Multi-Agent System (MAS) Platform Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

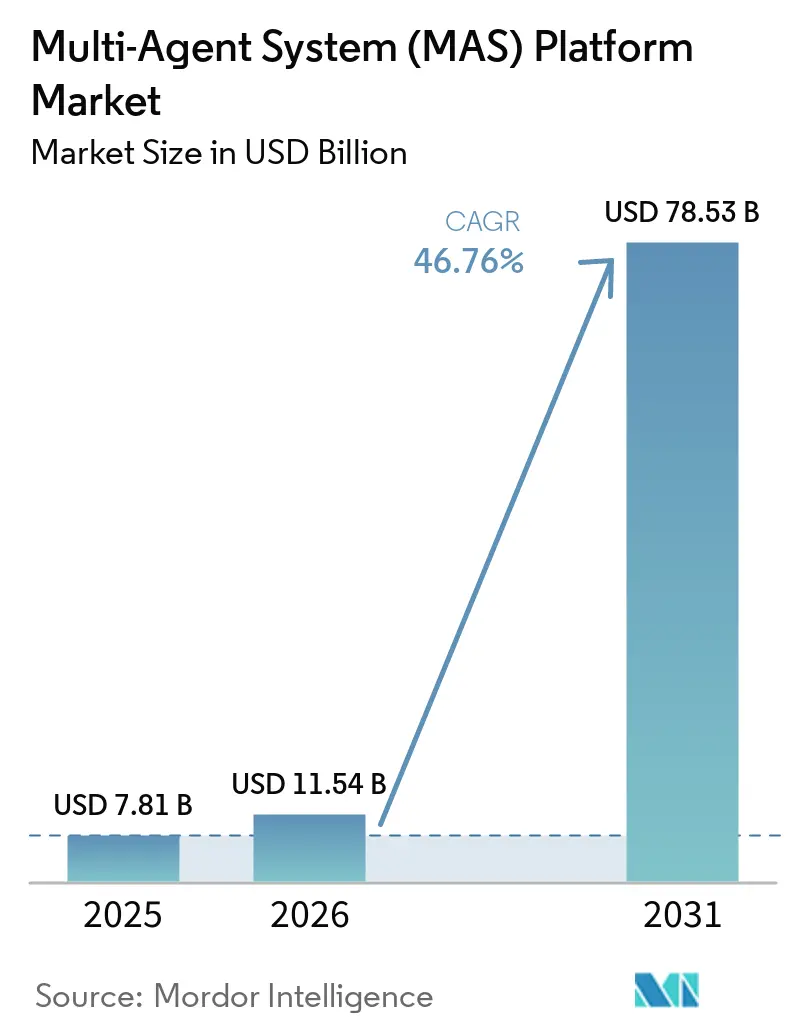

| Market Size (2026) | USD 11.54 Billion |

| Market Size (2031) | USD 78.53 Billion |

| Growth Rate (2026 - 2031) | 46.76% CAGR |

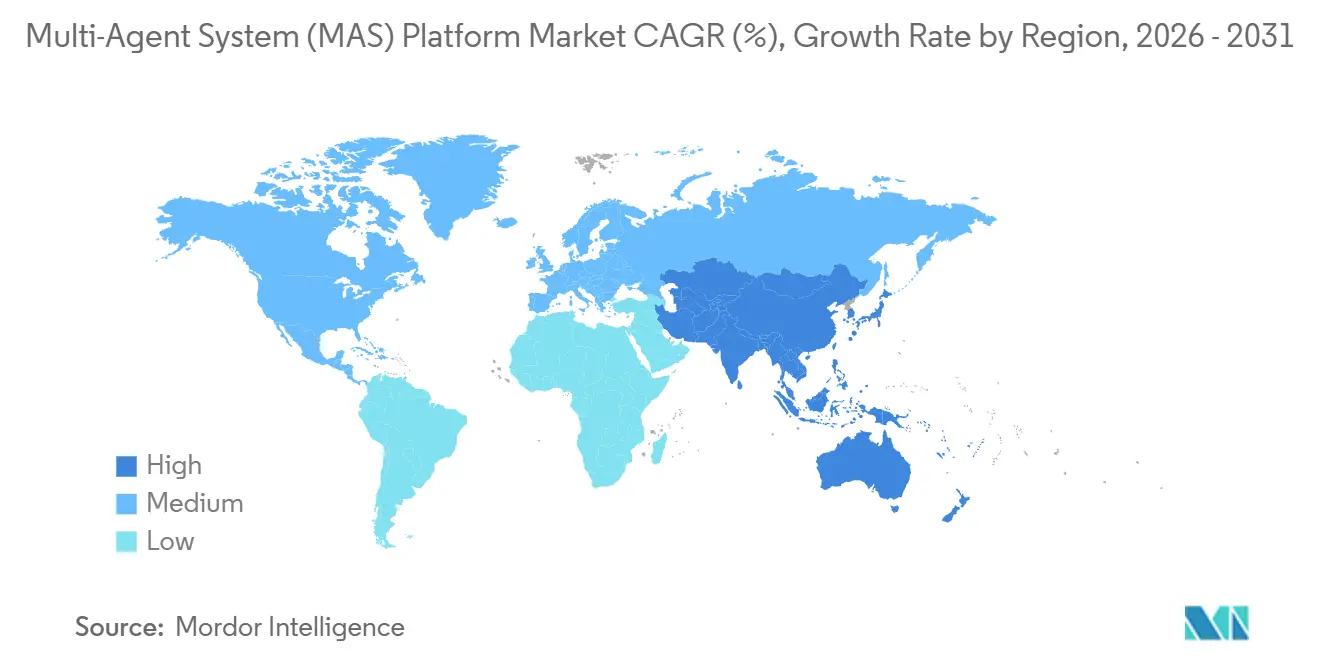

| Fastest Growing Market | Middle East |

| Largest Market | North America |

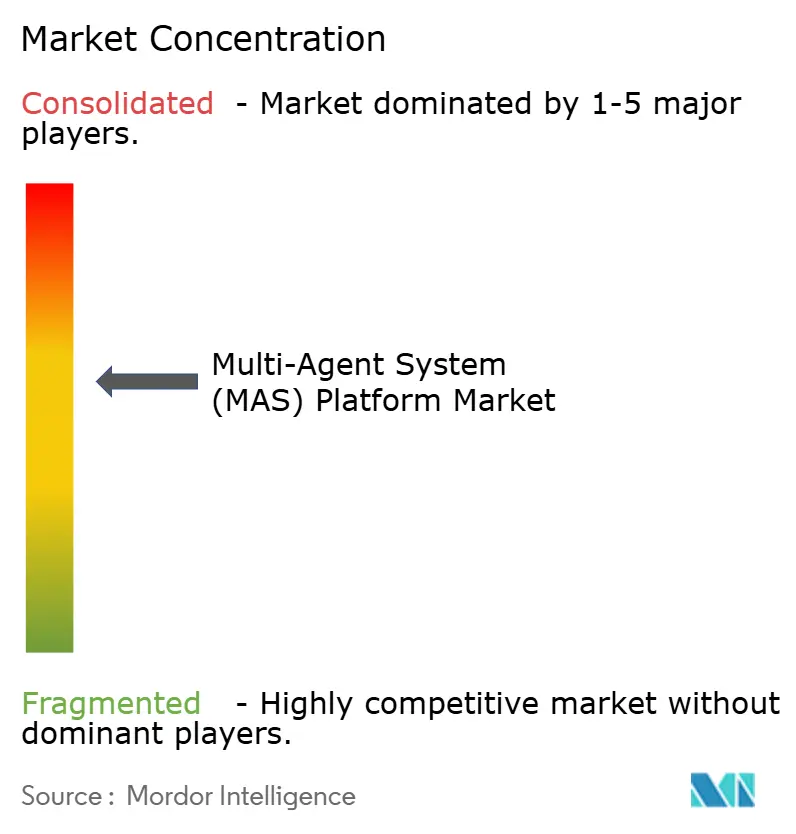

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Multi-Agent System (MAS) Platform Market Analysis by Mordor Intelligence

The multi-agent system platform market size is projected to expand from USD 7.81 billion in 2025 and USD 11.54 billion in 2026 to USD 78.53 billion by 2031, registering a CAGR of 46.76% between 2026 and 2031. Enterprises are accelerating the switch from monolithic automation toward distributed agent architectures that coordinate robotics, software workflows, and autonomous decision support. Widespread cloud availability, falling edge-AI costs, and convergence of large-language-model agents with reinforcement-learning policies are removing technical barriers. Vendors are embedding alignment and safety guardrails to comply with emerging regulations, while token-incentivized protocols demonstrate alternative coordination models. Intense competition coupled with open-source momentum keeps pricing in check, favoring rapid, cross-industry proliferation of the multi-agent system platform market.

