| Study Period | 2019 - 2030 |

| Market Size (2025) | USD 34.80 Billion |

| Market Size (2030) | USD 47.98 Billion |

| CAGR (2025 - 2030) | 6.63 % |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order |

Advanced Packaging Market Analysis

The Advanced Packaging Market size is estimated at USD 34.80 billion in 2025, and is expected to reach USD 47.98 billion by 2030, at a CAGR of 6.63% during the forecast period (2025-2030).

The advanced semiconductor packaging industry is experiencing significant transformation through consolidation and strategic partnerships, as companies seek to remain competitive amid increasing technological complexity. Major advanced packaging companies are pursuing mergers and acquisitions to strengthen their capabilities, with notable examples including ASE Technology's partnership with GlobalFoundries in February 2023 to establish the first at-scale back-end facility in Europe. This consolidation trend is particularly evident as chipmakers grapple with increasing design complexities and the challenges of sustaining Moore's Law, leading to the emergence of new collaborative approaches in advanced packaging solutions.

The industry is witnessing a dramatic shift toward innovative advanced packaging technologies, particularly in response to the growing demand for 5G infrastructure and applications. According to Ericsson's latest forecasts, 5G subscriptions are expected to surge to over 4.5 billion globally by 2028, driving the need for advanced packaging solutions that can support high-frequency applications and improved thermal management. In September 2023, Intel made a significant breakthrough by launching glass substrates for next-generation advanced packaging, offering distinctive properties such as ultra-low flatness and better thermal stability for high-density, high-performance chip packages.

Major investments in advanced packaging capabilities are reshaping the industry landscape, particularly in Asia. In July 2023, Silicon Box announced a USD 2 billion investment in an advanced semiconductor manufacturing foundry in Singapore, while TSMC revealed plans to invest NTD 90 billion in an advanced chip packaging plant in Taiwan. These investments are largely driven by the artificial intelligence boom and the increasing demand for high-performance computing applications, demonstrating the industry's rapid evolution toward more sophisticated advanced packaging solutions.

The industry is seeing a significant shift toward chiplet technology and heterogeneous integration, with companies developing new platforms to address the growing complexity of semiconductor devices. In October 2023, ASE Technology launched its Integrated Design Ecosystem (IDE), enabling seamless transition from single-die SoC to multi-die disaggregated IP blocks. This trend is further supported by Micron's announcement in June 2023 to invest YUAN 4.3 billion in upgrading its chip packaging factory in Xi'an, highlighting the industry's movement toward more advanced packaging solutions for memory and storage applications.

Advanced Packaging Market Trends

Increasing Trend of Advanced Architecture in Electronic Products

The rapid advancement in technology has catalyzed the development of more sophisticated architectures in electronic products, driving significant demand for advanced packaging solutions. These advancements encompass improvements in semiconductor manufacturing processes, component miniaturization, and the development of new materials and technologies. The increasing demand for faster processors, enhanced memory capacity, improved graphics capabilities, and superior connectivity options has created a substantial need for advanced packaging solutions that can support these high-performance requirements.

The rise of applications requiring high computational power, such as artificial intelligence, virtual reality, and data analytics, has further accelerated the need for advanced architectures in electronic products. These applications demand specialized hardware and optimized architectures to deliver the desired performance levels. The growing adoption of cloud computing and the generation of large amounts of data have put additional pressure on electronic products to handle complex computational tasks efficiently. Advanced architectures, such as parallel processing and distributed computing, have become essential for processing and analyzing big data in real-time, driving the need for sophisticated advanced packaging solutions that can support these demanding applications.

