Acetic Acid Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

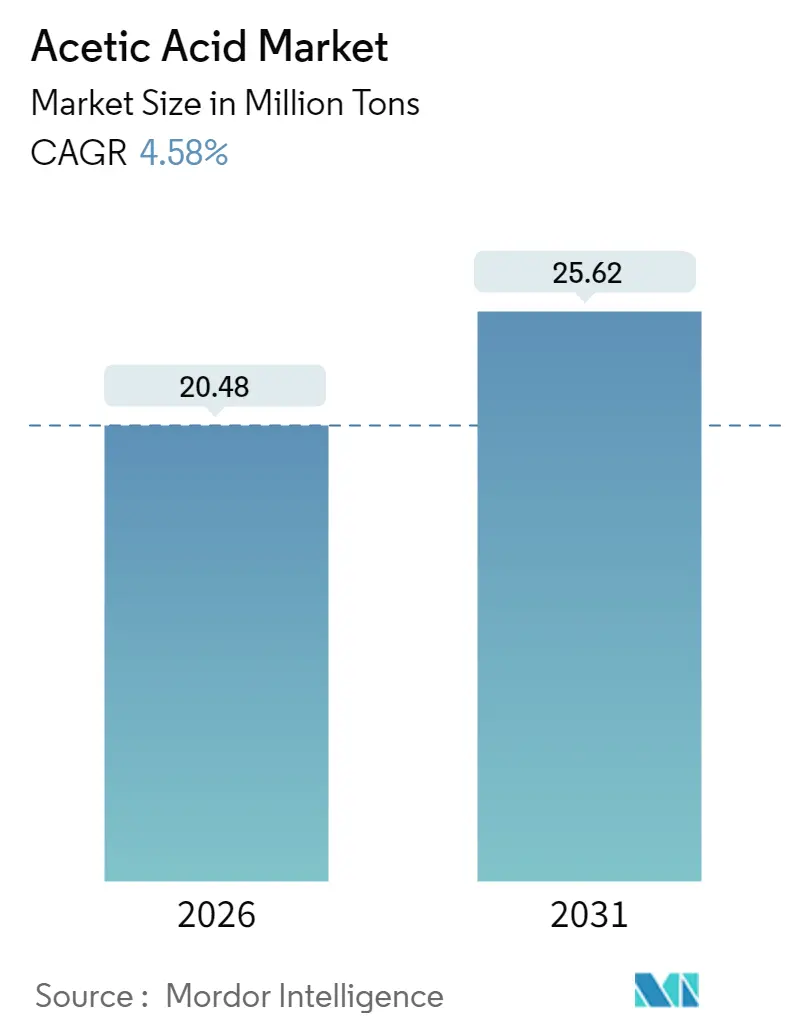

| Market Volume (2026) | 20.48 Million tons |

| Market Volume (2031) | 25.62 Million tons |

| Growth Rate (2026 - 2031) | 4.58% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Acetic Acid Market Analysis by Mordor Intelligence

Acetic Acid market size in 2026 is estimated at 20.48 Million tons, growing from 2025 value of 19.58 Million tons with 2031 projections showing 25.62 Million tons, growing at 4.58% CAGR over 2026-2031. Robust demand across vinyl acetate monomer, purified terephthalic acid, and emerging battery-grade electrolytes anchors growth. Scale-based cost efficiency, rising sustainability mandates, and downstream integration strengthen producer margins. Asia-Pacific dominance persists as polyester, adhesive, and solvent consumption remains high. Investment in low-carbon production technologies and carbon-capture projects is accelerating as regulatory scrutiny tightens, further shaping competitive dynamics in the acetic acid market.

