| Study Period | 2024 - 2030 |

| Market Size (2025) | USD 1.05 Billion |

| Market Size (2030) | USD 2.58 Billion |

| CAGR (2025 - 2030) | 19.64 % |

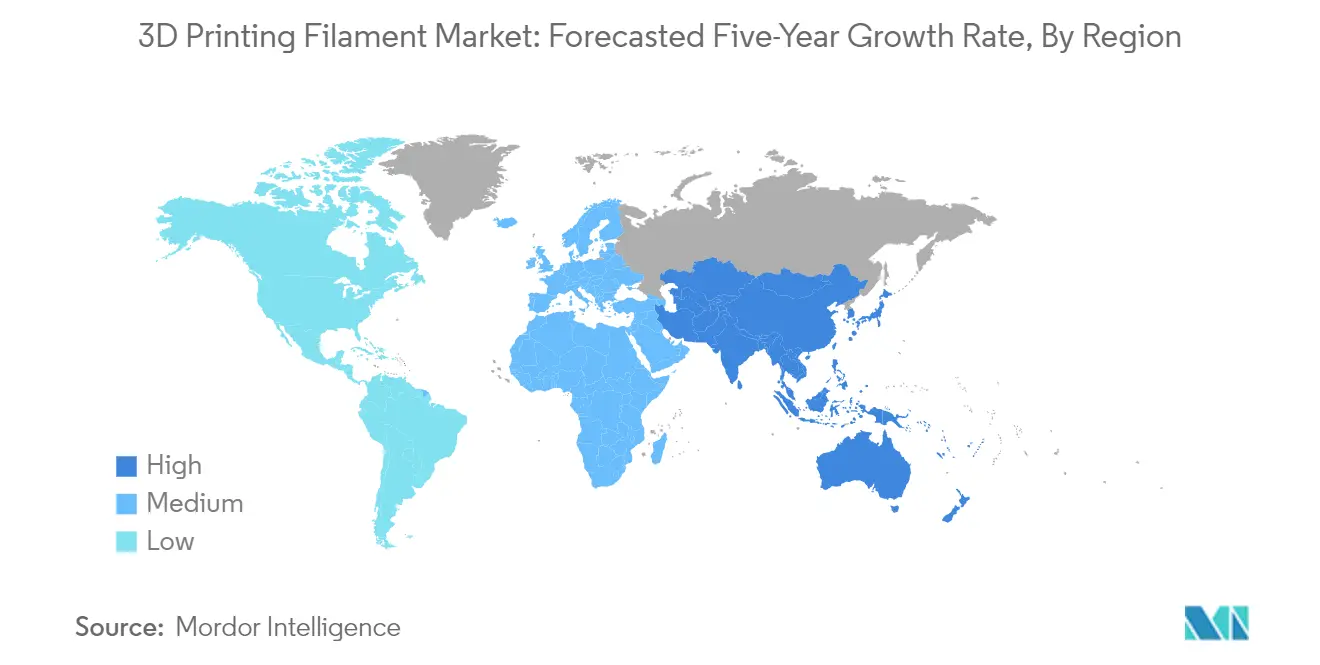

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Europe |

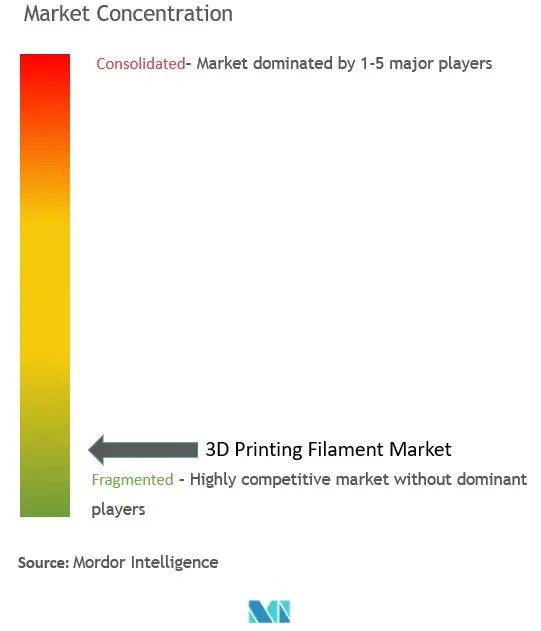

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order |

3D Printing Filament Market Analysis

The 3D Printing Filament Market size is estimated at USD 1.05 billion in 2025, and is expected to reach USD 2.58 billion by 2030, at a CAGR of 19.64% during the forecast period (2025-2030).

The 3D printing filament industry is experiencing significant consolidation through strategic mergers and acquisitions, reflecting the market's maturation and companies' efforts to expand their technological capabilities. In August 2022, Stratasys announced an agreement to acquire Covestro's additive manufacturing material business, while 3D Systems agreed to acquire dp polar GmbH, the designer of the industry's first additive manufacturing system for high-speed mass production. These strategic moves indicate a shift toward vertical integration and enhanced manufacturing capabilities within the industry, as companies seek to strengthen their market positions and expand their product portfolios.

The industry is witnessing increased adoption across diverse sectors, particularly in aerospace and defense applications. In August 2022, Boeing and Northrop Grumman signed up for participation in the Biden administration's Additive Manufacturing Forward initiative, aimed at strengthening US supply chains by increasing the use of 3D printing material for applications such as aerospace structures, radio-frequency sensors, and printed electronics. This initiative demonstrates the growing confidence in 3D printing technology for critical applications and highlights the industry's potential for revolutionizing traditional manufacturing processes.

Sustainability has emerged as a crucial focus area in the 3D printing filament industry, with manufacturers increasingly developing eco-friendly materials and processes. Companies are introducing innovative biodegradable filament and implementing recycling programs to address environmental concerns. For instance, Dutch startup Refil has pioneered the production of 3D filament made from recycled ABS and PET, primarily sourced from plastic bottles and car dashboards, while New Design University in Austria has developed a 100% compostable 3D filament made from natural raw materials.

