| Study Period | 2017 - 2029 |

| Base Year For Estimation | 2023 |

| Forecast Data Period | 2024 - 2029 |

| Market Size (2024) | USD 1.09 Billion |

| Market Size (2029) | USD 2.86 Billion |

| CAGR (2024 - 2029) | 21.39 % |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order |

Aerospace and Defence MLCC Market Analysis

The Aerospace and Defence MLCC Market size is estimated at 1.09 billion USD in 2024, and is expected to reach 2.86 billion USD by 2029, growing at a CAGR of 21.39% during the forecast period (2024-2029).

The aerospace and defense industry is experiencing unprecedented transformation driven by escalating global security concerns and technological advancements. North America continues to lead global military expenditure, reaching USD 912 billion in 2022, with the United States' aerospace and defense sector contributing USD 391 billion to the economy. This substantial investment has catalyzed rapid advancement in military modernization programs, particularly in electronic warfare systems and advanced avionics. The integration of artificial intelligence, the Internet of Things, and 5G communications into aerospace applications has created a pressing demand for more sophisticated electronics for defense components, especially in military aircraft and defense systems.

The space sector is witnessing remarkable growth, particularly in satellite technology and deployment. Industry projections indicate plans to launch over 20,000 satellites for observation and communication purposes within the next decade, fundamentally transforming space-based capabilities. This trend is exemplified by companies like Rocket Lab, which successfully completed 29 launches and deployed more than 150 satellites by December 2022. The industry's shift toward satellite miniaturization has revolutionized space technology, with developments ranging from palm-sized satellites to more complex CubeSat configurations, driving innovation in electronic components for aerospace design and manufacturing.

The integration of advanced avionics technologies is reshaping aircraft capabilities and operational efficiency. European defense spending surged by 14% to reach USD 345 billion in 2022, reflecting a strong focus on modernizing military aviation platforms. This investment has accelerated the adoption of sophisticated avionics systems, including enhanced flight control systems, advanced navigation capabilities, and improved communication networks. The trend toward miniaturization and weight reduction in avionics has become particularly prominent, driving the development of more compact and efficient electronics for defense components.

The unmanned aerial vehicle (UAV) and manned aerial vehicle (MAV) sectors are experiencing significant growth, supported by increased defense budgets worldwide. India's substantial defense budget allocation of INR 5.94 lakh crore for FY 2023-24 exemplifies the global trend of investing in advanced aerial capabilities. This investment has spurred the development of sophisticated electronic systems for both military and civilian applications, particularly in areas such as surveillance, reconnaissance, and tactical operations. The industry's focus on developing more capable autopilot systems and expanding real-time UAV applications has necessitated the integration of increasingly advanced electronic components for aerospace and systems.

Global Aerospace and Defence MLCC Market Trends

Growing demand for improved surveillance solutions is propelling the market

- The demand for MLCCs is rising in the aerospace and defense (A&D) sectors, especially in applications such as military aircraft and electronic warfare defense systems like UAVs. These industries require reliable power electronic systems that utilize components with specific functionalities. MLCCs are crucial in meeting these demands as they offer high reliability, optimal performance with a high-quality factor, effective EMI suppression, noise reduction, line filtering, energy storage capabilities, decoupling of high-frequency noise, and voltage regulation capabilities. MLCCs are critical in ensuring the dependable operation of UAVs and other aerospace and defense power electronic systems.

- The production of UAVs experienced a significant 14% increase from 3.847 million in 2021 to 4.448 million in 2022. This growth has led to a substantial rise in the demand for MLCCs, particularly for UAVs, specifically for high-voltage power supply applications. MLCCs play critical roles in UAVs as power supply bypass capacitors, input/output filters in DC-DC converters, smoothing capacitors, and essential components in digital circuits and LCD modules. A&D companies are increasingly recognizing the value and significance of MLCCs in meeting their specific requirements and enhancing the performance of their systems.

- Advancements in MLCCs, including smaller sizes and enhanced capabilities, have increased demand. This has led to the development of more capable autopilot systems and the expansion of real-time UAV applications facilitated by the compact integration of MLCCs without compromising functionality. Improved capabilities of MLCCs, such as high reliability and fast response times, have fueled the adoption of real-time UAV applications.

Understand The Key Trends Shaping This Market

Download PDF

Growing geopolitical tensions and the modernization plans to replace aging military aircraft are propelling military spending

- MLCCs are vital components in defense electronics, providing crucial energy storage and signal filtering capabilities. The demand for MLCCs is directly influenced by fluctuations in defense spending, with increased spending driving higher demand, particularly in areas such as missile systems and defense communication equipment. However, the decline in defense spending during the COVID-19 pandemic negatively affected the MLCC market as the industry shifted focus to medical technology. As defense spending stabilizes, the demand for MLCCs in defense electronics is expected to rebound.

- The COVID-19 pandemic had significant implications for defense electronics as global priorities shifted toward medical technology and laboratory test equipment. This led to a decline in demand for high-reliability defense electronics, requiring efforts to stabilize the high-voltage defense markets. The pandemic also adversely affected many defense vertical platforms, highlighting the importance of adaptability and resilience in the face of unexpected disruptions.

- Between 2012 and 2016, government-imposed sequestering resulted in a stagnant defense market. However, a notable turnaround occurred from 2017 to 2019, with remarkable growth in specific narrow end-market areas such as aircraft and space electronics. However, the pandemic disrupted this growth trajectory in 2020, causing an 11% decline in defense electronics demand. The shift in the US leadership restrained defense spending through 2022. Nonetheless, 2023 was expected to bring new opportunities in the small and precise European markets for defense electronics, focused on missiles and missile defense systems.

