Technology, Media and Telecom

5th MayPricing Strategy for Semiconductor Components

3 Min Read

The Middle East and Africa Proximity Sensors Market is Segmented by Technology (Inductive, Capacitive), Sensing Range (Short, Medium, Long), Output Type (Digital, Analog), End-User Industry (Automotive, Industrial Manufacturing and Automation), and Country (Saudi Arabia, UAE, South Africa, Egypt, Nigeria, and Rest of Middle East and Africa). The Market Size and Forecasts are Provided in Terms of Value (USD).

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Base Year For Estimation | 2025 |

| Forecast Data Period | 2026 - 2031 |

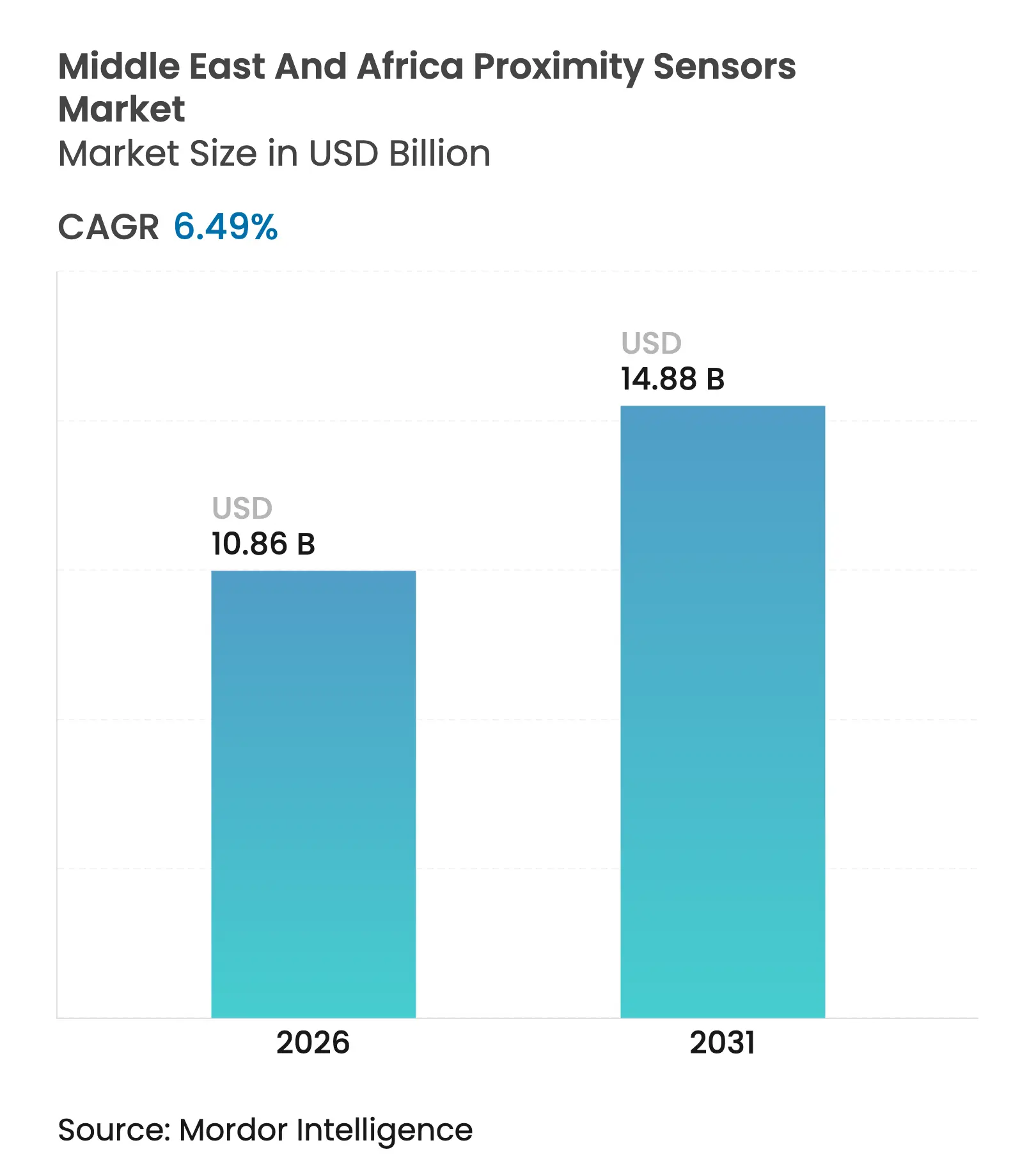

| Market Size (2026) | USD 10.86 Billion |

| Market Size (2031) | USD 14.88 Billion |

| Growth Rate (2026 - 2031) | 6.49 % CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

