Optogenetics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

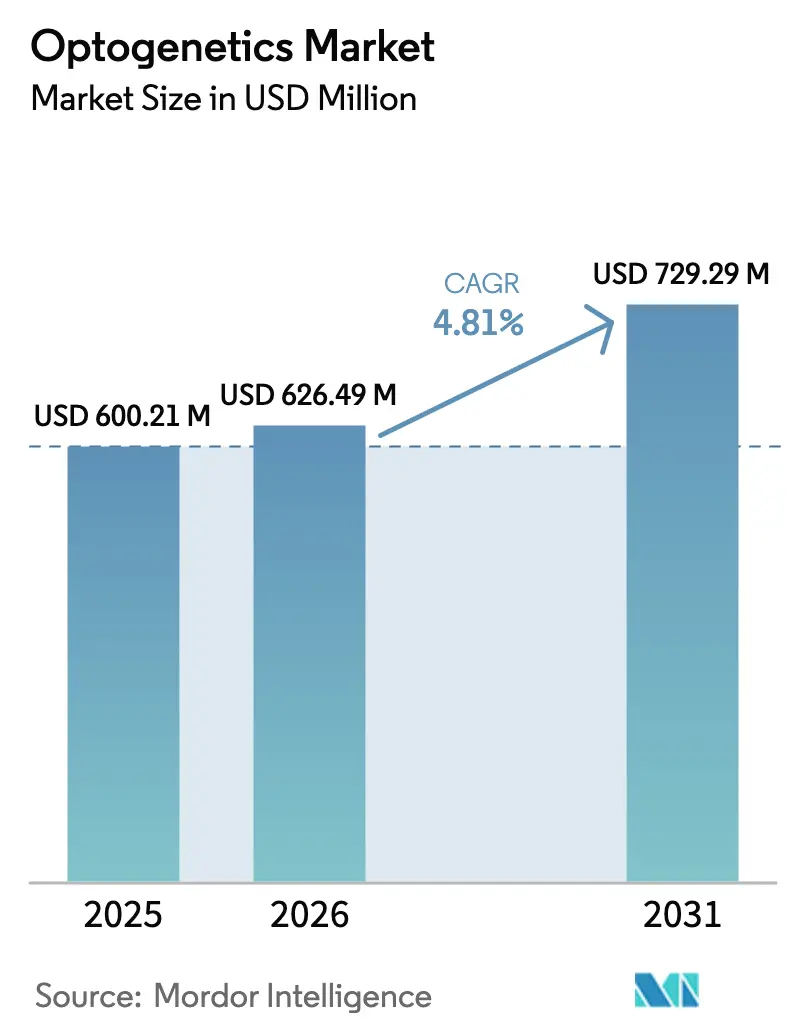

| Market Size (2026) | USD 626.49 Million |

| Market Size (2031) | USD 729.29 Million |

| Growth Rate (2026 - 2031) | 4.81% CAGR |

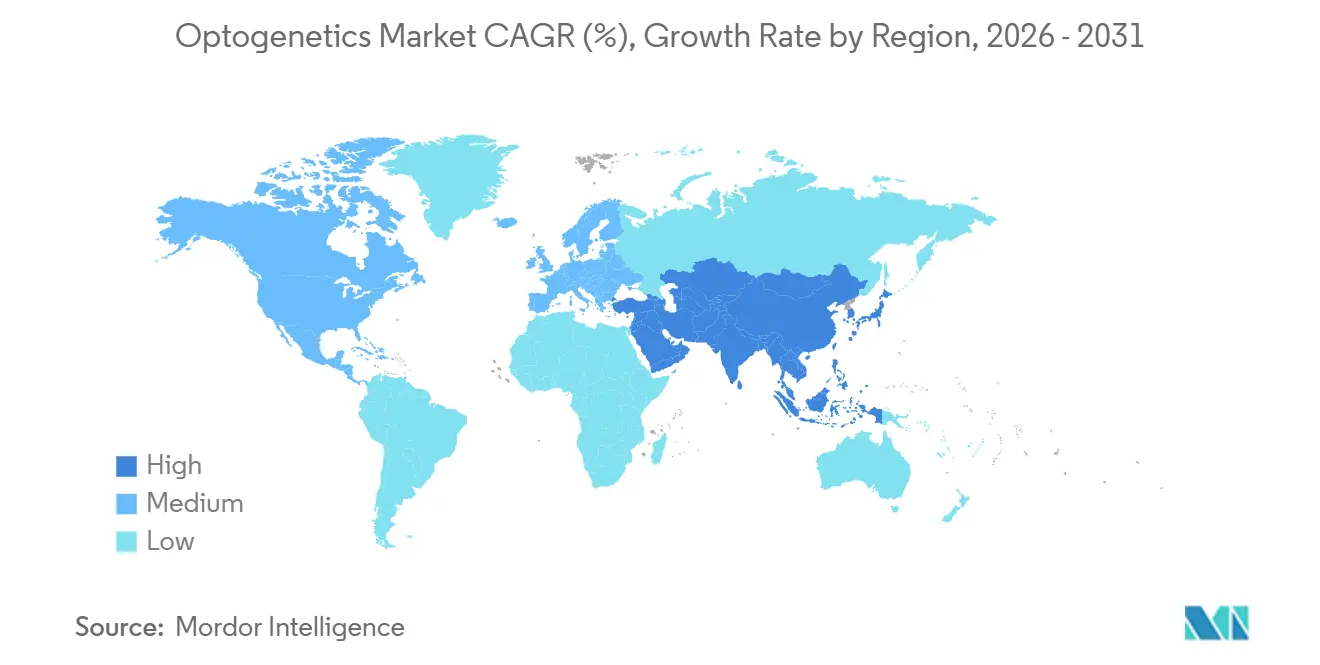

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

