Market Size of Active Protection Systems Industry

| Study Period | 2019 - 2029 |

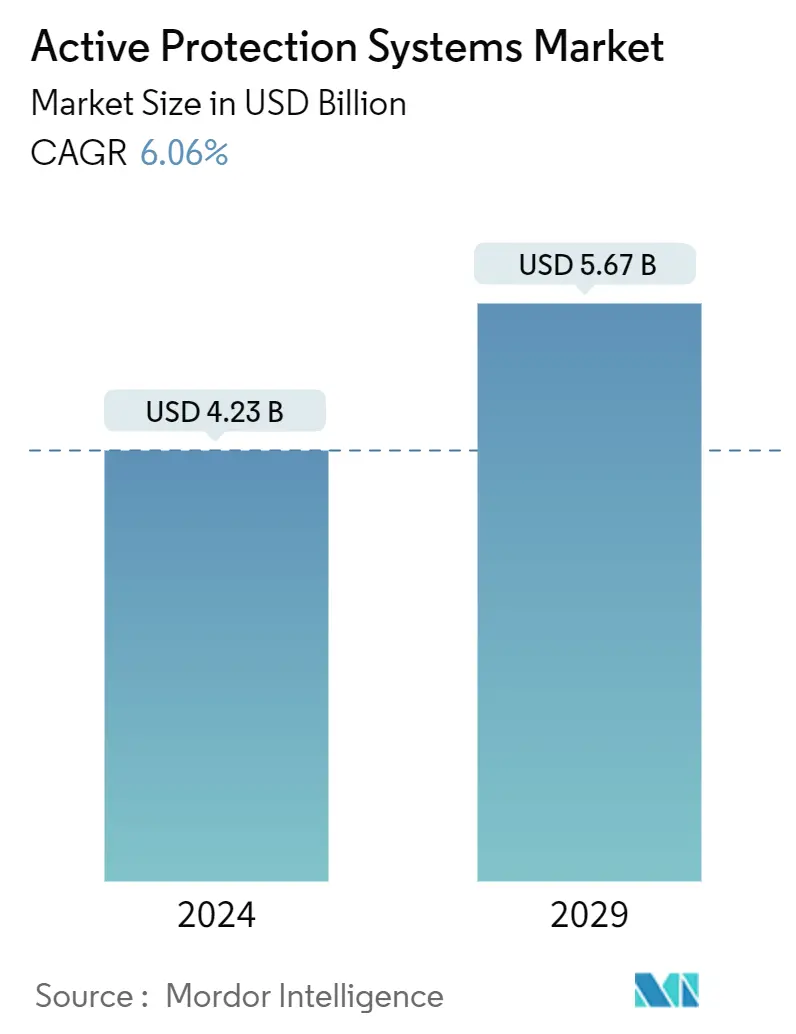

| Market Size (2024) | USD 4.23 Billion |

| Market Size (2029) | USD 5.67 Billion |

| CAGR (2024 - 2029) | 6.06 % |

| Fastest Growing Market | North America |

| Largest Market | North America |

| Market Concentration | High |

Major Players

*Disclaimer: Major Players sorted in no particular order |

Active Protection Systems Market Analysis

The Active Protection Systems Market size is estimated at USD 4.23 billion in 2024, and is expected to reach USD 5.67 billion by 2029, growing at a CAGR of 6.06% during the forecast period (2024-2029).

Growing instances of asymmetric warfare and the emphasis on developing advanced warfare systems are the main drivers of the market. The emphasis on increasing the autonomy of the weapon systems has given rise to unmanned weapon technologies such as RWS and CIWS that can effectively neutralize a target without human intervention. The new variants of APS feature advanced optronic that renders them exceptionally suitable for urban warfare and thus reduce the casualties during a war.

The increasing sophistication of missile systems and other anti-tank threats has heightened the demand for active protection systems. These technologies offer a proactive defense layer, countering emerging threats and significantly increasing the survivability of military platforms. Ongoing advancements in sensor technologies, artificial intelligence, and rapid response mechanisms have propelled the evolution of APS. Enhanced sensors enable quicker threat detection, while AI-driven algorithms optimize response times, making these systems highly effective in dynamic and complex combat scenarios.

During the last decade, many countries have developed and fielded their autonomous weapon systems to bolster their military capabilities and to strengthen their troops in several conflicts around the world. The proliferation of innovations in the field of sensor technologies, weapon firing systems, and other auxiliary systems are aimed at enhancing the accuracy and performance capabilities of the current generation of active protection systems. Technological advancements remain a driving force across all segments of the APS market. Continuous innovation in sensor technologies, artificial intelligence algorithms, and response mechanisms enhances the overall effectiveness of APS solutions.

However, the market is marred by frequent installation and operational challenges associated with autonomous weapon systems, such as the inherent vulnerability to magnetic fields, radio signals, and other electronic attacks. The design and operational issues regarding the use of automated weaponry such as remote weapon stations (RWS) and CIWS may challenge the industry in the short term.