Middle East and Africa proximity sensors market size in 2026 is estimated at USD 10.86 billion, growing from 2025 value of USD 10.2 billion with 2031 projections showing USD 14.88 billion, growing at 6.49% CAGR over 2026-2031. The region’s diversification push, large-scale renewable-energy roll-outs and growing automotive hubs are creating sustained demand for non-contact sensing devices. Saudi Arabia, the United Arab Emirates (UAE) and South Africa continue to concentrate the bulk of industrial automation projects, while Egypt’s wind corridors and Morocco’s export-oriented vehicle plants are driving the fastest incremental volumes. Import-substitution incentives in GCC states favour suppliers that can localise final assembly, and the steady adoption of IO-Link is tilting preference toward digital-output devices. Long-range ultrasonic and ruggedised inductive types are gaining visibility as harsh desert and mining environments expose the limits of legacy photoelectric alternatives. Cooperative ventures among European and Japanese vendors signal a strategic shift toward shared regional production and service networks that can meet local certification demands.

Key Report Takeaways

*Drivers Impact Analysis

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE | |||

|---|---|---|---|---|---|---|

Industrial-Automation Investments in GCC Discrete Manufacturing Industrial-Automation Investments in GCC Discrete Manufacturing | 1.2% | GCC core, spillover to Egypt | Medium term (2-4 years) | (~) % IMPACT ON CAGR FORECAST:1.2% | GEOGRAPHIC RELEVANCE:GCC core, spillover to Egypt | IMPACT TIMELINE:Medium term (2-4 years) |

Automotive Assembly Expansion across Morocco and South Africa Automotive Assembly Expansion across Morocco and South Africa | 0.9% | Morocco, South Africa, regional supply chains | Long term (≥ 4 years) | |||

Surge in UAE Smart-Packaging Lines for Halal Foods Surge in UAE Smart-Packaging Lines for Halal Foods | 0.6% | UAE, Kuwait, Qatar | Short term (≤ 2 years) | |||

Wind-Turbine Build-Out in Saudi Arabia and Egypt Driving Long-Range Sensors Wind-Turbine Build-Out in Saudi Arabia and Egypt Driving Long-Range Sensors | 0.8% | Saudi Arabia, Egypt, Oman | Medium term (2-4 years) | |||

Maintenance-Free Inductive Sensors in Harsh Mining Sites (RSA, Namibia) Maintenance-Free Inductive Sensors in Harsh Mining Sites (RSA, Namibia) | 0.5% | South Africa, Namibia, Botswana | Long term (≥ 4 years) | |||

IO-Link Protocol Standardization Across GCC Industrial Facilities IO-Link Protocol Standardization Across GCC Industrial Facilities | 0.4% | GCC countries, Morocco | Short term (≤ 2 years) | |||

| Source: Mordor Intelligence | ||||||

Industrial-automation investments in GCC discrete manufacturing

GCC governments are mandating higher automation ratios in new factories under national industrial strategies, pushing plant operators toward sensor networks that can withstand high ambient temperatures and fine dust.[1]Ishida Europe, “More Intelligent and Faster Together,” ishidaeurope.com Integrated IO-Link connectivity is now a de-facto specification in major Saudi and Emirati green-field projects, enabling device-level diagnostics that cut unscheduled downtime. Local content rules grant tariff relief for proximity-sensor sub-assemblies finished within GCC free zones, steering global suppliers toward joint manufacturing with regional distributors. These policies, coupled with subsidised energy, keep the Middle East and Africa proximity sensors market on a steady uptrend.