Understand The Key Trends Shaping This Market

Download PDF

Favorable Government Policies and Regulations in Developing Countries

Governments worldwide are actively supporting the semiconductor industry through reduced barriers and increased subsidies for production, research, and development. In July 2023, India's government announced a significant initiative offering 50% financial assistance to technology firms establishing semiconductor manufacturing facilities in the country. This support extends to the identification of 300 colleges for starting semiconductor design courses, demonstrating a comprehensive approach to developing the semiconductor ecosystem. Similarly, China's announcement of a new state-backed investment fund worth USD 40 billion in September 2023 showcases the strong government commitment to advancing domestic semiconductor capabilities.

The implementation of supportive policies extends beyond direct financial assistance to include strategic partnerships and infrastructure development. For instance, in October 2023, Mexico and the United States launched a joint "semiconductor action plan" aimed at making North America the world's most powerful chip-producing region. This collaboration, supported by initiatives like the CHIPS and Science Act, demonstrates how government policies are fostering regional cooperation and development in the semiconductor industry. Additionally, Japan's adoption of major new industrial policies, including the formation of the Leading-Edge Semiconductor Technology Center (LSTC) and collaboration with foreign partners, illustrates the comprehensive approach governments are taking to strengthen their domestic semiconductor capabilities.

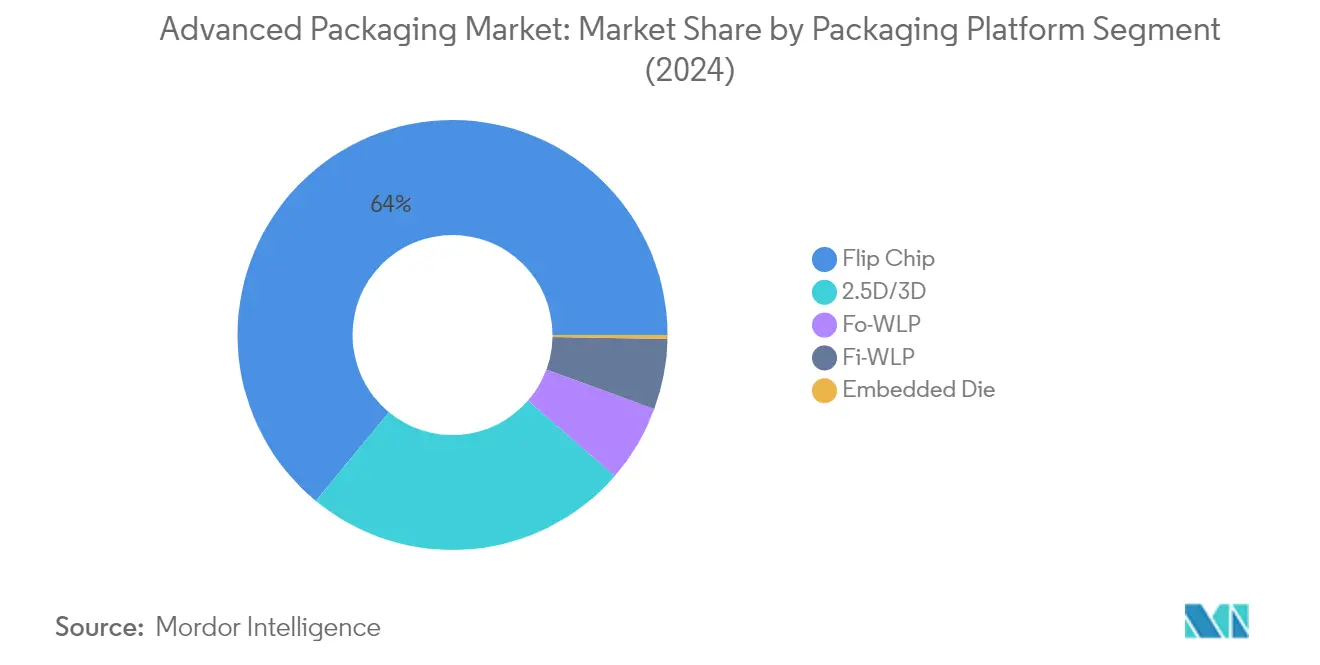

Segment Analysis: Packaging Platform

Flip Chip Segment in Advanced Packaging Market

The Flip Chip segment continues to dominate the advanced packaging market, commanding approximately 64% market share in 2024, driven by its widespread adoption in high-performance computing and mobile applications. This technology's prominence is attributed to its superior electrical performance, reduced signal inductance, and ability to handle higher temperatures compared to traditional chip packaging technologies. The segment's leadership position is reinforced by its effectiveness in applications requiring smaller assembly sizes, making it particularly suitable for smartphones, consumer electronics, and automotive applications. Flip chip packaging enables optimized electrical paths for high-frequency signals, making it ideal for RF, baseband, and in-substrate antenna applications, while its ability to bring power directly into the core of the die rather than requiring rerouting to the edges significantly decreases core power noise and improves silicon performance.

Embedded Die Segment in Advanced Packaging Market

The Embedded Die segment is emerging as the most dynamic segment in the advanced packaging market, projected to grow at approximately 30% annually from 2024 to 2029. This remarkable growth trajectory is primarily driven by the increasing demand for 5G network technology and consumer electronics applications. The technology's ability to provide enhanced chip quality, superior reliability, and better security, while consuming no area on the chip, makes it particularly attractive for emerging applications. The segment's growth is further accelerated by the rising implementation of the Internet of Things (IoT), where miniature electronic circuits with requirements for small size, low power consumption, less heat dissipation, and smaller form factors are essential. The technology's excellent electrical performance at high frequencies and its promise for emerging microwave applications position it as a crucial enabler for next-generation devices. Embedded die packaging is pivotal in meeting these demands, ensuring robust performance and integration.

Remaining Segments in Packaging Platform

The advanced packaging market's ecosystem is further enriched by Fi-WLP, Fo-WLP, and 2.5D/3D segments, each serving distinct market needs. The Fi-WLP technology offers advantages for cost and space-constrained mobile devices and emerging applications in automotive and wearable electronics. The Fo-WLP segment has emerged as a promising technology for meeting consumer electronic products' increasing demands, offering substrate-less packages and lower thermal resistance. The 2.5D/3D segment has gained significant traction in high-performance computing applications, enabling multiple dies to be positioned laterally with signal redistribution interconnect layers, particularly beneficial for advanced memory integration and processor-to-memory bandwidth optimization. This segment also leverages through-silicon via and 3D packaging technologies to enhance performance and efficiency. Additionally, wafer-level packaging and panel-level packaging are becoming increasingly relevant in addressing the industry's evolving needs.