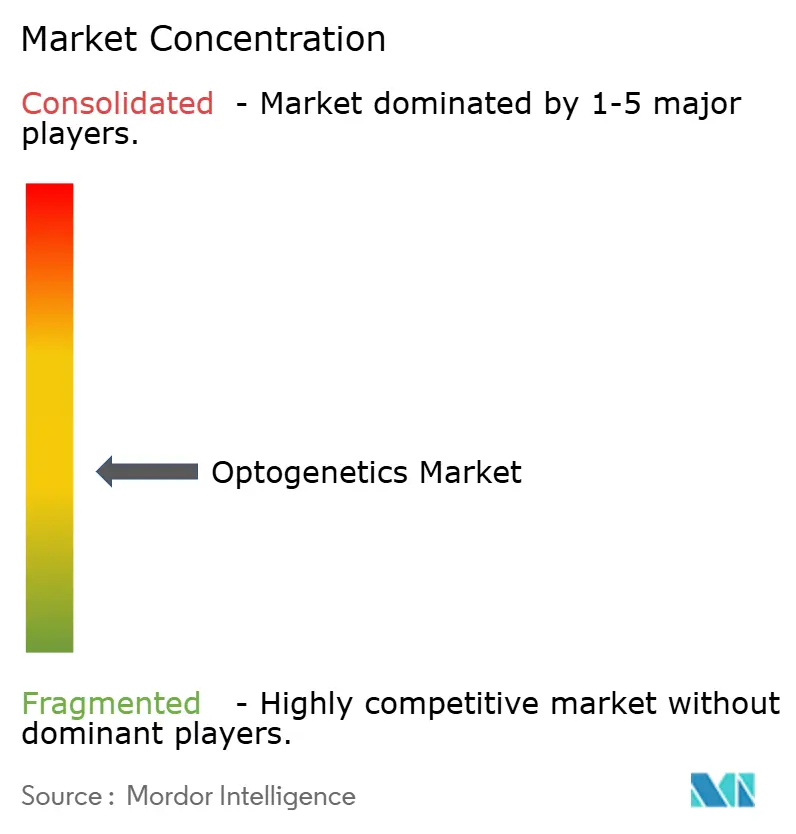

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Optogenetics Market Analysis by Mordor Intelligence

The Optogenetics Market size is expected to increase from USD 600.21 million in 2025 to USD 626.49 million in 2026 and reach USD 729.29 million by 2031, growing at a CAGR of 4.81% over 2026-2031.