Segment Analysis: Vehicle Type

Manned Aerial Vehicle Segment in Aerospace and Defense MLCC Market

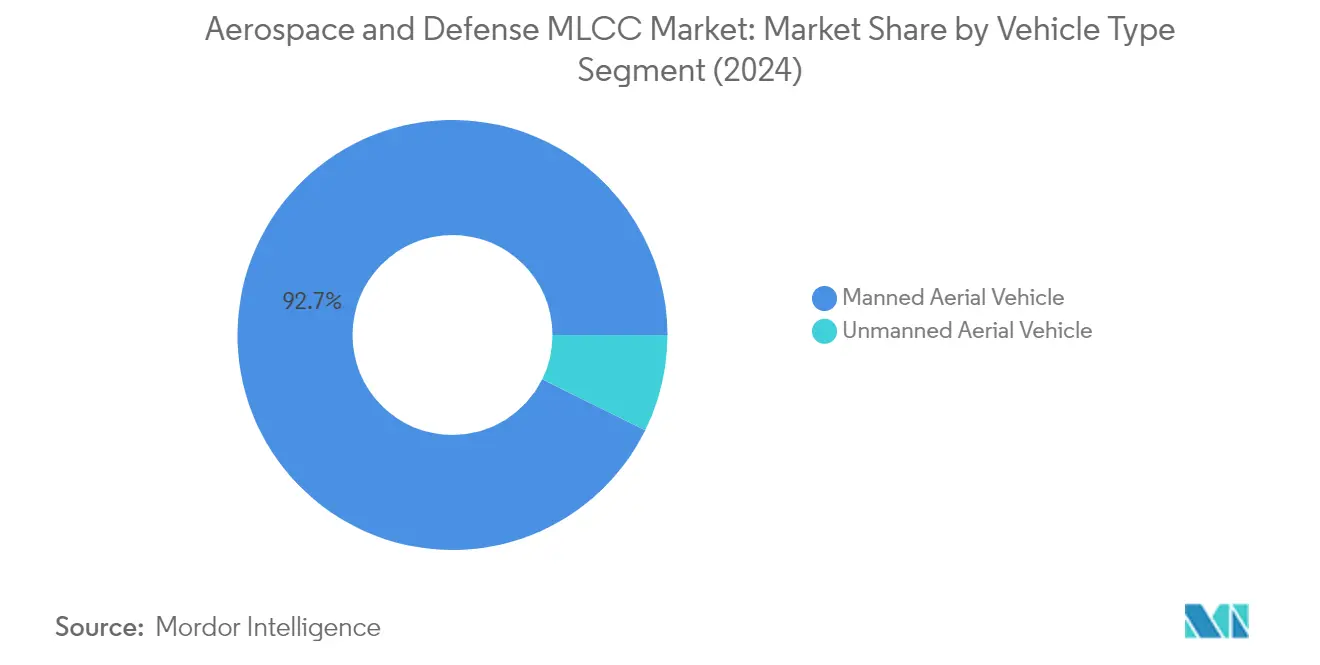

The Manned Aerial Vehicle (MAV) segment dominates the Aerospace and Defense MLCC market, commanding approximately 93% market share in 2024. This substantial market presence is driven by the increasing complexity of modern aircraft systems and the growing demand for reliable aerospace electronic components in commercial and military aviation. The segment's prominence is further reinforced by the surge in aircraft production worldwide, particularly in response to rising air travel demands and military modernization programs. MAVs require sophisticated electronic systems for navigation, communication, and flight control, making MLCCs essential components in ensuring stable and efficient operations. The newer generation aircraft's focus on better fuel efficiency, enhanced safety features for commercial aviation, and improved situational awareness for military applications has intensified the demand for high-quality MLCCs in this segment.

Unmanned Aerial Vehicle Segment in Aerospace and Defense MLCC Market

The Unmanned Aerial Vehicle (UAV) segment is experiencing remarkable growth in the Aerospace and Defense MLCC market, projected to expand at approximately 24% CAGR from 2024 to 2029. This exceptional growth trajectory is fueled by increasing investments in drone technology across military and commercial applications. The segment's expansion is particularly driven by the rising adoption of UAVs for surveillance, reconnaissance, and combat missions, necessitating advanced electronic systems that rely heavily on MLCCs. Technological advancements in UAV capabilities, including enhanced autonomous features and improved payload capacity, are creating a strong demand for reliable and high-performance aerospace electronic components. The integration of sophisticated sensors, communication systems, and control mechanisms in modern UAVs continues to drive the need for compact and efficient MLCCs, making this segment a key growth driver in the market.

Segment Analysis: Case Size

0 201 Segment in Aerospace and Defense MLCC Market

The 0 201 case size segment maintains its dominant position in the aerospace and defense MLCC market, commanding approximately 32% market share in 2024. This segment's prominence is driven by its extensive application in military aircraft and electronic warfare defense systems, particularly in UAVs. The compact form factor of 0 201 MLCCs makes them ideal for miniaturized avionic devices and systems, supporting crucial electronic components in flight control systems, navigation systems, and communication equipment. These MLCCs are particularly valued for their ability to ensure stable and efficient electronic components while enabling significant space savings in modern aerospace applications.

1 210 Segment in Aerospace and Defense MLCC Market

The 1 210 case size segment is experiencing remarkable growth in the aerospace and defense MLCC market. This segment's expansion is closely tied to the rising adoption of electric vertical takeoff and landing (eVTOL) technology, exemplified by prominent players such as Archer Aviation, Joby Aviation, and Lilium. The 1 210 MLCCs play integral roles in power distribution, control systems, and avionics within the eVTOL realm. These components are particularly crucial in managing power distribution, tempering heat dissipation, and ensuring steadfast operational reliability in advanced aircraft systems. The segment's growth is further supported by the increasing focus on hybrid-electric aircraft development and the expanding applications in power electronic systems.

Remaining Segments in Case Size

The other case sizes in the aerospace and defense MLCC market, including 0 402, 0 603, and 1 005, each serve specific applications and contribute significantly to the overall market dynamics. The 0 402 case size is particularly valued in air taxi applications and eVTOL vehicles, while 0 603 MLCCs are crucial in avionics, UAVs, radar systems, and communication equipment. The 1 005 case size finds its niche in satellite communication systems and data-intensive applications. These segments collectively provide a comprehensive range of solutions for various aerospace and defense applications, from compact designs for space-constrained applications to higher capacitance options for power management systems.

Segment Analysis: Voltage

Less than 600V Segment in Aerospace and Defense MLCC Market

The less than 600V segment maintains its dominant position in the aerospace and defense MLCC market, commanding approximately 48% of the market share in 2024. This segment's prominence is driven by its extensive application in advanced transport helicopters and modern avionics systems. The increasing global demand for transport helicopters across regions like Asia-Pacific, the Middle East, and North America has significantly boosted the adoption of less than 600V MLCCs. These components play a crucial role in ensuring efficient power distribution and robust electronic systems within these aircraft. The segment's growth is further supported by the surge in helicopter procurement worldwide, with notable acquisitions by various defense forces and commercial operators. The versatility of less than 600V MLCCs in supporting critical avionics functions, from communication systems to navigation equipment, continues to reinforce their market leadership.

More than 1100V Segment in Aerospace and Defense MLCC Market

The more than 1100V segment is emerging as the fastest-growing category in the aerospace and defense MLCC market, with an expected growth rate of approximately 20% from 2024 to 2029. This remarkable growth is primarily driven by the expanding realm of advanced multi-mission combat and attack helicopters. The strategic focus on bolstering combat capabilities has led defense forces to demand sophisticated rotorcraft equipped with cutting-edge technology. These high-voltage MLCCs are particularly crucial in power distribution, control systems, navigation, and communication applications within combat aircraft. The segment's growth is further accelerated by ongoing modernization efforts and heightened security imperatives driving helicopter procurement globally. The increasing complexity of modern warfare systems and the need for reliable high-voltage components in advanced military aircraft continue to fuel the demand for more than 1100V MLCCs.