The medical sector continues to drive innovation in 3D printing polymer applications, with significant developments in customized medical devices and implants. According to the SelectUSA program by the International Trade Administration, the US medical devices market, the largest globally, is projected to reach USD 208 billion by 2023, creating substantial opportunities for 3D printing applications. Healthcare companies are actively investing in 3D printing technology, with California-based PrinterPrezz securing USD 16 million in Series A financing to expand its efforts in 3D printing medical devices and implants, demonstrating the growing confidence in this technology for medical applications.

3D Printing Filament Market Trends

GROWING USAGE IN MANUFACTURING APPLICATIONS

The evolution of 3D printing filament has registered rapid growth across manufacturing applications, revolutionizing traditional production methods through tooling aids, visual prototypes, functional prototypes, and end-use parts. The technology offers unique advantages, including the reduction of risks and costs, the elimination of geometric limitations, reduced material wastage, higher production speed, and minimal storage space requirements. According to JABIL's industry survey, the use of plastic/polymer filaments increased significantly from 74% to 90% between 2019 and 2021, while metal usage grew from 39% to 60%, demonstrating the expanding adoption across manufacturing sectors.

Manufacturing companies are increasingly leveraging 3D printing filament for both low and high-volume production scenarios. For instance, Siemens Mobility manufactures spare parts and tooling on-demand at its RRX Rail Service Centre using 3D printing technology, enabling cost-effective inventory management and eliminating the expensive storage of low-demand parts. The technology's versatility extends to various materials—from ABS filament for manufacturing tool handles and automotive components to PLA filament for aircraft brackets and structural components. In 2023, companies like Desktop Metal have expanded their capabilities to produce lightweight and complex parts for aircraft using aluminum filaments, demonstrating the technology's growing sophistication in manufacturing applications.