Capital is shifting from pure discovery projects to late-stage vision-restoration pipelines as three investigational therapies received FDA Fast Track or Breakthrough Therapy status during 2024-2025, signaling that commercial viability is replacing proof-of-concept as the field’s primary yardstick. Hardware vendors are compressing form factors and prices to meet demand for closed-loop neuromodulation, while opsin engineers are advancing red-shifted variants that enable deeper tissue penetration without photothermal injury. Investors are betting on vertically integrated players that bundle light sources, vectors, and analytics software, a strategy that crowds out academic tool vendors yet accelerates translational timelines. Regulatory agencies across three continents now publish dedicated optogenetics guidance, reducing dossier duplication and cutting 6 months from the average IND-enabling program.

Key Report Takeaways

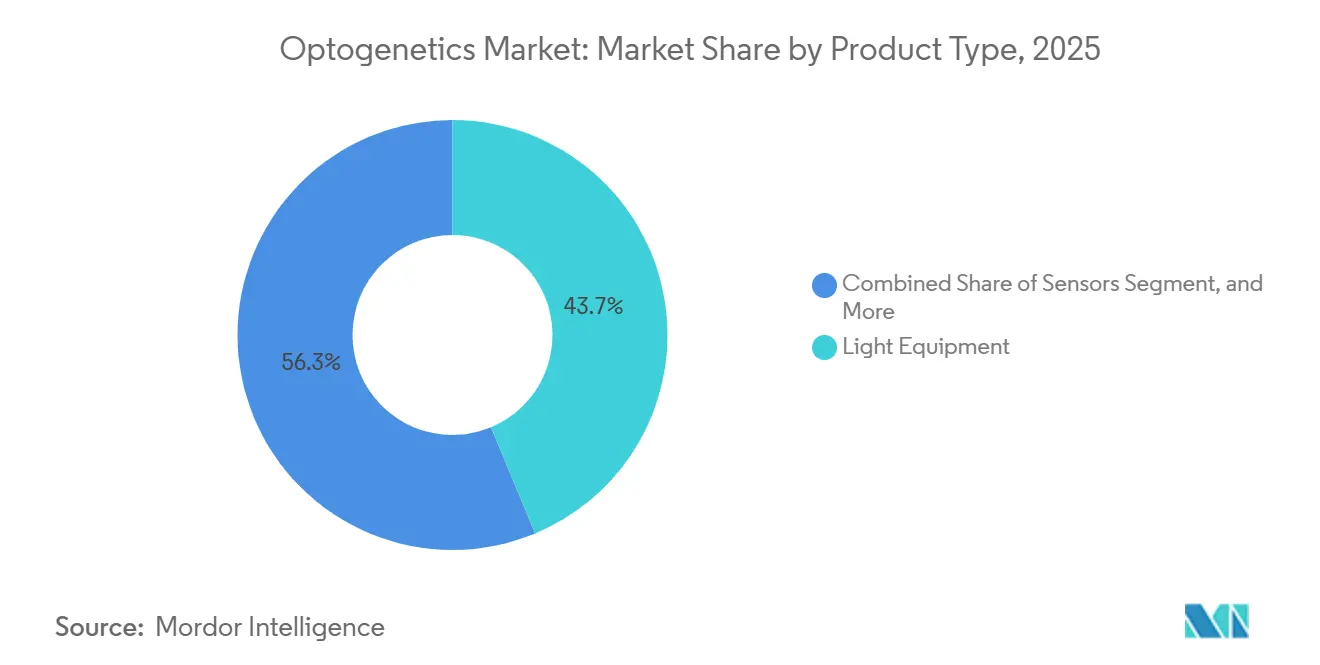

- By product type, light equipment led the optogenetics market with a 43.72% revenue share in 2025, while sensors are advancing at a 6.06% CAGR through 2031.