Remaining Segments in Voltage Segmentation

The 600V to 1100V segment plays a vital role in the aerospace and defense MLCC market, particularly in satellite applications and specialized military equipment. This voltage range is especially crucial for satellite miniaturization efforts, where compact yet high-performance electronic components are essential. These MLCCs are integral to various space applications, from communication satellites to earth observation systems, offering the perfect balance between power handling capability and size constraints. The segment's significance is particularly evident in the growing small satellite market, where these components enable efficient power management and signal processing while maintaining the strict size and weight requirements of modern spacecraft designs. The continued evolution of space technology and increasing satellite launches maintain the steady demand for MLCCs in this voltage range.

Segment Analysis: Capacitance

Less than 10 μF Segment in Aerospace and Defense MLCC Market

The less than 10 1⁄4F segment maintains its dominant position in the aerospace and defense MLCC market, commanding approximately 48% market share in 2024. This segment's prominence is driven by the increasing adoption of smart technology for surveillance, analysis, and imaging applications, particularly in unmanned aerial vehicles (UAVs). The compact size and lower capacitance values make these MLCCs ideal for miniaturized electronic systems in modern aerospace applications. These components play a crucial role in ensuring stable power distribution, signal processing, and noise suppression in critical avionics systems. The segment's growth is further supported by the rising demand for advanced avionics computers and sophisticated mission control capabilities across fixed-wing aircraft, helicopters, and drones. The integration of artificial intelligence, IoT, and 5G communications in aerospace applications continues to drive the demand for these lower capacitance MLCCs.

More than 100 μF Segment in Aerospace and Defense MLCC Market

The more than 100 1⁄4F segment is experiencing the fastest growth trajectory in the aerospace and defense MLCC market, with an expected CAGR of approximately 20% from 2024 to 2029. This remarkable growth is primarily attributed to the increasing demand for high-capacitance MLCCs in widebody aircraft applications, where complex avionics, communication systems, and advanced in-flight amenities require robust power management solutions. The segment's expansion is further driven by the aviation industry's shift toward more sophisticated electronic systems that demand higher capacitance values for improved energy storage and power stability. These high-capacitance MLCCs are becoming increasingly critical in powering advanced avionics and systems that drive widebody aircraft's efficiency, safety, and passenger experience. The segment's growth is also supported by ongoing technological advancements in MLCC manufacturing, enabling the production of more reliable and efficient high-capacitance components suitable for aerospace applications.

Remaining Segments in Capacitance

The 10 1⁄4F to 100 1⁄4F segment serves as a crucial intermediate range in the aerospace and defense MLCC market, bridging the gap between low and high capacitance applications. This segment plays a vital role in supporting various critical functions within narrowbody aircraft, which currently dominate the global passenger aircraft category. These MLCCs are particularly valuable in applications requiring moderate energy storage and filtering capabilities, such as power distribution systems, control units, and communication equipment. The segment's versatility makes it essential for both civilian and military aircraft applications, contributing significantly to the overall market dynamics. The balanced characteristics of these medium-range capacitors make them suitable for a wide range of aerospace and defense applications, from basic electronic systems to more complex avionics configurations.

Segment Analysis: Dielectric Type

Class 2 Segment in Aerospace and Defense MLCC Market

Class 2 MLCCs have emerged as the dominant force in the aerospace and defense MLCC market, commanding approximately 56% of the total market share in 2024. These capacitors play a pivotal role within avionics and electronic systems, contributing significantly to stable and reliable operations of communication, navigation, and control systems across diverse aircraft types. The segment's prominence is particularly evident in the Asia-Pacific region, where the demand for advanced aircraft and cutting-edge technology continues to drive significant growth and modernization efforts. Class 2 MLCCs are extensively utilized in widebody aircraft, with their complex avionics, communication systems, and advanced in-flight amenities relying heavily on these high-capacitance MLCCs to ensure seamless functionality and enhanced passenger experience. Their robust performance characteristics and reliability in demanding aerospace environments have made them indispensable components in powering avionics and systems that drive efficiency, safety, and overall operational excellence in modern aircraft.

Class 1 Segment in Aerospace and Defense MLCC Market

Class 1 MLCCs are experiencing remarkable growth momentum, projected to expand at approximately 22% CAGR from 2024 to 2029. These capacitors epitomize reliability, durability, and compactness, qualities that flourish within the rigorous aerospace environment. The segment's growth is being driven by their crucial role in ensuring the seamless operation of critical communication, navigation, and power distribution systems that underpin advanced aircraft. The increasing adoption of Class 1 MLCCs is particularly notable in cutting-edge applications such as Urban Aeronautics' revolutionary CityHawk and advanced electric vertical takeoff and landing (eVTOL) vehicles. Their exceptional performance in maintaining signal integrity, optimizing energy conversion, and facilitating inter-system communication has made them indispensable in hybrid-electric aircraft development. The integration of Universal Avionics' ClearVision Enhanced Flight Vision System (EFVS) and other advanced avionics systems further underscores the growing importance of Class 1 MLCCs in enabling next-generation aerospace technologies.

Aerospace and Defence MLCC Market Geography Segment Analysis

Aerospace and Defense MLCC Market in Asia-Pacific

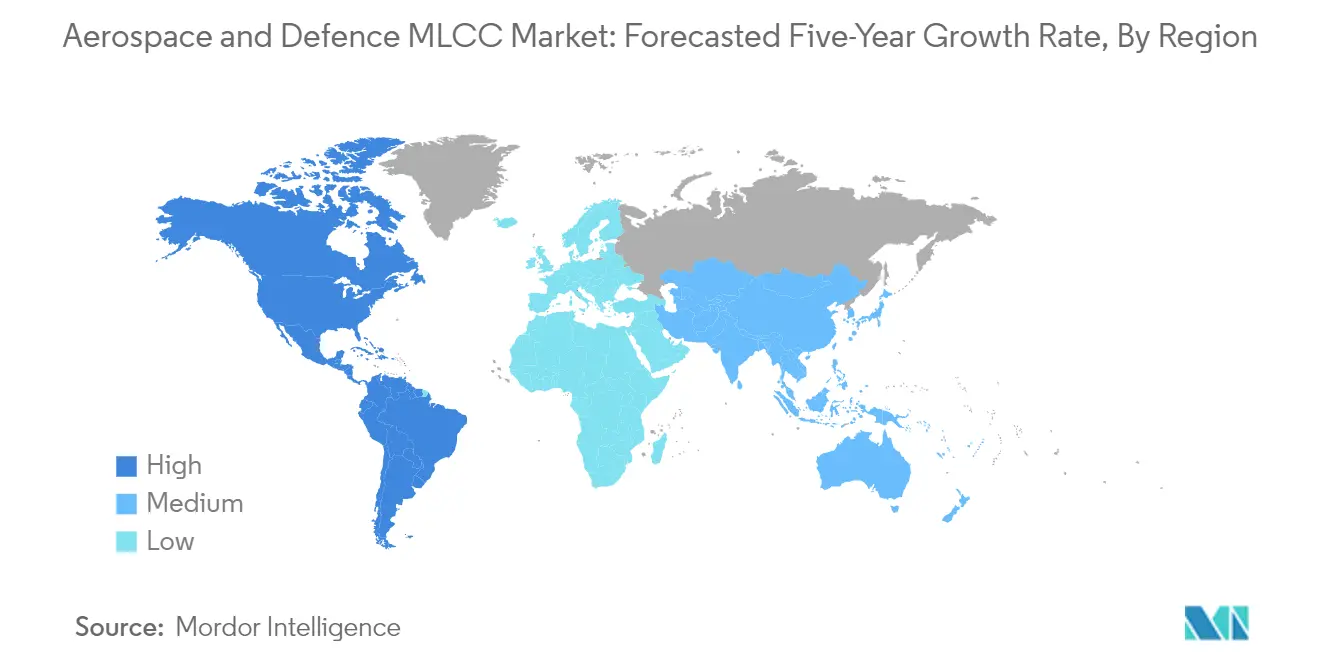

Asia-Pacific stands as a dynamic epicenter of aerospace and defense MLCC market development, commanding approximately 44% of the global market share in 2024. The region's dominance is driven by substantial investments from powerhouse nations like China, South Korea, India, and Japan in bolstering their aerospace and defense industries. These strategic endeavors serve a dual purpose: safeguarding national security while nurturing economic prosperity through advanced aerospace and defense capabilities. The region's commitment to technological advancement is evident in its focus on developing sophisticated military electronic equipment, where MLCCs play a crucial role in maintaining signal integrity and noise reduction. The emphasis on indigenous manufacturing capabilities, particularly in countries like India and China, has created a robust ecosystem for MLCC production and implementation. Furthermore, the increasing adoption of unmanned aerial vehicles (UAVs) and advanced avionics systems has amplified the demand for high-reliability MLCCs. The region's focus on modernizing military aircraft fleets and enhancing electronic warfare capabilities continues to drive the market's expansion, making Asia-Pacific a crucial hub for aerospace and defense MLCC innovations.

Aerospace and Defense MLCC Market in Europe

Europe has emerged as a significant force in the aerospace and defense MLCC market, demonstrating a robust growth trajectory with approximately 13% growth from 2019 to 2024. The region's market dynamics are shaped by its strong commitment to defense modernization and technological advancement in military capabilities. European defense enterprises have established themselves as industry leaders in innovation, particularly in areas such as UAVs, advanced avionics, and satellite communications. The region's focus on developing next-generation military aircraft and electronic warfare systems has created sustained demand for high-performance MLCCs. The emphasis on indigenous defense capabilities and the presence of major aerospace manufacturers has fostered a sophisticated ecosystem for MLCC applications. European nations' commitment to enhancing their defense preparedness has led to increased investments in defense electronics, particularly in critical applications requiring high reliability and performance. The region's strong research and development infrastructure, coupled with stringent quality standards, has positioned Europe as a key market for advanced MLCC technologies in aerospace and defense applications.

Aerospace and Defense MLCC Market in North America

North America continues to demonstrate robust market potential in the aerospace and defense MLCC sector, with projections indicating a strong growth rate of approximately 23% from 2024 to 2029. The region's market is characterized by its advanced technological infrastructure and substantial investments in military modernization programs. North America's leadership in defense innovation, particularly in the United States, drives the continuous development and implementation of cutting-edge MLCC technologies. The region's focus on electronic warfare capabilities and advanced military aircraft systems creates sustained demand for high-performance MLCCs. The presence of major aerospace and defense contractors, coupled with significant research and development investments, fosters an environment conducive to MLCC market growth. The emphasis on maintaining technological superiority in defense systems, particularly in areas such as radar systems, communication equipment, and advanced avionics, continues to drive the demand for sophisticated MLCCs. The region's commitment to developing next-generation military platforms and the increasing focus on unmanned systems further strengthens the market outlook for aerospace and defense MLCCs. The North American defense electronics market is poised for significant growth, driven by these strategic initiatives.

Aerospace and Defense MLCC Market in Rest of the World

The Rest of the World region, encompassing the Middle East, Africa, and South America, represents an emerging market for aerospace and defense MLCCs, characterized by unique regional dynamics and growing defense modernization efforts. These regions face distinct challenges, including geopolitical tensions and the need to enhance military capabilities, driving investments in advanced defense electronics. The Middle East, in particular, demonstrates strong potential due to its focus on military modernization and the acquisition of advanced defense systems. Countries in these regions are increasingly prioritizing the development of indigenous defense capabilities, creating opportunities for MLCC applications in military electronics. The growing emphasis on enhancing air defense systems and modernizing military aircraft fleets continues to drive demand for high-reliability MLCCs. The region's diverse security challenges and the need for sophisticated defense electronics create a sustained market for MLCCs in various military applications. The increasing focus on developing local defense manufacturing capabilities and the adoption of advanced military technologies continue to shape the market landscape for aerospace and defense MLCCs in these regions.

Get Analysis on Important Geographic Markets

Download PDF

Aerospace and Defence MLCC Industry Overview

Top Companies in Aerospace and Defense MLCC Market

The aerospace and defense MLCC market is characterized by continuous product innovation focused on miniaturization, enhanced reliability, and performance optimization. Companies are investing heavily in research and development to create MLCCs with higher capacitance values while maintaining compact form factors. Operational agility is demonstrated through smart manufacturing initiatives, with major players implementing data-driven production processes and automated quality control systems. Strategic moves in the industry primarily revolve around expanding manufacturing capabilities, particularly in Asia-Pacific regions, to meet growing demand and ensure supply chain resilience. Market leaders are also focusing on sustainability initiatives, including the development of recycling systems for production materials and the implementation of environmentally conscious manufacturing practices.

