North America Pedestrian Detection Systems Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Base Year For Estimation | 2025 |

| Forecast Data Period | 2026 - 2031 |

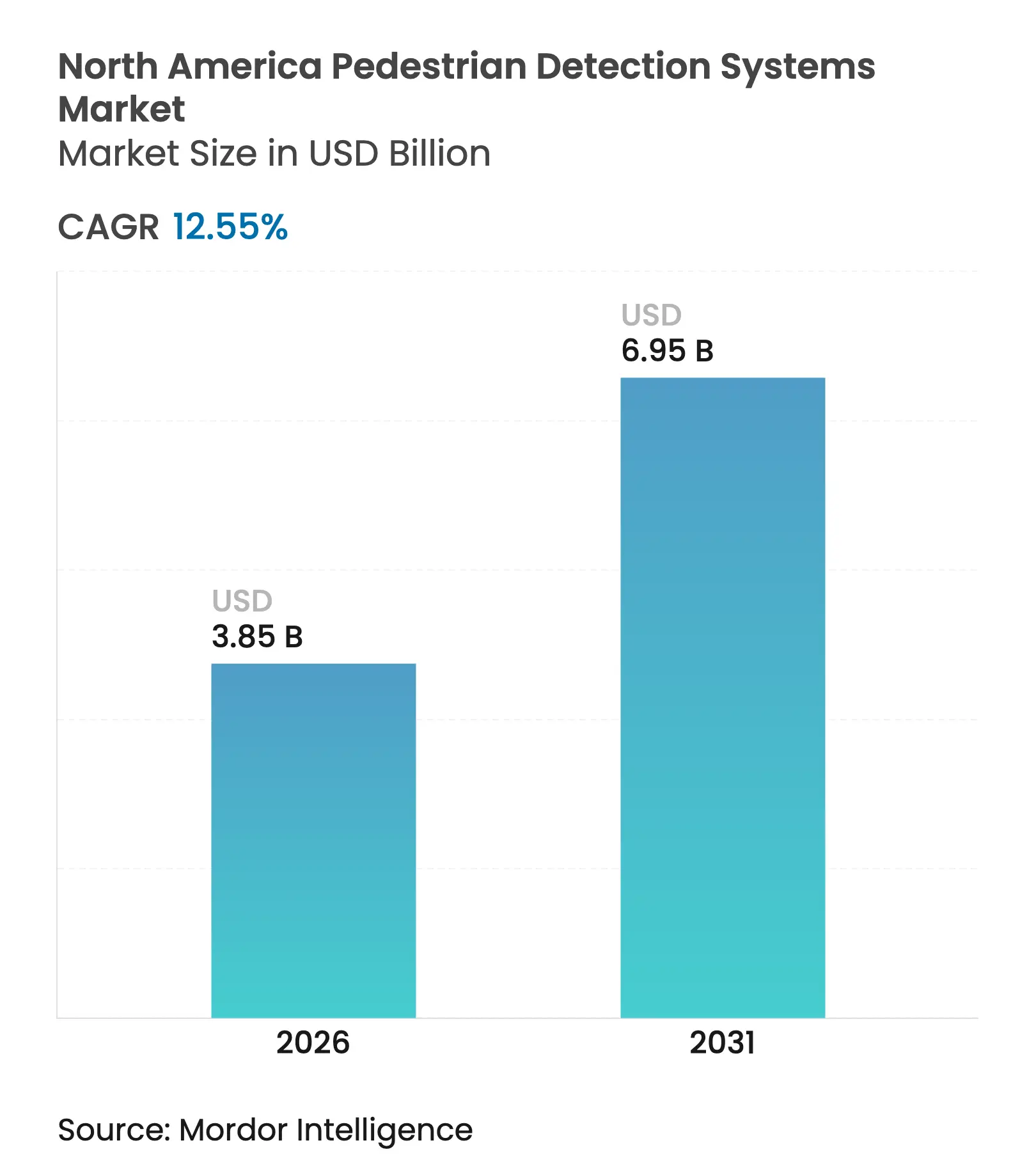

| Market Size (2026) | USD 3.85 Billion |

| Market Size (2031) | USD 6.95 Billion |

| Growth Rate (2026 - 2031) | 12.55 % CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