Key Report Takeaways

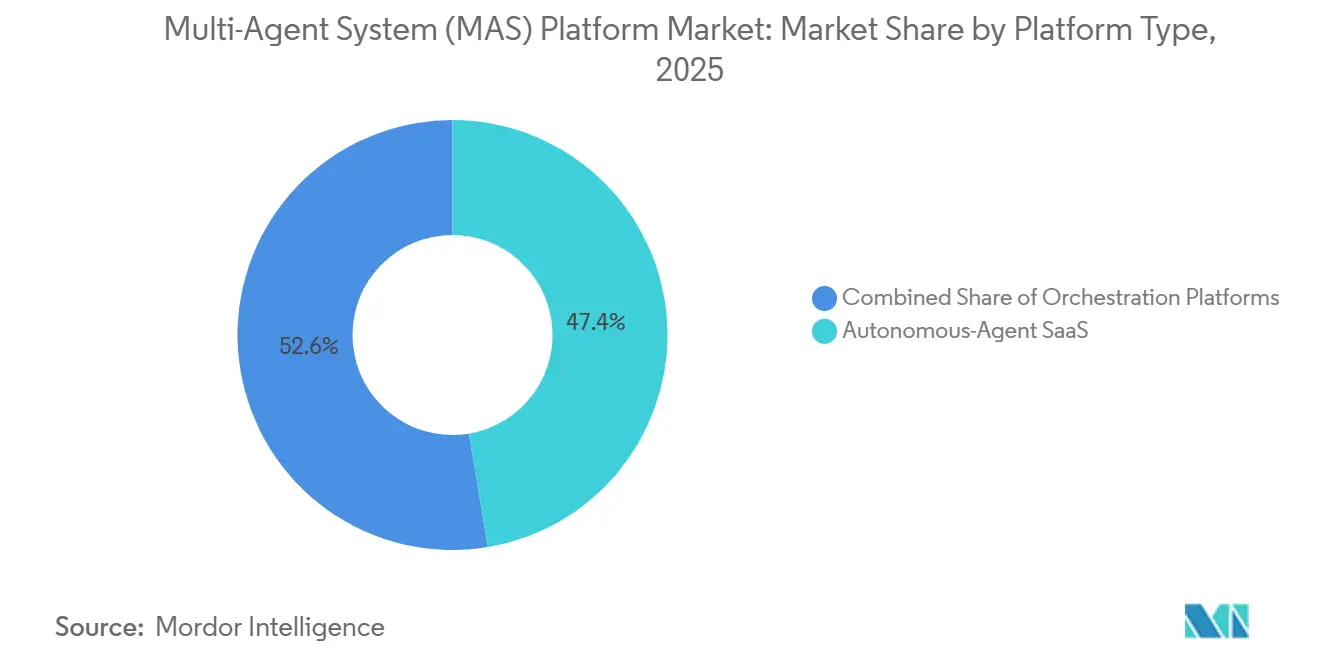

- By platform type, orchestration platforms led with 34.63% revenue share in 2025, whereas autonomous-agent software-as-a-service offerings are projected to grow at a 47.37% CAGR to 2031.

- By deployment mode, cloud captured 72.58% of the 2025 revenue base, while on-premises and edge configurations are expected to advance at a 47.21% CAGR through 2031.