Automotive assembly expansion across Morocco and South Africa

Morocco produced 614,000 vehicles in 2024 and has become the European Union’s largest external vehicle supplier, a status that necessitates near-zero defect tolerances on body-in-white lines. Tier-1 suppliers in Tangier’s free zone are specifying long-range laser and ultrasonic sensors for battery-pack positioning, raising per-line sensor counts by up to 20%. South Africa, while contending with lower overall volumes, is automating battery-assembly stages to stay globally competitive, further stimulating the Middle East and Africa proximity sensors market.[2]ifm electronic, “Mining Catalogue,” ifm.com

Surge in UAE smart-packaging lines for halal foods

Halal processors are installing fully automated inspection systems to comply with Dubai’s Food Security Strategy 2051. New lines deploy photoelectric proximity sensors able to detect foreign particles smaller than 0.1 mm at throughputs exceeding 1,200 packs per minute. The premium placed on traceability is driving replacement of legacy analog devices with self-diagnosing digital models that feed data into central quality dashboards.

Wind-turbine build-out in Saudi Arabia and Egypt

Each new on-shore turbine integrates 12-15 proximity sensors that govern blade pitch and nacelle yaw; Saudi turbines additionally require extended temperature tolerance up to 50 °C. Similar specifications are emerging at Egypt’s Gulf of Suez wind farms, where abrasive sand calls for IP67-rated housings with anti-erosion coatings. These conditions fuel demand for ultrasonic units capable of consistent detection beyond 40 mm, bolstering the Middle East and Africa proximity sensors market.[3]TotalEnergies, “Riyah 2 Wind Project ESIA Report,” oq.com

*Restraints Impact Analysis

| RESTRAINTS | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE | |||

|---|---|---|---|---|---|---|

Photonic-Sensor Performance Degradation in Desert Dust Conditions Photonic-Sensor Performance Degradation in Desert Dust Conditions | -0.7% | Saudi Arabia, UAE, Egypt, Algeria | Short term (≤ 2 years) | (~) % IMPACT ON CAGR FORECAST:-0.7% | GEOGRAPHIC RELEVANCE:Saudi Arabia, UAE, Egypt, Algeria | IMPACT TIMELINE:Short term (≤ 2 years) |

Volatile Capex Cycles in Sub-Saharan Automotive Tier-2 Suppliers Volatile Capex Cycles in Sub-Saharan Automotive Tier-2 Suppliers | -0.4% | South Africa, Nigeria, Kenya | Medium term (2-4 years) | |||

Low Local Value-Add = High Import Tariffs in Nigeria and Kenya Low Local Value-Add = High Import Tariffs in Nigeria and Kenya | -0.3% | Nigeria, Kenya, Ghana | Long term (≥ 4 years) | |||

Counterfeit Low-Cost Sensors Diluting Brand Premiums (informal trade) Counterfeit Low-Cost Sensors Diluting Brand Premiums (informal trade) | -0.2% | Nigeria, Kenya, informal cross-border trade | Medium term (2-4 years) | |||

| Source: Mordor Intelligence | ||||||

Photonic-sensor performance degradation in desert dust conditions

Severe sandstorms can slash optical-sensor reliability by more than 80%, triggering unplanned stoppages on conveyor and packaging lines. Operators resort to monthly cleaning cycles and protective air-purge systems, lifting the total cost of ownership and restraining wider adoption of photoelectric models within the Middle East and Africa proximity sensors market.

Volatile capex cycles in Sub-Saharan automotive Tier-2 suppliers

Production cuts in South African vehicle plants ripple into the feeder network, extending return-on-investment horizons for automation. Uncertain order books discourage Tier-2 part makers in Nigeria and Kenya from upgrading to advanced sensors, muting a portion of replacement demand.