Understand The Key Trends Shaping This Market

Download PDF

MASS CUSTOMIZATION ASSOCIATED WITH 3D PRINTING

Mass customization through 3D printing has emerged as a transformative force in modern manufacturing, enabling businesses to deliver personalized products without incurring additional tooling costs or production complexities. The technology's digital nature eliminates the need for costly tooling adjustments based on individual demand, as the design data is sent directly to the 3D printer without requiring specialized tools. This capability has found particular resonance in industries requiring high levels of customization—from personalized footwear fitted to individual foot measurements to custom medical prosthetics and dental implements tailored to patient anatomy.

The automotive and luxury sectors have been at the forefront of leveraging 3D printing for mass customization. Companies like Porsche have implemented innovative applications, such as 3D-printed customizable car seats with three different firmness levels, while furniture manufacturer Poltrona Frau enables customers to personalize furniture pieces through 3D printing technology. In the jewelry sector, manufacturers like Vowsmith demonstrate the scalability of customization, producing 35-40 rings per print with annual projections of 4,000 to 5,000 rings. The technology's versatility extends to the dental industry, where clinics worldwide utilize desktop dental 3D printers to produce a wide range of customized products, including aligners, dentures, prosthetics, night guards, and sports guards with high accuracy and rapid turnaround times. The use of 3D printer consumables and FDM material further enhances the customization capabilities, making it a vital component in the production process.

