| Study Period | 2019 - 2030 |

| Market Size (2025) | USD 3.41 Billion |

| Market Size (2030) | USD 8.00 Billion |

| CAGR (2025 - 2030) | 18.57 % |

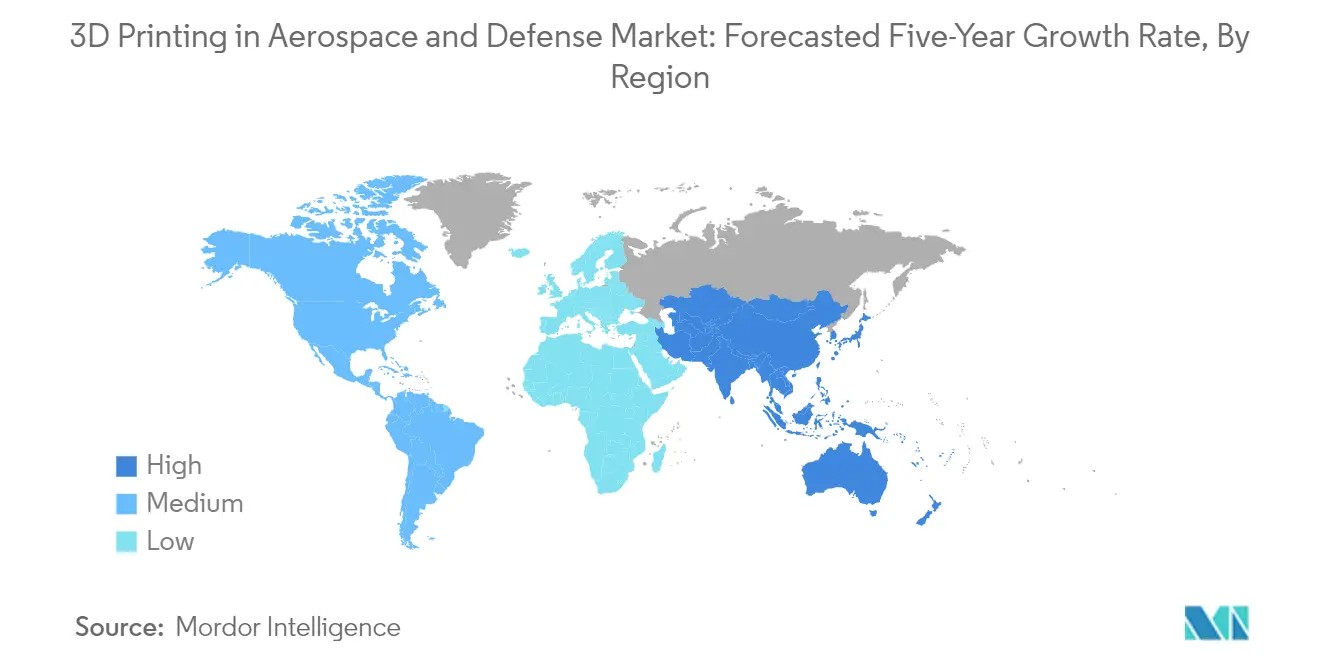

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Europe |

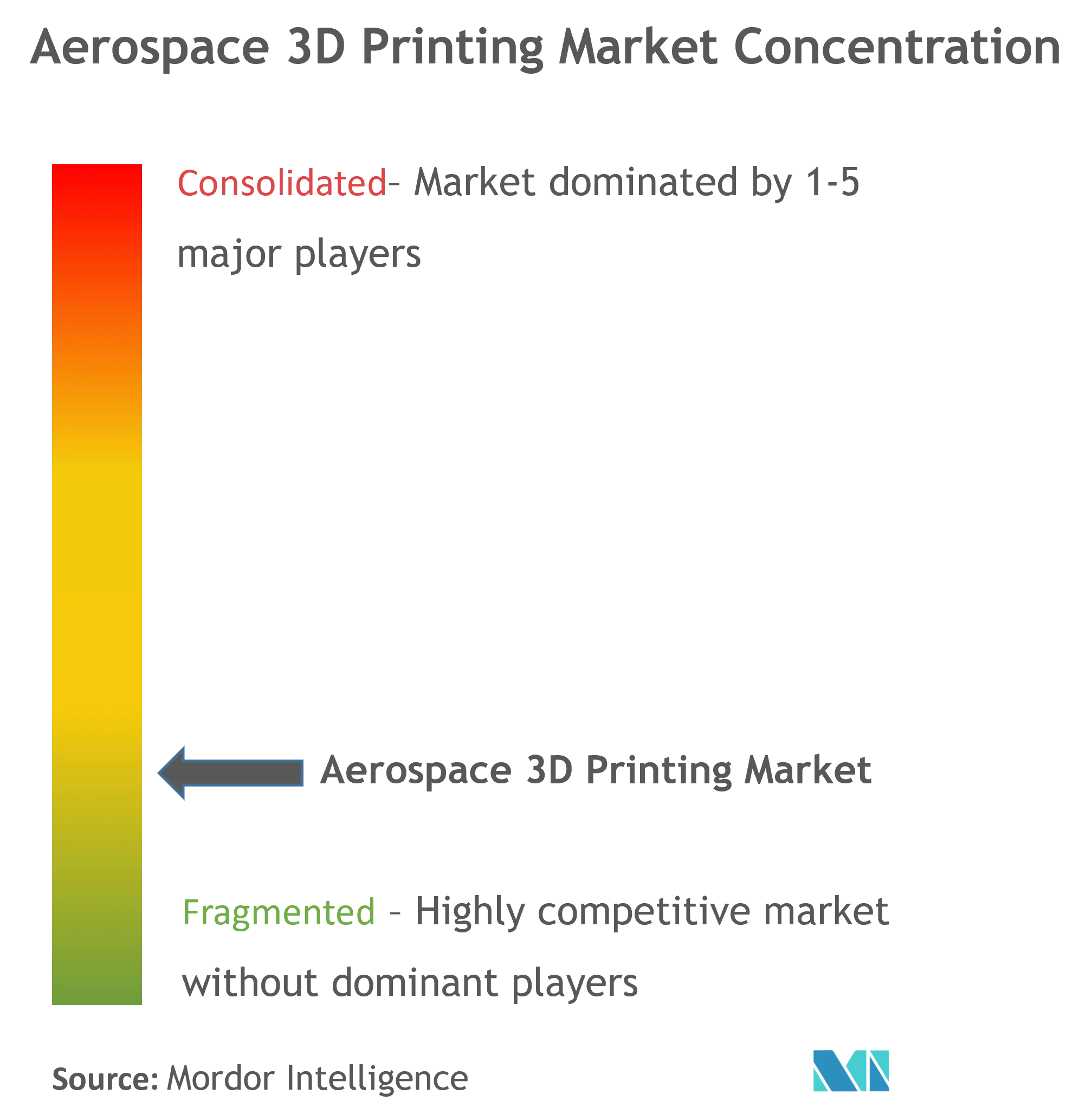

| Market Concentration | Low |

Major Players*Disclaimer: Major Players sorted in no particular order |

Aerospace 3D Printing Market Analysis

The 3D Printing In Aerospace And Defense Market size is estimated at USD 3.41 billion in 2025, and is expected to reach USD 8.00 billion by 2030, at a CAGR of 18.57% during the forecast period (2025-2030).

The aerospace manufacturing industry is experiencing a fundamental transformation as manufacturers increasingly integrate advanced manufacturing technologies with cloud management services. This integration enables remote manufacturing capabilities, real-time monitoring, and on-the-go component optimization, revolutionizing traditional production methods. The technology's maturation is evidenced by major industry players like GE Aviation, which currently employs approximately 48,000 people globally in its additive manufacturing and aerospace operations. The convergence of digital technologies with aerospace additive manufacturing is creating new possibilities for design innovation and production efficiency, particularly in complex aerospace components.

The industry is witnessing a significant shift in material science and manufacturing capabilities, with a growing emphasis on developing specialized materials for critical aerospace applications. Companies are investing heavily in research and development to enhance their technological capabilities, as demonstrated by Raytheon Technologies' substantial investment of USD 7.2 billion in R&D during 2022. This focus on innovation has led to breakthroughs in materials processing, enabling the production of components that can withstand extreme conditions while maintaining optimal performance characteristics.