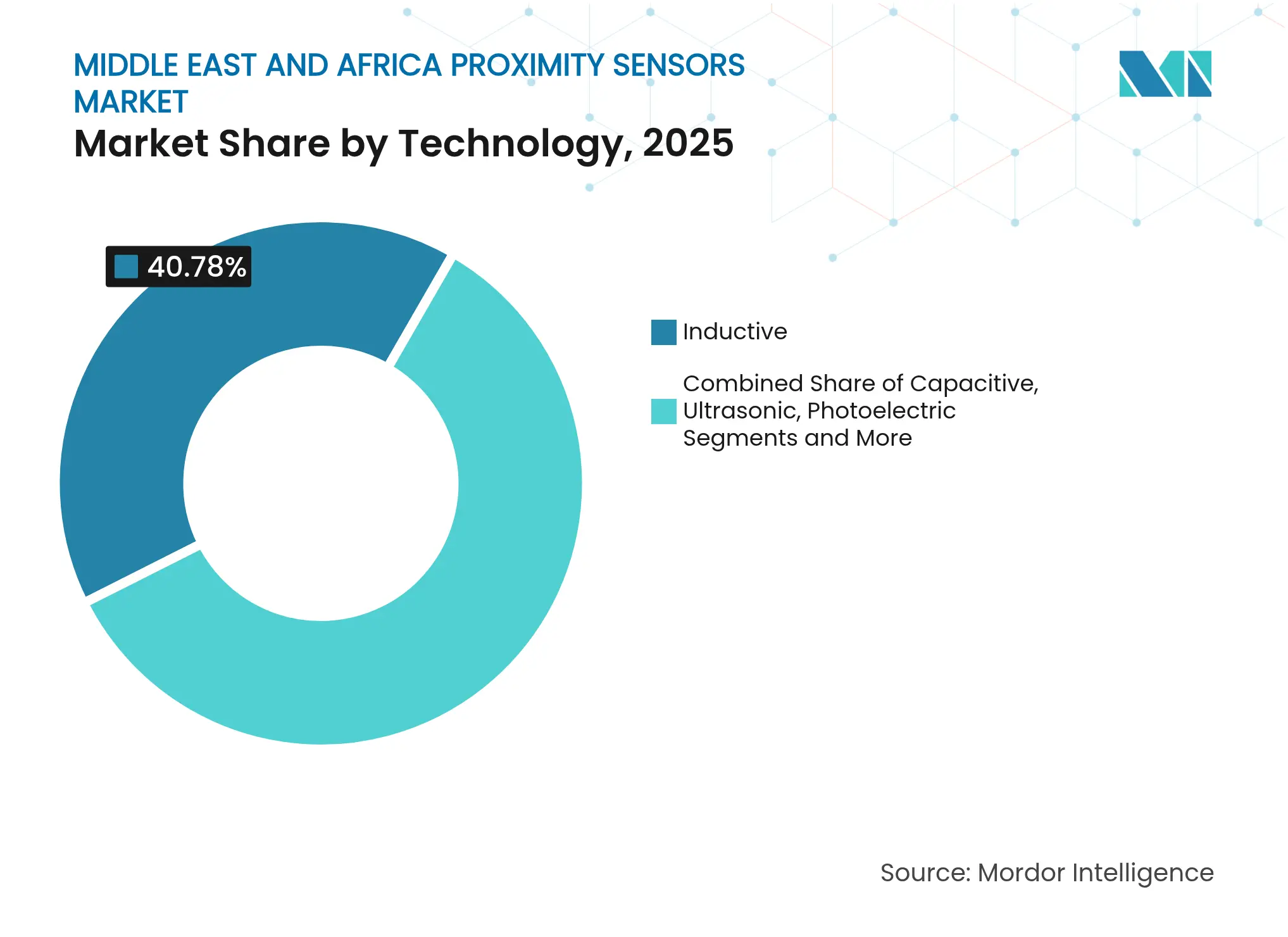

By Technology: Inductive Sensors Protect Reliability in Heavy-Duty Sites

Inductive devices contributed 40.78% to the Middle East and Africa proximity sensors market in 2025, valued at a Middle East and Africa proximity sensors market size of USD 4.16 billion. Their sealed construction eliminates optical windows that accumulate dust, extending mean-time-between-failure in mines and steel mills. Ultrasonic units, though only 14.55% of revenue, are on track for the fastest 9.35% CAGR as wind-energy operators standardise on long-range detection. Photoelectric adoption is restricted by dust-induced false triggers, while capacitive variants retain a foothold in food-and-beverage lines where non-contact level sensing prevents contamination. Magnetic Hall-effect sensors meet niche automotive and marine applications, and emerging eddy-current models serve aerospace composites inspection. Across all formats, native IO-Link support is becoming a decisive purchase criterion, reinforcing the digitalisation theme in the Middle East and Africa proximity sensors market.

Second-generation inductive platforms now bundle on-chip temperature compensation and self-healing algorithms that isolate partial coil faults. Suppliers emphasise conformity to IECEx standards to secure placement in petrochemical zones, a regulatory hurdle that favours established European manufacturers. Meanwhile, Japanese and Korean vendors are expanding regional stockholding to shorten lead times, a key differentiator where project schedules are compressed by government funding milestones.