- By technique, viral vector delivery captured 31.27% of the optogenetics market size in 2025; non-viral and nanoparticle delivery is growing fastest at a 7.63% CAGR.

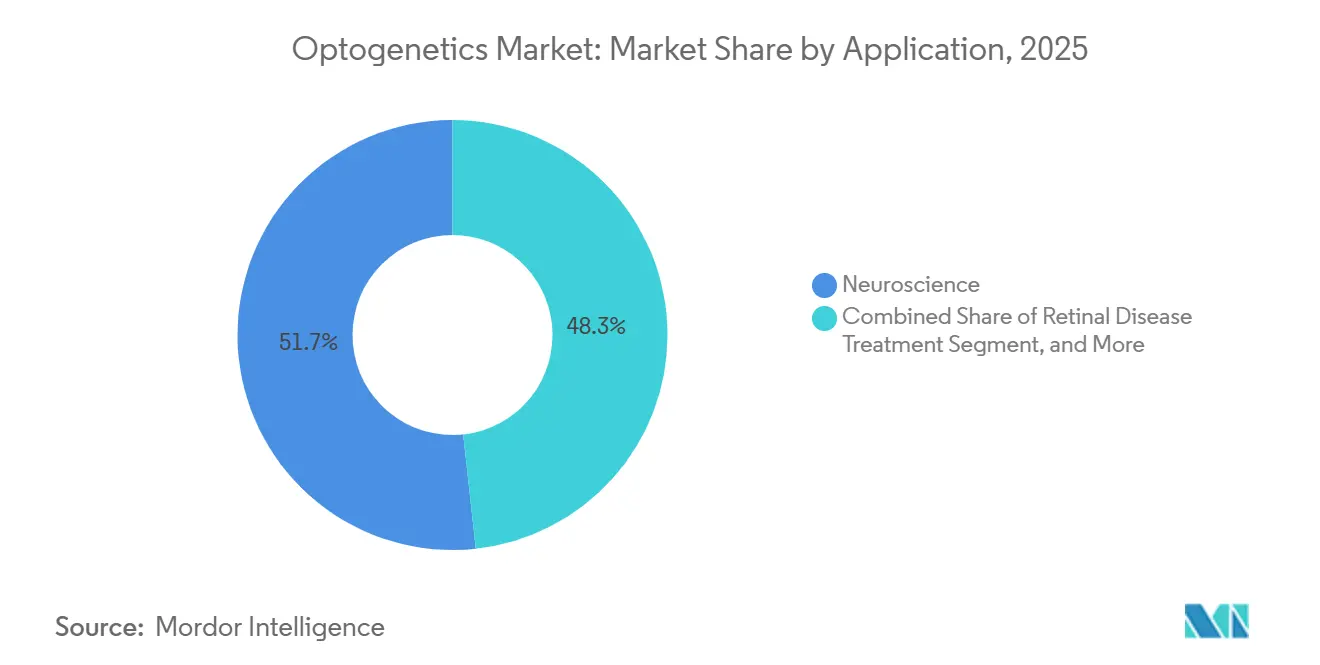

- By application, neuroscience accounted for 51.72% of the optogenetics market share in 2025, but retinal disease treatment is projected to record the highest 8.18% CAGR to 2031.

- By end user, academic and research institutes accounted for 57.78% of 2025 spending, yet biotech and pharmaceutical companies are scaling at a 9.41% CAGR.

- By geography, North America accounted for 41.08% of 2025 revenue, while Asia-Pacific is on track for the fastest expansion at a 10.27% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Optogenetics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Neuroscience Research Funding & BRAIN Initiative | +0.9% | North America, Europe, with spillover to Asia-Pacific academic hubs | Medium term (2-4 years) |

| Growing Prevalence of Neurological & Retinal Disorders | +1.2% | Global, with acute burden in aging populations of North America, Europe, Japan | Long term (≥4 years) |

| Advances in Opsins, Viral Vectors & Mini-LED/Laser Hardware | +1.5% | Global, led by North America and Europe R&D centers | Medium term (2-4 years) |

| Surge in Vision-Restoration Clinical Trials | +1.1% | North America, Europe, with emerging activity in China | Short term (≤2 years) |

| AI-Enabled Closed-Loop Neuromodulation Platforms | +0.7% | North America, Europe, with early adoption in Japan and South Korea | Medium term (2-4 years) |

| Reshoring of Optical-Component Supply Chains | +0.5% | North America, Europe, driven by CHIPS Act and strategic autonomy policies | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Rising Neuroscience Research Funding & BRAIN Initiative

United States federal appropriations fell from USD 680 million in 2023 to USD 321 million in 2025, yet the budget now prioritizes optogenetic tools with direct clinical endpoints.[1]National Institutes of Health, “BRAIN Initiative Funding,” nih.gov The BICAN atlas program alone awarded USD 126 million in 2024 to projects that tag brain-cell types with opsins, creating data sets already licensed by tool makers for assay validation. Europe’s Human Brain Project committed EUR 89 million (USD 97 million) in 2025 to platforms that integrate optogenetic readouts with electronic health records, while Japan’s Brain/MINDS 2.0 put JPY 15 billion (USD 102 million) toward marmoset disease models, positioning regional CROs for outsourced studies. The redirection of grants toward translational milestones favors companies able to supply hardware, vectors, and software as unified packages rather than à-la-carte components. This grant landscape strengthens the optogenetics market by underwriting both early discovery and preclinical validation phases.

Growing Prevalence of Neurological & Retinal Disorders

Age-related retinal degeneration and inherited retinal dystrophies affected 285 million individuals in 2025, with incidence climbing 3.2% annually.[2]WHO, “World Vision Impairment Data,” who.int Approximately 40% of legally blind patients in high-income nations are ineligible for cell transplants or electronic implants, leaving optogenetic therapy as a prime alternative. Parkinson’s disease cases reached 8.5 million in 2024, and preclinical optogenetic stimulation shows promise for cell-type-specific modulation without permanent electrodes. Epilepsy affects 50 million people globally, and a 2025 rodent trial reported a 62% drop in convulsions after closed-loop optogenetic inhibition. Demand therefore rises for scalable vectors, miniaturized light sources, and analytics platforms capable of chronic, cell-specific intervention.

Advances in Opsins, Viral Vectors & Mini-LED/Laser Hardware

Red-shifted channelrhodopsins such as ChRmine extend controllable depth beyond 3 mm, a 50% gain over earlier blue-light tools. Addgene shipped 12,400 optogenetic plasmids in 2024, of which 38% contained red-shifted constructs, indicating a clear preference for deeper penetration.[3]Addgene, “Plasmid Distribution Statistics,” addgene.org Novel AAV capsids now achieve 10-fold higher retinal ganglion-cell transduction, reducing vector doses and per-patient manufacturing costs by USD 18,000. Inscopix commercialized a 16-channel wireless micro-LED array in 2025, removing fiber-optic tethers that previously constrained animal movement studies. Simultaneously, laser-diode miniaturization lowered module volume to 8 × 8 × 15 mm, allowing fully implantable cardiac pacemakers in porcine trials.

Surge in Vision-Restoration Clinical Trials

Between 2024 and 2025, four retinal gene-therapy programs enrolled 412 patients, a 3.4-fold rise over 2020-2023. Nanoscope’s MCO-010 met its Phase 2b endpoint when 55% of retinitis pigmentosa patients gained ≥15 letters on the ETDRS chart. GenSight’s GS030 achieved object-localization gains in 63% of participants, leveraging goggles that convert images into amber light for ChR-activation. Bionic Sight’s BS01 received FDA Fast Track in 2024, while Ray Therapeutics inaugurated a first-in-human trial for RAY-01 in 2025. Collectively, these milestones signal investor confidence that optogenetic vision restoration will mature into a commercial category by decade’s end.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Capital Cost of Lasers & GMP Viral-Vector Manufacture | -0.8% | Global, with acute impact on emerging markets lacking subsidized infrastructure | Long term (≥4 years) |

| Gene-Therapy Regulatory Stringency & Long Timelines | -0.6% | North America, Europe, with gradual harmonization in Asia-Pacific | Medium term (2-4 years) |

| Photothermal Safety Limits for Red-Shifted Actuators | -0.3% | Global, particularly affecting deep-tissue and chronic stimulation applications | Medium term (2-4 years) |

| Talent Drain of Advanced Microscopists to Other Photonics Sectors | -0.4% | North America, Europe, with emerging impact in China and Japan | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