North America Pedestrian Detection Systems Market Analysis by Mordor Intelligence

The North America pedestrian detection systems market size was valued at USD 3.42 billion in 2025 and estimated to grow from USD 3.85 billion in 2026 to reach USD 6.95 billion by 2031, at a CAGR of 12.55% during the forecast period (2026-2031). Tightening federal safety mandates, persistent growth in pedestrian fatalities, and rapid ADAS integration across mainstream vehicle lines anchor this expansion. NHTSA’s Federal Motor Vehicle Safety Standard 127, which takes full effect in September 2029, obliges every light vehicle to carry automatic emergency braking with pedestrian detection that must work in daylight and darkness at speeds up to 62 mph.

Key Report Takeaways

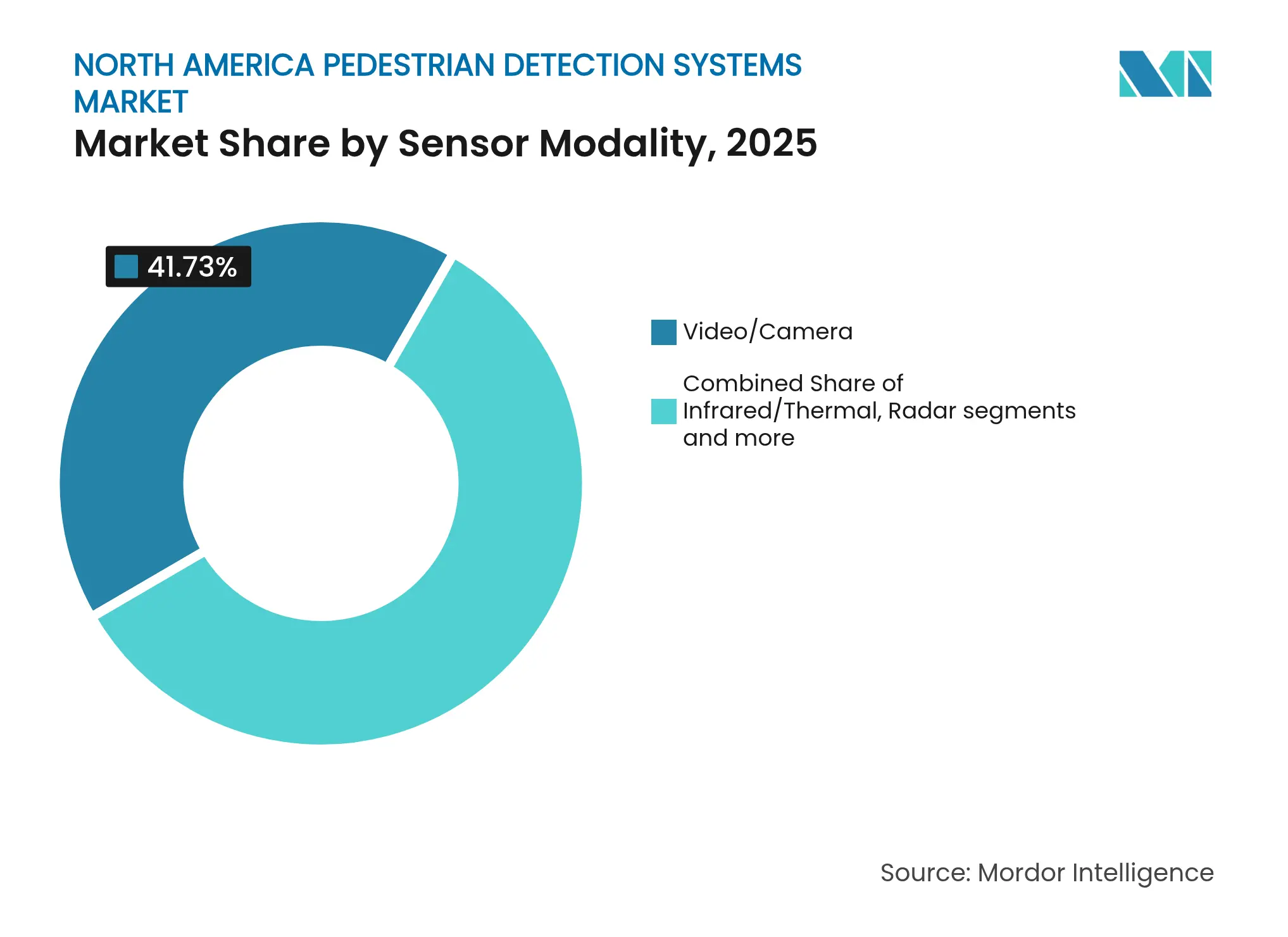

- By sensor modality, video/camera technology led with 41.73% revenue share in 2025; LiDAR is projected to register the fastest 20.68% CAGR to 2031.

- By vehicle type, passenger cars captured 61.55% of the North America pedestrian detection systems market share in 2025, while electric vehicles are expected to post the highest 17.96% CAGR through 2031.