Note: Segment shares of all individual segments available upon report purchase

By Sensing Range: Long-Range Growth Mirrors Renewable-Energy Build-outs

Short-range models below 10 mm dominated at 48.12% share thanks to high unit volumes on assembly lines and pick-and-place robots. Yet long-range units above 40 mm are forecast to chart an 8.42% CAGR, closing the gap as turbine and utility-scale solar plants specify wider detection envelopes. A 2.9 GW tranche of Saudi wind projects alone will require an incremental 50,000 long-range sensors during 2025-2027. Medium-range devices (10-40 mm) keep a balanced presence in automated storage and packaging systems where conveyor widths vary.

Sensor makers now incorporate micro-power radar for long-range slots, raising competitive pressure on legacy ultrasonic lines. At the ultra-short end, high-frequency capacitive probes are gaining interest for semiconductor backend assembly, an application cluster still nascent in the region but flagged in GCC technology roadmaps.

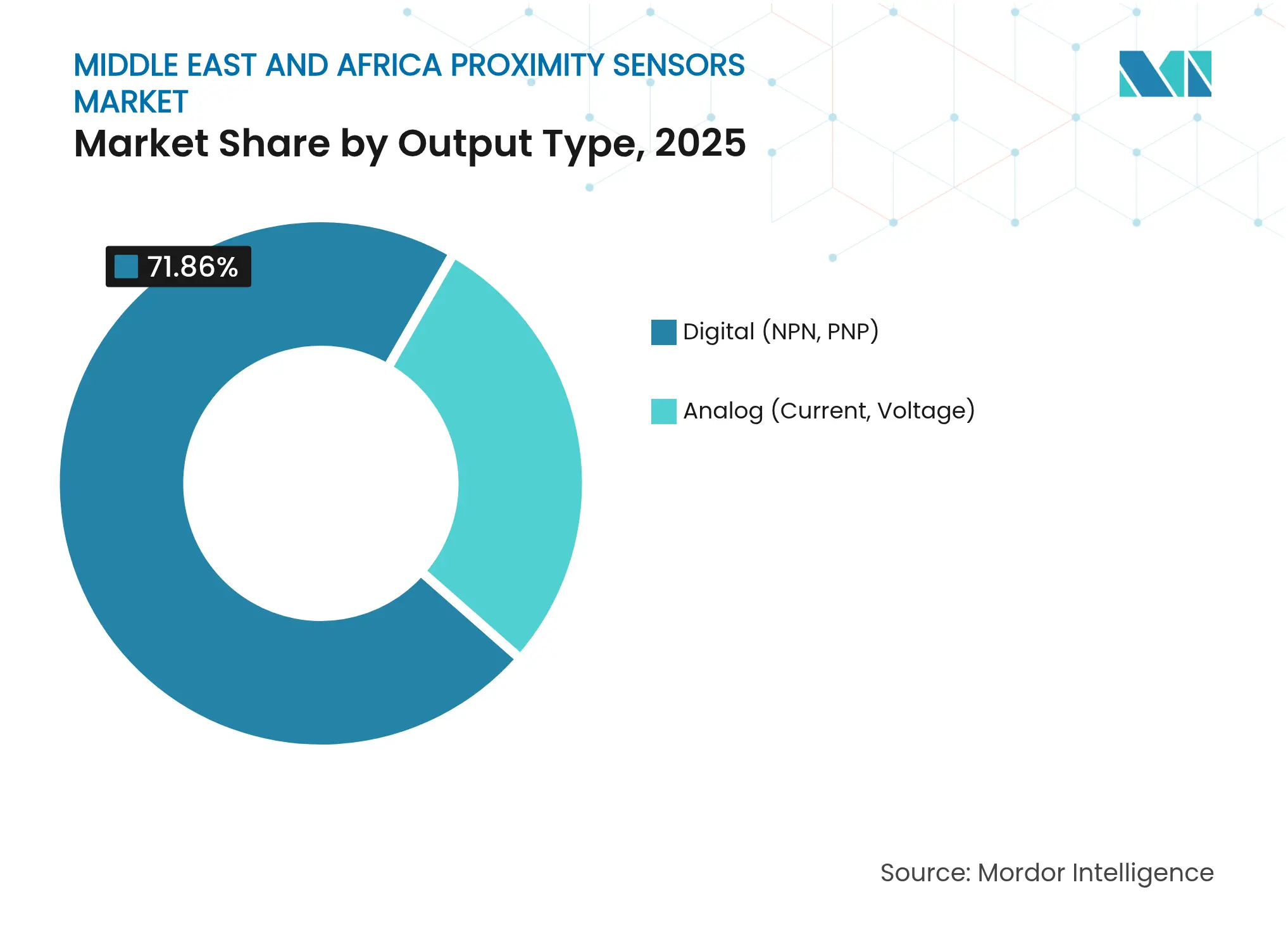

By Output Type: Digital Dominance Anchored by IO-Link Mandates

Digital variants captured a commanding 71.86% of revenue in 2025, underpinned by GCC procurement policies stipulating remote-diagnostics capability. Analog current-loop devices remain prevalent in legacy process plants and are projected to post a respectable 7.24% CAGR as retrofits roll on. The Middle East and Africa proximity sensors market size attributed to digital sensors is expected to top USD 10.62 billion by 2031. Within digital, PNP wiring dominates francophone North Africa due to European equipment lineage, while NPN gains traction in OEM machinery imported from East Asia. Software-defined outputs that allow user-selectable NPN/PNP switching are emerging as a hedge against inventory complexity.

Cyber-secure IO-Link masters, increasingly embedded in PLC racks, are elevating the value proposition of digital sensors. Vendors that couple hardware with dashboard analytics are unlocking subscription revenue streams, signalling a shift from product to service economics in the Middle East and Africa proximity sensors industry.

Note: Segment shares of all individual segments available upon report purchase

By End-User Industry: Renewable Energy Registers the Swiftest Upswing

Industrial manufacturing held 32.88% share in 2025. Automotive lines in Morocco and white-goods factories in Egypt anchor this base. Renewable energy, however, is projected to clock a 9.86% CAGR, buoyed by wind-farm construction in Saudi Arabia and Egypt as well as utility-scale solar parks across the UAE. Food and beverage processors rely on IP69K-rated sensors that endure wash-down cycles, while mining remains a stable adopter of maintenance-free inductive designs. Aerospace and defence projects, concentrated in UAE and Saudi Arabia, demand high-spec magnetic and optical sensors that meet MIL-STD shock benchmarks.

Growing e-commerce activity is stimulating investments in automated fulfilment centres, a nascent but noteworthy channel that could widen the addressable base of the Middle East and Africa proximity sensors market over the long term.

Saudi Arabia remained the largest national market with a 26.74% revenue slice in 2025, propelled by Vision 2030 industrial policies and the USD 500 billion NEOM complex. Localisation rebates for Saudi-assembled sensors, combined with 0% customs duty inside the GCC, sustain high replacement cycles for digital models. The Middle East and Africa proximity sensors market size attributable to the Kingdom is forecast to cross USD 3.9 billion by 2031.

The UAE occupies the second spot, undergirded by its role as a logistics and food-processing hub. Dubai’s ports integrate proximity sensors within automated crane fleets, and Abu Dhabi’s defence cluster specifies MIL-grade devices for UAV platforms. Legislated halal-food automation milestones continue to enlarge baseline demand.

Egypt, posting the region’s fastest 8.32% CAGR, is transitioning wind-resource potential into fabrication of turbine towers and nacelles along the Gulf of Suez. Government-backed industrial parks near Ain Sokhna are wooing component suppliers with ten-year tax holidays, making Egypt a focal point for new entrants to the Middle East and Africa proximity sensors market.

South Africa’s share has softened along with vehicle output declines, yet mining automation offsets part of the drop. De Beers’ offshore diamond vessels use geofenced wearables linked to ship-wide safety systems. Nigeria and Kenya struggle with tariff-inflated landed costs and counterfeit influx, factors that shift procurement toward lower-spec imports.

The Rest of MEA cohort includes Morocco, where the Tanger Med industrial platform hosts growing proximity-sensor integration lines, and Namibia, where uranium mines demand radiation-hardened housings. Overall, geographic diversification cushions macro shocks, keeping the Middle East and Africa proximity sensors market on a steady upward path.

Reports are available across multiple geographies.

Gain in-depth market insights across regions to support informed decisions.