Segment Analysis: TYPE

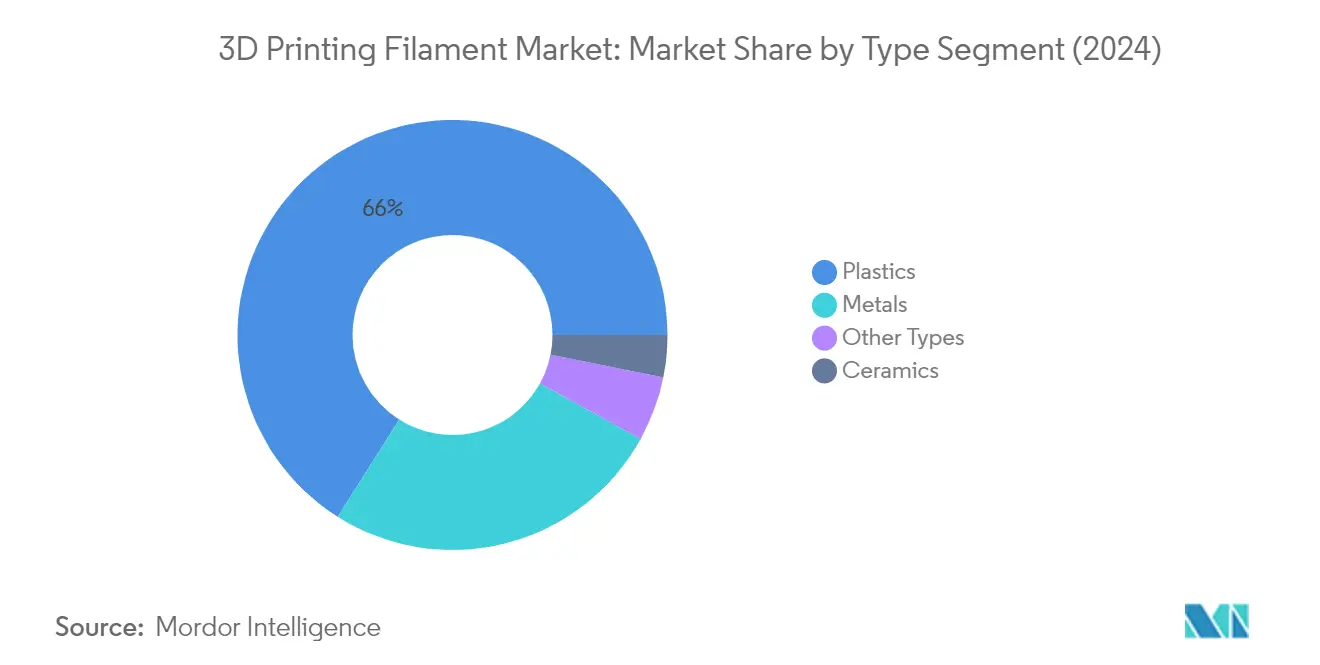

Plastics Segment in 3D Printing Filament Market

The plastics segment dominates the global 3D printing filament market, commanding approximately 66% of the market share in 2024. This significant market position is driven by the versatility and wide application range of plastic filaments, including PLA, ABS, PET, and nylon, across various industries. The segment's dominance is particularly evident in applications such as rapid prototyping, custom manufacturing, and consumer goods production. The extensive use of plastic filaments in medical device manufacturing, automotive parts production, and electronics has further strengthened its market position. Additionally, the continuous development of new plastic filament variants with enhanced properties, such as improved strength, heat resistance, and flexibility, has contributed to maintaining its market leadership. The segment is also experiencing the fastest growth trajectory in the market, driven by increasing adoption in mass customization applications and the development of eco-friendly variants.

Remaining Segments in 3D Printing Filament Market by Type

The metal filaments segment represents the second-largest portion of the market, with materials like titanium, stainless steel, and other metal alloys finding extensive applications in aerospace, defense, and medical implants. These materials are particularly valued for their strength, durability, and ability to produce functional end-use parts. The ceramics segment, while smaller, plays a crucial role in specialized applications such as dental prosthetics and industrial components requiring high temperature resistance. Other types, including wood-filled filaments and composite filament carbon fiber composites, serve niche markets where specific material properties are required. The continuous innovation in metal and ceramic filaments, particularly in terms of printability and final part properties, is driving their adoption in high-value applications. The development of new composite materials and specialty filaments is also expanding the possibilities for advanced manufacturing applications.

Segment Analysis: APPLICATION

Medical and Dental Segment in 3D Printing Filament Market

The medical and dental segment dominates the global 3D printing filament market, accounting for approximately 34% of the market share in 2024. This segment's leadership position is driven by the increasing adoption of 3D printing material technology in manufacturing medical devices, implants, dental restorations, and surgical instruments. The segment's growth is particularly strong in advanced economies where healthcare spending and technological adoption are high. The ability to create customized medical devices and implants that match patient anatomy, coupled with the capability to produce complex internal structures, has made FDM printing filament indispensable in the medical sector. The segment is also experiencing the fastest growth rate in the market, projected to expand at approximately 21% annually from 2024 to 2029, driven by increasing research and development activities, growing demand for personalized medical solutions, and continuous innovation in biocompatible printing materials.

Remaining Segments in 3D Printing Filament Market Applications

The aerospace and defense segment represents the second-largest application area, driven by the increasing use of 3D printing thermoplastic filaments in manufacturing aircraft components, prototypes, and defense equipment. The automotive sector has emerged as another significant segment, with applications ranging from prototyping to the production of custom parts and components, particularly in the electric vehicle sector. The electronics segment utilizes 3D printing filaments for producing circuit boards, energy storage devices, and various electronic components, while other applications include construction, consumer goods, and industrial manufacturing. Each of these segments contributes to the market's diversity and growth, with manufacturers continuously developing specialized filaments to meet the unique requirements of these applications.

3D Printing Filament Market Geography Segment Analysis

3D Printing Filament Market in Asia-Pacific

The Asia-Pacific region represents a dynamic market for 3D printing filaments, driven by rapid industrialization and technological adoption across various sectors. Countries like China, Japan, India, and South Korea are making significant investments in additive manufacturing technologies. The region benefits from a strong manufacturing base, particularly in the electronics and automotive sectors, along with growing aerospace and medical device industries. Government initiatives supporting advanced manufacturing technologies and increasing adoption of 3D printing in industrial applications are further propelling market growth across the region.