Key Report Takeaways

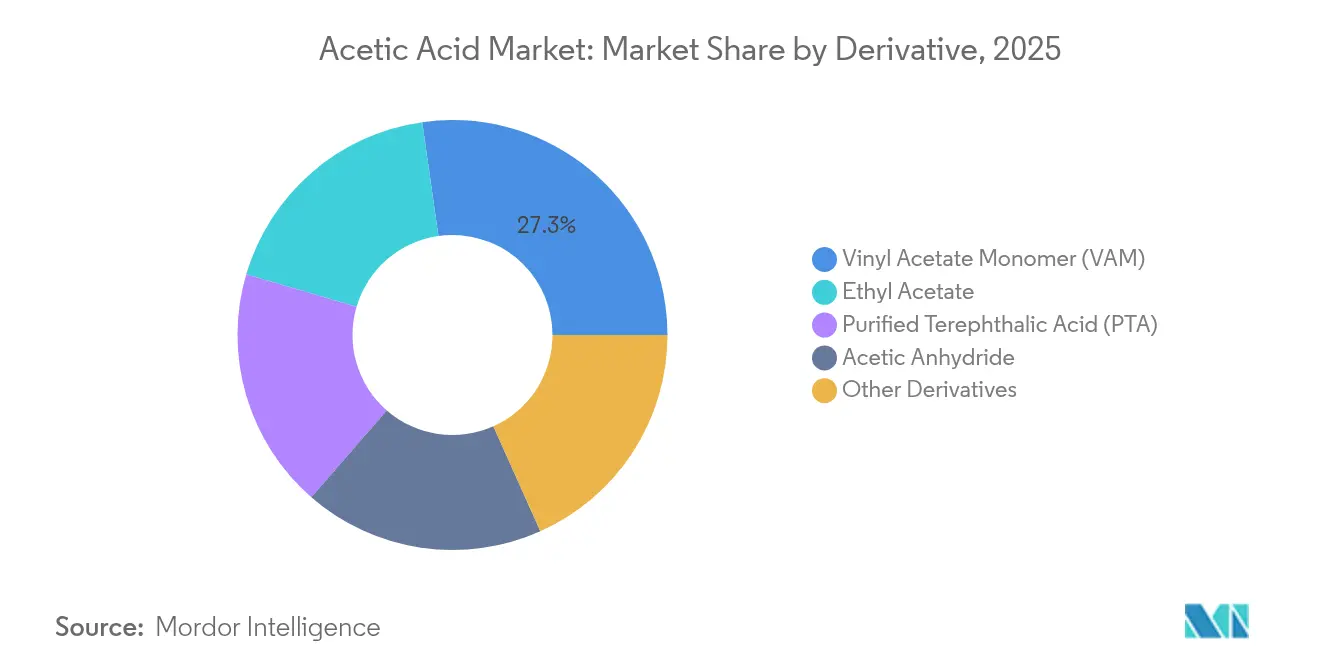

- By derivative, vinyl acetate monomer led with 27.25% of the acetic acid market share in 2025, while purified terephthalic acid recorded the fastest derivative growth at a 4.95% CAGR through 2031.

- By production route, methanol carbonylation held 84.55% of the acetic acid market size in 2025, while bio-based fermentation is projected to expand at 5.65% CAGR.