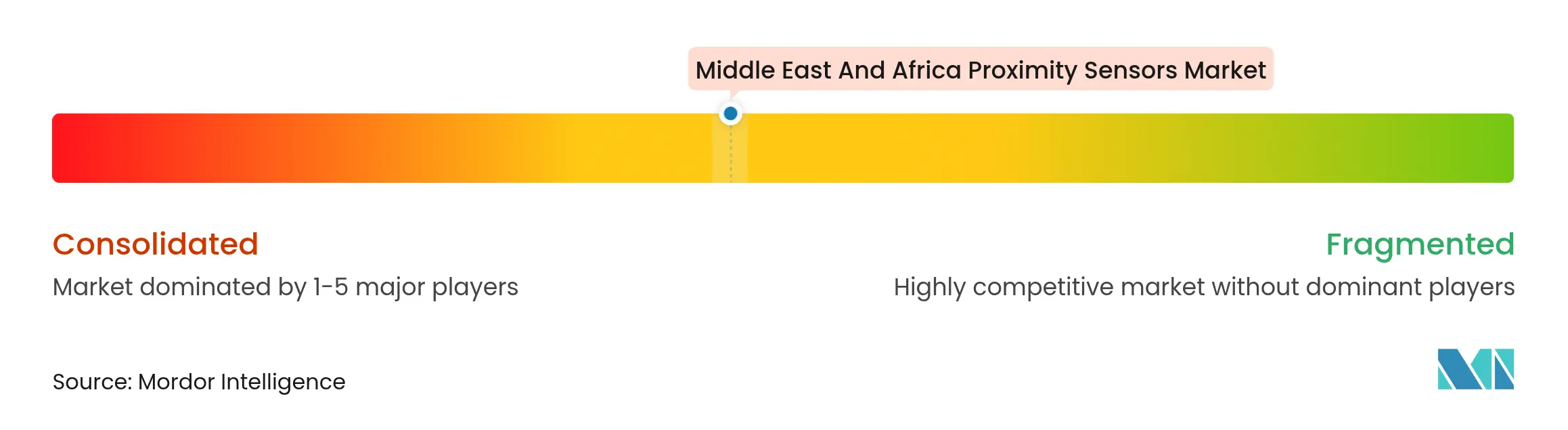

Market Concentration

The supply side features roughly twenty sizeable vendors, none exceeding 12% share, resulting in a market concentration score of 6. European leaders such as SICK AG, ifm electronic and Baumer pair with Japanese giants OMRON and Keyence. Endress+Hauser’s 2025 joint venture with SICK transfers 800 staff to a new entity producing gas analysers and flowmeters for the region’s process industries. This model highlights a trend toward shared localisation to satisfy IECEx and SASO audits.

Honeywell and Danfoss have agreed to co-develop data-integration layers that fuse sensor telemetry with building management platforms. The tie-up targets mining and battery plants where predictive maintenance cuts energy waste. Rockwell Automation’s alliance with NVIDIA on virtual factory acceptance testing demonstrates how software ecosystems influence hardware pull-through.

Product-level differentiation now centres on environmental hardening, with IP67 as a baseline and IP69K favoured in food segments. Suppliers are adding silicon-carbide coating, self-cleaning lenses and condition-based-monitoring chips to justify premium pricing. Wireless variants, though nascent, are emerging for mobile robotics and AGVs in warehouses, giving newer entrants a wedge into the Middle East and Africa proximity sensors market.

*Disclaimer: Major Players sorted in no particular order

1. INTRODUCTION

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET LANDSCAPE

5. MARKET SIZE AND GROWTH FORECASTS (VALUE)

6. COMPETITIVE LANDSCAPE

7. MARKET OPPORTUNITIES AND FUTURE OUTLOOK

A proximity sensor is a sensor that is able to detect the presence of nearby objects without any physical contact. For sensing objects, this sensor radiates or emits a beam of electromagnetic radiation, usually in the form of infrared light, and detects the reflection to determine the object's proximity or distance from the sensor. The scope of the study is comprehensive and is limited to Middle East and Africa.

Pricing Strategy for Semiconductor Components

3 Min Read

Accelerating Additive Manufacturing Adoption in India

3 Min Read

When decisions matter, industry leaders turn to our analysts. Let’s talk.