Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

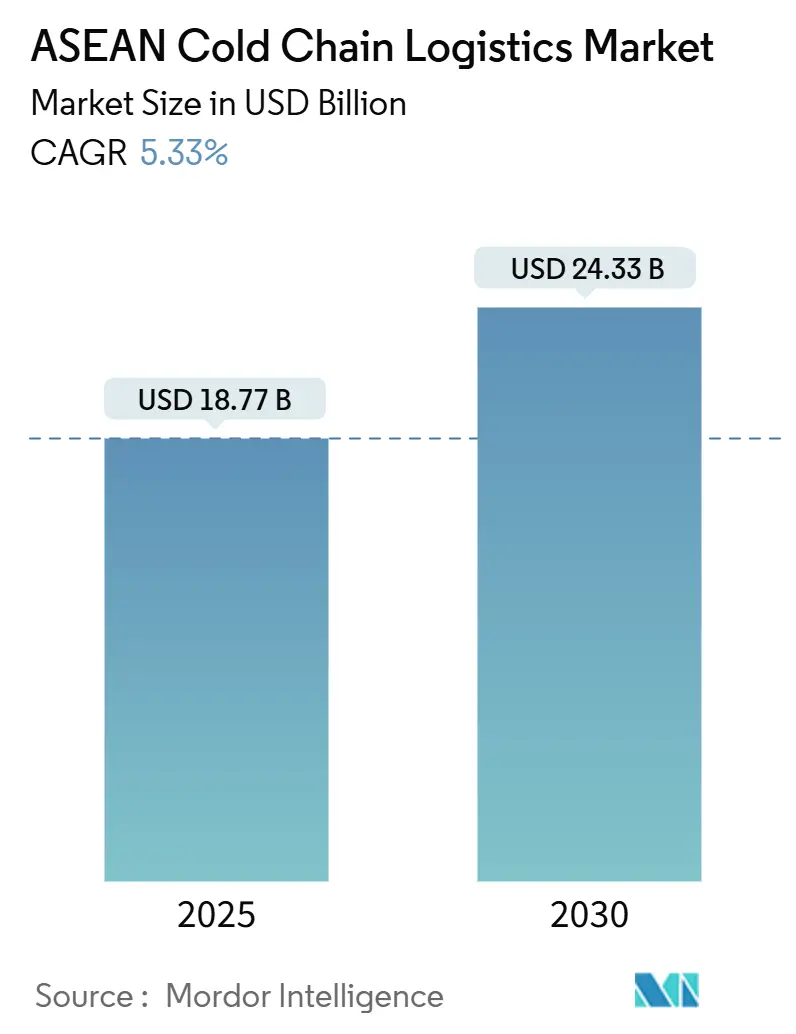

| Market Size (2025) | USD 18.77 Billion |

| Market Size (2030) | USD 24.33 Billion |

| Growth Rate (2025 - 2030) | 5.33% CAGR |

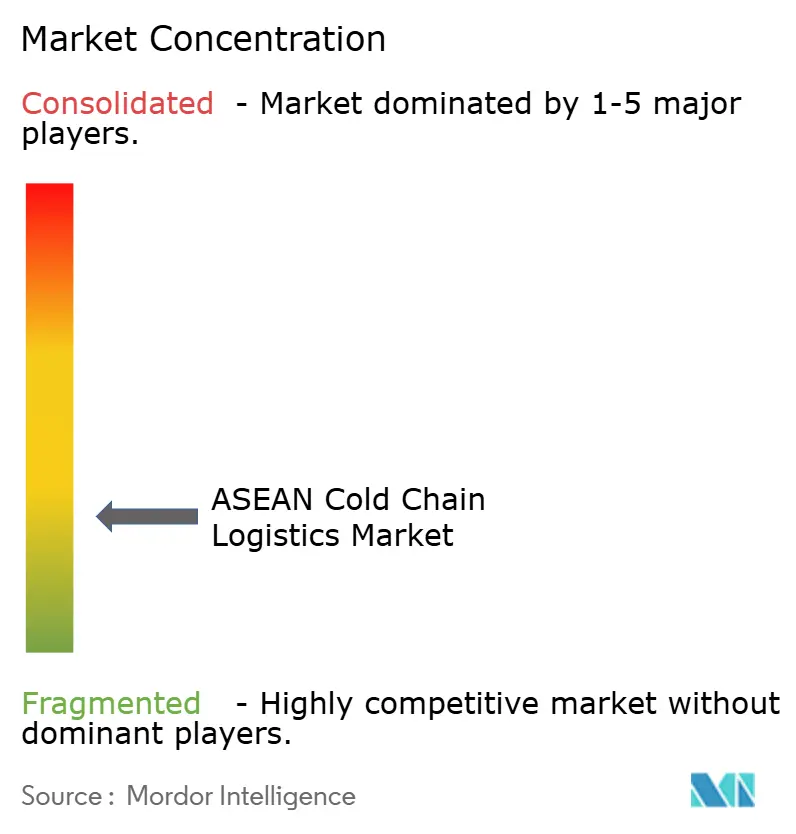

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

ASEAN Cold Chain Logistics Market Analysis by Mordor Intelligence

The ASEAN Cold Chain Logistics Market size is estimated at USD 18.77 billion in 2025, and is expected to reach USD 24.33 billion by 2030, at a CAGR of 5.33% during the forecast period (2025-2030).

Demand is rising because online grocery penetration, vaccine distribution, and cross-border trade reforms are widening temperature-controlled distribution