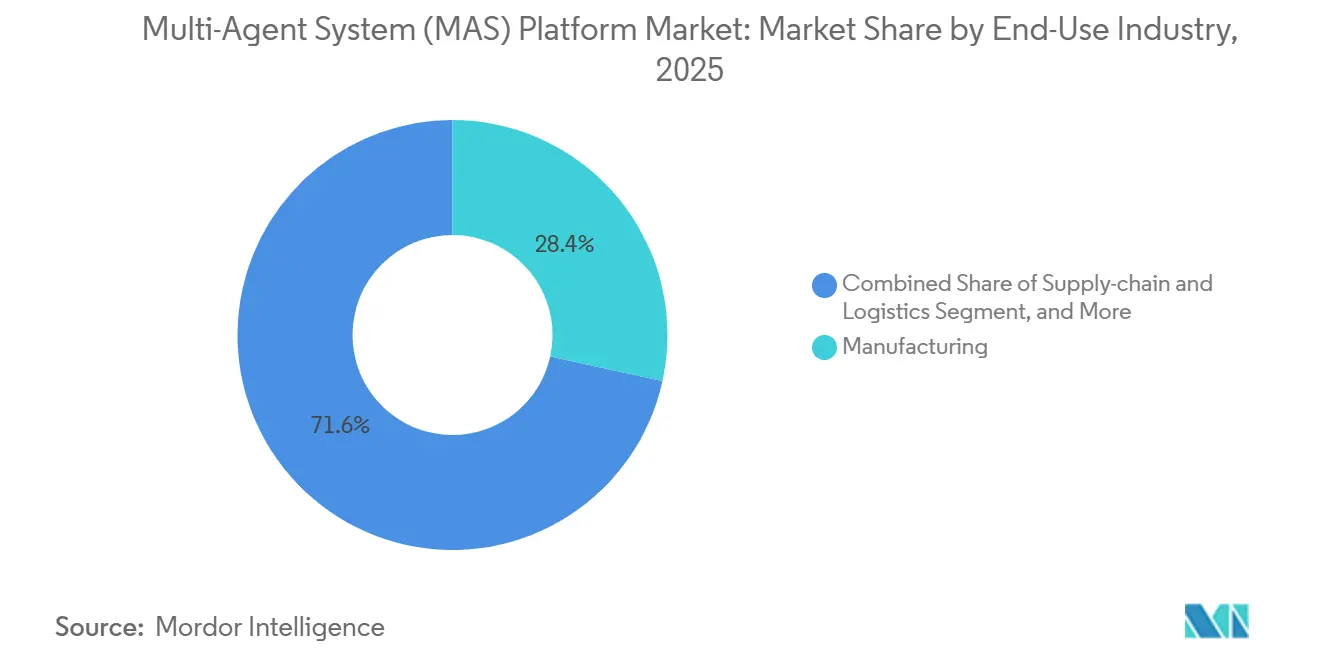

- By end-use industry, manufacturing accounted for 28.48% of revenue in 2025, but smart cities and infrastructure are forecast to expand at a 47.83% CAGR through 2031.

- By application, multi-robot coordination accounted for 31.52% of the market in 2025, and autonomous trading and financial operations are predicted to register a 47.04% CAGR through 2031.

- By geography, North America accounted for 41.38% of revenue share in 2025, whereas the Middle East is set to grow at a 47.11% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Multi-Agent System (MAS) Platform Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cloud-Native Multi-Agent System Deployment Boom | +9.2% | Global, concentrated in North America and Europe | Medium term (2-4 years) |

| Warehouse-Automation Demand for Multi-Robot Orchestration | +8.7% | North America, Europe, Asia-Pacific manufacturing hubs | Short term (≤ 2 years) |

| Convergence of Large-Language-Model-Based Agents and Reinforcement-Learning Frameworks | +8.4% | Global, led by North America and Asia-Pacific | Medium term (2-4 years) |

| Declining Edge-AI Costs Enabling On-Device Agents | +7.1% | Asia-Pacific core, spill-over to Middle East and Africa | Long term (≥ 4 years) |

| Token-Incentivized Open Multi-Agent System Protocols | +5.8% | Global, early traction in Europe and Asia-Pacific | Long term (≥ 4 years) |

| Emergence of Agent-Alignment Toolkits for Safety-Critical Industries | +4.9% | North America and Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Cloud-Native Multi-Agent System Deployment Boom

Kubernetes-compatible orchestration platforms let developers scale from dozens to thousands of agents without rewriting infrastructure. Microsoft’s AutoGen and LangGraph Cloud, both launched in 2025, introduced declarative templates that turn YAML descriptions into running clusters. Elastic compute and managed networking shorten proof-of-concept cycles, while hyperscalers bundle discounted inference accelerators that lock customers into their ecosystems. Financial institutions and logistics operators report faster time-to-value once cluster management is offloaded, reinforcing the positive feedback loop that is lifting the multi-agent system platform market.