3D Printing Filament Market in China

China dominates the Asia-Pacific 3D printing filament market, holding approximately 55% share of the regional market. The country's leadership position is supported by its robust electronics manufacturing sector and significant investments in aerospace and defense applications. The automotive sector in China continues to be a major driver, with increasing adoption of 3D printing technologies for prototyping and production parts. The country's healthcare sector is also emerging as a significant consumer of 3D printing filaments, particularly in dental and medical device applications. The government's "Made in China 2025" initiative continues to drive innovation and adoption of advanced manufacturing technologies, including 3D printing.

3D Printing Filament Market Growth Trajectory in China

China is also leading the region's growth trajectory, with a projected growth rate of approximately 24% from 2024-2029. This exceptional growth is driven by increasing domestic demand for 3D printing applications across various industries. The country's aerospace industry is witnessing significant expansion, with airline companies planning substantial aircraft purchases. The automotive sector's transition towards electric vehicles is creating new opportunities for 3D printing applications. Additionally, the medical device manufacturing sector is experiencing rapid growth, with over 27,000 companies operating in the country, driving demand for specialized 3D printing filaments.

3D Printing Filament Market in North America

North America represents a mature market for 3D printing filaments, characterized by high technology adoption rates and the presence of major market players. The United States, Canada, and Mexico form the key markets in this region, with strong demand from the aerospace, automotive, and healthcare sectors. The region's market is driven by substantial R&D investments, advanced manufacturing capabilities, and growing applications in medical device manufacturing. The presence of leading aerospace manufacturers and automotive companies continues to drive innovation in 3D printing materials and applications.

3D Printing Filament Market in United States

The United States leads the North American market, commanding approximately 86% of the regional market share. The country's dominance is supported by its strong aerospace and defense sector, robust automotive industry, and advanced healthcare infrastructure. The presence of major 3D printer manufacturers and material suppliers has created a strong ecosystem for market growth. The country's medical device market, valued as the largest globally, continues to drive innovation in 3D printing applications, particularly in customized medical solutions and dental applications.

3D Printing Filament Market Growth Trajectory in United States

The United States is experiencing the highest growth rate in North America, with an expected growth rate of approximately 17% from 2024-2029. This growth is driven by increasing adoption of 3D printing technologies across various industries. The country's aerospace sector continues to expand, with strong commercial aircraft demand and defense applications. The automotive industry's transition towards electric vehicles and the growing medical device sector are creating new opportunities for 3D printing applications. Additionally, the increasing focus on customized medical solutions and dental applications is driving demand for specialized 3D printing filaments.

3D Printing Filament Market in Europe

Europe represents a significant market for 3D printing filaments, with Germany, the United Kingdom, France, and Italy as key contributing countries. The region's market is characterized by a strong focus on industrial applications, particularly in the automotive, aerospace, and medical sectors. European countries are at the forefront of adopting advanced manufacturing technologies, supported by various government initiatives and strong research and development activities. The presence of major automotive manufacturers and aerospace companies continues to drive innovation in 3D printing applications.

3D Printing Filament Market in Germany

Germany leads the European market with its strong industrial base and advanced manufacturing capabilities. The country's automotive sector is a major driver for 3D printing applications, with numerous manufacturers adopting this technology for prototyping and production. The presence of leading aerospace companies and research institutions supports continuous innovation in 3D printing technologies. Germany's medical device industry also contributes significantly to market growth, with increasing adoption of 3D printing for customized medical solutions.

3D Printing Filament Market Growth Trajectory in Germany

Germany is experiencing the strongest growth in the European region, driven by increasing adoption across various industrial sectors. The country's automotive industry continues to innovate with 3D printing applications, particularly in electric vehicle manufacturing. The aerospace sector's growth and increasing focus on medical device manufacturing are creating new opportunities. Additionally, the country's strong focus on research and development in advanced manufacturing technologies is supporting market expansion.

3D Printing Filament Market in South America

The South American market for 3D printing filaments is emerging as a promising growth region, with Brazil and Argentina as key markets. The region is witnessing increasing adoption of 3D printing technologies across various industrial sectors, particularly in automotive and aerospace applications. Brazil emerges as the largest market in the region, while also showing the fastest growth potential. The region's manufacturing sector is gradually embracing advanced technologies, with increasing investments in 3D printing capabilities. Government initiatives supporting industrial modernization and growing awareness about additive manufacturing technologies are driving market growth across South America.

3D Printing Filament Market in Middle East & Africa

The Middle East & Africa region represents an emerging market for 3D printing filaments, with Saudi Arabia and South Africa as notable markets. The region is witnessing growing adoption of 3D printing technologies, particularly in construction, aerospace, and medical applications. South Africa emerges as the largest market in the region, while also demonstrating the fastest growth potential. The region's focus on industrial diversification and increasing investments in advanced manufacturing technologies are driving market growth. Government initiatives supporting technological advancement and growing awareness about additive manufacturing benefits are creating new opportunities across various sectors.

Get Analysis on Important Geographic Markets

Download PDF

3D Printing Filament Industry Overview

Top Companies in 3D Printing Filament Market

The global 3D printing filament market is led by major players, including Stratasys, SABIC, BASF SE, Evonik Industries, and Mitsubishi Chemical Corporation, who are driving innovation through continuous research and development initiatives. These industry leaders are focusing on expanding their product portfolios through strategic acquisitions and collaborations with regional distributors and manufacturers. Companies are investing heavily in developing new 3D printing materials and technologies while establishing innovation hubs across different regions to strengthen their market presence. The trend of vertical integration is becoming prominent, with companies like Stratasys acquiring material businesses to secure their supply chain. Product differentiation through enhanced properties and applications, coupled with the establishment of strong distribution networks, remains a key competitive strategy in the market.

Fragmented Market with High Growth Potential

The 3D printing filament market exhibits a highly fragmented structure with numerous global and domestic players operating across different regions. While established chemical conglomerates like BASF SE and SABIC leverage their extensive resources and distribution networks, specialized manufacturers are carving out niches through focused product development and customer relationships. The market is witnessing significant consolidation through mergers and acquisitions, as exemplified by Forward AM's acquisition of Owens Corning's Xstrand business and DSM's strategic acquisition of Clariant's 3D printing business.

The competitive landscape is characterized by fierce competition among existing and upcoming players, with many attempting to expand their product portfolios and geographic presence. Major companies are establishing partnerships with local manufacturers and distributors to penetrate new markets and enhance their regional footprint. The industry is seeing a trend where larger companies are acquiring smaller, innovative firms to boost their existing output and add specialized products to their portfolio, while also gaining access to new technologies and market segments.

Innovation and Distribution Drive Market Success

Success in the 3D printing filament market increasingly depends on companies' ability to innovate and develop application-specific solutions while maintaining strong distribution networks. Market leaders are investing in research and development centers to create new technologies and materials that meet evolving customer demands across industries such as aerospace, automotive, and healthcare. Companies are also focusing on establishing strategic partnerships with end-users and technology providers to develop customized solutions and secure long-term contracts.

The market presents significant barriers to entry due to high capital requirements and technical expertise needed for product development. However, opportunities exist for new entrants through innovative product offerings and strategic partnerships. Companies need to focus on intellectual property protection while navigating emerging regulatory frameworks, particularly in medical and aerospace applications. The ability to provide consistent quality, technical support, and after-sales service, combined with strong relationships with key industry stakeholders, will be crucial for maintaining a competitive advantage in this evolving market. Additionally, the development of additive manufacturing materials and 3D printing raw materials is essential for companies aiming to secure a competitive edge.

3D Printing Filament Market Leaders

-

Stratasys Ltd.