requirements across Southeast Asia. Operators are racing to add energy-efficient warehouses and multi-modal refrigerated transport fleets that meet tighter food-safety and GDP standards. Competitive dynamics favor providers that couple dense storage networks with digital tools for real-time temperature visibility, as last-mile reliability is now a decisive factor in contract awards. Consolidation is underway as global integrators acquire regional specialists to lock in strategic sites near major consumption hubs.

Key Report Takeaways

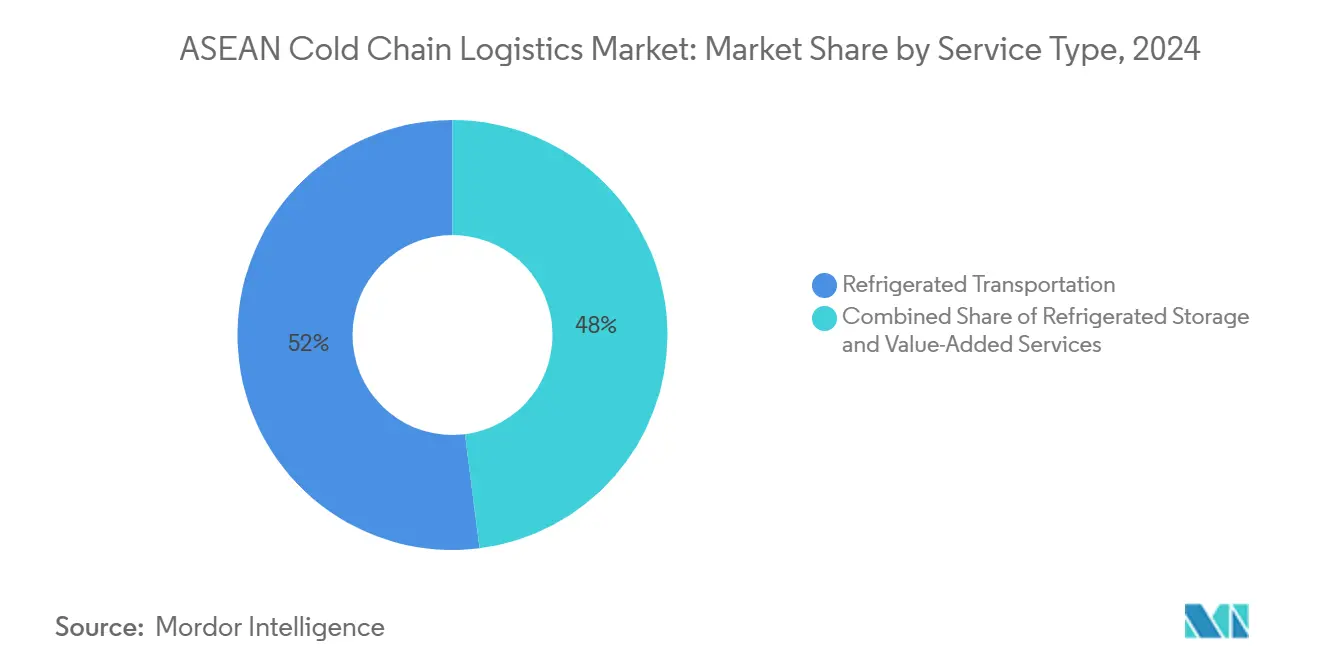

- By service type, refrigerated storage led with 52% revenue share in 2024; value-added services are projected to expand at a 4.10% CAGR through 2030.