Warehouse-Automation Demand for Multi-Robot Orchestration

Fulfillment centers now optimize fleet-level productivity rather than individual robot features. Locus Robotics coordinates more than 6,000 autonomous mobile robots across 300 warehouses, cutting order-cycle time by 25% compared with manual picking.[1]Locus Robotics, “Global Warehouse Expansion,” locusrobotics.com Symbotic earned USD 593.3 million from 42 Walmart distribution centers in fiscal 2024, underlining commercial willingness to invest when orchestration delivers double-digit throughput gains. Edge-resident agents avoid cloud latency, and simulation-based pretraining accelerates commissioning, positioning warehouse automation as a durable growth driver.

Convergence of Large-Language-Model-Based Agents and Reinforcement-Learning Frameworks

Academic teams demonstrated that combining language models with environment feedback elevates multi-step reasoning. Tsinghua University’s AGILE framework fine-tunes a transformer with reinforcement signals and achieves state-of-the-art scores on ALFWorld. OpenAI and Amazon Web Services committed USD 38 billion to specialized training clusters for such hybrid workloads in 2025. Enterprises can now issue natural-language goals, let agents refine plans, and adapt in real time, broadening addressable use cases beyond scripted automation.

Declining Edge-AI Costs Enabling On-Device Agents

Application-specific integrated circuits plus model quantization lowered the cost per million tokens on edge hardware below USD 0.01 in 2025. NVIDIA’s Jetson Orin module delivers 275 TOPS at sub-USD 500 price points. Qualcomm’s Snapdragon 8 Elite adds a 45 BOPS neural unit to flagship phones. Latency-sensitive sectors such as healthcare and industrial robotics increasingly embed agents locally, sidestepping data-sovereignty barriers and reducing cloud spend, which accelerates the multi-agent system platform market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Scarcity of Multi-Agent-System-Ready Talent and Standards | -4.3% | Global, acute in emerging markets | Medium term (2-4 years) |

| Expanded Cyber-Security Attack Surface at Agent Level | -3.8% | Global, heightened in BFSI and healthcare | Short term (≤ 2 years) |

| Graphics-Processing-Unit and Inference-Chip Supply-Chain Volatility | -3.2% | Global, concentrated in North America and Asia-Pacific | Short term (≤ 2 years) |

| Energy-Efficiency Pressure from Environmental, Social, and Governance Investors | -2.7% | Europe and North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Scarcity of Multi-Agent-System-Ready Talent and Standards

LinkedIn’s 2025 AI Talent Gap Report showed that 68% of enterprises struggle to hire engineers skilled in inter-agent communication and distributed reinforcement learning, stretching median recruitment cycles past 90 days. Fragmented standards complicate onboarding because vendors must support multiple ontologies, while global professional development pipelines lag behind demand. The shortfall inflates salaries and extends implementation timelines, slowing adoption.

Expanded Cyber-Security Attack Surface at Agent Level

Autonomous agents are vulnerable to prompt injection, data poisoning, and model extraction attacks. NIST cataloged 23 multi-agent-specific threat scenarios in its 2024 AI Cybersecurity Framework. The European Union Agency for Cybersecurity warned that adversaries could inject malicious agents into critical infrastructure protocols.[2]ENISA, “2025 Threat Landscape,” enisa.europa.eu Financial institutions already report attempts to embed fraudulent instructions into market data feeds. Limited off-the-shelf monitoring tools force buyers to craft bespoke defenses, raising the total cost of ownership and dampening near-term growth.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Platform Type: Autonomous-Agent SaaS Outpaces Orchestration

Autonomous-agent software-as-a-service offerings are forecast to grow at 47.37% between 2026 and 2031. This significant growth reflects the increasing buyer preference for turnkey subscription models that simplify the complexities of distributed systems. These models are driving the multi-agent system platform market size for SaaS well above historical norms, as businesses seek scalable and efficient solutions. Orchestration platforms, which maintained a 34.63% revenue share in 2025, highlight the strong position of incumbents among vendors that provide reliability, durability, and exactly-once execution capabilities.

Pure-play frameworks continue to attract engineering-led organizations due to their flexibility and customization potential. However, the steep learning curve associated with consensus mechanisms and failure detection has limited their broader adoption. Simulation suites, such as NVIDIA Omniverse, achieved a USD 1 billion annual run rate in fiscal 2025, emphasizing the growing demand for virtual validation of policies before physical deployment. This trend underscores the importance of simulation in reducing risks and optimizing performance in real-world applications. Competitive pressure from enterprise-software incumbents bundling agents into CRM and ERP suites is expected to compress standalone platform margins. Nevertheless, vertical specialization and tailored solutions can help mitigate the effects of commoditization, enabling vendors to maintain a competitive edge.

By Deployment Mode: Edge Momentum Builds Under Sovereignty Rules

Cloud retained 72.58% of the revenue share in 2025, primarily due to its ability to scale elastically and simplify operations. This dominance highlights the growing preference for cloud-based solutions in the multi-agent system platform market. However, on-premises and edge configurations are projected to achieve a significant compound annual growth rate (CAGR) of 47.21% through 2031. This rapid growth is expected to narrow the market share gap between cloud and other configurations. The increasing adoption of on-premises and edge solutions is driven by the need for localized data processing, particularly among manufacturers and hospitals. These entities aim to comply with stringent data protection regulations, such as the European Union’s General Data Protection Regulation (GDPR), which imposes penalties for cross-border data transfers.[3]European Commission, “GDPR Portal,” ec.europa.eu

Advancements in technology, such as quantized models and cost-effective inference chips, have enabled robots, point-of-sale devices, and industrial sensors to operate agents at a significantly reduced cost-less than one cent per million tokens. This affordability has expanded the accessibility of multi-agent systems across various industries. Additionally, hybrid topologies that combine on-device perception loops with cloud-based planning synchronization offer substantial latency benefits while maintaining centralized oversight. These hybrid systems are particularly advantageous for applications requiring real-time decision-making and operational efficiency. To support such deployments, platforms like Microsoft Azure IoT Edge and AWS Greengrass have introduced orchestration extensions. These enhancements simplify the management of split deployments, ensuring seamless integration between edge devices and cloud infrastructure.

By End-Use Industry: Smart Cities Achieve the Fastest Growth

Manufacturing contributed 28.48% revenue in 2025, driven by the adoption of multi-robot coordination in automotive production lines and e-commerce fulfillment centers. These systems have enabled manufacturers to optimize workflows, reduce operational costs, and improve overall efficiency. However, smart cities and infrastructure are projected to grow at a robust 47.83% CAGR, positioning municipal deployments as a significant growth driver for the multi-agent system platform market. For instance, Singapore’s Nanjing Eco Hi-Tech Island implemented agent-based coordination systems, which successfully reduced peak electricity demand by 22%, showcasing the potential of such technologies in urban planning and energy management.

Digital twins, which create virtual replicas of physical systems, are increasingly being used by city planners to simulate and test policy decisions before committing financial and physical resources. This approach minimizes risks and ensures better resource allocation. Additionally, sovereign wealth funds in the Middle East are actively financing large-scale rollouts of these technologies, further accelerating their adoption. In the healthcare and finance sectors, advancements are also being made as specialists deploy multi-agent systems to orchestrate diagnostic processes, ensure regulatory compliance, and manage trading operations. Research conducted by Mount Sinai Health System has demonstrated that orchestrated ensembles of agents outperform traditional monolithic models across 80 medical tasks, highlighting their effectiveness in complex, data-intensive environments.

By Application: Autonomous Trading Leads Future Expansion

Multi-robot coordination delivered 31.52% of 2025 revenue, but autonomous trading and financial operations are projected to register a 47.04% CAGR to 2031, signaling that algorithmic finance will play an outsized role in the multi-agent system platform industry. Hedge funds are increasingly replacing traditional rule-based strategies with reinforcement-learning agents that adapt to regime shifts, achieving Sharpe ratios exceeding 2.0 in live trading. This shift highlights the growing reliance on advanced multi-agent systems to optimize financial operations and enhance decision-making processes.

Workflow orchestration, decision support, and digital-twin modeling are also experiencing significant growth as enterprises aim to achieve cross-domain optimization. For instance, NVIDIA Omniverse enables automakers to simulate thousands of vehicles in photorealistic virtual cities, allowing them to stress-test agent policies extensively before conducting physical trials. These advancements not only reduce costs but also improve efficiency and safety in real-world applications. Combined, these applications are expanding the multi-agent system platform market footprint across diverse sectors, including knowledge work, operations, and capital markets, driving innovation and operational excellence.

Geography Analysis

North America captured 41.38% of 2025 revenue, driven by hyperscaler product launches and early adoption in logistics and finance. OpenAI and AWS’s USD 38 billion infrastructure partnership underscores regional commitment to scaling hybrid-agent workloads. Additionally, the U.S. defense programs that coordinate autonomous vehicles and logistics chains have further legitimized the technology for commercial buyers, encouraging broader adoption across industries. Europe emphasizes data sovereignty and algorithmic transparency, with automotive and industrial automation leaders in Germany piloting agent-based scheduling systems that align with the AI Act. GDPR limitations are also fueling demand for localized deployments, as businesses seek to comply with stringent data protection regulations. Government funding initiatives and university-led research projects continue to drive innovation in the region, ensuring a steady contribution to the overall growth of the multi-agent system platform market.

The Middle East is forecast to record the fastest regional CAGR at 47.11% between 2026 and 2031. Large-scale projects like Saudi Arabia’s NEOM and the United Arab Emirates’ Dubai Digital Twin are integrating agents for energy management, mobility, and waste management. Sovereign wealth funds in the region are not only supplying capital but also mandating cutting-edge sustainability targets, creating a fertile environment for vendors to innovate and expand. Asia-Pacific benefits from China’s significant investments in smart-city infrastructure, Japan’s well-established robotics industry, and India’s abundant software development talent.

Singapore’s agent-driven eco-district serves as a performance benchmark for regional planners, showcasing the potential of agent-based systems in urban development. South America and Africa, while smaller markets today, are demonstrating early adoption in sectors such as mining, agriculture, and telecommunications. In these regions, agents are being used to optimize resource allocation and improve operational efficiency, even in areas with limited infrastructure, highlighting their adaptability and growth potential.

Competitive Landscape

The multi-agent system platform market remains moderately fragmented, with no vendor exceeding a 15% share in 2025. UiPath, Salesforce, and Microsoft embed agentic capabilities into existing footprints, leveraging their extensive installed bases to accelerate cross-sell opportunities. These established players focus on integrating multi-agent systems into their existing product ecosystems to provide seamless solutions to their customers. Startups, including CrewAI and Swarms, focus on improving the developer experience, fostering open-source ecosystems, and addressing vertical-specific needs. These startups differentiate themselves through rapid iteration cycles, enabling them to adapt quickly to market demands and deliver innovative solutions tailored to niche applications.

Token-incentivized networks such as Fetch.ai supply autonomous economic agents that discover services and settle payments on-chain, appealing to industries that require decentralized trust mechanisms. These networks enable secure, efficient transactions, making them particularly attractive to sectors such as supply chain management and financial services. Temporal Technologies’ USD 300 million Series D funding round highlights the growing investor interest in durable execution engines that guarantee workflow completion. Such engines are critical for ensuring reliability and efficiency in complex multi-agent systems. Open-standards initiatives, notably IEEE’s P2846 working group, aim to unify communication ontologies, which could significantly lower switching costs for businesses and accelerate market consolidation by fostering interoperability among different platforms.[4]IEEE, “P2846 Working Group Charter,” standards.ieee.org

White-space opportunities are emerging in sectors such as healthcare, finance, and manufacturing, where add-ons that integrate seamlessly with legacy programmable-logic controllers or electronic health record systems are in high demand. These integrations enable organizations to modernize their operations without overhauling existing infrastructure, providing a cost-effective pathway to adopting advanced technologies. Vendors that excel at mastering domain-specific compliance requirements and aligning with stringent safety standards are well-positioned to secure premium contracts as regulatory frameworks become increasingly stringent. This focus on compliance and safety will be a key differentiator for vendors aiming to establish a strong foothold in the market.

Multi-Agent System (MAS) Platform Industry Leaders

OpenAI LLC

UiPath Inc.

GreyOrange Inc.

Symbotic Inc.

Blue Yonder Group Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: UiPath Inc. introduced next-generation agentic automation capabilities, integrating AI agents with RPA workflows for industry-specific deployments (healthcare, finance).