-

SABIC

-

BASF SE

-

Evonik Industries AG

-

Mitsubishi Chemical Corporation

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competiters?

Download PDF

3D Printing Filament Market News

- February 2024: Evonik Industries AG launched its INFINAM FR 4100 L 3D printing resin, designed for use with digital light processing (DLP) 3D printing technology. This resin is used to manufacture touch, pliable, and flame-retardant parts.

- February 2024: Solvay spun off its specialty business to an independent company, Syensqo. All 3D printing-related activities of Solvay are projected to be integrated into and ultimately become Syensqo businesses.

- October 2023: Evonik Industries AG introduced a new carbon fiber reinforced PEEK filament that can be processed in common extrusion-based 3D printing technologies, such as fused filament fabrication (FFF), and is suitable for use in long-term 3D-printed medical implants.

- June 2023: Mitsubishi Chemical Corporation announced its distribution collaboration with FormFutura to make the company an official distribution partner for Mitsubishi Chemical’s portfolio of 3D printing filaments.

3D Printing Filament Market Report - Table of Contents

1. INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET DYNAMICS

-

4.1 Drivers

- 4.1.1 Growing Usage in Manufacturing Applications

- 4.1.2 Mass Customization Associated with 3D Printing

-

4.2 Restraints

- 4.2.1 High Capital Investment Requirement in 3D Printing Process

- 4.3 Industry Value Chain Analysis

-

4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5. MARKET SEGMENTATION (Market Size in Value)

-

5.1 Type

- 5.1.1 Metals

- 5.1.1.1 Titanium

- 5.1.1.2 Stainless Steel

- 5.1.1.3 Other Metals

- 5.1.2 Plastics

- 5.1.2.1 Polyethylene Terephthalate (PET)

- 5.1.2.2 Polylactic Acid (PLA)

- 5.1.2.3 Acrylonitrile Butadiene Styrene (ABS)

- 5.1.2.4 Nylon

- 5.1.2.5 Other Plastics

- 5.1.3 Ceramics

- 5.1.4 Other Types

-

5.2 Application

- 5.2.1 Aerospace and Defense

- 5.2.2 Automotive

- 5.2.3 Medical and Dental

- 5.2.4 Electronics

- 5.2.5 Other Applications

-

5.3 Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Malaysia

- 5.3.1.6 Thailand

- 5.3.1.7 Vietnam

- 5.3.1.8 Indonesia

- 5.3.1.9 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Spain

- 5.3.3.6 Russia

- 5.3.3.7 NORDIC

- 5.3.3.8 Turkey

- 5.3.3.9 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Colombia

- 5.3.4.4 Rest of South America

- 5.3.5 Middle East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 United Arab Emirates

- 5.3.5.4 Nigeria

- 5.3.5.5 Qatar

- 5.3.5.6 Egypt

- 5.3.5.7 Rest of Middle East and Africa

6. COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%)**/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

-

6.4 Company Profiles

- 6.4.1 BASF SE

- 6.4.2 Covestro Ag

- 6.4.3 DOW

- 6.4.4 DSM

- 6.4.5 Evonik Industries Ag

- 6.4.6 Keene Village Plastics

- 6.4.7 Mitsubishi Chemical Corporation

- 6.4.8 SABIC

- 6.4.9 Solvay

- 6.4.10 Shenzhen Esun Industrial Co. Ltd

- 6.4.11 Stratasys

- *List Not Exhaustive

7. MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 3D Printing Innovation in the Medical Industry

- 7.2 Advancements in 3D Printing Materials

**Subject to Availability

You Can Purchase Parts Of This Report. Check Out Prices For Specific Sections

Get Price Break-up Now

3D Printing Filament Industry Segmentation

3D printer filament is a type of printing material used by the FFF-type 3D printer. It is one of the most common 3D printing materials in the world. It is mostly made of thermoplastic. However, metal, ceramics, and other materials are also used to make 3D printing filaments.