High Capital Cost of Lasers & GMP Viral-Vector Manufacture

Building a 200 L GMP viral-vector plant can cost USD 45-65 million, a barrier that bars most academic spin-outs from vertical integration. Multi-wavelength laser systems run USD 80,000-150,000, and full behavioral setups can exceed USD 500,000, limiting adoption in budget-constrained settings. Contract manufacturers charge USD 250,000-400,000 per AAV batch, so Phase 1/2 ophthalmology trials often front-load USD 1.2 million in vector costs before dosing begins. Emerging markets must also absorb import tariffs and regulatory delays that tack on 12-18% to hardware prices and extend lab commissioning by 2 years. These factors collectively dampen uptake in developing regions.

Gene-Therapy Regulatory Stringency & Long Timelines

FDA guidance issued in 2024 demands 12-month toxicology in two species plus biodistribution across three ocular tissues, extending IND packages to 24 months and adding USD 3-5 million per program. The European Medicines Agency now requires large-animal proof-of-concept before orphan-drug status, delaying GenSight’s European filing by nine months. Post-approval, mandatory five-year patient monitoring costs USD 12,000-18,000 per subject, squeezing reimbursement margins. Japan’s SAKIGAKE pathway trims formal review yet obligates sponsors to gather real-world data from 200 patients within seven years, a heavy lift for seed-stage firms. China’s ten-year post-marketing registry adds quarterly surveillance, lifting life-cycle costs by 22%.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Sensors Gain Ground on Closed-Loop Demand

Light Equipment maintained a 43.72% stake in 2025, as fiber-coupled LEDs and laser diodes remained lab staples, even as average selling prices slid 6% amid new Chinese entrants. Actuators, including ChRmine and Chrimson, benefited from deeper penetration requirements, expanding shipments by 22% in 2024, according to Addgene.

Sensors are outpacing all other categories at a 6.06% CAGR. The FDA classified closed-loop neuromodulation as Class III in 2024, but it also issued a streamlined combination-product path that catalyzed demand for calcium and voltage sensors tethered to real-time processors. Inscopix’s nVoke couples a 1.2-g miniscope with on-board GPUs, enabling adaptive experiments that are impossible with legacy open-loop rigs. As these systems proliferate, component suppliers are integrating embedded AI to automate feedback, a feature that strengthens the optogenetics market’s long-term stickiness among drug-discovery teams.

By Technique: Non-Viral Methods Challenge AAV Dominance

AAV-based Viral Vector Delivery held 31.27% of 2025 revenues, buoyed by three FDA-approved retinal gene therapies that validate the platform. Emerging serotypes with 10-fold retinal transduction enable dose cuts and reduce per-patient COGS by USD 18,000.

Non-viral and Nanoparticle Delivery is expanding at a 7.63% CAGR, eclipsing transgenic-animal workflows as ultrasound and lipid nanoparticles bypass AAV’s 4.7 kb limit and immune responses. A 2024 Nature Biomedical Engineering paper reported 42% cortical-neuron transfection with a 9 kb construct using focused ultrasound, a feat unattainable with standard vectors. Given the FDA’s 2024 clinical hold on an AAV-retinal trial due to inflammation, labs are pivoting to nanoparticle kits that pair well with rapid mRNA expression and transient safety profiles.

By Application: Retinal Disease Outpaces Neuroscience Growth

Neuroscience still accounted for 51.72% of 2025 revenue, supported by 11 NIH-subsidized core facilities that link viral-vector supply with microscopy training. Behavioral tracking platforms such as Noldus EthoVision now leverage machine-learning classifiers to correlate locomotion with real-time optogenetic perturbations across 340 labs worldwide.

Retinal Disease Treatment is advancing at the fastest pace, with an 8.18% CAGR. The addressable cohort comprises RP or geographic-atrophy patients with intact inner retina, totaling 1.2 million in the U.S. and EU, and economic models show willingness-to-pay up to USD 600,000 per treatment. GenSight’s PIONEER topline, released in 2024, demonstrated meaningful function in 63% of subjects wearing image-converting goggles, a dataset expected to anchor 2025 BLA filings. Positive momentum here lifts the overall optogenetics market size by seeding high-value procedures reimbursed under gene-therapy frameworks.

By End User: Biotech Firms Accelerate Adoption

Academic and research institutes spent 57.78% of their budgets in 2025, thanks to USD 1.8 billion in public grants spanning the NIH, ERC, and national brain programs. Mandatory construct-sharing within six months of publication generates network effects that drive broader uptake.

Biotech and Pharmaceutical Companies constitute the fastest-growing cohort, with a 9.41% CAGR. Danaher’s 2024 acquisition of Inscopix folds mini-scopes into multimodal screening suites, while Merck KGaA’s 2025 Addgene collaboration aims to halve GPCR assay timelines. Circuit Therapeutics raised USD 45 million to pilot optogenetic pain management, the first non-sensory clinical application of the technology. Consequently, the optogenetics market share attributed to industry users will rise steadily as pharma integrates opsin-based readouts into mainstream pipelines.

Geography Analysis

North America accounted for 41.08% of 2025 revenue, buoyed by NIH’s USD 321 million BRAIN budget and an extensive roster of CDMOs capable of delivering research-grade AAV in 12 weeks. Eighteen of 28 active optogenetic trials are conducted under the FDA’s 2024 streamlined ocular-gene guidance, underscoring U.S. primacy in first-in-human studies. Canada’s CAD 22 million (USD 16 million) CIHR program accelerates the development of closed-loop epilepsy devices, while concurrent filings with Health Canada and the FDA trim four months off regulatory timelines.

Europe benefits from harmonized 2024 EU guidance that cuts IND-enabling costs by 18% and allows one dossier for multi-country trials. Germany leads hardware exports, shipping 4,200 LED modules in 2024, a 16% jump over 2023. The UK Dementia Research Institute invested GBP 18 million in optogenetic Alzheimer's disease projects, leveraging subsidized GMP capacity at national therapy centers. France’s GenSight generated EUR 42 million in 2024 revenue on milestone payments, spotlighting therapeutic traction in the region.

Asia-Pacific is the velocity leader at 10.27% CAGR. China’s CNY 2.1 billion (USD 290 million) brain-mapping fund mandates optogenetic validation, creating guaranteed domestic demand. Japan’s Brain/MINDS 2.0 and SAKIGAKE fast tracks shave four years off conventional approval cycles, attracting Western sponsors to local CROs. South Korea’s USD 28 million national optogenetics center focuses on psychiatric disorders, while India and Australia channel smaller but strategic grants into low-cost hardware and pain-addiction research.

Middle East & Africa and South America remain nascent. Qatar’s USD 3.2 million allocation and South Africa’s USD 1.8 million lab signal early-stage capacity building, but FAPESP’s 30% cost-share cap forces Brazilian investigators to outsource vector work offshore, elongating lead times by 18 months.

Competitive Landscape

The optogenetics market is moderately fragmented as hardware, vector, and therapeutic niches converge. Thorlabs and Doric Lenses vie for module miniaturization; Thorlabs’ 8 × 8 × 15 mm blue-laser debut in 2024 trimmed the implant footprint by 40%, spurring wireless cardiac-pacing prototypes. Addgene’s 12,400-plasmid volume grants near-monopoly status, yet VectorBuilder’s three-week custom-cloning service is gaining footholds among time-sensitive biotech programs.

Therapeutic developers GenSight, Nanoscope, and Bionic Sight are locked in a race to file the first optogenetic BLA. GenSight’s 2024 PIONEER data became the clinical bar, pushing peers to pursue differentiated goggles or capsids. Inscopix’s nVoke platform is the only commercial closed-loop system, but its USD 180,000 price tag leaves room for mid-priced challengers. Patent intensity jumped 27% in 2024, with 142 USPTO grants covering red-shifted opsins, wireless LED arrays, and feedback algorithms, underscoring sustained innovation.

Compliance is emerging as a moat: six hardware vendors attained ISO 13485 certification during 2024-2025, qualifying them for clinical-trial supply contracts that demand audited manufacturing flows. Overall, strategic alliances between tool makers and therapeutics companies are narrowing gaps along the value chain and accelerating the development of end-to-end solutions.

Optogenetics Industry Leaders

Laserglow Technologies

Coherent Inc.

Thorlabs Inc.

Noldus Information Technology

GenSight Biologics S.A.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: GenSight Biologics announced a milestone in its Catalent partnership, adding commercial-scale vector capacity for European launches

- April 2025: Bruker released the 2-gram nVista 2P miniature microscope, enabling deep-brain imaging in freely moving animals

Global Optogenetics Market Report Scope

As per the report's scope, optogenetics refers to a range of optical techniques used to elicit a physiological response in targeted biological systems without pharmacological or electrical stimulation. Optogenetics controls neural activity by combining genetic engineering and optical tools. It is widely used in neuroscience for modulating neural circuits with high precision and specificity.

The Optogenetics Market Report is Segmented by Product Type (Light Equipment, Actuators, Sensors), Technique (Viral Vector Delivery, Transgenic Animals & Cre-dependent Systems, Non-viral & Nanoparticle Delivery), Application (Neuroscience, Retinal Disease Treatment, Behavioral Tracking, Cardiovascular & Pacing), End User (Academic & Research Institutes, Biotech & Pharmaceutical Companies, Contract Research Organizations, Hospitals & Clinics), and Geography (North America, Europe, Asia-Pacific, Middle East & Africa, South America). The Market Forecasts are Provided in Terms of Value (USD).

| Light Equipment |

| Actuators |

| Sensors |

| Viral Vector Delivery |

| Transgenic Animals & Cre-dependent Systems |

| Non-viral & Nanoparticle Delivery |

| Neuroscience |

| Retinal Disease Treatment |

| Behavioral Tracking |

| Cardiovascular & Pacing |

| Academic & Research Institutes |

| Biotech & Pharmaceutical Companies |

| Contract Research Organizations |

| Hospitals & Clinics |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Light Equipment | |

| Actuators | ||

| Sensors | ||

| By Technique | Viral Vector Delivery | |

| Transgenic Animals & Cre-dependent Systems | ||

| Non-viral & Nanoparticle Delivery | ||

| By Application | Neuroscience | |

| Retinal Disease Treatment | ||

| Behavioral Tracking | ||

| Cardiovascular & Pacing | ||

| By End User | Academic & Research Institutes | |

| Biotech & Pharmaceutical Companies | ||

| Contract Research Organizations | ||

| Hospitals & Clinics | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the projected value of the optogenetics market in 2031?

It is forecast to reach USD 0.79 billion by 2031, growing at a 4.81% CAGR from 2026-2031.

Which product category is expanding fastest within optogenetics?

Sensors are rising at a 6.06% CAGR due to demand for closed-loop neuromodulation platforms that integrate real-time imaging and AI-driven feedback.

Why is Asia-Pacific registering the highest growth rate?

Large public neuroscience funds in China and Japan, coupled with accelerated regulatory pathways such as SAKIGAKE, are driving a 10.27% CAGR for the region.

What restrains wider adoption of optogenetic therapies?

High capital outlays for GMP viral-vector plants and stringent gene-therapy regulations lengthen timelines and inflate costs, curbing uptake in resource-limited geographies.

Which clinical application shows the greatest commercial momentum?

Retinal Disease Treatment leads with an 8.18% CAGR, propelled by positive Phase 2 data and multiple FDA Fast Track designations for vision-restoration candidates.

Page last updated on: