDM Metals)

- 6.4.3 Akzo Nobel NV

- 6.4.4 Aluminum Corporation of China Limited (Chalco)

- 6.4.5 Arkema

- 6.4.6 ATI

- 6.4.7 Axalta Coating Systems

- 6.4.8 BASF SE

- 6.4.9 Beacon Adhesives Inc.

- 6.4.10 Carpenter Technology Corporation

- 6.4.11 Corporation VSMPO-AVISMA

- 6.4.12 DELO Industrie Klebstoffe GmbH & Co. KGaA

- 6.4.13 Evonik Industries AG

- 6.4.14 Greiner AG

- 6.4.15 Henkel AG & Co. KGaA

- 6.4.16 Hentzen Coatings Inc.

- 6.4.17 Hexcel Corporation

- 6.4.18 Howmet Aerospace

- 6.4.19 Huntsman International LLC

- 6.4.20 HYOSUNG

- 6.4.21 ISOVOLTA AG

- 6.4.22 Jiangsu Hengshen Co. Ltd

- 6.4.23 Mankiewicz Gebr & Co.

- 6.4.24 Mitsubishi Chemical Corporation

- 6.4.25 Nanjing Yunhai Special Metal Co. Ltd

- 6.4.26 NIPPON STEEL CORPORATION

- 6.4.27 PPG Industries Inc.

- 6.4.28 Precision Castparts Corp.

- 6.4.29 Reliance Industries Ltd

- 6.4.30 Rogers Corporation

- 6.4.31 SGL Carbon

- 6.4.32 Socomore

- 6.4.33 Solvay

- 6.4.34 Tata Steel (Corus)

- 6.4.35 The Sherwin-Williams Company

- 6.4.36 Toray Industries Inc.

- *List Not Exhaustive

7. MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Use of Carbon Nanotubes and Nano Additives with Epoxy Adhesives

**Subject to Availability

You Can Purchase Parts Of This Report. Check Out Prices For Specific Sections

Get Price Break-up Now

Aerospace Materials Industry Segmentation

Aerospace materials are critical in aircraft manufacturing and must possess various characteristics such as strength and high heat resistance. The materials should be durable and have a high tolerance to damage, which is essential for fuselages. These materials are also chosen for their long lifespan and reliability, especially for fatigue resistance.

The aerospace materials market is segmented by type, aircraft type, and geography. By type, the market is segmented into structural and non-structural materials. By aircraft type, the market is segmented into general and commercial, military and defense, and space vehicles. The report also covers the market size and forecasts for the aerospace materials market in 13 countries across the region. For each segment, the market sizing and forecasts are done based on revenue (USD).

| Type | Structural | Composites | Glass Fiber | |

| Carbon Fiber | ||||

| Aramid Fiber | ||||

| Other Composites | ||||

| Plastics | ||||

| Alloys | Titanium | |||

| Aluminium | ||||

| Steel | ||||

| Super | ||||

| Magnesium | ||||

| Other Alloys | ||||

| Non-structural | Coatings | |||

| Adhesives and Sealants | Epoxy | |||

| Polyurethane | ||||

| Silicone | ||||

| Other Adhesives and Sealants | ||||

| Foams | Polyethylene | |||

| Polyurethane | ||||

| Other Foams | ||||

| Seals | ||||

| Aircraft Type | General and Commercial | |||

| Military and Defense | ||||

| Space Vehicles | ||||

| Geography | Asia-Pacific | China | ||

| India | ||||

| Japan | ||||

| South Korea | ||||

| Rest of Asia-Pacific | ||||

| North America | United States | |||

| Canada | ||||

| Mexico | ||||

| Europe | Germany | |||

| United Kingdom | ||||

| France | ||||

| Italy | ||||

| Spain | ||||

| Russia | ||||

| Rest of Europe | ||||

| Rest of the World | South America | |||

| Middle East and Africa | ||||

Need A Different Region or Segment?

Customize Now

Aerospace Materials Market Research FAQs

How big is the Aerospace Materials Market?

The Aerospace Materials Market size is expected to reach USD 55.73 billion in 2025 and grow at a CAGR of greater than 8.20% to reach USD 82.65 billion by 2030.

What is the current Aerospace Materials Market size?

In 2025, the Aerospace Materials Market size is expected to reach USD 55.73 billion.

Who are the key players in Aerospace Materials Market?

BASF SE, Toray Industries Inc., Hexcel Corporation, Solvay and Huntsman International LLC are the major companies operating in the Aerospace Materials Market.

Which is the fastest growing region in Aerospace Materials Market?

Asia-Pacific is estimated to grow at the highest CAGR over the forecast period (2025-2030).

Which region has the biggest share in Aerospace Materials Market?

In 2025, the North America accounts for the largest market share in Aerospace Materials Market.

What years does this Aerospace Materials Market cover, and what was the market size in 2024?

In 2024, the Aerospace Materials Market size was estimated at USD 51.16 billion. The report covers the Aerospace Materials Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Aerospace Materials Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Our Best Selling Reports

Aerospace Materials Market Research

Mordor Intelligence provides a comprehensive analysis of the aerospace materials market. With decades of expertise in aerospace industry research, we offer a detailed examination of aerospace materials applications. Our report spans both commercial and defense sectors, offering crucial insights into aerospace industry growth patterns and emerging opportunities. We thoroughly analyze the global aerospace market size and key factors driving aerospace sector growth. This includes technological advancements in aeronautical materials and evolving industry dynamics.

Stakeholders gain valuable insights through our detailed assessment of aerospace market trends and aerospace market forecast data. This information is available in an easy-to-download report PDF format. The analysis covers commercial aircraft materials market developments and future aerospace materials innovations. It also includes a comprehensive aerospace market analysis. Our research provides strategic intelligence on aerospace materials companies and their contributions to the industry's evolution. We track the aerospace industry growth rate across various regions and applications. The report delivers actionable insights for businesses navigating the complex landscape of the aerospace and defense materials market. It is supported by robust data on aerospace market growth rate projections and regional market dynamics.