Active Protection Systems Industry Segmentation

An active protection system (APS) is a close-in weapon system (CIWS) that acts as the last line of defense and is deployed to prevent the incoming projectile from having a direct impact on the target. The report includes both hard-kill and soft-kill systems installed onboard military assets, such as main battle tanks (MBTs), and naval assets, such as frigates and destroyers. The hard-kill systems include rocket/missile-based, gun-based, and reactive armour-based weaponry that physically counterattacks an incoming threat thereby destroying/altering its payload/warhead in such a way that the intended effect on the target is severely impeded. The soft kill systems include electronic countermeasures, such as electro-optic jammer, radar decoy, and infrared decoy, that alter the electromagnetic, acoustic, or other signature of the target thereby altering the tracking and sensing behaviour of an incoming threat.

The active protection systems market is segmented by type, platform, and geography. By type, the market is segmented into hard-kill systems and soft-kill systems. By platform, the market is segmented into terrestrial and naval. The report also covers the market sizes and forecasts in 11 countries across major regions. For each segment, the market sizing has been done in terms of value (USD).

| Type | |

| Hard-Kill Systems | |

| Soft-Kill Systems |

| Platform | |

| Terrestrial | |

| Naval |

| Geography | |||||||

| |||||||

| |||||||

| |||||||

| |||||||

|

Active Protection Systems Market Size Summary

The active protection systems (APS) market is experiencing significant growth, driven by the increasing need for advanced defense solutions in asymmetric warfare and the development of unmanned weapon technologies. These systems, which include remote weapon stations (RWS) and close-in weapon systems (CIWS), are designed to neutralize threats without human intervention, making them particularly effective in urban warfare scenarios. The market is characterized by ongoing advancements in sensor technologies, artificial intelligence, and rapid response mechanisms, which enhance the effectiveness of APS in dynamic combat environments. The terrestrial segment holds the largest market share, attributed to the extensive use of APS in ground-based military vehicles like main battle tanks and armored personnel carriers. This segment's growth is further fueled by technological innovations such as modular and scalable APS solutions.

North America leads the APS market, with the United States and Canada investing heavily in upgrading their military capabilities amid heightened geopolitical tensions. The region's dominance is supported by substantial defense budgets and a focus on modernizing defense assets. Key players in the market, including RTX Corporation, Leonardo S.p.A., BAE Systems plc, Rheinmetall AG, and Rafael Advanced Defense Systems Ltd., are actively engaged in research and development to enhance APS technologies. Collaborations and strategic partnerships are common as companies seek to expand their geographical presence and maintain competitive advantage. Despite challenges related to the installation and operation of autonomous systems, the market is poised for continued growth, driven by the demand for enhanced military protection and the ongoing evolution of APS technologies.

Active Protection Systems Market Size - Table of Contents

-

1. MARKET DYNAMICS

-

1.1 Market Overview

-

1.2 Market Drivers

-

1.3 Market Restraints

-

1.4 Porter's Five Forces Analysis

-

1.4.1 Threat of New Entrants

-

1.4.2 Bargaining Power of Buyers/Consumers

-

1.4.3 Bargaining Power of Suppliers

-

1.4.4 Threat of Substitute Products

-

1.4.5 Intensity of Competitive Rivalry

-

-

-

2. MARKET SEGMENTATION

-

2.1 Type

-

2.1.1 Hard-Kill Systems

-

2.1.2 Soft-Kill Systems

-

-

2.2 Platform

-

2.2.1 Terrestrial

-

2.2.2 Naval

-

-

2.3 Geography

-

2.3.1 North America

-

2.3.1.1 United States

-

2.3.1.2 Canada

-

-

2.3.2 Europe

-

2.3.2.1 United Kingdom

-

2.3.2.2 France

-

2.3.2.3 Germany

-

2.3.2.4 Russia

-

2.3.2.5 Rest of Europe

-

-

2.3.3 Asia-Pacific

-

2.3.3.1 China

-

2.3.3.2 India

-

2.3.3.3 Japan

-

2.3.3.4 South Korea

-

2.3.3.5 Rest of Asia-Pacific

-

-

2.3.4 Latin America

-

2.3.4.1 Brazil

-

2.3.4.2 Mexico

-

2.3.4.3 Rest of Latin America

-

-

2.3.5 Middle East and Africa

-

2.3.5.1 United Arab Emirates

-

2.3.5.2 Saudi Arabia

-

2.3.5.3 Israel

-

2.3.5.4 South Africa

-

2.3.5.5 Rest of Middle East and Africa

-

-

-

Active Protection Systems Market Size FAQs

How big is the Active Protection Systems Market?

The Active Protection Systems Market size is expected to reach USD 4.23 billion in 2024 and grow at a CAGR of 6.06% to reach USD 5.67 billion by 2029.

What is the current Active Protection Systems Market size?

In 2024, the Active Protection Systems Market size is expected to reach USD 4.23 billion.