The adoption of aerospace 3D printing technology is expanding across various aerospace applications, from commercial aircraft components to space exploration vehicles. This expansion is supported by robust order backlogs in the commercial aviation sector, with Boeing maintaining a significant backlog of 4,312 B737 aircraft as of December 2022. The technology is being increasingly utilized for manufacturing critical components, including engine parts, structural elements, and interior components, demonstrating its versatility and reliability in aerospace applications.

The aerospace manufacturing sector is experiencing a transformation in supply chain dynamics and aftermarket opportunities through additive manufacturing. Major aviation hubs are making substantial investments in this technology, as exemplified by Saudi Arabia's planned investment of USD 100 billion in aviation by 2030, which includes significant allocations for advanced manufacturing technologies. This shift is enabling manufacturers to reduce inventory costs, minimize storage requirements, and produce parts on-demand, leading to more efficient and responsive supply chain operations. The technology is particularly valuable in the aftermarket segment, where it enables rapid production of replacement parts and reduces maintenance downtimes.

Aerospace 3D Printing Market Trends

Rapid Rise in Demand for Lightweight and Cost-effective Parts and Components

The aerospace and defense industry is experiencing an unprecedented surge in demand for lightweight components, driven by the need to enhance energy efficiency and reduce fuel consumption through mass reduction of aircraft and defense platforms. Lightweight design has become an extensively explored and utilized criterion, particularly associated with green aviation concepts, as lower mass requires less lift force and thrust during flight. The principle focuses on using less material with lower density while ensuring enhanced technical performance, which can be achieved through advanced lightweight materials applied to numerically optimized structures manufactured using appropriate aerospace additive manufacturing methods.

Recent developments showcase the significant impact of 3D printing on production efficiency and cost reduction. For instance, in October 2023, Boeing and ASTRO America demonstrated a breakthrough in manufacturing efficiency by reducing the production time of the AH-64 Apache attack helicopter's main rotor system from one year to just eight hours using the world's largest 3D metal printer. This advancement highlights the role of military 3D printing in revolutionizing production timelines. Similarly, the B777X aircraft represents a milestone in additive manufacturing integration, with its GE9X engines incorporating 300 3D-printed parts, including fuel nozzles, temperature sensors, heat exchangers, and low-pressure turbine blades. These implementations have demonstrated that 3D printing can cut the weight of commercial aircraft by approximately 7%, while reducing the energy required for production by one-third to one-half compared to conventional manufacturing methods.

Understand The Key Trends Shaping This Market

Download PDF

Rising Government Initiatives Towards Incentivizing 3D Printing for A&D Sector

Governments worldwide are implementing comprehensive policies and significant investments to accelerate the adoption of 3D printing technologies in the aerospace and defense sector. In February 2022, the Government of India unveiled its new 3D printing policy, embodying the tenets of 'Make in India' and 'Atmanirbhar Bharat Abhiyaan,' which promote self-reliance through technological innovation. Similarly, France launched its National Plan for 3D printing in October 2021, supporting the economic development of the industry with an investment of USD 60 million towards research and development in additive manufacturing, particularly focusing on composites and metal deposits, which have shown the strongest demand in aerospace applications.

The United States has demonstrated substantial commitment through various initiatives, including the establishment of the National Additive Manufacturing Innovation Institute (NAMII) with an investment of USD 30 million, aimed at boosting 3D printing's use in manufacturing through collaboration with industries and government agencies. Additionally, in July 2021, the US Department of Defense (DoD) announced its comprehensive additive manufacturing policy, focusing on harnessing the technology's potential through strategies, policies, and inter-departmental collaboration. The policy aims to transform maintenance operations, increase logistics resiliency, and improve self-sustainment and readiness for military services, with particular emphasis on solving frontline and logistical challenges through accelerated adoption of military additive manufacturing technologies. These initiatives underscore the growing importance of the military 3D printing industry in enhancing defense capabilities.