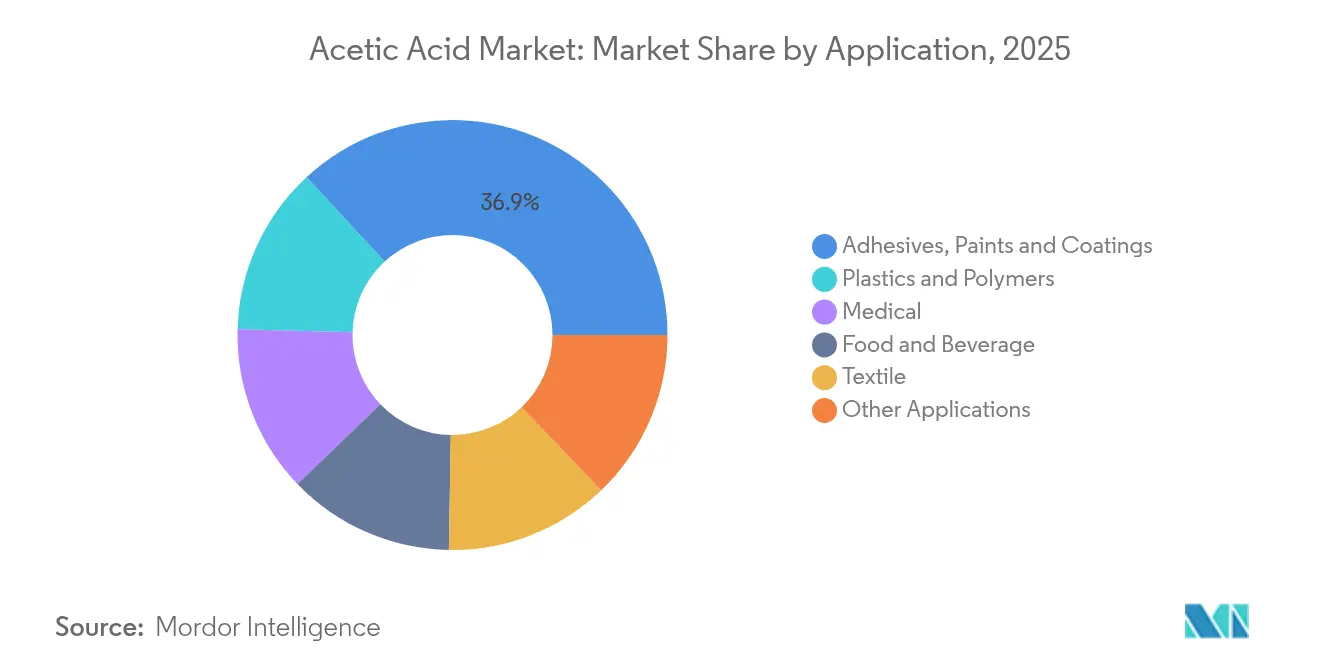

- By application, adhesives, paints, and coatings commanded 36.88% of the acetic acid market size in 2025; the medical segment is advancing at a 6.55% CAGR to 2031.

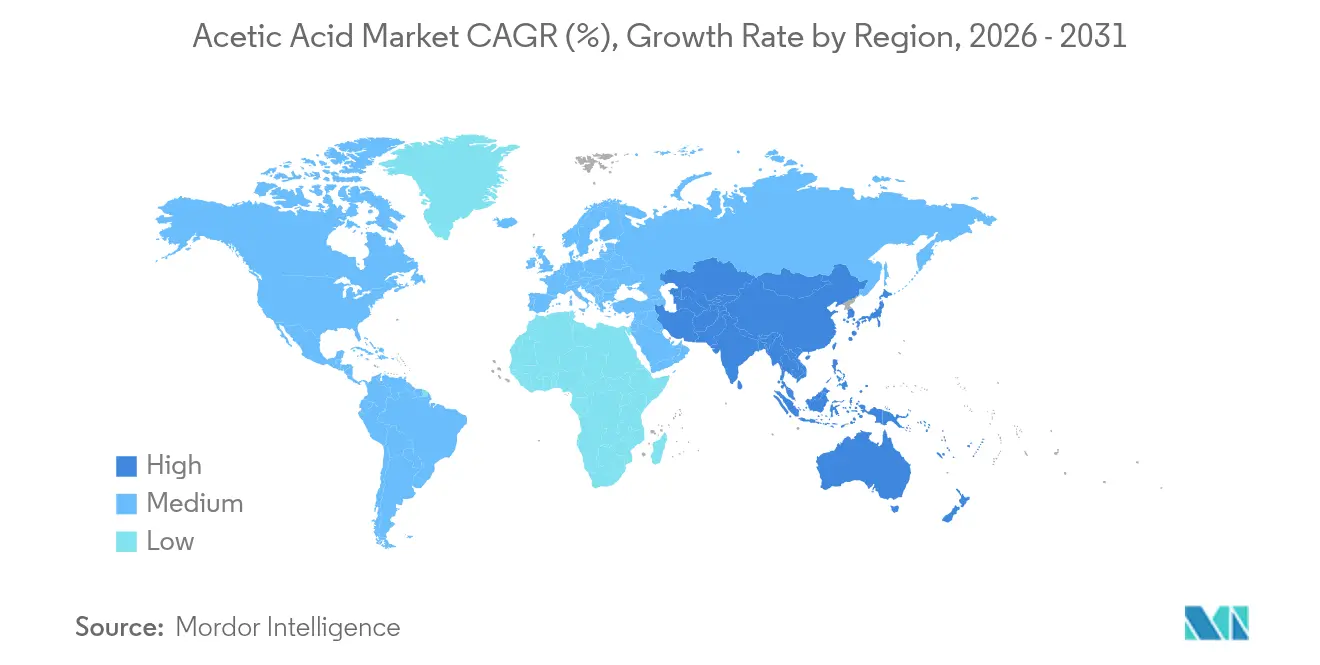

- By geography, Asia-Pacific captured 68.10% of the acetic acid market share in 2025 and is expected to grow at a CAGR of 5.05% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Acetic Acid Market Trends and Insights

Driver Impact Analysis

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing demand for Vinyl Acetate Monomer | +1.2% | Global with Asia-Pacific focus | Medium term (2-4 years) |

| Rising consumption of Purified Terephthalic Acid | +0.9% | Asia-Pacific core, spill-over to MEA | Long term (≥4 years) |

| Expansion of acetate-ester solvents in high-solids coatings | +0.7% | North America and EU | Medium term (2-4 years) |

| Bio-based acetic acid adoption under net-zero mandates | +0.6% | EU and North America, expanding globally | Long term (≥4 years) |

| Emerging use in Li-ion battery electrolyte additives | +0.3% | Asia-Pacific and North America | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Increasing Demand for Vinyl Acetate Monomer

Water-based adhesive and coating formulations rely on vinyl acetate monomer for superior bonding strength and flexibility. These attributes meet stricter environmental rules on solvent emissions, especially in construction and automotive production. Asia-Pacific accounts for more than 60% of global VAM consumption, encouraging integrated acetyl chain investments near demand hubs. Celanese started a new vinyl acetate ethylene unit in Nanjing that adds 70,000 tons of capacity, illustrating the proximity advantage.

Rising Consumption of Purified Terephthalic Acid

Polyester growth in textiles and packaging drives higher purified terephthalic acid volumes, sustaining acetic acid usage as solvent and reaction medium. Sinopec’s single-train PTA plant in Jiangsu, with 3 million tons annual capacity, shows the scale now typical in Asia-Pacific production. Larger units improve acetic acid utilization efficiency yet keep total demand rising. Regional supply imbalances, such as India’s premium PTA pricing, allow flexible suppliers to capture arbitrage gains.

Expansion of Acetate-Ester Solvents in High-Solids Coatings

Tighter volatile organic compound limits in the United States and Europe heighten demand for acetate-ester solvents that balance viscosity control with low emissions. The U.S. Environmental Protection Agency continues to update control guidelines for organic chemical processes, increasing compliance needs among coatings producers[1]U.S. Environmental Protection Agency, “Control of Volatile Organic Compound Emissions from Reactor Processes and Distillation in SOCMI,” epa.gov . Formulators rely on acetate esters to achieve high-solids content without performance loss, reinforcing stable offtake for integrated acetic acid producers.

Emerging Use in Li-Ion Battery Electrolyte Additives

Patent activity for lithium-ion electrolyte systems incorporating acetic acid salts underscores a future specialty application. Mitsubishi Chemical’s filings show how acetate-based salts enhance low-temperature conductivity and safety in advanced cells. Battery-grade demand remains small today yet offers premium pricing opportunities that can offset commodity margin pressures.

Restraint Impact Analysis

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile methanol feedstock pricing | −0.8% | Global, acute where feedstock diversity is limited | Short term (≤2 years) |

| Carbonylation-related CO₂/VOC emission regulations | −0.5% | North America and EU, expanding to Asia-Pacific | Medium term (2-4 years) |

| Anti-dumping actions against Chinese exports | −0.3% | Global trade flows with China-centric impact | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Carbonylation-Related CO₂/VOC Emission Regulations

North American and European regulators now target emissions from carbonylation reactors and distillation steps. The EPA’s control guidelines and Canada’s Environmental Protection Act both tighten emission thresholds[2]Environment Canada, “Environmental Emergencies,” ec.gc.ca. Compliance requires investments in carbon capture and advanced scrubbers, favoring larger producers with available capital. Celanese’s Clear Lake retrofit captures CO₂ for methanol synthesis, setting a benchmark for integrated abatement.

Anti-Dumping Actions Against Chinese Exports

Several economies continue to review duties on Chinese acetic acid shipments to curb price undercutting. Such actions create trade flow re-routing and inventory overhang in Asia-Pacific. Producers with diversified geographic footprints mitigate exposure, while single-asset exporters face restricted access to key markets.

Segment Analysis

By Derivative – VAM Leadership Shapes Polymer Demand

Vinyl acetate monomer held 27.25% acetic acid market share in 2025 as construction and automotive sectors favored water-based adhesives. Polyvinyl acetate and ethylene-vinyl acetate copolymers secure growth by replacing solvent-borne systems that fail new emission norms. Celanese and INEOS leverage backward integration to keep costs low and service captive downstream units.

Purified terephthalic acid, growing at a 4.95% CAGR, benefits from polyester expansion in apparel and bottle resin. Ethyl acetate maintains steady use in pharmaceutical and coating solvents, while acetic anhydride demonstrates resilience in pharmaceutical acetylation despite cigarette filter decline. Derivative demand patterns reflect producer strategies that capture value along the acetyl chain. Integrated operators convert commodity acetic acid volumes into higher-margin downstream products, protecting earnings during feedstock price swings.

Note: Segment shares of all individual segments available upon report purchase

By Production Route – Carbonylation Dominance Meets Rising Bio-Options

Methanol carbonylation delivered 84.55% of global acetic acid market size in 2025 due to high reaction yields and established infrastructure. The iridium-catalyzed Cativa process achieves over 99% selectivity, reinforcing low-cost positions. Bio-based fermentation, while only a niche today, is projected to grow 5.65% CAGR as renewable feedstocks gain policy support. Acetaldehyde and ethylene oxidation routes retain importance where regional feedstock advantages exist, yet lack scale against carbonylation.

Technological evolution centers on lowering carbon intensity. Producers are piloting e-methanol pathways that combine captured CO2 with green hydrogen, delivering carbon-negative acetic acid when coupled with carbonylation. Small-to-medium biorefineries in Europe and India demonstrate commercial bio-routes using waste biomass and molasses. Capital access and feedstock logistics remain hurdles before these routes exceed pilot scale.

By Application – Adhesives Lead While Medical Grades Accelerate

Adhesives, paints, and coatings captured 36.88% of the acetic acid market size in 2025 as lightweighting trends in vehicles and eco-friendly building codes stimulated demand for water-based systems. Regulatory agencies endorse formulations with lower volatile organic compound emissions, a shift that drives acetate-derivative uptake. Plastics and polymers show steady expansion through vinyl acetate polymerization, supporting packaging innovations.

Medical applications, advancing at a 6.55% CAGR, illustrate acetic acid’s value in pharmaceutical synthesis and antimicrobial formulations. Aspirin, acetaminophen, and topical antiseptics rely on high-purity grades, commanding premium pricing. Textile applications benefit from acetate fiber production and dyeing auxiliaries. Emerging battery-grade electrolytes offer future specialty demand that could provide producers with attractive margins beyond conventional end-uses.

Note: Segment shares of all individual segments available upon report purchase

Geography Analysis

Asia-Pacific dominated with 68.10% acetic acid market share in 2025 and is forecast to grow at 5.05% CAGR through 2031. China alone controls about 55% of global capacity, granting scale economies and regional pricing influence. The region’s large polyester and adhesive industries stabilize volume demand even during external economic swings.

North America exhibits mature consumption yet notable investment in low-carbon production. Celanese’s 1.3 million ton Clear Lake upgrade integrates carbon capture and feedstock security to ensure competitiveness. Regulatory focus on emission reduction promotes bio-based projects across the United States and Canada, potentially shifting a portion of import volumes to domestic supply.

Europe prioritizes circular economy principles and stringent lifecycle assessments. Producers with verified low-carbon footprints gain procurement preference among automotive and packaging customers. Emerging Middle East and Africa capacity aims to leverage competitive feedstock costs, yet infrastructure and regulatory frameworks remain in development. Latin America experiences steady acetic acid market growth tied to polyester bottle resin and food preservative applications, but scale is limited compared with Asia-Pacific production.

Competitive Landscape

The acetic acid market shows moderate fragmentation. Celanese, INEOS, and LyondellBasell employ vertically integrated strategies that include methanol, acetic acid, and downstream derivatives, safeguarding margins across the value chain. Technology advantages center on emission control, catalyst efficiency, and energy integration. Smaller bio-route innovators compete through sustainability branding, though scale economics remain challenging. Anti-dumping measures and regional trade policies influence strategic site selection and export flows, reinforcing the need for diversified plant networks.

Acetic Acid Industry Leaders

Celanese Corporation

INEOS

Eastman Chemical Company

Jiangsu SOPO (Group) Co., Ltd.

LyondellBasell Industries Holdings B.V.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2024: Celanese Corporation completed its 1.3 million ton acetic acid expansion at Clear Lake, Texas, integrating carbon capture and securing long-term carbon monoxide supply.

- May 2023: Sekab expanded production of 100% bio-based acetic acid, enabling downstream users to cut carbon dioxide emissions by 50%.

Global Acetic Acid Market Report Scope

Acetic acid is a monocarboxylic acid containing two carbons. It is a clear, colorless liquid with a strong, pungent odor, like vinegar. Acetic acid can be derived from the carbonylation of methanol, the oxidation of acetaldehyde and ethylene, or a biological method like bacterial fermentation. It is used as a chemical reagent to produce several chemical compounds like acetic anhydride, ester, vinyl acetate monomer, vinegar, and many other polymeric materials. The acetic acid market is segmented by derivative, application, and geography. By derivative, the market is segmented into vinyl acetate monomer (VAM), purified terephthalic acid (PTA), ethyl acetate, acetic anhydride, and other derivatives. By application, the market is segmented into plastics and polymers, food and beverage, adhesives, paints and coatings, textiles, medical, and other applications. By geography, the market is segmented into Asia-Pacific, North America, Europe, South America, and the Middle East and Africa. The report also covers the market size and forecasts for the acetic acid market in 15 countries across major regions. For each segment, the market sizing and forecasts have been done in terms of volume in kilotons.

| Vinyl Acetate Monomer (VAM) |

| Purified Terephthalic Acid (PTA) |

| Ethyl Acetate |

| Acetic Anhydride |

| Other Derivatives |

| Methanol Carbonylation |

| Acetaldehyde Oxidation |

| Ethylene Oxidation |

| Bio-based Fermentation |

| Plastics and Polymers |

| Food and Beverage |

| Adhesives, Paints and Coatings |

| Textile |

| Medical |

| Other Applications |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Derivative | Vinyl Acetate Monomer (VAM) | |

| Purified Terephthalic Acid (PTA) | ||

| Ethyl Acetate | ||

| Acetic Anhydride | ||

| Other Derivatives | ||

| By Production Route | Methanol Carbonylation | |

| Acetaldehyde Oxidation | ||

| Ethylene Oxidation | ||

| Bio-based Fermentation | ||

| By Application | Plastics and Polymers | |

| Food and Beverage | ||

| Adhesives, Paints and Coatings | ||

| Textile | ||

| Medical | ||

| Other Applications | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the current size of the acetic acid market?

The acetic acid market size is 20.48 million tons in 2026.

Which derivative segment holds the largest share of acetic acid demand?

Vinyl acetate monomer leads with 27.25% market share in 2025.

How fast is bio-based acetic acid production growing?

Bio-based fermentation routes are projected to expand at a 5.65% CAGR through 2031.

Which region dominates acetic acid production capacity?

Asia-Pacific accounts for 68.10% of global capacity, with China controlling roughly 55%.

What is the biggest restraint on acetic acid market growth?

Volatile methanol feedstock pricing reduces the CAGR outlook by 0.8% in the near term.