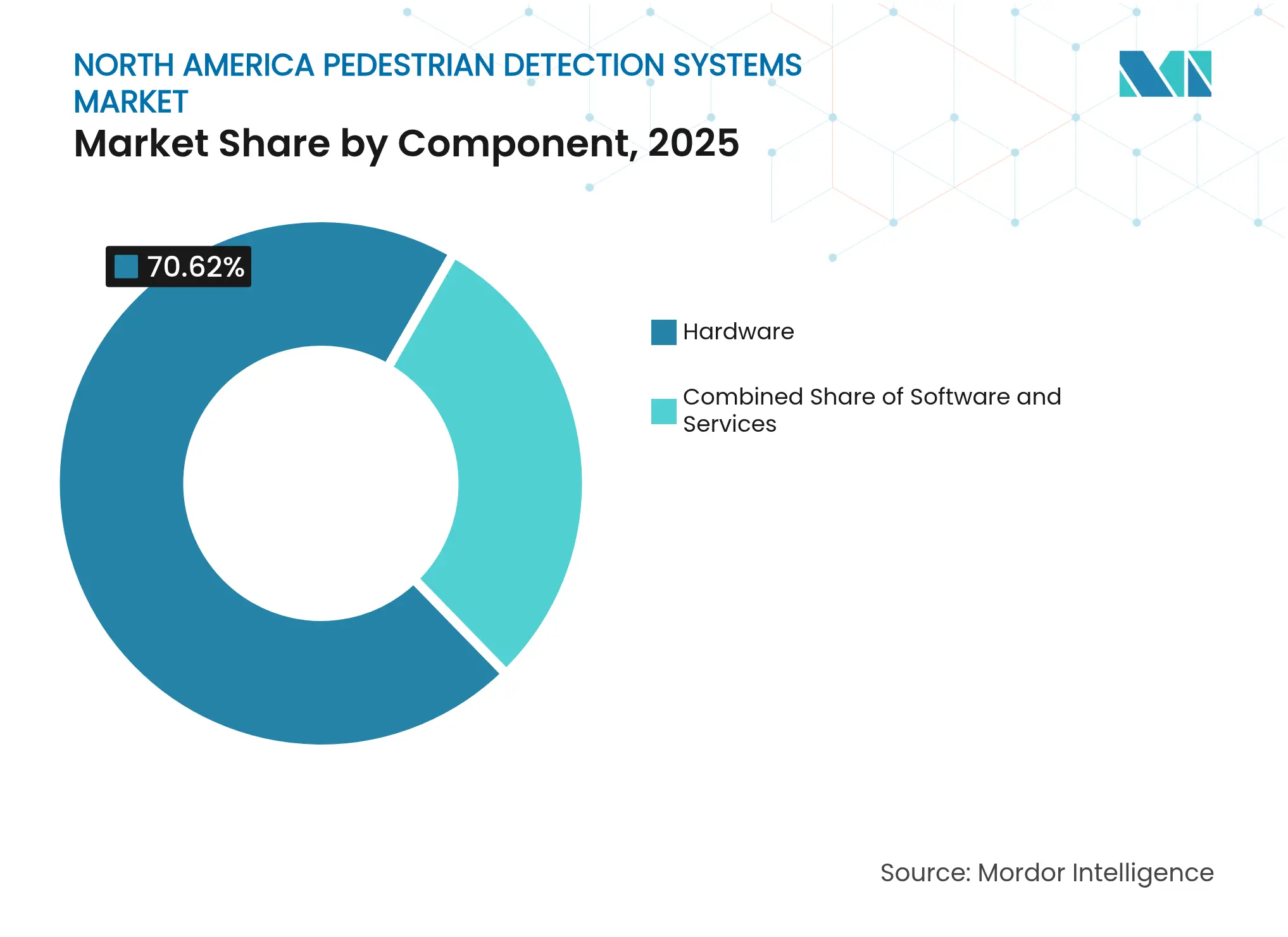

- By component, hardware accounted for 70.62% of the North American pedestrian detection systems market size in 2025; software is forecast to expand at 20.95% CAGR over the same horizon.

- By sales channel, OEM-fitted systems held 85.52% of 2025 revenue, whereas the aftermarket is on track for a 14.23% CAGR to 2031.

- By country, the United States commanded 78.35% of regional demand in 2025, and Canada is anticipated to rise at a 13.02% CAGR through 2031.

North America Pedestrian Detection Systems Market Trends and Insights

*Drivers Impact Analysis

| Driver | Qualitative Impact | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | ||||

|---|---|---|---|---|---|---|---|---|

Growing pedestrian-safety regulations Growing pedestrian-safety regulations | Strong | +3.2% | North America-wide, strongest in US | Medium term (2-4 years) | Qualitative Impact:Strong | (~) % Impact on CAGR Forecast:+3.2% | Geographic Relevance:North America-wide, strongest in US | Impact Timeline:Medium term (2-4 years) |

Rising pedestrian fatalities & ADAS demand Rising pedestrian fatalities & ADAS demand | Strong | +2.8% | US and Canada, urban concentrations | Short term (≤ 2 years) | ||||

Expansion of Level-2/3 autonomy in passenger cars Expansion of Level-2/3 autonomy in passenger cars | Moderate | +2.1% | US leading, Canada following | Medium term (2-4 years) | ||||