Segment Analysis: By Application

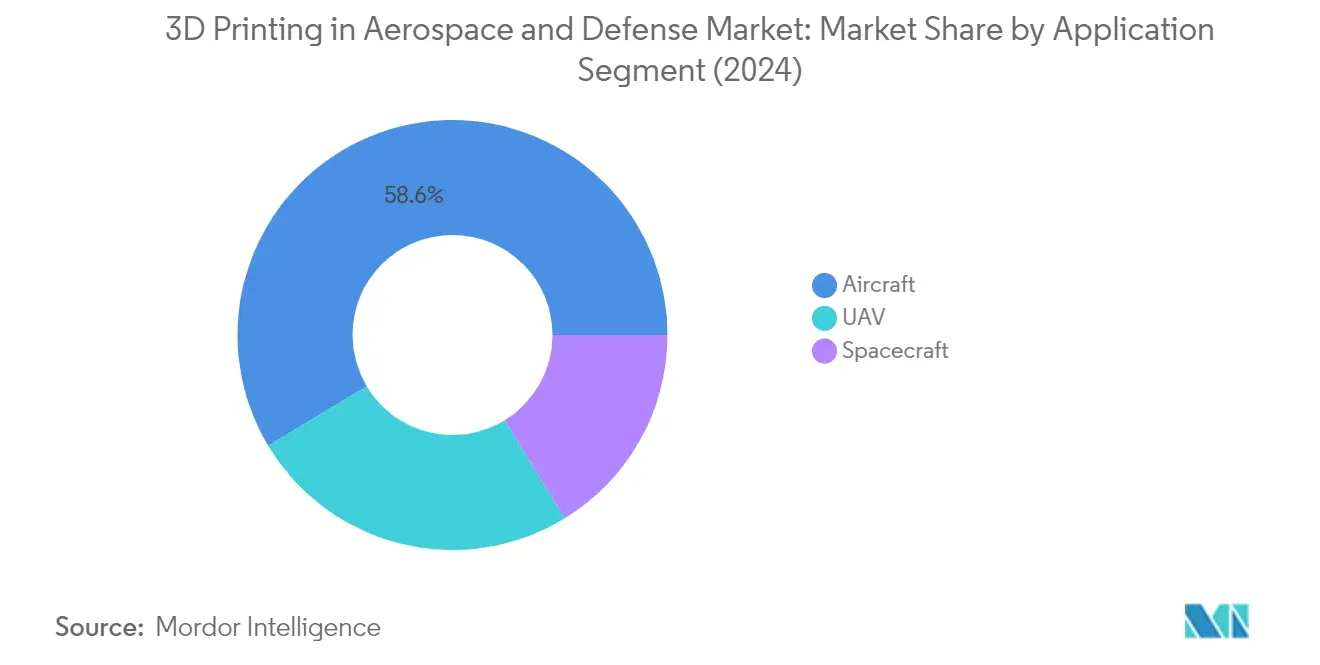

Aircraft Segment in 3D Printing in Aerospace and Defense Market

The aircraft 3D printing segment dominates the 3D printing in aerospace and defense market, commanding approximately 59% market share in 2024, while also maintaining the fastest growth trajectory with a projected growth rate of around 18% from 2024-2029. This segment's leadership position is driven by the revolutionary impact of 3D printing on aircraft manufacturing, enabling the production of parts at lower costs with faster lead times and more digitally flexible design methods. The technology has proven particularly valuable for manufacturing critical components like engine parts, structural elements, and cabin interiors. Major aircraft manufacturers are increasingly integrating aviation 3D printing into their production processes, with applications ranging from printing fuel nozzles and temperature sensors to heat exchangers and low-pressure turbine blades. The technology's ability to reduce material wastage, decrease component weight, and enable rapid prototyping has made it indispensable in modern aircraft manufacturing. Additionally, the use of 3D printing in aircraft maintenance, repair, and overhaul (MRO) operations has demonstrated significant cost savings, particularly in the restoration of damaged components that would otherwise require expensive replacements.

Remaining Segments in 3D Printing in A&D Market

The Unmanned Aerial Vehicles (UAV) and Spacecraft segments represent significant opportunities in the 3D printing aerospace and defense market. The UAV segment has witnessed substantial adoption of 3D printing technology for producing precise, high-quality components at reduced costs, enabling the creation of lightweight frames, enhanced maneuverability systems, and efficient communication components. The technology has proven particularly valuable in manufacturing customized parts for various UAV applications, from surveillance to defense operations. In the Spacecraft segment, space 3D printing has become increasingly crucial for satellite manufacturers and space exploration companies, enabling the production of complex geometries and customized components that can withstand extreme space conditions. The technology has demonstrated particular value in manufacturing satellite sensors, structural components, and various mission-critical parts, while significantly reducing production timelines and costs compared to traditional manufacturing methods.