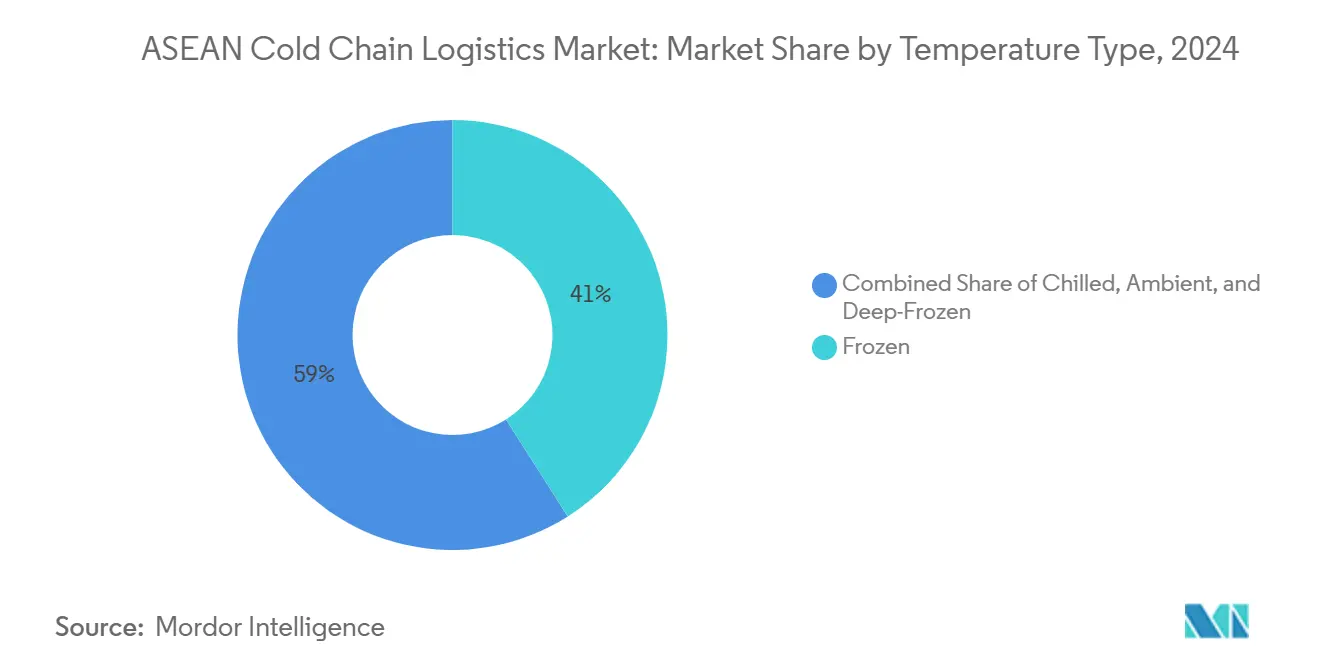

- By temperature type, frozen storage accounted for 41% share of the ASEAN cold chain logistics market size in 2024, while chilled storage is expected to advance at a 4.90% CAGR through 2030.

- By application, meat & seafood captured 27% share of the ASEAN cold chain logistics market size in 2024; vaccines & clinical trial materials are forecast to grow at a 5.22% CAGR to 2030.

- By geography, Indonesia held 22% of the ASEAN cold chain logistics market share in 2024 and Thailand is forecast to register a 5.10% CAGR between 2025 and 2030.

ASEAN Cold Chain Logistics Market Trends and Insights

Drivers Impact Analysis

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| E-commerce boom fuelling last-mile cold distribution | +1.2% | Indonesia, Thailand, Vietnam with spillover to Malaysia | Medium term (2-4 years) |

| Rising demand for perishable foods & seafood exports | +0.9% | Global, with concentration in Vietnam, Thailand, Indonesia | Long term (≥ 4 years) |

| Pharmaceutical and vaccine temperature-controlled logistics surge | +1.4% | Singapore, Thailand, Malaysia as regional hubs | Short term (≤ 2 years) |

| ASEAN Single Window accelerating cross-border cold freight | +0.8% | Thailand-Malaysia-Singapore corridor, expanding regionally | Medium term (2-4 years) |

| Halal-compliant logistics requirements in Malaysia and Indonesia | +0.6% | Malaysia, Indonesia with export reach to global Muslim markets | Long term (≥ 4 years) |

| ESG funding favouring green refrigerants and energy-efficient assets | +0.7% | Singapore, Thailand, Malaysia leading adoption | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Understand The Key Trends Shaping This Market