- January 2026: Fetch.ai Foundation Pte Ltd. advanced its decentralized multi-agent infrastructure with enhancements to autonomous economic agents and blockchain-based coordination protocols.

- December 2025: Cognizant Technology Solutions Corp. partnered with leading AI platform providers to scale enterprise adoption of agent-based automation and decision intelligence solutions.

- November 2025: Anthropic P.B.C. expanded its AI assistant ecosystem with enterprise integrations, supporting multi-agent collaboration and safe deployment frameworks.

Global Multi-Agent System (MAS) Platform Market Report Scope

The Multi-Agent System Platform Market refers to the global ecosystem of software platforms and integrated solutions that enable the design, development, deployment, coordination, and management of multiple autonomous or semi-autonomous agents operating within a shared environment. These agents, powered by artificial intelligence, machine learning, and rule-based systems- interact with each other and external systems to perform complex, distributed tasks such as decision-making, simulation, optimization, and automation across enterprise and industrial contexts.

The Multi-Agent System Platform Market Report is Segmented by Platform Type (Agent-Development Frameworks, Orchestration Platforms, Simulation and Digital-Twin Suites, Autonomous-Agent SaaS, and Other Platform Type), Deployment Mode (Cloud, On-Premises/Edge), End-Use Industry (Manufacturing, Supply-Chain and Logistics, Healthcare and Life-Sciences, BFSI, and Smart Cities and Infrastructure), Application (Workflow and Process Orchestration, Multi-Robot Coordination, Decision-Support and Planning, Simulation and Digital-Twin Modelling, and Autonomous Trading and Fin-Ops), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Agent-Development Frameworks |

| Orchestration Platforms |

| Simulation and Digital-Twin Suites |

| Autonomous-Agent SaaS |

| Other Platform Type |

| Cloud |

| On-Premises / Edge |

| Manufacturing |

| Supply-Chain and Logistics |

| Healthcare and Life-Sciences |

| BFSI |

| Smart Cities and Infrastructure |

| Workflow and Process Orchestration |

| Multi-Robot Coordination |

| Decision-Support and Planning |

| Simulation and Digital-Twin Modelling |

| Autonomous Trading and Fin-Ops |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Qatar | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Egypt | |

| Rest of Africa |

| By Platform Type | Agent-Development Frameworks | |

| Orchestration Platforms | ||

| Simulation and Digital-Twin Suites | ||

| Autonomous-Agent SaaS | ||

| Other Platform Type | ||

| By Deployment Mode | Cloud | |

| On-Premises / Edge | ||

| By End-Use Industry | Manufacturing | |

| Supply-Chain and Logistics | ||

| Healthcare and Life-Sciences | ||

| BFSI | ||

| Smart Cities and Infrastructure | ||

| By Application | Workflow and Process Orchestration | |

| Multi-Robot Coordination | ||

| Decision-Support and Planning | ||

| Simulation and Digital-Twin Modelling | ||

| Autonomous Trading and Fin-Ops | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Qatar | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Egypt | ||

| Rest of Africa | ||

Key Questions Answered in the Report

How fast is revenue expanding for the multi-agent system platform market?

The multi-agent system platform market size is projected to climb from USD 11.54 billion in 2026 to USD 78.53 billion by 2031, reflecting a 46.76% CAGR.

Which deployment mode is gaining momentum after cloud?

On-premises and edge configurations are forecast to grow at a 47.21% CAGR through 2031 as firms address latency and data-sovereignty constraints.

Which end-use will outpace manufacturing?

Smart cities and infrastructure deployments are expected to advance at a 47.83% CAGR between 2026 and 2031, the fastest among all industries.

Why are autonomous trading platforms attractive?

Hedge funds adopting reinforcement-learning agents achieve higher risk-adjusted returns, propelling autonomous trading to a projected 47.04% CAGR through 2031.

What hampers rapid adoption despite strong growth drivers?

A shortage of engineers skilled in distributed reinforcement learning and agent standards, plus heightened cyber-security risks, slows deployment momentum.

Which region offers the strongest near-term upside?

The Middle East shows the highest projected regional CAGR at 47.11% thanks to sovereign-fund backed smart-city initiatives.

Page last updated on: