Market Size of 5G Devices Industry

| Study Period | 2019 - 2029 |

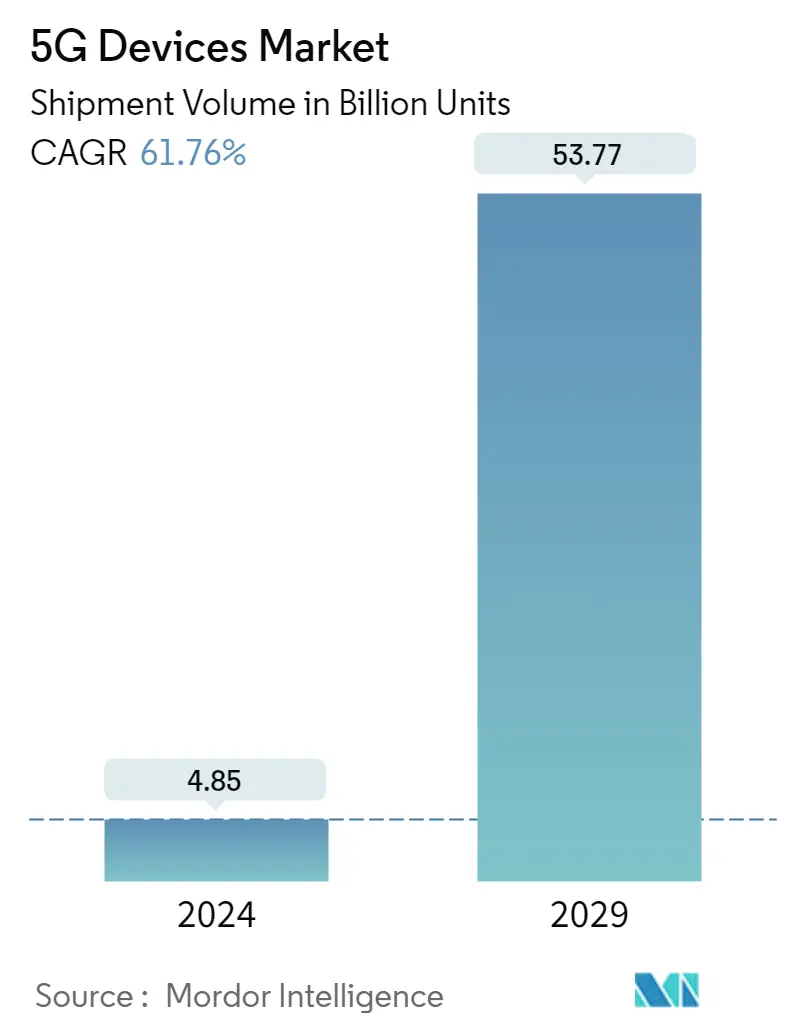

| Market Volume (2024) | 4.85 Billion units |

| Market Volume (2029) | 53.77 Billion units |

| CAGR (2024 - 2029) | 61.76 % |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

Major Players

*Disclaimer: Major Players sorted in no particular order |

5G Devices Market Analysis

The 5G Devices Market size in terms of shipment volume is expected to grow from 4.85 Billion units in 2024 to 53.77 Billion units by 2029, at a CAGR of 61.76% during the forecast period (2024-2029).

5G technology will offer ultra-high-speed network coverage and enable numerous new applications with the help of IoT. Also, the COVID-19 pandemic has delayed the widespread deployment of 5G.

- According to the last year's Ericsson ConsumerLab report, Online interviews were conducted with 49,100 customers in 37 markets between April and July last year. The respondents chosen for the interview represent the surveyed markets' online population of 1.7 billion customers and 430 million 5G users, who range in age from 15 to 69. According to studies, the next wave of 5G is already in motion, with mainstream customers starting to accept the technology in early adopter markets.

- The growing adoption of connectivity, digital applications, and wearable technology is expected to drive growth for players in the 5G devices market. Moreover, upgrading existing supporting infrastructure, including modems, towers, and other supporting infrastructure, will present significant opportunities for new players. The 5G devices market's growth is expected to drive significant opportunities as the adoption of 5G technology has received positive signals in several local markets worldwide.

- Major chip makers also focus on 5G device component development to boost device penetration in the market. This includes chipset vendors competing in volume-driven markets as they introduce more models for mass deployments. In May last year, MediaTek launched Dimensity 1050 mmWave SoC, and related models, to highlight 5G connectivity in devices.

- Also, emerging applications, business models, and falling device costs have driven IoT adoption, increasing the number of connected devices and endpoints globally. 5G offers massive machine-type communication (mMTC), poised to support tens of billions of network-enabled devices to be wirelessly connected. Modern communication systems already serve several MTC applications. However, the characteristic properties of mMTC, i.e., the massive number of devices and the tiny payload sizes, require novel concepts and approaches. 5G allows a density of approximately one million devices per square kilometer.

- However, the global operation and installation of the supportive infrastructure continue to be a significant hurdle in many areas. For instance, in September last year, the international standardization body, 3GPP, updated the next release of the 5G specification, Release 17, for the second half of the previous year. The release was frozen in March last year due to the pandemic and other reasons. Such delays create subsequent delays in companies' supply chains and other operational activities.

- The COVID-19 pandemic's immediate effects have been felt in every industry, causing widespread layoffs, record unemployment, and severely curtailing consumer spending. The spread of COVID-19 resulted in a significant supply chain disruption impeding the 5G buildout process in the short & medium term. The critical 5G hardware delays and general effects of the economic slowdown thus apply.

5G Devices Industry Segmentation

The fifth generation of mobile network equipment is referred to as 5G. To connect practically everyone and everything, including machines, objects, and gadgets, 5G enables a new type of network.

5G Devices Market is Segmented by Form Factor (Modules, CPE (Indoor/Outdoor), Smartphones, Hotspots, Laptops, Industrial Grade CPE/Router/Gateway), Spectrum Support (Sub-6 GHz, mmWave, Both Spectrum Bands), and Geography (North America (United States, Canada), Europe (Germany, UK, France, Spain, and Rest of Europe), Asia Pacific (China, Japan, India, Australia, and Rest of Asia-Pacific), and Latin America (Brazil, Mexico, Argentina, and Rest of Latin America), and Middle East & Africa (UAE, Saudi Arabia, South Africa, and Rest of MEA).

The market sizes and forecasts are provided in terms of value (USD million) for all the above segments.

| Form Factor | |

| Modules | |

| CPE (Indoor/Outdoor) | |

| Smartphone | |

| Hotspots | |

| Laptops | |

| Industrial Grade CPE/Router/Gateway | |

| Other Form Factors |

| Spectrum Support | |

| Sub-6 GHz | |

| mmWave | |

| Both Spectrum Bands |

| Geography | |||||||

| |||||||

| |||||||

| |||||||

| |||||||

|

5G Devices Market Size Summary

The 5G devices market is poised for significant expansion, driven by the technology's ability to provide ultra-high-speed network coverage and support a myriad of new applications through IoT integration. The market is experiencing a surge in adoption as mainstream consumers begin to embrace 5G technology, particularly in early adopter regions. This growth is further fueled by the increasing demand for connectivity, digital applications, and wearable technology. The market landscape is characterized by intense competition among major chip manufacturers and device vendors, who are actively developing components and models to enhance device penetration and facilitate mass deployments. Despite the challenges posed by the COVID-19 pandemic, which delayed infrastructure deployment and caused supply chain disruptions, the market is expected to recover and thrive, offering substantial opportunities for new entrants and existing players alike.

The proliferation of 5G devices is set to transform various sectors by enabling massive machine-type communication, supporting billions of network-enabled devices. The market is witnessing a wave of technological advancements, with smartphone manufacturers launching 5G-enabled devices to meet the rising demand for high-speed data connectivity. Strategic partnerships and investments in research and development are key strategies employed by market players to maintain a competitive edge. The introduction of 5G services, particularly in regions like North America, is bolstered by infrastructural support and regional launches, enhancing the adoption of 5G technology. As the market continues to evolve, the focus remains on providing consumers with high-end 5G experiences, driving the transition from non-5G to 5G smartphones and expanding the global 5G device ecosystem.

5G Devices Market Size - Table of Contents

-

1. MARKET INSIGHTS

-

1.1 Market Overview

-

1.2 Industry Stakeholder Analysis

-

1.3 Industry Attractiveness - Porter's Five Forces Analysis

-

1.3.1 Bargaining Power of Suppliers

-

1.3.2 Bargaining Power of Consumers

-

1.3.3 Threat of New Entrants

-

1.3.4 Threat of Substitute Products

-

1.3.5 Intensity of Competitive Rivalry

-

-

1.4 Impact of COVID-19 on the 5G Landscape

-

-

2. MARKET SEGMENTATION

-

2.1 Form Factor

-

2.1.1 Modules

-

2.1.2 CPE (Indoor/Outdoor)

-

2.1.3 Smartphone

-

2.1.4 Hotspots

-

2.1.5 Laptops

-

2.1.6 Industrial Grade CPE/Router/Gateway

-

2.1.7 Other Form Factors

-

-

2.2 Spectrum Support

-

2.2.1 Sub-6 GHz

-

2.2.2 mmWave

-

2.2.3 Both Spectrum Bands

-

-

2.3 Geography

-

2.3.1 North America

-

2.3.1.1 United States

-

2.3.1.2 Canada

-

-

2.3.2 Europe

-

2.3.2.1 Germany

-

2.3.2.2 UK

-

2.3.2.3 France

-

2.3.2.4 Spain

-

2.3.2.5 Rest of Europe

-

-

2.3.3 Asia-Pacific

-

2.3.3.1 China

-

2.3.3.2 Japan

-

2.3.3.3 India

-

2.3.3.4 Australia

-

2.3.3.5 Rest of Asia-Pacific

-

-

2.3.4 Latin America

-

2.3.4.1 Brazil

-

2.3.4.2 Mexico

-

2.3.4.3 Argentina

-

2.3.4.4 Rest of Latin America

-

-

2.3.5 Middle East and Africa

-

2.3.5.1 UAE

-

2.3.5.2 Saudi Arabia

-

2.3.5.3 South Africa

-

2.3.5.4 Rest of Middle East and Africa

-

-

-

5G Devices Market Size FAQs

How big is the 5G Devices Market?

The 5G Devices Market size is expected to reach 4.85 billion units in 2024 and grow at a CAGR of 61.76% to reach 53.77 billion units by 2029.

What is the current 5G Devices Market size?

In 2024, the 5G Devices Market size is expected to reach 4.85 billion units.