Consolidated Market with Strong Global Leaders

The aerospace and defense MLCC market exhibits a highly consolidated structure dominated by global conglomerates with extensive manufacturing capabilities and technological expertise. These major players, primarily based in Asia, possess significant advantages through their vertically integrated operations, established distribution networks, and long-standing relationships with key aerospace and defense contractors. The market is characterized by high entry barriers due to stringent quality requirements, certification needs, and substantial capital investments required for manufacturing facilities. The presence of specialized manufacturers remains limited, with most focusing on niche applications or specific regional markets.

The industry has witnessed strategic consolidations through mergers and acquisitions, particularly aimed at expanding technological capabilities and geographic reach. Major conglomerates have strengthened their market positions by acquiring smaller, specialized manufacturers to enhance their product portfolios and access new customer segments. This consolidation trend has been driven by the need to achieve economies of scale, optimize research and development resources, and maintain competitive advantages in an increasingly demanding market environment. The dominance of established players has created significant challenges for new entrants, leading to a relatively stable competitive landscape.

Innovation and Adaptability Drive Future Success

For incumbent players to maintain and expand their market share, continuous investment in technological innovation and manufacturing capabilities remains crucial. Leading companies must focus on developing next-generation MLCCs that meet the evolving requirements of advanced aerospace and defense systems, particularly in areas such as unmanned aerial vehicles and electronic warfare. Establishing strong partnerships with key aerospace manufacturers and defense contractors, while maintaining high quality standards and reliability, will be essential for long-term success. Additionally, incumbents need to strengthen their supply chain resilience and expand their global manufacturing footprint to mitigate geopolitical risks and ensure consistent supply.

Contenders seeking to gain ground in this market must focus on developing specialized capabilities and targeting specific market segments where they can establish competitive advantages. This includes investing in innovative technologies, such as advanced materials and manufacturing processes, that can differentiate their products from established players. Building strong relationships with tier-two aerospace and defense manufacturers, while maintaining compliance with stringent industry standards and regulations, will be crucial for market entry and growth. The increasing focus on indigenous manufacturing in various countries presents opportunities for regional players to establish themselves as reliable suppliers, though success will depend on their ability to meet the industry's high quality and reliability requirements. The defense electronics industry is also seeing a rise in demand for specialized aerospace electronic components, which presents further opportunities for growth.

Aerospace and Defence MLCC Market Leaders

-

Murata Manufacturing Co., Ltd

-

Samsung Electro-Mechanics

-

Taiyo Yuden Co., Ltd

-

Walsin Technology Corporation

-

Yageo Corporation

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competiters?

Download PDF

Aerospace and Defence MLCC Market News

- June 2023: The growing demand for industrial equipments has driven the company to introduce NTS/NTF NTS/NTF Series of SMD type MLCC. These capacitors are rated with 25 to 500 Vdc with a capacitance ranging from 0.010 to 47µF. These MLCCs are used in on-board power supplies,voltage regulators for computers,smoothing circuit of DC-DC converters,etc.

- February 2023: Kyocera AVX introduced MIL-PRF-32535 BME NP0 MLCCs that are compact, high-CV MLCCs approved for the Defense Logistics Agency (DLA) Qualified Products Database. The new MLCCs are designed to enable board space, weight, and component count reductions for high-reliability military applications (QPD). In addition, the products are patented with the company's Flexiterm technology, which enhances the product's resistance to thermomechanical stresses during its operation in harsh environments.

- October 2022: Vishay introduced a new line of surface-mount MLCC to serve DC-blocking applications better. In RF, Bluetooth, 5G, military radios, fiber optic lines, and high-frequency data links applications, the MLCCs effectively carry the necessary AC signal over the chosen frequency band with less than 0.5 dB insertion loss, removing the need for more expensive broadband blocks.

Free With This Report

We provide a complimentary and exhaustive set of data points on the country and regional level metrics that present the fundamental structure of the industry. Presented in the form of 40+ free charts, the sections cover difficult to find data on various indicators including but not limited to smartphones sales, raw materials pricing trends, and EV sales etc

Aerospace and Defence MLCC Market Report - Table of Contents

1. EXECUTIVE SUMMARY & KEY FINDINGS

2. REPORT OFFERS

3. INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4. KEY INDUSTRY TRENDS

-

4.1 Aerial Vehicle Production

- 4.1.1 Global Unmanned Aerial Vehicles Production

-

4.2 Military Spending

- 4.2.1 Global Military Spending

- 4.3 Regulatory Framework

- 4.4 Value Chain & Distribution Channel Analysis

5. MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2029 and analysis of growth prospects)

-

5.1 Vehicle Type

- 5.1.1 Manned Aerial Vehicle

- 5.1.2 Unmanned Aerial Vehicle

-

5.2 Case Size

- 5.2.1 0 201

- 5.2.2 0 402

- 5.2.3 0 603

- 5.2.4 1 005

- 5.2.5 1 210

- 5.2.6 Others

-

5.3 Voltage

- 5.3.1 600V to 1100V

- 5.3.2 Less than 600V

- 5.3.3 More than 1100V

-

5.4 Capacitance

- 5.4.1 10 μF to 100 μF

- 5.4.2 Less than 10 μF

- 5.4.3 More than 100 μF

-

5.5 Dielectric Type

- 5.5.1 Class 1

- 5.5.2 Class 2

-

5.6 Region

- 5.6.1 Asia-Pacific

- 5.6.2 Europe

- 5.6.3 North America

- 5.6.4 Rest of the World

6. COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

-

6.4 Company Profiles

- 6.4.1 Kyocera AVX Components Corporation (Kyocera Corporation)

- 6.4.2 Maruwa Co ltd

- 6.4.3 Murata Manufacturing Co., Ltd

- 6.4.4 Nippon Chemi-Con Corporation

- 6.4.5 Samsung Electro-Mechanics

- 6.4.6 Samwha Capacitor Group

- 6.4.7 Taiyo Yuden Co., Ltd

- 6.4.8 TDK Corporation

- 6.4.9 Vishay Intertechnology Inc.

- 6.4.10 Walsin Technology Corporation

- 6.4.11 Yageo Corporation

- *List Not Exhaustive

7. KEY STRATEGIC QUESTIONS FOR MLCC CEOS

8. APPENDIX

-

8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter’s Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

You Can Purchase Parts Of This Report. Check Out Prices For Specific Sections

Get Price Break-up Now

List of Tables & Figures

- Figure 1:

- VALUE OF MILITARY SPENDING, BILLION, GLOBAL, 2017 - 2022

- Figure 2:

- VOLUME OF GLOBAL AEROSPACE AND DEFENCE MLCC MARKET, USD, GLOBAL, 2017 - 2029

- Figure 3:

- VALUE OF GLOBAL AEROSPACE AND DEFENCE MLCC MARKET, USD, GLOBAL, 2017 - 2029

- Figure 4:

- VOLUME OF GLOBAL AEROSPACE AND DEFENCE MLCC MARKET BY VEHICLE TYPE, , GLOBAL, 2017 - 2029

- Figure 5:

- VALUE OF GLOBAL AEROSPACE AND DEFENCE MLCC MARKET BY VEHICLE TYPE, USD, GLOBAL, 2017 - 2029

- Figure 6:

- VALUE SHARE OF GLOBAL AEROSPACE AND DEFENCE MLCC MARKET BY VEHICLE TYPE, %, GLOBAL, 2017 - 2029

- Figure 7:

- VOLUME SHARE OF GLOBAL AEROSPACE AND DEFENCE MLCC MARKET BY VEHICLE TYPE, %, GLOBAL, 2017 - 2029

- Figure 8:

- VOLUME OF MANNED AERIAL VEHICLE AEROSPACE AND DEFENCE MLCC MARKET, NUMBER, , GLOBAL, 2017 - 2029

- Figure 9:

- VALUE OF MANNED AERIAL VEHICLE AEROSPACE AND DEFENCE MLCC MARKET, USD, GLOBAL, 2017 - 2029

- Figure 10:

- VOLUME OF UNMANNED AERIAL VEHICLE AEROSPACE AND DEFENCE MLCC MARKET, NUMBER, , GLOBAL, 2017 - 2029

- Figure 11:

- VALUE OF UNMANNED AERIAL VEHICLE AEROSPACE AND DEFENCE MLCC MARKET, USD, GLOBAL, 2017 - 2029

- Figure 12:

- VOLUME OF GLOBAL AEROSPACE AND DEFENCE MLCC MARKET BY CASE SIZE, , GLOBAL, 2017 - 2029

- Figure 13:

- VALUE OF GLOBAL AEROSPACE AND DEFENCE MLCC MARKET BY CASE SIZE, USD, GLOBAL, 2017 - 2029

- Figure 14:

- VALUE SHARE OF GLOBAL AEROSPACE AND DEFENCE MLCC MARKET BY CASE SIZE, %, GLOBAL, 2017 - 2029

- Figure 15:

- VOLUME SHARE OF GLOBAL AEROSPACE AND DEFENCE MLCC MARKET BY CASE SIZE, %, GLOBAL, 2017 - 2029

- Figure 16:

- VOLUME OF 0 201 AEROSPACE AND DEFENCE MLCC MARKET, NUMBER, , GLOBAL, 2017 - 2029

- Figure 17:

- VALUE OF 0 201 AEROSPACE AND DEFENCE MLCC MARKET, USD, GLOBAL, 2017 - 2029

- Figure 18:

- VOLUME OF 0 402 AEROSPACE AND DEFENCE MLCC MARKET, NUMBER, , GLOBAL, 2017 - 2029

- Figure 19:

- VALUE OF 0 402 AEROSPACE AND DEFENCE MLCC MARKET, USD, GLOBAL, 2017 - 2029

- Figure 20:

- VOLUME OF 0 603 AEROSPACE AND DEFENCE MLCC MARKET, NUMBER, , GLOBAL, 2017 - 2029

- Figure 21:

- VALUE OF 0 603 AEROSPACE AND DEFENCE MLCC MARKET, USD, GLOBAL, 2017 - 2029

- Figure 22:

- VOLUME OF 1 005 AEROSPACE AND DEFENCE MLCC MARKET, NUMBER, , GLOBAL, 2017 - 2029

- Figure 23:

- VALUE OF 1 005 AEROSPACE AND DEFENCE MLCC MARKET, USD, GLOBAL, 2017 - 2029

- Figure 24:

- VOLUME OF 1 210 AEROSPACE AND DEFENCE MLCC MARKET, NUMBER, , GLOBAL, 2017 - 2029

- Figure 25:

- VALUE OF 1 210 AEROSPACE AND DEFENCE MLCC MARKET, USD, GLOBAL, 2017 - 2029

- Figure 26:

- VOLUME OF OTHERS AEROSPACE AND DEFENCE MLCC MARKET, NUMBER, , GLOBAL, 2017 - 2029

- Figure 27:

- VALUE OF OTHERS AEROSPACE AND DEFENCE MLCC MARKET, USD, GLOBAL, 2017 - 2029

- Figure 28:

- VOLUME OF GLOBAL AEROSPACE AND DEFENCE MLCC MARKET BY VOLTAGE, , GLOBAL, 2017 - 2029

- Figure 29:

- VALUE OF GLOBAL AEROSPACE AND DEFENCE MLCC MARKET BY VOLTAGE, USD, GLOBAL, 2017 - 2029

- Figure 30:

- VALUE SHARE OF GLOBAL AEROSPACE AND DEFENCE MLCC MARKET BY VOLTAGE, %, GLOBAL, 2017 - 2029

- Figure 31:

- VOLUME SHARE OF GLOBAL AEROSPACE AND DEFENCE MLCC MARKET BY VOLTAGE, %, GLOBAL, 2017 - 2029

- Figure 32:

- VOLUME OF 600V TO 1100V AEROSPACE AND DEFENCE MLCC MARKET, NUMBER, , GLOBAL, 2017 - 2029

- Figure 33:

- VALUE OF 600V TO 1100V AEROSPACE AND DEFENCE MLCC MARKET, USD, GLOBAL, 2017 - 2029

- Figure 34:

- VOLUME OF LESS THAN 600V AEROSPACE AND DEFENCE MLCC MARKET, NUMBER, , GLOBAL, 2017 - 2029

- Figure 35:

- VALUE OF LESS THAN 600V AEROSPACE AND DEFENCE MLCC MARKET, USD, GLOBAL, 2017 - 2029

- Figure 36:

- VOLUME OF MORE THAN 1100V AEROSPACE AND DEFENCE MLCC MARKET, NUMBER, , GLOBAL, 2017 - 2029

- Figure 37:

- VALUE OF MORE THAN 1100V AEROSPACE AND DEFENCE MLCC MARKET, USD, GLOBAL, 2017 - 2029

- Figure 38:

- VOLUME OF GLOBAL AEROSPACE AND DEFENCE MLCC MARKET BY CAPACITANCE, , GLOBAL, 2017 - 2029

- Figure 39:

- VALUE OF GLOBAL AEROSPACE AND DEFENCE MLCC MARKET BY CAPACITANCE, USD, GLOBAL, 2017 - 2029

- Figure 40:

- VALUE SHARE OF GLOBAL AEROSPACE AND DEFENCE MLCC MARKET BY CAPACITANCE, %, GLOBAL, 2017 - 2029

- Figure 41:

- VOLUME SHARE OF GLOBAL AEROSPACE AND DEFENCE MLCC MARKET BY CAPACITANCE, %, GLOBAL, 2017 - 2029

- Figure 42:

- VOLUME OF 10 ΜF TO 100 ΜF AEROSPACE AND DEFENCE MLCC MARKET, NUMBER, , GLOBAL, 2017 - 2029

- Figure 43:

- VALUE OF 10 ΜF TO 100 ΜF AEROSPACE AND DEFENCE MLCC MARKET, USD, GLOBAL, 2017 - 2029

- Figure 44:

- VOLUME OF LESS THAN 10 ΜF AEROSPACE AND DEFENCE MLCC MARKET, NUMBER, , GLOBAL, 2017 - 2029

- Figure 45:

- VALUE OF LESS THAN 10 ΜF AEROSPACE AND DEFENCE MLCC MARKET, USD, GLOBAL, 2017 - 2029

- Figure 46:

- VOLUME OF MORE THAN 100 ΜF AEROSPACE AND DEFENCE MLCC MARKET, NUMBER, , GLOBAL, 2017 - 2029

- Figure 47:

- VALUE OF MORE THAN 100 ΜF AEROSPACE AND DEFENCE MLCC MARKET, USD, GLOBAL, 2017 - 2029

- Figure 48:

- VOLUME OF GLOBAL AEROSPACE AND DEFENCE MLCC MARKET BY DIELECTRIC TYPE, , GLOBAL, 2017 - 2029

- Figure 49:

- VALUE OF GLOBAL AEROSPACE AND DEFENCE MLCC MARKET BY DIELECTRIC TYPE, USD, GLOBAL, 2017 - 2029

- Figure 50:

- VALUE SHARE OF GLOBAL AEROSPACE AND DEFENCE MLCC MARKET BY DIELECTRIC TYPE, %, GLOBAL, 2017 - 2029

- Figure 51:

- VOLUME SHARE OF GLOBAL AEROSPACE AND DEFENCE MLCC MARKET BY DIELECTRIC TYPE, %, GLOBAL, 2017 - 2029

- Figure 52:

- VOLUME OF CLASS 1 AEROSPACE AND DEFENCE MLCC MARKET, NUMBER, , GLOBAL, 2017 - 2029

- Figure 53:

- VALUE OF CLASS 1 AEROSPACE AND DEFENCE MLCC MARKET, USD, GLOBAL, 2017 - 2029

- Figure 54:

- VOLUME OF CLASS 2 AEROSPACE AND DEFENCE MLCC MARKET, NUMBER, , GLOBAL, 2017 - 2029

- Figure 55:

- VALUE OF CLASS 2 AEROSPACE AND DEFENCE MLCC MARKET, USD, GLOBAL, 2017 - 2029

- Figure 56:

- VOLUME OF AEROSPACE AND DEFENCE MLCC MARKET, BY REGION, NUMBER, , 2017 - 2029

- Figure 57:

- VALUE OF AEROSPACE AND DEFENCE MLCC MARKET, BY REGION, USD, 2017 - 2029

- Figure 58:

- CAGR OF AEROSPACE AND DEFENCE MLCC MARKET, BY REGION, %, 2017 - 2029

- Figure 59:

- CAGR OF AEROSPACE AND DEFENCE MLCC MARKET, BY REGION, %, 2017 - 2029

- Figure 60:

- VOLUME OF GLOBAL AEROSPACE AND DEFENCE MLCC MARKET,NUMBER, IN ASIA-PACIFIC, 2017 - 2029

- Figure 61:

- VALUE OF GLOBAL AEROSPACE AND DEFENCE MLCC MARKET, IN ASIA-PACIFIC, 2017 - 2029

- Figure 62:

- VOLUME OF GLOBAL AEROSPACE AND DEFENCE MLCC MARKET,NUMBER, IN EUROPE, 2017 - 2029

- Figure 63:

- VALUE OF GLOBAL AEROSPACE AND DEFENCE MLCC MARKET, IN EUROPE, 2017 - 2029

- Figure 64:

- VOLUME OF GLOBAL AEROSPACE AND DEFENCE MLCC MARKET,NUMBER, IN NORTH AMERICA, 2017 - 2029

- Figure 65:

- VALUE OF GLOBAL AEROSPACE AND DEFENCE MLCC MARKET, IN NORTH AMERICA, 2017 - 2029

- Figure 66:

- VOLUME OF GLOBAL AEROSPACE AND DEFENCE MLCC MARKET,NUMBER, IN REST OF THE WORLD, 2017 - 2029

- Figure 67:

- VALUE OF GLOBAL AEROSPACE AND DEFENCE MLCC MARKET, IN REST OF THE WORLD, 2017 - 2029

- Figure 68:

- MOST ACTIVE COMPANIES BY NUMBER OF STRATEGIC MOVES, COUNT, GLOBAL, 2017 - 2029

- Figure 69:

- MOST ADOPTED STRATEGIES, COUNT, GLOBAL, 2017 - 2029

- Figure 70:

- VALUE SHARE OF MAJOR PLAYERS, %, GLOBAL, 2017 - 2029

Aerospace and Defence MLCC Industry Segmentation

Manned Aerial Vehicle, Unmanned Aerial Vehicle are covered as segments by Vehicle Type. 0 201, 0 402, 0 603, 1 005, 1 210, Others are covered as segments by Case Size. 600V to 1100V, Less than 600V, More than 1100V are covered as segments by Voltage. 10 μF to 100 μF, Less than 10 μF, More than 100 μF are covered as segments by Capacitance. Class 1, Class 2 are covered as segments by Dielectric Type. Asia-Pacific, Europe, North America are covered as segments by Region.| Vehicle Type | Manned Aerial Vehicle |

| Unmanned Aerial Vehicle | |

| Case Size | 0 201 |

| 0 402 | |

| 0 603 | |

| 1 005 | |

| 1 210 | |

| Others | |

| Voltage | 600V to 1100V |

| Less than 600V | |

| More than 1100V | |

| Capacitance | 10 μF to 100 μF |

| Less than 10 μF | |

| More than 100 μF | |

| Dielectric Type | Class 1 |

| Class 2 | |

| Region | Asia-Pacific |

| Europe | |

| North America | |

| Rest of the World |

Need A Different Region or Segment?

Customize Now

Market Definition

- MLCC (Multilayer Ceramic Capacitor) - A type of capacitor that consists of multiple layers of ceramic material, alternating with conductive layers, used for energy storage and filtering in electronic circuits.