Rapid camera & SoC cost decline Rapid camera & SoC cost decline | Moderate | +1.9% | Global impact, North America adoption | Long term (≥ 4 years) | ||||

Insurance premium discounts for vehicles with certified PDS Insurance premium discounts for vehicles with certified PDS | Weak | +1.4% | US and Canada markets | Short term (≤ 2 years) | ||||

Fleet electrification needing enhanced safety Fleet electrification needing enhanced safety | Weak | +1.1% | Urban centers across North America | Medium term (2-4 years) | ||||

| Source: Mordor Intelligence | ||||||||

Growing Pedestrian-Safety Regulations

Regulatory momentum is reshaping the North American pedestrian detection systems market by imposing clear performance benchmarks on every light vehicle. NHTSA’s Federal Motor Vehicle Safety Standard 127 requires automatic emergency braking that recognizes pedestrians at speeds up to 62 mph in daylight and darkness.NHTSA has further folded pedestrian automatic emergency braking into its New Car Assessment Program for 2026 models, ensuring that safety ratings influence consumer choices. As insurers increasingly peg premiums to verified system performance, compliance moves from a legal obligation to a competitive differentiator.[1]National Highway Traffic Safety Administration, “Federal Motor Vehicle Safety Standard 127 Final Rule,” nhtsa.gov