Segment Analysis: By Material

Special Metals Segment in 3D Printing in Aerospace and Defense Market

Special metals dominate the 3D printing in aerospace and defense market, commanding approximately 59% of the market share in 2024. This significant market position is driven by the extensive use of materials such as titanium, gold, silver, platinum, and palladium in designing critical components and circuitry for aerospace and defense platforms. Manufacturing units of prominent aerospace and defense players are increasingly embracing 3D printing technology to cut costs and accelerate production for increasingly capable platforms such as aircraft, satellites, and spacecraft. The made-in-space concept has particularly attracted several startups and major organizations to invest in special metals additive manufacturing technologies, as these materials provide exceptional benefits in terms of structural strength, durability, and performance in extreme conditions.

Alloys Segment in 3D Printing in Aerospace and Defense Market

The alloys segment demonstrates robust growth potential in the 3D printing aerospace and defense market for the forecast period 2024-2029. This growth is primarily driven by the versatility of alloys in various 3D printing technologies, including metal deposition and laser sintering processes. Commercial organizations and universities are aggressively engaged in research and development to refine existing alloys used in additive manufacturing technologies, making them more stable and versatile. The segment's growth is further supported by the increasing adoption of alloy-based 3D printed components in aircraft engines, structural components, and defense applications, where the combination of strength, lightweight properties, and durability is crucial.

Remaining Segments in Material Segmentation

Other materials, primarily including polymers and composites, play a vital role in the 3D printing aerospace and defense market, particularly in non-structural applications and interior components. These materials are extensively used in manufacturing cabin interiors, ventilation systems, and various non-load-bearing components where aesthetic appeal and weight reduction are primary considerations. The segment's significance is particularly evident in aircraft interior applications, where these materials enable the production of highly customized components to fit specific cabin layouts and design requirements, while maintaining compliance with stringent aviation safety standards.

3D Printing In Aerospace And Defense Market Geography Segment Analysis

3D Printing in Aerospace and Defense Market in North America

North America represents a dominant force in the aerospace manufacturing industry, driven by the presence of major industry players and advanced technological infrastructure. The United States and Canada form the key markets in this region, with both countries demonstrating significant investments in research and development of aerospace 3D printing technologies. The region's growth is primarily attributed to the strong presence of aerospace and defense manufacturers, established supply chains, and supportive government policies promoting advanced manufacturing technologies.

3D Printing in Aerospace and Defense Market in United States

The United States leads the North American market with approximately 91% share of the regional market in 2024. The country's dominance is driven by the presence of major industry players like Boeing, Lockheed Martin, and NASA, which have enhanced the adoption of aircraft 3D printing technologies. The US Air Force and other defense organizations are actively incorporating additive manufacturing into their operations, particularly for rapid prototyping and spare parts production. The country's aerospace sector continues to leverage 3D printing for both commercial and military applications, with significant investments in research and development of new materials and printing technologies.

3D Printing in Aerospace and Defense Market Growth in United States

The United States is also experiencing the fastest growth in North America, with a projected CAGR of approximately 15% from 2024-2029. This growth is driven by increasing adoption of additive manufacturing in spacecraft component production, defense applications, and commercial aviation. The US military's growing focus on incorporating 3D printing for maintenance, repair, and overhaul (MRO) operations is creating new opportunities. Additionally, the country's strong focus on space 3D printing and satellite manufacturing is further accelerating the adoption of advanced 3D printing technologies.

3D Printing in Aerospace and Defense Market in Europe

Europe maintains a strong position in the aerospace and defense 3D printing market, with France, Germany, and the United Kingdom serving as key markets. The region's strength lies in its robust aerospace manufacturing infrastructure and significant investments in research and development of advanced materials. European aerospace firms are increasingly adopting 3D printing technologies to enhance their manufacturing capabilities and reduce production costs.

3D Printing in Aerospace and Defense Market in France

France dominates the European market with approximately 30% share of the regional market in 2024. The country's leadership position is supported by the presence of major aerospace incumbents like Airbus and Dassault Systems, who have established strong partnership agreements with local and international composite suppliers. The French aerospace industry has demonstrated significant commitment to integrating 3D printing technologies in both commercial and military applications.