The 3D printing filament market is segmented by type, application, and geography. By type, the market is segmented into metals, plastics, ceramics, and other types (carbon fiber, etc.). By application, the market is segmented into aerospace and defense, automotive, medical and dental, electronics, and other applications (tool-making, etc.). The report also covers the market sizes and forecasts for the 3D printing filament market in 27 countries across major regions. For each segment, the market sizes and forecasts are provided based on revenue (USD).

| Type | Metals | Titanium | |

| Stainless Steel | |||

| Other Metals | |||

| Plastics | Polyethylene Terephthalate (PET) | ||

| Polylactic Acid (PLA) | |||

| Acrylonitrile Butadiene Styrene (ABS) | |||

| Nylon | |||

| Other Plastics | |||

| Ceramics | |||

| Other Types | |||

| Application | Aerospace and Defense | ||

| Automotive | |||

| Medical and Dental | |||

| Electronics | |||

| Other Applications | |||

| Geography | Asia-Pacific | China | |

| India | |||

| Japan | |||

| South Korea | |||

| Malaysia | |||

| Thailand | |||

| Vietnam | |||

| Indonesia | |||

| Rest of Asia-Pacific | |||

| North America | United States | ||

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| NORDIC | |||

| Turkey | |||

| Rest of Europe | |||

| South America | Brazil | ||

| Argentina | |||

| Colombia | |||

| Rest of South America | |||

| Middle East and Africa | Saudi Arabia | ||

| South Africa | |||

| United Arab Emirates | |||

| Nigeria | |||

| Qatar | |||

| Egypt | |||

| Rest of Middle East and Africa | |||

Need A Different Region or Segment?

Customize Now

3D Printing Filament Market Research Faqs

How big is the 3D Printing Filament Market?

The 3D Printing Filament Market size is expected to reach USD 1.05 billion in 2025 and grow at a CAGR of 19.64% to reach USD 2.58 billion by 2030.

What is the current 3D Printing Filament Market size?

In 2025, the 3D Printing Filament Market size is expected to reach USD 1.05 billion.

Who are the key players in 3D Printing Filament Market?

Stratasys Ltd., SABIC, BASF SE, Evonik Industries AG and Mitsubishi Chemical Corporation are the major companies operating in the 3D Printing Filament Market.

Which is the fastest growing region in 3D Printing Filament Market?

Asia-Pacific is estimated to grow at the highest CAGR over the forecast period (2025-2030).

Which region has the biggest share in 3D Printing Filament Market?

In 2025, the Europe accounts for the largest market share in 3D Printing Filament Market.

What years does this 3D Printing Filament Market cover, and what was the market size in 2024?

In 2024, the 3D Printing Filament Market size was estimated at USD 0.84 billion. The report covers the 3D Printing Filament Market historical market size for years: 2024. The report also forecasts the 3D Printing Filament Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Our Best Selling Reports

3D Printing Filament Market Research

Mordor Intelligence provides a comprehensive analysis of the 3D printing filament industry. We leverage our extensive expertise in additive manufacturing material research to deliver this detailed examination. The report covers a wide range of materials, including PLA filament, TPU filament, PETG filament, and ABS filament technologies. It offers in-depth insights into 3D printing material developments, from traditional nylon filament to advanced engineering filament solutions. Our analysis also includes FDM printing filament technologies and emerging biodegradable filament innovations. This information is available in an easy-to-read report PDF format for immediate download.

The report provides stakeholders with crucial insights into 3D printing supplies and 3D printer consumables. It examines both composite filament and specialty filament categories. Our research thoroughly evaluates 3D printing polymer applications and 3D printing thermoplastic developments. Additionally, it analyzes trends in raw materials for 3D printing. The comprehensive coverage includes a detailed analysis of materials for FDM printing and their applications across various industries. Stakeholders gain valuable understanding of emerging technologies, market dynamics, and future opportunities in the additive manufacturing material market. This is supported by extensive data and expert analysis.