Download PDF

E-commerce Boom Fuelling Last-Mile Cold Distribution

Online grocery and meal-kit platforms are scaling rapidly, making temperature-controlled micro-fulfillment capabilities essential for same-day deliveries in Jakarta, Bangkok, and Ho Chi Minh City. Smaller urban stores and cloud kitchens rely on distributed chillers rather than centralized warehouses, shifting investment toward modular, energy-efficient refrigeration units that fit dense city footprints. Indonesian startups such as Paxel and Coldspace integrate IoT sensors that upload real-time data to cloud dashboards, providing proof of temperature compliance for food brands. Regulators encourage digital tools by releasing ASEAN guidelines on smart agriculture and food distribution, which outline interoperable data standards for farm-to-fork traceability[1]“Accelerating the Digitalisation of the Agriculture and Food System in the ASEAN Region,” Economic Research Institute for ASEAN and East Asia, eria.org. As customer expectations tighten around freshness guarantees, 5G-enabled route optimization and predictive maintenance are becoming baseline requirements for last-mile fleets, spurring partnerships between telcos and logistics providers.

Rising Demand for Perishable Foods & Seafood Exports

Vietnam and Thailand continue to climb the value chain in global seafood commerce, reinforcing the need for blast-freezing, quick-chilling, and controlled-atmosphere shipping to preserve quality during long voyages to North America and Europe[2]“Asia-Pacific Trade Facilitation Report 2024,” Asian Development Bank, adb.org. Government export incentives and free-trade agreements drive cold-chain upgrades in processing hubs near Da Nang and Samut Sakhon, where producers now demand ISO 22000-compliant warehouses. Multi-country consolidation centers in Malaysia and Singapore re-pack mixed loads bound for retail chains, leveraging digital customs platforms that slash border dwell times by 11% on average. Temperature outages carry brand-reputation risks, so exporters install satellite trackers and blockchain seals that trigger alerts when limits are breached. Container lines add more reefer plugs at ASEAN deep-sea ports, while inland haulers invest in dual-evaporator trailers that switch between chilled and frozen settings on multi-drop routes.

Pharmaceutical & Vaccine Temperature-Controlled Logistics Surge

Regional vaccine manufacturing under the ASEAN Vaccine Security and Self-Reliance initiative has amplified sub-zero storage needs for bulk antigen shipments departing plants in Bangkok and Penang[3]“Unlocking Regional Power Trade,” ASEAN-BAC, asean-bac.org. DHL earmarked EUR 500 million (USD 551.82 million) for GDP-certified hubs that feature −80°C freezers and redundant power systems, positioning Singapore as the region’s principal life-science gateway. Indonesia tightened rules by mandating CDAKB certificates for medical-device distributors, prompting wholesalers to retrofit depots with validation-ready monitoring systems. Clinical-trial sponsors require cloud-based custody logs, so operators embed IoT probes that record minute-by-minute temperature data from origin to investigator site. The push for mRNA therapies accelerates demand for dry-ice replenishment stations and active containers, shifting the ASEAN cold chain logistics market toward high-margin specialty services.

ASEAN Single Window Accelerating Cross-Border Cold Freight

The April 2025 roll-out of the ASEAN Customs Transit System allows a single electronic declaration to cover multi-country truck moves, cutting paperwork and border times for perishable cargo. Thailand’s pilot with Malaysia and Singapore shows release times falling below 30 minutes at key checkpoints, enabling continuous refrigeration without generator switch-overs. Indonesia’s National Logistics Ecosystem achieved 98% adoption at major ports and airports, demonstrating how digital lodgment platforms can synchronize cold-room allocations and haulage slots. Faster border throughput improves equipment utilization, which lowers operating costs and incentivizes investment in new reefer fleets. Shippers now design milk-run corridors that link produce farms in Mekong Delta to retail DCs in Kuala Lumpur within 36 hours, enhancing inventory freshness and reducing spoilage.

Restraints Impact Analysis

| Restraint | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fragmented infrastructure & unreliable power supply | -1.1% | Indonesia, Philippines, Vietnam with infrastructure gaps | Long term (≥ 4 years) |

| High urban land and energy costs for cold facilities | -0.7% | Singapore, urban centers in Thailand, Malaysia | Medium term (2-4 years) |

| Kigali-driven refrigerant phase-out compliance costs | -0.5% | Global, with higher impact in developing ASEAN economies | Medium term (2-4 years) |

| Skilled talent shortage in IoT-enabled temperature monitoring | -0.4% | Regional, particularly affecting technology adoption | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Fragmented Infrastructure & Unreliable Power Supply

Electricity demand across ASEAN is set to triple by 2050, yet distribution grids in outer islands and rural zones still suffer voltage instability that can spoil an entire cold room inventory within hours. Indonesia’s warehouse operators install costly diesel gensets to protect against blackouts, adding 15-20% to operating expenses. Cold facilities in the Philippines and Vietnam face similar issues, which deter investors and raise insurance premiums. The ASEAN Power Grid concept promises cross-border energy trade, but technical harmonization and financing hurdles slow progress. Until reliability improves, operators may confine expansion to Tier-1 corridors, limiting the ASEAN cold chain logistics market’s penetration in secondary cities.

High Urban Land and Energy Costs for Cold Facilities

Singapore’s land scarcity drives warehouse rents above USD 200 per m² annually, constraining on-island cold-room expansion despite proximity advantages to Changi air cargo flows. Operators shift to multi-tier mezzanine structures to increase pallet density, but lift-truck automation and racking systems escalate capital budgets. Energy price volatility compounds cost pressures because refrigeration can account for 50-70% of facility power bills, especially where tariffs link to LNG imports. Bangkok and Kuala Lumpur face similar land-cost inflation, pushing new sites to peripheral zones that lengthen delivery routes. The economics of urban cold storage therefore hinge on high throughput and premium service offerings to justify elevated cost structures.

Segment Analysis

By Service Type: Diversified Storage Anchors Growth

ASEAN cold chain logistics market size for refrigerated storage reached USD 9.77 billion in 2024, equal to 52% of total value. High humidity and equatorial temperatures across the archipelago economies mandate year-round temperature control, making storage networks the backbone of integrated solutions. Providers differentiate by adding automated pallet shuttles, multi-chamber zoning, and HACCP-certified quality management that reduce handling errors. Many exporters adopt public multi-tenant warehouses to de-risk capital outlays, contracting dedicated bays during harvest peaks. Second-generation facilities near Surabaya and Laem Chabang incorporate solar rooftops and thermal-energy storage to shave peak-hour electricity charges, illustrating how ESG imperatives align with cost control within the ASEAN cold chain logistics market.

Value-added services generated USD 1.23 billion in 2024 and delivered the fastest 4.10% CAGR to 2030, buoyed by pharmaceutical kitting, customs pre-clearance, and IoT-enabled condition reporting. GDP-compliant repacking rooms and GDP-validated labeling booths inside regional gateways improve turnaround for high-value clinical shipments. Specialized cleaning, blast-freezing, and ripening chambers allow fresh-produce exporters to meet retailer-specific shelf-life requirements. The convergence of e-commerce and courier segments sparks demand for pick-and-pack operations that support small-batch delivery, broadening the addressable base for third-party logistics providers in the ASEAN cold chain logistics market.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Temperature Type: Chilled Momentum Builds

Frozen storage held 41% of the ASEAN cold chain logistics market share in 2024, anchored by seafood, poultry, and prepared foods, which can remain in freezers for months without compromising safety. Investment focuses on high-density mobile racking and cascade refrigeration for energy efficiency. Still, chilled capacity expands faster at a 4.90% CAGR because supermarkets and meal-kit companies demand farm-fresh produce and ready-to-eat salads with tighter temperature tolerances. Operators retrofit facilities with humidity controls and ethylene scrubbers to extend produce freshness, reducing shrinkage for retailers.

Deep-frozen and ultra-low segments below −20°C show niche but accelerating uptake as mRNA vaccine deployment widens. Providers adopt phase-change packaging and active containers to maintain ultra-cold temperatures during intercontinental flights from Singapore’s airport pharma zone to end-sites across ASEAN. Ambient cross-dock rooms facilitate temperature transitions between modes without breaking cold integrity. Collectively, these innovations elevate the ASEAN cold chain logistics market size devoted to temperature-precision services and diversify revenue streams beyond commodity frozen warehousing.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Application: Traditional Proteins Meet Biologic Disruption

Meat & seafood still command the largest revenue slice, contributing USD 5.07 billion in 2024, reinforced by ASEAN’s status as a leading shrimp and chicken exporter. Supply chains integrate on-site blast-freezers and brine chillers at processing plants, and digital catch certificates help fishermen preserve export eligibility to the European Union. Nonetheless, vaccine and clinical-trial materials carve out the steepest 5.22% CAGR as regional pharma output scales. Ultra-cold depots in Penang Science Park and Singapore Tuas Biomedical Park receive biologic APIs that require 24-hour monitoring and redundant cooling.

Fruits & vegetables benefit from government post-harvest loss reduction programs that subsidize chilled trucks and pack-houses. Dairy and frozen desserts enjoy tailwinds from rising urban incomes and café culture. Ready-to-eat meals thrive on app-driven demand, stimulating investment in cook-chill kitchens inside multi-temperature facilities. Chemicals and specialty materials, although smaller, need strict humidity and temperature governance to prevent polymer degradation, reinforcing the versatility required of ASEAN cold chain logistics market participants.

Geography Analysis

Indonesia’s dominance arises from scale and archipelagic logistics complexity that require multimodal networks linking more than 17,000 islands; yet supply still lags demand, keeping utilization high and pricing firm. Warehousing clusters around Jakarta, Surabaya, and Makassar handle imported beef and domestic poultry surpluses, while coastal container ports add reefer plugs to support seafood exports. Government toll-road projects shorten transit times, although power reliability outside Java remains a persistent challenge within the ASEAN cold chain logistics market.

Thailand enjoys superior infrastructure maturity, enabling rapid deployment of temperature-controlled trucks that service agro-clusters in Chiang Mai and Nakhon Sawan before feeding Bangkok’s hypermarkets. The country also positions itself as a transshipment conduit, capitalizing on the ASEAN Single Window and bonded warehouses along the Eastern Economic Corridor that consolidate inbound pharma, dairy, and confectionery headed to CLMV markets. State-supported R&D on natural refrigerants facilitates lower lifecycle costs for new warehouses.

Vietnam leverages free-trade pacts to pull in seafood and electronics supply chains, bolstering demand for export-ready cold stores along the Hai Phong–Hanoi corridor. E-commerce is projected to hit USD 52 billion by 2025, intensifying last-mile chilled delivery requirements in Ho Chi Minh City. Singapore, despite land limits, commands premium yields thanks to GDP-certified clusters near Changi that secure multinational clinical-trial shipments. Malaysia’s halal compliance framework differentiates its cold chain services, while the Philippines’ island geography creates niche air-cargo opportunities albeit at higher cost structures.

Competitive Landscape

The ASEAN cold chain logistics market hosts a dynamic mix of global integrators, regional champions, and tech-enabled startups, leading to moderate fragmentation. DHL’s EUR 500 million (USD 551.82 million) Asia Pacific healthcare spend and its March 2025 acquisition of CRYOPDP underscore the strategic pivot toward pharma and biologics. UPS follows with a USD 250 million commitment, including a new Clark hub in the Philippines geared toward cold-chain parcels.

Regional specialists such as JWD Logistics and Royal Cargo invest in automated storage and retrieval systems to lock in anchor clients across meat, seafood, and vaccine verticals. Technology disruptors like Indonesia’s Paxel deploy cloud dashboards and AI routing engines to win same-day grocery contracts in Greater Jakarta. Strategic collaborations proliferate: YCH Group partners Vietnam Post to embed blockchain into SME logistics flows, illustrating how digital ecosystems grant smaller shippers end-to-end visibility.

Compliance-driven barriers raise entry costs, favoring incumbents with certified facilities. The ASEAN mutual recognition agreement on PIC/S GMP standards requires strict process documentation, directing pharma clients toward operators that can demonstrate audit readiness. ESG differentiation intensifies as investors ask for greenhouse-gas metrics before funding new builds. Lineage Logistics and Nichirei Logistics ramp up greenfield projects, leveraging global expertise in low-charge ammonia systems to edge out local rivals on energy efficiency.

ASEAN Cold Chain Logistics Industry Leaders

-

Nippon Express

-

Deutsche Post DHL

-

Yusen Logistics (Part of NYK Line)

-

DSV

-

United Parcel Service (UPS)

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- January 2025: Nippon Express opened the NX Tomakomai Hazardous Materials Logistics Park in Hokkaido, adding advanced temperature-controlled storage for semiconductor supply chains.

- April 2025: DHL announced a EUR 2 billion global health-logistics plan with EUR 500 million earmarked for Asia Pacific GDP-certified hubs.

- March 2025: DHL Group acquired CRYOPDP, adding 600,000 annual specialty health shipments to its network.

- December 2024: CH Group and Vietnam Post agreed to develop a blockchain-enabled digital logistics marketplace for SMEs.

ASEAN Cold Chain Logistics Market Report Scope

Cold chain refers to temperature-controlled logistics procedures. A complete background analysis of the ASEAN Cold Chain Logistics Market, including the assessment of the economy and contribution of sectors in the economy, market overview, market size estimation for key segments, and emerging trends in the market segments, market dynamics, and geographical trends, and COVID-19 impact is included in the report.

The ASEAN cold chain logistics market is segmented by service, temperature, and geography. By service, the market is segmented by storage, transportation, and value-added service. By temperature, the market is segmented into ambient, chilled, and frozen. By application, the market is segmented into horticulture, dairy products, meats and fish, processed food products, pharma, life sciences, chemicals, and other applications, and by geography, the market is segmented by Singapore, Thailand, Vietnam, Indonesia, Malaysia, Philippines and Rest of ASEAN.

The report offers market size and forecasts for the ASEAN cold chain logistics market in value (USD) for all the above segments.

By Service Type

| Refrigerated Storage | Public Warehousing |

| Private Warehousing | |

| Refrigerated Transportation | Road |

| Rail | |

| Sea | |

| Air | |

| Value-Added Services |

By Temperature Type

| Chilled (0-5°C) |

| Frozen (-18-0°C) |

| Ambient |

| Deep-Frozen/Ultra-Low (less than-20°C) |

By Application

| Fruits and Vegetables |

| Meat and Poultry |

| Fish and Seafood |

| Dairy and Frozen Desserts |

| Bakery and Confectionery |

| Ready-to-Eat Meals |

| Pharmaceuticals and Biologics |

| Vaccines and Clinical Trial Materials |

| Chemicals and Specialty Materials |

| Other Perishables |

By Geography

| Singapore |

| Thailand |

| Vietnam |

| Indonesia |

| Malaysia |

| Philippines |

| Rest of ASEAN |

| By Service Type | Refrigerated Storage | Public Warehousing |

| Private Warehousing | ||

| Refrigerated Transportation | Road | |

| Rail | ||

| Sea | ||

| Air | ||

| Value-Added Services | ||

| By Temperature Type | Chilled (0-5°C) | |

| Frozen (-18-0°C) | ||

| Ambient | ||

| Deep-Frozen/Ultra-Low (less than-20°C) | ||

| By Application | Fruits and Vegetables | |

| Meat and Poultry | ||

| Fish and Seafood | ||

| Dairy and Frozen Desserts | ||

| Bakery and Confectionery | ||

| Ready-to-Eat Meals | ||

| Pharmaceuticals and Biologics | ||

| Vaccines and Clinical Trial Materials | ||

| Chemicals and Specialty Materials | ||

| Other Perishables | ||

| By Geography | Singapore | |

| Thailand | ||

| Vietnam | ||

| Indonesia | ||

| Malaysia | ||

| Philippines | ||

| Rest of ASEAN | ||

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the 2025 value of the ASEAN cold chain logistics market?

It stands at USD 18.77 billion, with a forecast to reach USD 24.33 billion by 2030.

Which service type leads spending?

Refrigerated storage accounts for 52% of 2024 revenue, reflecting high demand for temperature-controlled warehousing.

Which country is the largest revenue contributor?

Indonesia holds 22% of total value thanks to extensive domestic demand and archipelago logistics complexity.

What application segment is growing fastest?

Vaccines and clinical-trial materials are expanding at a 5.22% CAGR as regional pharmaceutical capacity rises.

How is sustainability affecting cold-chain investment?

ESG-linked funding favors natural refrigerants and energy-efficient systems, lowering lifecycle costs and emissions.

What are the main barriers to wider cold-chain adoption?

Grid unreliability, high urban land prices, refrigerant phase-out costs, and shortages of IoT-skilled labor constrain expansion.

Page last updated on: