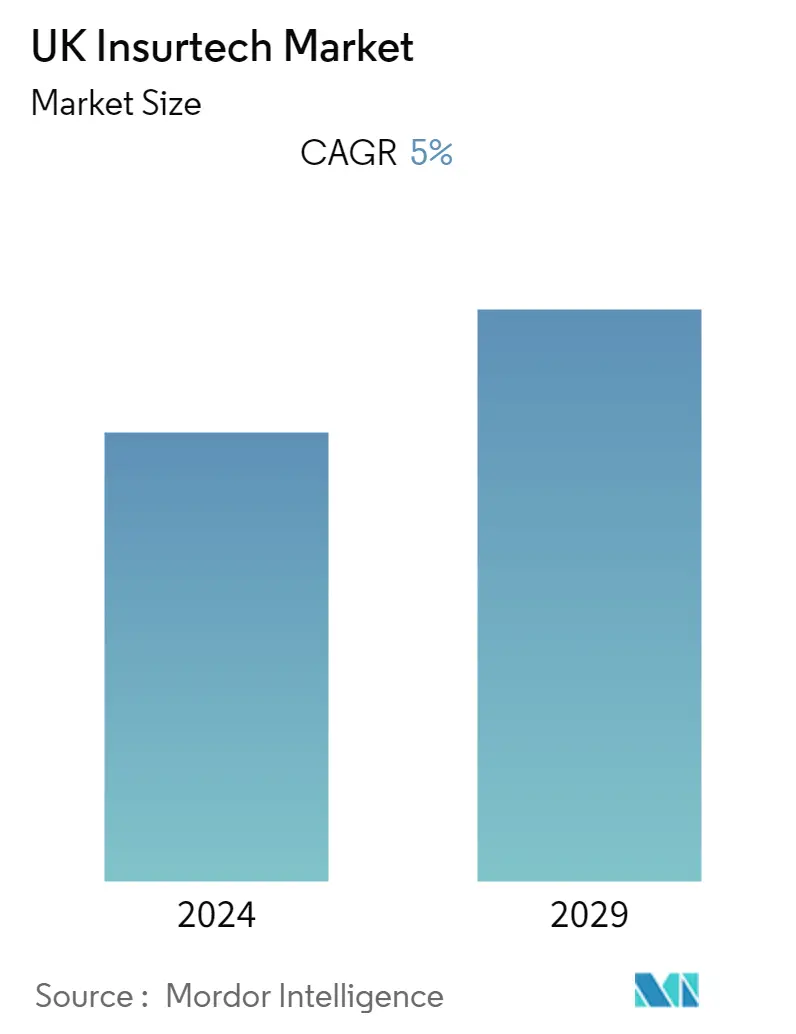

UK Insurtech Market Size

| Study Period | 2020 - 2029 |

| Base Year For Estimation | 2023 |

| Forecast Data Period | 2024 - 2029 |

| Historical Data Period | 2020 - 2022 |

| CAGR | 5.00 % |

| Market Concentration | High |

Major Players

*Disclaimer: Major Players sorted in no particular order |

UK Insurtech Market Analysis

The UK insurance industry is fundamentally changing. The UK general insurance market continues to be fiercely competitive but is troubled by sustained low profitability fueled by the predominance of online distribution channels. Insurers recognize that the everyday lives of their customers are being transformed by new technologies. They also recognize that this transformation is affecting their own industry, which is undergoing an ecosystem disruption caused by technology-driven new entrants and existing competitors alike. Insurers are thus facing increasing pressure to evolve and reinvent themselves before that disruption hits the bottom line.

Just as the banking industry is being revolutionized by FinTech companies, so the insurance industry is joining the digital revolution. For millennials and other customers who are now getting comfortable running their entire financial lives from their mobile devices, insurance represents just another component of their financial lives that can be handled on a phone, via an app. consumers now demand real-time engagement and online access to services managed across their mobile and personal devices. Insurers therefore need to embrace the transition from the traditional and rather dusty world of insurance to a new, comprehensive, fully integrated, digital ecosystem. The InsurTech industry looks to be here to stay. Young and agile startups will continue to make inroads into the mature UK insurance industry.