Advanced Packaging Market Geography Segment Analysis

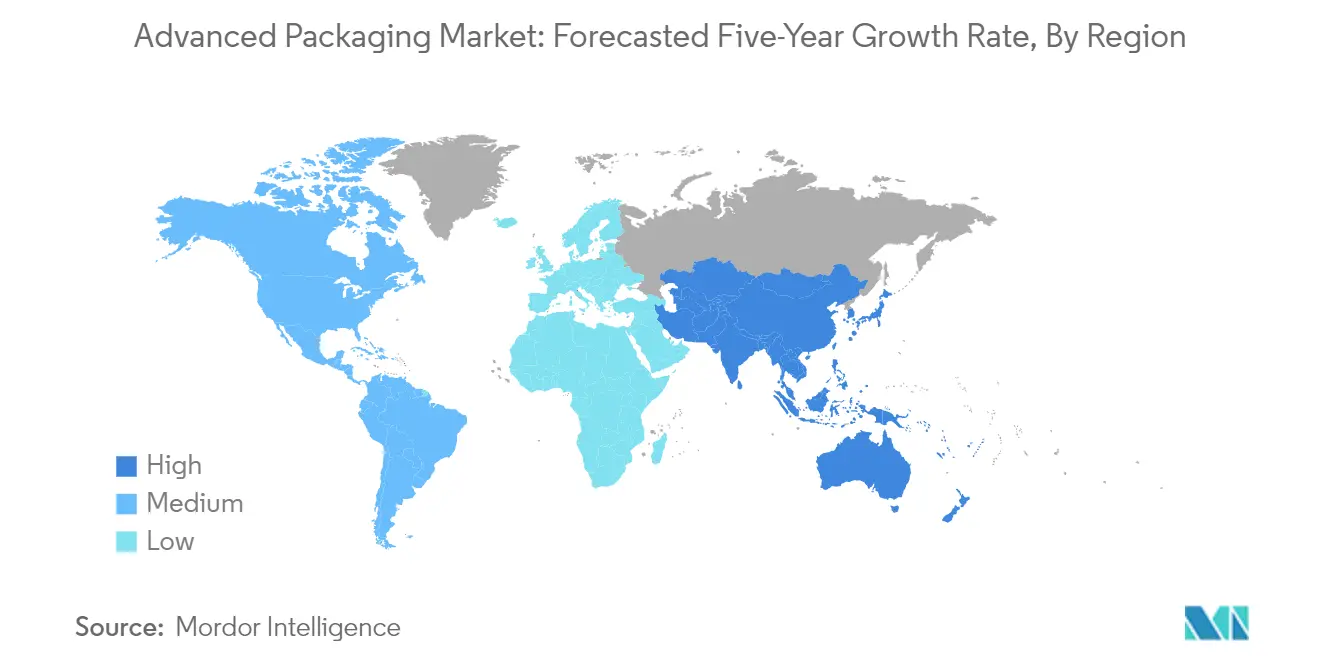

Advanced Packaging Market in North America

The North American advanced packaging market continues to be a significant force in the global landscape, commanding approximately 17% of the global advanced packaging market share in 2024. The region's prominence is largely driven by extensive semiconductor packaging capabilities and the rising demand for miniature consumer electronic devices. The United States, in particular, maintains its dominance within the North American region, supported by aggressive government initiatives to boost domestic chip production. The implementation of the CHIPS and Science Act has become a cornerstone for market growth, with a substantial focus on reinvigorating domestic advanced packaging manufacturing and innovation. The National Institute for Standards and Technology's establishment of the National Advanced Packaging Manufacturing Program (NAPMP) demonstrates the region's commitment to developing robust domestic advanced packaging industries. Private investments exceeding $210 billion across 20 states for domestic manufacturing capacity enhancement further underscore the region's strategic importance. The region's technological leadership in developing packages, especially in new and advanced forms of technology, positions it uniquely in the semiconductor packaging industry. Despite having extensive chip production capabilities, the region's strategic focus on reducing dependence on Asian OSAT firms for packaging services is creating new opportunities for market expansion.

Advanced Packaging Market in Europe

The European advanced packaging market has demonstrated robust growth, registering approximately a 6% growth rate from 2019 to 2024, driven by the region's position as a crucial tech hub and significant adopter of modern technology. The European semiconductor industry has established a strong foothold in applications for the automotive, aerospace industries, and industrial automation, complemented by world-class research facilities like Imec in Leuven, Belgium. The European Chips Act has emerged as a transformative initiative, facilitating substantial public and private investments to strengthen Europe's position in production capacities and expertise. The region's commitment to sustainability has positioned it ahead in terms of long-term growth drivers, although it faces challenges in the major growth area of advanced chips. Major semiconductor manufacturers are increasingly investing in European facilities, particularly in countries like Germany, France, and Italy, indicating a strategic shift towards building robust local semiconductor ecosystems. The region's focus on reducing dependency on foreign companies and preventing supply chain disruptions has led to increased support for investments in the semiconductor sector, creating new opportunities for advanced packaging solutions.

Advanced Packaging Market in Asia Pacific

The Asia Pacific advanced packaging market is poised for exceptional growth, with a projected growth rate of approximately 12% from 2024 to 2029, establishing itself as the dominant force in the semiconductor packaging landscape. The region's supremacy is attributed to the presence of major semiconductor manufacturers, rapid industrialization, and a vast consumer electronics market. The region's strength lies in its high-volume production capabilities and the widespread adoption of advanced packaging technologies across diverse industries, including consumer electronics, automotive, and telecommunications. China's ambitious semiconductor agenda, supported by substantial funding and strategic investments in evolving packaging technologies, positions it as a major competitor in the global market. Taiwan's significant strides in chip packaging and fabless segments, coupled with its advanced foundry services, further strengthen the region's dominance. The integration of industry resources through strategic mergers and acquisitions, continuous R&D investments, and the development of new product applications characterize the region's dynamic market environment. The presence of major players and their focus on innovative packaging solutions continues to drive technological advancement and market growth.

Advanced Packaging Market in Rest of the World

The Rest of the World region in the advanced packaging market represents an emerging frontier with significant untapped potential, particularly in the Middle Eastern and African markets. The GCC countries are emerging as qualified candidates for developing semiconductor industries, supported by their robust investment capabilities and access to key raw materials such as silicon, copper, and aluminum. The region benefits from developed infrastructure in specialized zones like Masdar City, Silicon Oasis in the UAE, and Neom in Saudi Arabia, which provide fertile ground for semiconductor industry development. Middle Eastern economies are actively working to position themselves as major players in the global technology scene, with a particular focus on high-technology manufacturing products. The region's strategic focus on localization compared with other manufacturing sectors, combined with its growth potential and the wide-reaching economic effects of supply disruptions, creates unique opportunities for market development. Africa's progress in technology, particularly in countries like South Africa, Egypt, Algeria, and Morocco with significant silicon resources, presents long-term growth potential despite current underutilization of resources.

Get Analysis on Important Geographic Markets

Download PDF

Advanced Packaging Market Overview

Top Companies in Advanced Packaging Market

The advanced packaging market features prominent players like ASE Technology, TSMC, Intel, Amkor Technology, JCET Group, Samsung Electronics, ChipMOS Technologies, and Universal Instruments Corporation leading innovation and development. Companies are heavily investing in research and development to advance their foundry and semiconductor capabilities, with a particular focus on heterogeneous integration and advanced packaging technology solutions. The industry is witnessing significant product innovations, including glass substrates, fan-out packaging technologies, and 3D integration solutions. Operational strategies emphasize expanding manufacturing capabilities through new facility establishments and capacity expansions, particularly in key regions like Asia Pacific and North America. Strategic partnerships and collaborations are becoming increasingly common, especially in developing next-generation packaging solutions for artificial intelligence, 5G, and automotive applications. Companies are also focusing on sustainability initiatives and quality management systems to maintain competitive advantages.

Market Consolidation Drives Industry Evolution Pattern

The advanced packaging market exhibits a moderately fragmented structure with a mix of global conglomerates and specialized players competing for advanced packaging market share. Major semiconductor manufacturers are increasingly moving towards vertical integration by developing in-house advanced packaging manufacturing capabilities, while pure-play packaging companies are expanding their technological expertise to remain competitive. The industry is witnessing significant consolidation through mergers and acquisitions, particularly as companies seek to acquire specialized technologies and expand their geographical presence. Asian manufacturers, especially from Taiwan, South Korea, and China, dominate the market landscape, supported by strong government initiatives and established semiconductor ecosystems.

The market is characterized by high barriers to entry due to substantial capital requirements, complex manufacturing processes, and the need for specialized expertise. Companies are forming strategic alliances and joint ventures to share resources and technological capabilities, particularly in developing next-generation packaging solutions. The industry's competitive dynamics are further shaped by the increasing focus on advanced semiconductor packaging as a strategic differentiator rather than a commodity service, leading to greater investment in proprietary technologies and solutions.

Innovation and Integration Drive Future Success

Success in the advanced packaging industries increasingly depends on companies' ability to develop innovative solutions while maintaining cost competitiveness. Market leaders are investing heavily in research and development to create proprietary technologies and processes, particularly in areas like heterogeneous integration and chiplet-based solutions. Companies are also focusing on strengthening their relationships with key customers through early engagement in product development cycles and offering comprehensive turnkey solutions. The ability to provide integrated services, from design to final testing, is becoming crucial for maintaining market position.

Future success in the market will require companies to effectively manage supply chain complexities and maintain flexibility in manufacturing capabilities. Players must develop expertise in multiple packaging technologies to serve diverse application needs while maintaining operational efficiency. Regulatory compliance, particularly in areas like environmental sustainability and quality standards, is becoming increasingly important for maintaining market position. Companies must also carefully manage customer concentration risks by diversifying their customer base across different end-user segments and geographical regions, while continuously monitoring and adapting to technological changes in the semiconductor industry.

Advanced Packaging Market Leaders

-

Amkor Technology, Inc.

-

Taiwan Semiconductor Manufacturing Company Limited

-

Advanced Semiconductor Engineering Inc.

-

Intel Corporation

-

JCET Group Co. Ltd

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competiters?

Download PDF

Advanced Packaging Market News

- October 2023 - Advanced Semiconductor Engineering Inc. (ASE) announced the launch of its Integrated Design Ecosystem (IDE), a collaborative design toolset optimized to boost advanced package architecture across its VIPack platform systematically. This innovative approach allows a seamless transition from single-die SoC to multi-die disaggregated IP blocks, including chiplets and memory for integration using 2.5D or advanced fanout structures.

- June 2023- Amkor Technology Inc., a significant provider of semiconductor packaging and test services and the automotive OSAT, is innovating advanced packaging to enable the car of the future. The evolution of the enhanced automotive experience has been dramatic over the past few years, a rise evidenced in car-related semiconductor sales. As a frequent automotive OSAT with more than 40 years of automotive experience and a broad geographic footprint supporting global and enabling regional supply chains, Amkor is well-positioned to capture growth from the acceleration of car semiconductor content.

Advanced Packaging Market Report - Table of Contents

1. INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

-

4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Threat of New Entrants

- 4.3.2 Bargaining Power of Buyers

- 4.3.3 Bargaining Power of Suppliers

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

- 4.4 Assessment of the Impact of COVID-19 and Macro Economic Trends on the Industry

5. MARKET DYNAMICS

-

5.1 Market Drivers

- 5.1.1 Increasing Trend of Advanced Architecture in Electronic Products

- 5.1.2 Favorable Government Policies and Regulations in Developing Countries

-

5.2 Market Restraints

- 5.2.1 Market Consolidation affecting Overall Profitability

6. MARKET SEGMENTATION

-

6.1 By Packaging Platform

- 6.1.1 Flip Chip

- 6.1.2 Embedded Die

- 6.1.3 Fi-WLP

- 6.1.4 Fo-WLP

- 6.1.5 2.5D/3D

-

6.2 By Geography***

- 6.2.1 North America

- 6.2.2 Europe

- 6.2.3 Asia

- 6.2.4 Australia and New Zealand

- 6.2.5 Latin America

- 6.2.6 Middle East and Africa

7. COMPETITIVE LANDSCAPE

-

7.1 Company Profiles

- 7.1.1 Amkor Technology Inc.

- 7.1.2 Taiwan Semiconductor Manufacturing Company Limited

- 7.1.3 Advanced Semiconductor Engineering Inc.

- 7.1.4 Intel Corporation

- 7.1.5 JCET Group Co. Ltd

- 7.1.6 Chipbond Technology Corporation

- 7.1.7 Samsung Electronics Co. Ltd

- 7.1.8 Universal Instruments Corporation

- 7.1.9 ChipMOS Technologies Inc.

- 7.1.10 Brewer Science Inc.

- *List Not Exhaustive

8. INVESTMENT ANALYSIS

9. MARKET OPPORTUNITIES AND FUTURE TRENDS

**Subject to Availability

***In the final report, Asia, Australia, and New Zealand will be studied together as 'Asia Pacific' and Latin America and Middle East and Africa will be considered together as 'Rest of the World'

You Can Purchase Parts Of This Report. Check Out Prices For Specific Sections

Get Price Break-up Now

Advanced Packaging Market Industry Segmentation

Advanced packaging refers to the aggregation and interconnection of components before traditional integrated circuit packaging. It allows multiple devices, such as electrical, mechanical, or semiconductor components, to be merged and packaged as a single electronic device. Unlike traditional integrated circuit packaging, advanced packaging employs processes and techniques at semiconductor fabrication facilities.

The advanced packaging market is segmented by packaging platform and geography. By packaging platform market is segmented into flip chip, embedded die, Fi-WLP, Fo-WLP, and 2.5D/3D. By geography, the market is segmented into North America, Europe, Asia Pacific, Latin America, and the Middle East and Africa.

The report offers market forecasts and size in value (USD) for all the above segments.

| By Packaging Platform | Flip Chip |

| Embedded Die | |

| Fi-WLP | |

| Fo-WLP | |

| 2.5D/3D | |

| By Geography*** | North America |

| Europe | |

| Asia | |

| Australia and New Zealand | |

| Latin America | |

| Middle East and Africa |

Need A Different Region or Segment?

Customize Now

Advanced Packaging Market Research FAQs

How big is the Advanced Packaging Market?

The Advanced Packaging Market size is expected to reach USD 34.80 billion in 2025 and grow at a CAGR of 6.63% to reach USD 47.98 billion by 2030.

What is the current Advanced Packaging Market size?

In 2025, the Advanced Packaging Market size is expected to reach USD 34.80 billion.

Who are the key players in Advanced Packaging Market?

Amkor Technology, Inc., Taiwan Semiconductor Manufacturing Company Limited, Advanced Semiconductor Engineering Inc., Intel Corporation and JCET Group Co. Ltd are the major companies operating in the Advanced Packaging Market.

Which is the fastest growing region in Advanced Packaging Market?

Asia Pacific is estimated to grow at the highest CAGR over the forecast period (2025-2030).

Which region has the biggest share in Advanced Packaging Market?

In 2025, the Asia Pacific accounts for the largest market share in Advanced Packaging Market.

What years does this Advanced Packaging Market cover, and what was the market size in 2024?

In 2024, the Advanced Packaging Market size was estimated at USD 32.49 billion. The report covers the Advanced Packaging Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Advanced Packaging Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Our Best Selling Reports

Advanced Packaging Market Research

Mordor Intelligence provides comprehensive insights into the advanced packaging market through detailed industry analysis, market forecasts, and competitive landscapes. Our research extensively covers various segments including semiconductor packaging, wafer level packaging, through silicon via, and electronic packaging, offering stakeholders a thorough understanding of market dynamics and growth opportunities. The report pdf delivers in-depth analysis of emerging technologies, market drivers, and challenges, helping businesses make informed decisions in the rapidly evolving advanced semiconductor packaging landscape.

Our consulting expertise extends beyond traditional market research to provide tailored solutions for the advanced packaging industry. We assist companies in technology scouting for next-generation packaging solutions, conduct detailed patent analysis for innovation tracking, and offer comprehensive competition assessment focusing on key advanced packaging companies. Our services include strategic analysis of heterogeneous integration trends, R&D support for new packaging technologies, and assessment of emerging opportunities in chiplet packaging and 3D packaging segments. Through data aggregation and advanced analytics, we help clients identify market gaps, evaluate potential partnerships, and develop effective go-to-market strategies in this dynamic industry.