- Voltage - The maximum voltage that a capacitor can safely withstand without experiencing breakdown or failure. It is typically expressed in volts (V)

- Capacitance - The measure of a capacitor's ability to store electrical charge, expressed in farads (F). It determines the amount of energy that can be stored in the capacitor

- Case Size - The physical dimensions of an MLCC, typically expressed in codes or millimeters, indicating its length, width, and height

| Keyword | Definition |

|---|---|

| MLCC (Multilayer Ceramic Capacitor) | A type of capacitor that consists of multiple layers of ceramic material, alternating with conductive layers, used for energy storage and filtering in electronic circuits. |

| Capacitance | The measure of a capacitor's ability to store electrical charge, expressed in farads (F). It determines the amount of energy that can be stored in the capacitor |

| Voltage Rating | The maximum voltage that a capacitor can safely withstand without experiencing breakdown or failure. It is typically expressed in volts (V) |

| ESR (Equivalent Series Resistance) | The total resistance of a capacitor, including its internal resistance and parasitic resistances. It affects the capacitor's ability to filter high-frequency noise and maintain stability in a circuit. |

| Dielectric Material | The insulating material used between the conductive layers of a capacitor. In MLCCs, commonly used dielectric materials include ceramic materials like barium titanate and ferroelectric materials |

| SMT (Surface Mount Technology) | A method of electronic component assembly that involves mounting components directly onto the surface of a printed circuit board (PCB) instead of through-hole mounting. |

| Solderability | The ability of a component, such as an MLCC, to form a reliable and durable solder joint when subjected to soldering processes. Good solderability is crucial for proper assembly and functionality of MLCCs on PCBs. |

| RoHS (Restriction of Hazardous Substances) | A directive that restricts the use of certain hazardous materials, such as lead, mercury, and cadmium, in electrical and electronic equipment. Compliance with RoHS is essential for automotive MLCCs due to environmental regulations |

| Case Size | The physical dimensions of an MLCC, typically expressed in codes or millimeters, indicating its length, width, and height |

| Flex Cracking | A phenomenon where MLCCs can develop cracks or fractures due to mechanical stress caused by bending or flexing of the PCB. Flex cracking can lead to electrical failures and should be avoided during PCB assembly and handling. |

| Aging | MLCCs can experience changes in their electrical properties over time due to factors like temperature, humidity, and applied voltage. Aging refers to the gradual alteration of MLCC characteristics, which can impact the performance of electronic circuits. |

| ASPs (Average Selling Prices) | The average price at which MLCCs are sold in the market, expressed in USD million. It reflects the average price per unit |

| Voltage | The electrical potential difference across an MLCC, often categorized into low-range voltage, mid-range voltage, and high-range voltage, indicating different voltage levels |

| MLCC RoHS Compliance | Compliance with the Restriction of Hazardous Substances (RoHS) directive, which restricts the use of certain hazardous substances, such as lead, mercury, cadmium, and others, in the manufacturing of MLCCs, promoting environmental protection and safety |

| Mounting Type | The method used to attach MLCCs to a circuit board, such as surface mount, metal cap, and radial lead, which indicates the different mounting configurations |

| Dielectric Type | The type of dielectric material used in MLCCs, often categorized into Class 1 and Class 2, representing different dielectric characteristics and performance |

| Low-Range Voltage | MLCCs designed for applications that require lower voltage levels, typically in the low voltage range |

| Mid-Range Voltage | MLCCs designed for applications that require moderate voltage levels, typically in the middle range of voltage requirements |

| High-Range Voltage | MLCCs designed for applications that require higher voltage levels, typically in the high voltage range |

| Low-Range Capacitance | MLCCs with lower capacitance values, suitable for applications that require smaller energy storage |

| Mid-Range Capacitance | MLCCs with moderate capacitance values, suitable for applications that require intermediate energy storage |

| High-Range Capacitance | MLCCs with higher capacitance values, suitable for applications that require larger energy storage |

| Surface Mount | MLCCs designed for direct surface mounting onto a printed circuit board (PCB), allowing for efficient space utilization and automated assembly |

| Class 1 Dielectric | MLCCs with Class 1 dielectric material, characterized by a high level of stability, low dissipation factor, and low capacitance change over temperature. They are suitable for applications requiring precise capacitance values and stability |

| Class 2 Dielectric | MLCCs with Class 2 dielectric material, characterized by a high capacitance value, high volumetric efficiency, and moderate stability. They are suitable for applications that require higher capacitance values and are less sensitive to capacitance changes over temperature |

| RF (Radio Frequency) | It refers to the range of electromagnetic frequencies used in wireless communication and other applications, typically from 3 kHz to 300 GHz, enabling the transmission and reception of radio signals for various wireless devices and systems. |

| Metal Cap | A protective metal cover used in certain MLCCs (Multilayer Ceramic Capacitors) to enhance durability and shield against external factors like moisture and mechanical stress |

| Radial Lead | A terminal configuration in specific MLCCs where electrical leads extend radially from the ceramic body, facilitating easy insertion and soldering in through-hole mounting applications. |

| Temperature Stability | The ability of MLCCs to maintain their capacitance values and performance characteristics across a range of temperatures, ensuring reliable operation in varying environmental conditions. |

| Low ESR (Equivalent Series Resistance) | MLCCs with low ESR values have minimal resistance to the flow of AC signals, allowing for efficient energy transfer and reduced power losses in high-frequency applications. |

Need More Details on Market Definition?

Ask a Question

Research Methodology

Mordor Intelligence has followed the following methodology in all our MLCC reports.

- Step 1: Identify Data Points: In this step, we identified key data points crucial for comprehending the MLCC market. This included historical and current production figures, as well as critical device metrics such as attachment rate, sales, production volume, and average selling price. Additionally, we estimated future production volumes and attachment rates for MLCCs in each device category. Lead times were also determined, aiding in forecasting market dynamics by understanding the time required for production and delivery, thereby enhancing the accuracy of our projections.

- Step 2: Identify Key Variables: In this step, we focused on identifying crucial variables essential for constructing a robust forecasting model for the MLCC market. These variables include lead times, trends in raw material prices used in MLCC manufacturing, automotive sales data, consumer electronics sales figures, and electric vehicle (EV) sales statistics. Through an iterative process, we determined the necessary variables for accurate market forecasting and proceeded to develop the forecasting model based on these identified variables.

- Step 3: Build a Market Model: In this step, we utilized production data and key industry trend variables, such as average pricing, attachment rate, and forecasted production data, to construct a comprehensive market estimation model. By integrating these critical variables, we developed a robust framework for accurately forecasting market trends and dynamics, thereby facilitating informed decision-making within the MLCC market landscape.

- Step 4: Validate and Finalize: In this crucial step, all market numbers and variables derived through an internal mathematical model were validated through an extensive network of primary research experts from all the markets studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step 5: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases, and Subscription Platform

Get More Details On Research Methodology

Download PDF