3D Printing in Aerospace and Defense Market Growth in United Kingdom

The United Kingdom is emerging as the fastest-growing market in Europe for aerospace and defense 3D printing. The country's growth is driven by increasing expenditure on advanced aerospace systems development and the growing adoption of 3D printing technology in the manufacturing sector. The UK serves as a hub for R&D of advanced materials for the aerospace sector, with several aerospace incumbents creating steady demand for advanced composites.

3D Printing in Aerospace and Defense Market in Asia Pacific

The Asia Pacific region is witnessing substantial growth in the aerospace and defense 3D printing market, with China, India, and Japan emerging as key players. The region's expansion is driven by increasing investments in aerospace manufacturing capabilities, rising defense budgets, and growing adoption of advanced manufacturing technologies. Each country in the region is developing its unique strengths in different aspects of 3D printing applications.

3D Printing in Aerospace and Defense Market in China

China leads the Asia Pacific market in terms of market size, demonstrating strong capabilities in both commercial and military applications of 3D printing technology. The country's aerospace industry has started using 3D printing technologies extensively in new-generation aircraft manufacturing, with 3D printed parts being widely used in major aircraft manufacturing facilities. China's commitment to developing indigenous aerospace capabilities has led to significant investments in additive manufacturing technologies.

3D Printing in Aerospace and Defense Market Growth in India

India is emerging as the fastest-growing market in the Asia Pacific region for aerospace and defense 3D printing. The country's growth is driven by increasing investments in aviation sector development and rising defense manufacturing capabilities. India's approach to adopting 3D printing technology is comprehensive, with applications ranging from aircraft component manufacturing to defense equipment production.

3D Printing in Aerospace and Defense Market in Latin America

The Latin American market for aerospace and defense 3D printing is developing steadily, with Brazil and Mexico as the key markets. Brazil leads the regional market, benefiting from the presence of major aircraft manufacturers and increasing investments in aerospace research and development. Mexico is emerging as the fastest-growing market, driven by its growing aerospace manufacturing base and integration with North American supply chains.

3D Printing in Aerospace and Defense Market in Middle East and Africa

The Middle East and Africa region is gradually expanding its presence in the aerospace and defense 3D printing market, with the United Arab Emirates, Saudi Arabia, and South Africa as notable markets. The UAE leads the regional market, supported by its ambitious aerospace development programs and significant investments in advanced manufacturing technologies. Saudi Arabia is showing the fastest growth, driven by its increasing focus on defense modernization and aerospace sector development.

Get Analysis on Important Geographic Markets

Download PDF

Aerospace 3D Printing Industry Overview

Top Companies in 3D Printing in Aerospace and Defense Market

The aerospace 3D printing market is characterized by the strong presence of established aerospace and defense manufacturers who have integrated 3D printing capabilities into their operations. These companies are heavily investing in advanced materials development, particularly focusing on special metals and alloys suited for critical aerospace components. Product innovation is primarily centered around lightweight components, fuel system parts, and structural elements that can withstand extreme conditions. Companies are establishing dedicated additive manufacturing centers and forming strategic partnerships with technology providers to enhance their capabilities. Operational agility is being achieved through the implementation of digital manufacturing processes and cloud-based 3D printing services, enabling remote production and real-time monitoring. Strategic moves include significant investments in research and development facilities, particularly in regions with a strong aerospace presence like Europe and North America. Market expansion is being driven by increasing applications in both commercial aviation and defense sectors, with companies developing specialized solutions for different platform requirements.

Market Dominated by Integrated Defense Giants

The competitive landscape is primarily dominated by large-scale aerospace and defense conglomerates that have substantial resources for research and development in aerospace additive manufacturing technologies. Companies like GE Aviation, Boeing, Airbus, and Lockheed Martin have established themselves as market leaders through their extensive manufacturing capabilities and deep integration of 3D printing across their product lines. These companies leverage their existing relationships with defense departments and commercial airlines to maintain their market positions. The aerospace 3D printing market shows a high degree of consolidation, with the top players accounting for a significant share of the total market value.

The industry is witnessing strategic collaborations between traditional aerospace manufacturers and specialized 3D printing technology providers to enhance manufacturing capabilities. Merger and acquisition activities are focused on acquiring companies with advanced materials expertise and proprietary printing technologies. Regional players, particularly in emerging markets, are forming partnerships with global leaders to access advanced technologies and expand their market presence. The barrier to entry remains high due to the significant capital requirements, stringent certification processes, and the need for specialized expertise in both aerospace manufacturing and additive technologies.

Innovation and Integration Drive Future Success

Success in this market increasingly depends on the ability to develop proprietary materials and printing technologies specifically designed for aerospace applications. Incumbent companies need to focus on expanding their material portfolios, particularly in high-performance metals and composites, while continuously improving their manufacturing processes to reduce costs and increase production efficiency. The development of integrated digital platforms that can manage the entire additive manufacturing process, from design to final production, will be crucial for maintaining a competitive advantage. Companies must also invest in building robust supply chains that can ensure consistent material quality and timely delivery of components.

For new entrants and smaller players, success lies in identifying and focusing on specific niche applications where they can develop specialized expertise. The aerospace manufacturing industry presents opportunities for companies that can offer innovative solutions in areas such as rapid aerospace prototyping, spare parts manufacturing, and custom component development. Building strong relationships with certification authorities and understanding regulatory requirements is crucial for long-term success. The risk of substitution from traditional manufacturing methods is relatively low due to the unique capabilities of 3D printing in producing complex geometries and lightweight structures. However, companies must continue to demonstrate the cost-effectiveness and reliability of their 3D printed components to maintain customer confidence and market share.

Aerospace 3D Printing Market Leaders

-

3D Systems Corporation

-

EOS Gmbh

-

Ultimaker B.V.

-

Norsk Titanium AS

-

Stratasys Ltd.

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competiters?

Download PDF

Aerospace 3D Printing Market News

April 2024: Relativity Space signed a USD 8.7 million agreement with the US Air Force Research Lab to advance real-time flaw detection in additive manufacturing. This two-year project enhances quality control in large-scale metal 3-D printing, aligning with the National Defense Authorization Act's mandates to accelerate aerospace component production.

March 2024: GE Aerospace invested over USD 650 million in manufacturing and the supply chain, with over USD 150 million dedicated to additive manufacturing equipment. This includes USD 450 million for new equipment and facility upgrades at 22 sites in 14 states, USD 100 million for the base of US-based suppliers, and another USD 100 million for international sites in North America, Europe, and India.

March 2024: Safran Nacelles acquired 3DMF, enhancing its capabilities in high energy hydroforming (HEHF) for metal parts. This technology boosts Safran's production of nacelle and engine components, such as nozzles and air inlet lips. It facilitates manufacturing monolithic integrated structures from thick plates, advancing aerospace 3D printing.

February 2024: BotFactory secured a USD 1.25 million SBIR Phase II contract with AFWERX to advance ultra-fast additive manufacturing of electronics with correction and validation for the US Air Force. As part of the reformed SBIR/STTR program, the effort looks to improve national defense through leading-edge aerospace 3D printing technologies.

3D Printing in Aerospace and Defense Market Report - Table of Contents

1. INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.3 Market Restraints

-

4.4 Industry Attractiveness - Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5. MARKET SEGMENTATION

-

5.1 Application

- 5.1.1 Aircraft

- 5.1.2 Unmanned Aerial Vehicles

- 5.1.3 Spacecraft

-

5.2 Material

- 5.2.1 Alloys

- 5.2.2 Special Metals

- 5.2.3 Other Materials

-

5.3 Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.2 Europe

- 5.3.2.1 United Kingdom

- 5.3.2.2 France

- 5.3.2.3 Germany

- 5.3.2.4 Italy

- 5.3.2.5 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 India

- 5.3.3.3 Japan

- 5.3.3.4 South Korea

- 5.3.3.5 Rest of Asia-Pacific

- 5.3.4 Latin America

- 5.3.4.1 Mexico

- 5.3.4.2 Brazil

- 5.3.4.3 Rest of Latin America

- 5.3.5 Middle East and Africa

- 5.3.5.1 South Africa

- 5.3.5.2 Saudi Arabia

- 5.3.5.3 United Arab Emirates

- 5.3.5.4 Rest of Middle East and Africa

6. COMPETITIVE LANDSCAPE

- 6.1 Vendor Market Share

-

6.2 Company Profiles

- 6.2.1 Stratasys Ltd

- 6.2.2 3D Systems Corporation

- 6.2.3 Norsk Titanium AS

- 6.2.4 Ultimaker BV

- 6.2.5 ENVISIONTEC US LLC

- 6.2.6 GE Additive (General Electric Company)

- 6.2.7 EOS GmbH

- 6.2.8 MATERIALSE NV

- 6.2.9 Renishaw PLC

- 6.2.10 TRUMPF SE + Co. KG

- 6.2.11 OC Oerlikon Management AG

- 6.2.12 Hoganas AB

- *List Not Exhaustive

7. MARKET OPPORTUNITIES AND FUTURE TRENDS

You Can Purchase Parts Of This Report. Check Out Prices For Specific Sections

Get Price Break-up Now

Aerospace 3D Printing Industry Segmentation

3D printing or additive manufacturing refers to how the material is deposited, joined, or solidified under computer control to create a three-dimensional solid object from a digital file. The report covers 3D printing in the aviation (civil and military) and defense sectors. Terrestrial and naval vehicles are excluded from the scope of the study.

The aerospace 3D printing market is segmented by application, material, and geography. The report is segmented by application into aircraft, unmanned aerial vehicles, and spacecraft. By material, the market is segmented into alloys, special metals, and other materials. The report also covers the market sizes and forecasts for the aerospace 3D printing market in major countries across different regions. The market size is provided for each segment in terms of value (USD).

| Application | Aircraft | ||

| Unmanned Aerial Vehicles | |||

| Spacecraft | |||

| Material | Alloys | ||

| Special Metals | |||

| Other Materials | |||

| Geography | North America | United States | |

| Canada | |||

| Europe | United Kingdom | ||

| France | |||

| Germany | |||

| Italy | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| Latin America | Mexico | ||

| Brazil | |||

| Rest of Latin America | |||

| Middle East and Africa | South Africa | ||

| Saudi Arabia | |||

| United Arab Emirates | |||

| Rest of Middle East and Africa | |||

Need A Different Region or Segment?

Customize Now

3D Printing in Aerospace and Defense Market Research FAQs

How big is the 3D Printing In Aerospace And Defense Market?

The 3D Printing In Aerospace And Defense Market size is expected to reach USD 3.41 billion in 2025 and grow at a CAGR of 18.57% to reach USD 8.00 billion by 2030.

What is the current 3D Printing In Aerospace And Defense Market size?

In 2025, the 3D Printing In Aerospace And Defense Market size is expected to reach USD 3.41 billion.

Who are the key players in 3D Printing In Aerospace And Defense Market?

3D Systems Corporation, EOS Gmbh, Ultimaker B.V., Norsk Titanium AS and Stratasys Ltd. are the major companies operating in the 3D Printing In Aerospace And Defense Market.

Which is the fastest growing region in 3D Printing In Aerospace And Defense Market?

Asia-Pacific is estimated to grow at the highest CAGR over the forecast period (2025-2030).

Which region has the biggest share in 3D Printing In Aerospace And Defense Market?

In 2025, the Europe accounts for the largest market share in 3D Printing In Aerospace And Defense Market.

What years does this 3D Printing In Aerospace And Defense Market cover, and what was the market size in 2024?

In 2024, the 3D Printing In Aerospace And Defense Market size was estimated at USD 2.78 billion. The report covers the 3D Printing In Aerospace And Defense Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the 3D Printing In Aerospace And Defense Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Our Best Selling Reports

3D Printing In Aerospace And Defense Market Research

Mordor Intelligence provides comprehensive insights into the aerospace manufacturing industry. We specialize in detailed analysis of aerospace and defense 3D printing applications. Our extensive research covers the rapidly evolving landscape of aerospace manufacturing technologies. This includes aircraft 3D printing innovations and aerospace additive manufacturing developments. The report PDF, available for immediate download, offers an in-depth analysis of aviation 3D printing implementations and aerospace prototyping methodologies across the global industry.

Our research extensively covers military 3D printing applications and space 3D printing innovations. It offers stakeholders crucial insights into aerospace rapid prototyping and military additive manufacturing advancements. The analysis encompasses emerging trends in the aerospace manufacturing industry. It focuses on how defense 3D printing and aerospace 3D printing technologies are transforming traditional manufacturing processes. This comprehensive report equips decision-makers with actionable intelligence on the aerospace additive manufacturing market and military 3D printing market. It supports strategic planning and investment decisions in this dynamic sector.