Rising Pedestrian Fatalities & ADAS Demand

Escalating casualties sustain urgency for widespread adoption. US roadways recorded 7,522 pedestrian deaths in 2022, the highest count since 1981 and an 83% jump from 2009 levels. Urban corridors concentrate 85% of these fatalities, and 78% occur after dark, exposing optical-based detection limits when risk peaks. Early 2024 indicators show the upward trend persisting even as overall traffic fatalities moderate. Public pressure intensifies because older adults and minority communities bear disproportionate harm. Fleet operators now prioritize ADAS-equipped vehicles to mitigate liability, and larger vehicle platforms such as SUVs face mounting scrutiny because impact forces raise injury severity.[2]Governors Highway Safety Association, “Pedestrian Traffic Fatalities by State: 2024 Preliminary Data,” ghsa.org

Expansion of Level-2/3 Autonomy in Passenger Cars

Advancement toward conditional automation propels deeper sensor integration. Mercedes-Benz Drive Pilot, certified for Level 3 operation on certain highways, embeds urban pedestrian detection for seamless transition from automated to manual control. BMW’s newest ADAS suite applies AI-driven prediction to anticipate foot-traffic trajectories, while Mobileye’s EyeQ6 Lite processor brings similar functions to high-volume platforms. These systems reuse sensors needed for autonomous tasks, lowering marginal costs for pedestrian detection and expanding coverage across trims. Regulatory bodies now recognize system sophistication as a pathway to fewer crashes, promoting the North American pedestrian detection systems market.[3]Mercedes-Benz Group AG, “Drive Pilot: First SAE Level 3 Certified System,” mercedes-benz.com

Rapid Camera & SoC Cost Decline

Semiconductor progress erodes hardware cost barriers. Sony’s ISX038 CMOS sensor outputs RAW and YUV simultaneously and achieves 106 dB dynamic range, boosting low-light performance without expensive auxiliary lighting. Unit camera prices fell sharply as average vehicles moved from 2 cameras in 2019 to 8 cameras by 2025, reaching 12 cameras later in the decade. Mobileye has shipped more than 170 million EyeQ processors worldwide, an achievement that spreads development costs and enables sub-USD 100 pedestrian detection bundles for mass-market vehicles. Falling bills of materials broaden addressable volume and speed penetration into value-oriented segments.

*Restraints Impact Analysis

| Restraint | Qualitative Impact | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | ||||

|---|---|---|---|---|---|---|---|---|

Poor performance in darkness & severe weather Poor performance in darkness & severe weather | Moderate | -2.1% | Northern regions, seasonal impact | Medium term (2-4 years) | Qualitative Impact:Moderate | (~) % Impact on CAGR Forecast:-2.1% | Geographic Relevance:Northern regions, seasonal impact | Impact Timeline:Medium term (2-4 years) |

High upfront cost for economy-segment vehicles High upfront cost for economy-segment vehicles | Moderate | -1.8% | Price-sensitive markets across North America | Short term (≤ 2 years) | ||||

Complex calibration & maintenance raising TCO Complex calibration & maintenance raising TCO | Weak | -1.3% | Service-limited rural areas | Long term (≥ 4 years) | ||||

Data-privacy & cyber-security concerns over camera feeds Data-privacy & cyber-security concerns over camera feeds | Weak | -0.9% | Privacy-conscious regions, urban centers | Medium term (2-4 years) | ||||

| Source: Mordor Intelligence | ||||||||

Poor Performance in Darkness & Severe Weather

Environmental constraints still erode user confidence. Studies show camera-only systems lose detection accuracy during rain, fog, and snow, just when pedestrian risk escalates. Nighttime is especially problematic, accounting for 78% of fatalities. Thermal imaging fills part of the gap, and LiDAR’s active illumination copes well with darkness, yet costs and packaging limit fleet-wide adoption. Automakers thus pursue multi-sensor fusion, but real-world validation under extreme northern-climate conditions remains a hurdle, delaying complete market penetration in Canada and the upper US Midwest.[4]Teledyne FLIR, “Thermal Imaging for Automotive Safety,” flir.com

High Upfront Cost for Economy-Segment Vehicles

Entry-level models face tight retail price ceilings. Although NHTSA pegs automatic emergency braking at USD 82 per vehicle, full pedestrian detection needs extra sensors and domain controllers. With profit margins compressed on small cars, manufacturers must decide whether to absorb costs, raise prices, or pare other content. Commercial fleets apply even stricter payback analysis, balancing safety benefits against capital outlays. Aftermarket kits exist but introduce performance compromises and installation complexity, leading many fleet buyers to defer adoption until OEM prices fall.

Segment Analysis

By Sensor Modality: Camera leadership meets LiDAR acceleration

Video and camera setups owned 41.73% of revenue in 2025, giving them the largest slice of the North America pedestrian detection systems market. Legacy integration in mass-produced platforms explains the scale, while gradual pixel-density improvements keep them cost-effective. LiDAR, however, is sprinting at a 20.68% CAGR to 2031 as unit prices retreat and its weather-agnostic depth maps win favor among premium electric vehicles. Radar remains a staple with a 25.38% share and 16.32% growth due to all-weather dependability, and infrared sensors inch forward for superior nocturnal performance.

Integrated approaches define the next phase. Carmakers blend cameras with LiDAR and radar, using deep-learning fusion to offset each sensor’s blind spots. Toyota’s decision to source RoboSense LiDAR for certain Lexus electric variants highlights this transition. In parallel, Sony’s high-dynamic-range CMOS chips deliver clearer imagery in low light, narrowing performance gaps and extending the life of camera-centric architectures within the North America pedestrian detection systems market.

Note: Segment shares of all individual segments available upon report purchase

By Vehicle Type: Electrification amplifies the safety demand

Passenger cars contributed 61.55% of 2025 revenue, reflecting production volume and consumer-safety expectations. Yet, electric vehicles are the clear momentum story, rising 17.96% annually through 2031. Their premium positioning and software-centric design ethos make advanced safety a default feature, not an add-on. Light commercial vans follow closely, boosted by dense urban delivery cycles that elevate pedestrian interaction risks, while heavy trucks adopt sensors more cautiously due to tighter cost calculus.

Fleet electrification magnifies the narrative. Operators of ride-hail and last-mile services now embed pedestrian detection to curb liability and secure insurance rebates. Waymo clocked over 4 million autonomous trips in 2024, each relying on redundant perception stacks. Conversely, multiple investigations into Tesla’s Autopilot accentuate what happens when system performance falls short, incentivizing rivals to invest in more robust pedestrian recognition.

By Component: Software gains strategic weight

Hardware still claimed 70.62% revenue in 2025 as cameras, radar modules, and control units anchor bill-of-materials budgets. However, software is advancing 20.95% annually to 2031, reflecting the escalating complexity of neural networks that classify movement and foresee intent. Services, including calibration and over-the-air upgrades, occupy 10.06% of sales and grow at a healthy 15.98% pace, unlocking lifetime monetization.

Mobileye’s EyeQ6 Lite combines dedicated AI cores with power savings suitable for compact ECUs, while Indie Semiconductor’s backing of Expedera underscores the industry’s push for domain-specific inference engines. As algorithms evolve from static object detection to behavioral prediction, software licensing and feature-unlock models broaden revenue options in North America pedestrian detection.

Note: Segment shares of all individual segments available upon report purchase

By Sales Channel: OEM installs eclipse retrofit options

Factory-fit systems controlled 85.52% of shipments in 2025 and will continue expanding at 10.83% CAGR. Automakers prefer integrated designs that simplify homologation and give them full validation oversight. Though only 14.48% today, aftermarket kits log a quicker 14.23% growth trajectory because millions of vehicles on the road lack any detection function.

OEM dominance also reflects liability. Manufacturers can certify system performance and secure insurance partner approvals, while shoppers receive standardized user interfaces. Aftermarket players cater to fleets refreshing safety specs mid-life, but integration often stops short of deep brake-control links, curbing ultimate efficacy.

Geography Analysis

The US anchors the North American pedestrian detection systems market with a 78.35% share in 2025 and is on course for a 12.56% CAGR to 2031. Success stems from NHTSA’s binding regulation, aggressive insurance incentives, and strong R&D ecosystems in Michigan, California, and Texas. Urban centers with high fatality counts, such as Phoenix and Los Angeles, absorb solutions first, aided by municipal safety campaigns that highlight technology benefits.

Canada’s 15.02% share grows steadily at 13.02%. Transport Canada’s collaborative approach mixes voluntary adoption with education, and the agency reframes existing safety rules to cover ADAS without impeding local innovation. Winter weather extremes encourage the uptake of radar and thermal sensors over camera-only systems. Provinces with large metro areas like Ontario and Quebec set the adoption tone, influencing adjacent regions through inter-provincial fleet operations.

Mexico currently contributes 6.63% of revenue and exhibits a 11.18% CAGR as domestic safety regulation catches up. The government’s 2025 decree on autonomous-ready vehicles signals intent to harmonize with United States-Mexico-Canada Agreement norms. Major OEMs running plants in Nuevo León incorporate pedestrian detection into export models, which lowers per-unit costs for local sales over time. Lower consumer purchasing power still restrains base-trim availability, yet fleet buyers in logistics corridors begin specifying ADAS packages to meet cross-border contractual terms.

Competitive Landscape

Market Concentration

Competition is moderately fragmented, with Tier 1 suppliers, chip firms, and sensor startups jostling for design wins. Bosch, Continental, and DENSO leverage decades of integration expertise and global manufacturing scale. Mobileye leads perception software and silicon, underpinning over 170 million deployed systems and extending reach through recent contracts with Volkswagen Group and Polestar. Emerging LiDAR vendors like RoboSense secure footholds in luxury EV programs by promising weather-resistant precision at declining prices.

Strategic alliances dominate. Toyota’s partnership with RoboSense exemplifies automaker-sensor co-development, while Qualcomm’s acquisition of Autotalks for USD 350 million enhances V2X connectivity to complement perception hardware. Firms also pursue vertical integration; Sony supplies image sensors while expanding into edge AI modules, bridging component and algorithm layers.

White space remains in affordable solutions for economy vehicles. Several startups target software-only enhancements that work with existing cameras, aiming to boost detection quality without new hardware. Mature suppliers respond by offering scalable product families, ensuring the North American pedestrian detection systems market can meet both luxury and value segments without compromising regulation compliance.

North America Pedestrian Detection Systems Industry Leaders

*Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Qualcomm acquired Autotalks for USD 350 million to embed V2X communications within the Snapdragon Digital Chassis platform, enhancing pedestrian collision avoidance capabilities.

- March 2025: Volkswagen Group, Valeo, and Mobileye agreed to integrate upgraded pedestrian detection into future MQB platform vehicles starting with 2026 models.

- December 2024: Teledyne FLIR and VSI Labs' advanced automotive thermal imaging, boosting detection accuracy in darkness and adverse weather.

- January 2024: Mobileye secured a new global OEM contract to deploy EyeQ6 processors with enhanced pedestrian detection in future urban-centric vehicle lines.

Table of Contents for North America Pedestrian Detection Systems Industry Report

1. Introduction

- 1.1Study Assumptions & Market Definition

- 1.2Scope of the Study

2. Research Methodology

3. Executive Summary

4. Market Landscape

- 4.1Market Overview

- 4.2Market Drivers

- 4.2.1Growing pedestrian-safety regulations

- 4.2.2Rising pedestrian fatalities & ADAS demand

- 4.2.3Expansion of Level-2/3 autonomy in passenger cars

- 4.2.4Rapid camera & SoC cost decline

- 4.2.5Insurance premium discounts for vehicles with certified PDS

- 4.2.6Fleet electrification (ride-hail & last-mile) needing enhanced safety

- 4.3Market Restraints

- 4.3.1Poor performance in darkness & severe weather

- 4.3.2High upfront cost for economy-segment vehicles

- 4.3.3Complex calibration & maintenance raising TCO

- 4.3.4Data-privacy & cyber-security concerns over camera feeds

- 4.4Value / Supply-Chain Analysis

- 4.5Regulatory Landscape

- 4.6Technological Outlook

- 4.7Porter’s Five Forces

- 4.7.1Bargaining Power of Suppliers

- 4.7.2Bargaining Power of Buyers/Consumers

- 4.7.3Threat of New Entrants

- 4.7.4Threat of Substitute Products

- 4.7.5Intensity of Competitive Rivalry

5. Market Size & Growth Forecasts (Value, 2024-2030)

- 5.1By Sensor Modality

- 5.1.1Video/Camera

- 5.1.2Infrared/Thermal

- 5.1.3Radar

- 5.1.4LiDAR

- 5.1.5Sensor-Fusion/Hybrid

- 5.2By Vehicle Type

- 5.2.1Passenger Cars

- 5.2.2Light Commercial Vehicles (LCV)

- 5.2.3Heavy Commercial Vehicles (HCV)

- 5.2.4Electric Vehicles (EV)

- 5.3By Component

- 5.3.1Hardware

- 5.3.2Software

- 5.3.3Services

- 5.4By Sales Channel

- 5.4.1OEM-fitted

- 5.4.2Aftermarket

- 5.5By Country

- 5.5.1United States

- 5.5.2Canada

- 5.5.3Mexico

6. Competitive Landscape

- 6.1Strategic Moves

- 6.2Market Share Analysis

- 6.3Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)}

- 6.3.1Toyota Motor Corporation

- 6.3.2Volvo Cars

- 6.3.3BMW Group

- 6.3.4Mercedes-Benz Group AG

- 6.3.5Audi AG

- 6.3.6Nissan Motor Co., Ltd.

- 6.3.7Stellantis (Peugeot)

- 6.3.8Honda Motor Co., Ltd.

- 6.3.9General Motors Company

- 6.3.10Tesla, Inc.

- 6.3.11Mobileye (Intel)

- 6.3.12Aptiv PLC

- 6.3.13Robert Bosch GmbH

- 6.3.14Continental AG

- 6.3.15DENSO Corporation

- 6.3.16FLIR (now Teledyne FLIR)

- 6.3.17Panasonic Corporation

- 6.3.18Magna International

- 6.3.19Valeo SA

- 6.3.20ZF Friedrichshafen AG

- 6.3.21Autoliv Inc.

- 6.3.22Luminar Technologies

- 6.3.23Innoviz Technologies

- 6.3.24LeddarTech

- 6.3.25NXP Semiconductors

- 6.3.26NVIDIA Corporation

- 6.3.27Velodyne Lidar

7. Market Opportunities & Future Outlook

- 7.1White-space & unmet-need assessment

North America Pedestrian Detection Systems Market Report Scope

Pedestrian Detection (PD) is an advanced driver assistance system (ADAS) that recognizes pedestrians (and occasionally bikers and pets) in the path of a vehicle. When a risk is recognized, Pedestrian Detection alerts drivers with an audio, visual, or tactile warning.

The North American pedestrian detection systems market is segmented by type and by country. By type, the market is segmented into video, infrared, hybrid, and other types by country: United States of America, Canada, and the Rest of North America.

The report offers the market size and forecasts in value (USD) for all the above segments.