UK Insurtech Market Trends

This section covers the major market trends shaping the UK Insurtech Market according to our research experts:

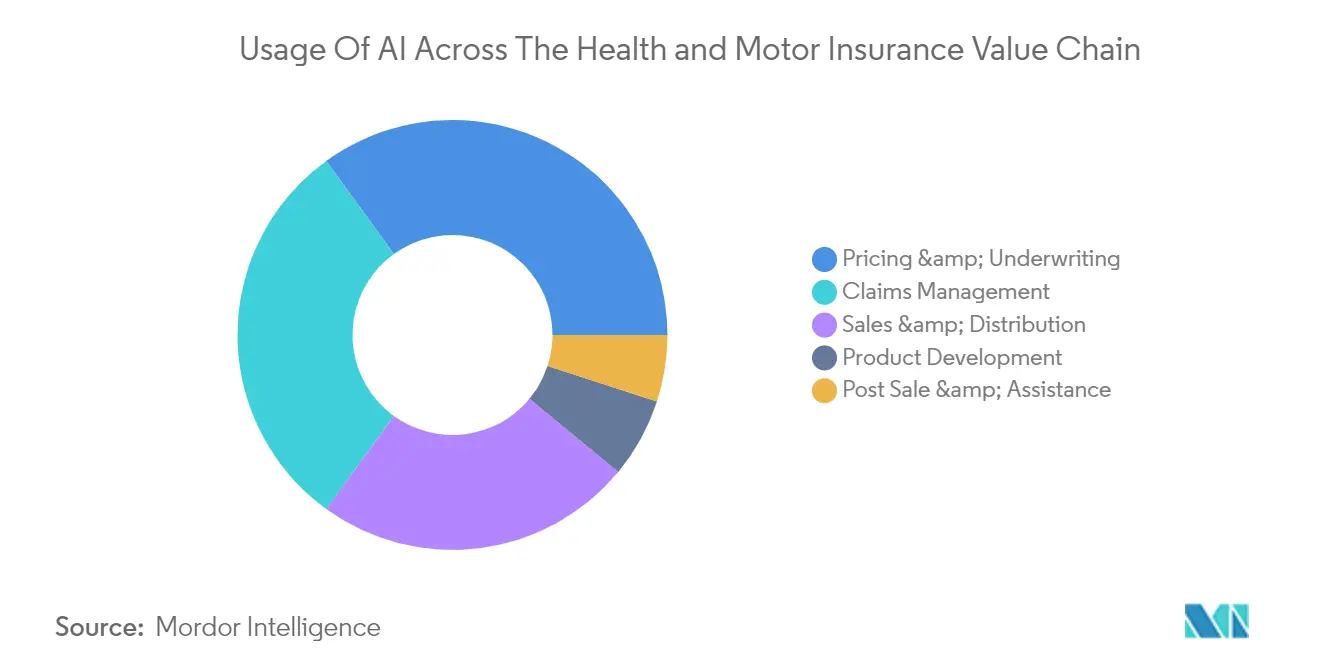

INSURTECHS FOCUS ON ANALYTICS / BIG DATA and AI

The emerging wave of 'Insurtech' solutions companies are seeking to transform the business of insurance through the introduction of Big Data, Machine Learning, and AI capabilities. When insurance providers tap into the vast repositories of Big Data that is available to them and combine this data with machine learning and AI capabilities, they can develop new policies that can reach new audiences.

According to various studies AI platform revenues within insurance would grow by 23% to $3.4 billion between 2019 and 2024. Most traditional insurance companies don't use a lot of data to create their products. They rely on demographic information that is 40 years old, and older. They are struggling to price policies correctly and many will miss out on huge financial opportunities. insurance companies must evolve to adapt to changing customer demographics and preferences.

Digital transformation of the insurance industry accelerated during the Covid-19 pandemic, as a growing number of consumers turned to digital channels to shop for insurance solutions. This prompted leading insurers to invigorate their digital transformation initiatives. New Insurtech companies help traditional insurers price products more competitively, deliver products that consumers want, and improve the efficiency and convenience of the insurance purchase process for both the consumer and for the insurance agent.

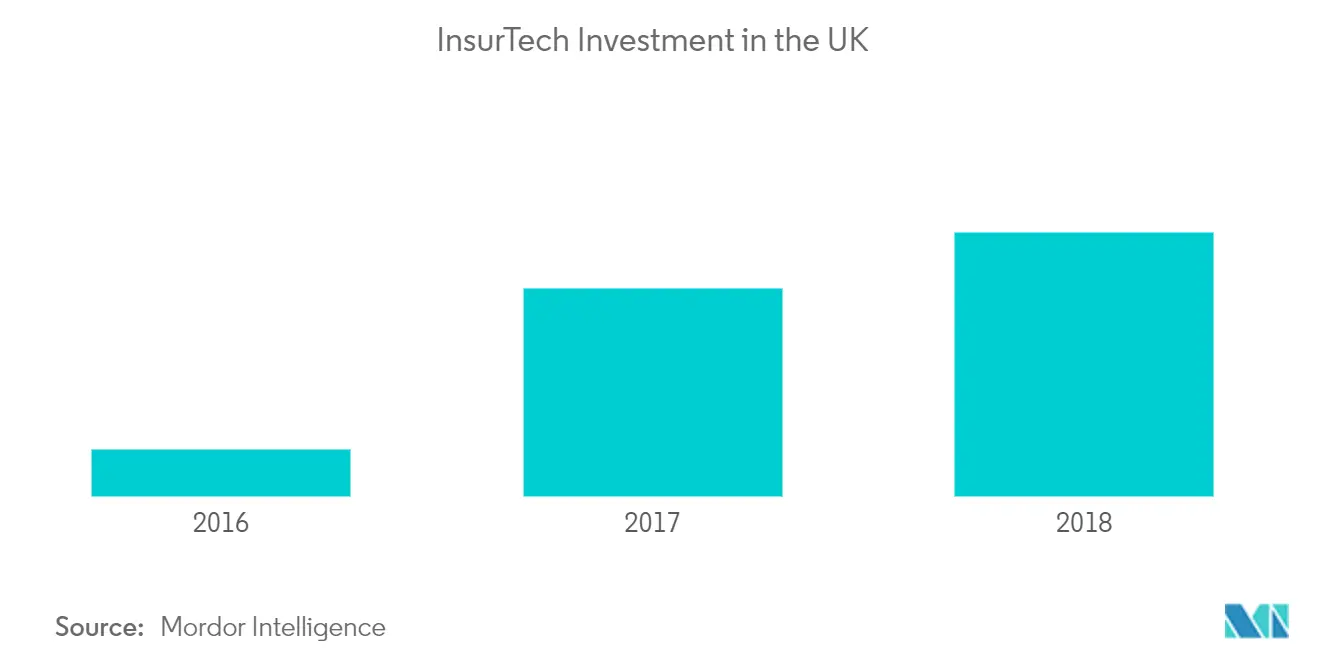

UK Insurtech VC Funding

COVID-19 pandemic shifts InsurTech investment priorities. The growing success of UK insurtechs has been largely attributed to the creative ways they address customers' insurance needs in an increasingly digital economy, opening up new opportunities across the whole of the insurance value chain. Insurtech is thriving in the UK, having spun out of the Fintech revolution and UK Insurtechs are providing solutions across the whole insurance market. This is enabling insurers and carriers to deliver innovative products that challenge the status quo of the incumbents, in personal lines, commercial insurance and for specialist markets.

In response to the growing desire amongst both insurtechs and insurance firms to foster stronger partnerships with one another, they now explore how insurance firms and insurtechs can best work together to foster real relationships and drive higher levels of innovation across the industry.

UK Insurtech Industry Overview

UK insurtech market is highly competitive, with the presence of both international and domestic players. The market studied presents opportunities for growth during the forecast period, which is expected to further drive the market competition. With multiple players holding significant shares, the market studied is competitive.

UK Insurtech Market Leaders

-

Gryphon Group Holdings

-

Zego

-

Bought By Many

-

Quantemplate

-

Trunomi

*Disclaimer: Major Players sorted in no particular order

UK Insurtech Market Report - Table of Contents

-

1. INTRODUCTION

-

1.1 Study Assumptions and market definition

-

1.2 Scope of the Study

-

-

2. RESEARCH METHODOLOGY

-

3. EXECUTIVE SUMMARY

-

4. MARKET DYNAMICS

-

4.1 Market Overview

-

4.1.1 Regulatory Framework in The Industry

-

4.1.2 Introduction of Various Technologies in InsurTech

-

4.1.2.1 Analytics / Big data

-

4.1.2.2 AI / Automation

-

4.1.2.3 IoT

-

4.1.2.4 Connected Insurance

-

-

4.1.3 Benefits of InsurTech

-

4.1.4 Brexit Impact on the InsurTech Sector

-

4.1.5 The Niche InsurTech markets

-

4.1.5.1 Appetite Solutions

-

4.1.5.2 Data Solutions

-

4.1.5.3 Payment solutions

-

4.1.5.4 Quoting Solutions

-

-

-

4.2 Market Drivers

-

4.2.1 Customer Acquisition

-

4.2.2 Customer Retention

-

4.2.3 Risk Assessment

-

4.2.4 Fraud Prevention and Detection

-

4.2.5 Others

-

-

4.3 Market Restraints

-

4.3.1 International jurisdiction

-

4.3.2 Privacy challenge

-

4.3.3 Regulation and Governance

-

4.3.4 Others

-

-

4.4 Value Chain / Supply Chain Analysis

-

4.5 Porters 5 Force Analysis

-

4.5.1 Threat of New Entrants

-

4.5.2 Bargaining Power of Buyers/Consumers

-

4.5.3 Bargaining Power of Suppliers

-

4.5.4 Threat of Substitute Products

-

4.5.5 Intensity of Competitive Rivalry

-

-

4.6 Impact of Covid 19 on the Industry

-

-

5. MARKET SEGMENTATION

-

5.1 By Insurance type

-

5.1.1 Life

-

5.1.2 Non-Life

-

5.1.2.1 Motor

-

5.1.2.2 House

-

5.1.2.3 Accident

-

5.1.2.4 Health

-

5.1.2.5 Others

-

-

-

-

6. COMPETITIVE LANDSCAPE

-

6.1 Market Concentration Overview

-

6.2 Company Profiles

-

6.2.1 Gryphon Group Holdings

-

6.2.2 Zego

-

6.2.3 Bought By Many

-

6.2.4 Quantemplate

-

6.2.5 Trunomi

-

6.2.6 Anorak Technologies

-

6.2.7 Wrisk

-

6.2.8 Cazana

-

6.2.9 Setoo

-

6.2.10 By Miles

-

6.2.11 Others

-

-

-

7. Future Of The Market

-

8. Disclaimer

UK Insurtech Industry Segmentation

The insurance sector is home to some of the largest areas ripe for disruption across the Financial Services industry in the coming years. With increasingly demanding consumers, struggling legacy systems, and growing amounts of data at their fingertips, technological advances are offering the insurance market the opportunity to transform the way they do business. The UK InsurTech Market is segmented by the type of Insurances Provided ( Life and non-life; Non-Life can be further segmented into Motor, House, Accident, Pet, Health and Others).

| By Insurance type | |||||||

| Life | |||||||

|

UK Insurtech Market Research FAQs

What is the current UK Insurtech Market size?

The UK Insurtech Market is projected to register a CAGR of 5% during the forecast period (2024-2029)

Who are the key players in UK Insurtech Market?

Gryphon Group Holdings, Zego, Bought By Many, Quantemplate and Trunomi are the major companies operating in the UK Insurtech Market.

What years does this UK Insurtech Market cover?

The report covers the UK Insurtech Market historical market size for years: 2020, 2021, 2022 and 2023. The report also forecasts the UK Insurtech Market size for years: 2024, 2025, 2026, 2027, 2028 and 2029.

Insurtech in UK Industry Report

Statistics for the 2024 Insurtech in UK market share, size and revenue growth rate, created by Mordor Intelligence™ Industry Reports. Insurtech in UK analysis includes a market forecast outlook to 2029 and historical overview. Get a sample of this industry analysis as a free report PDF download.

Insurtech Market in UK Report Snapshots