Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

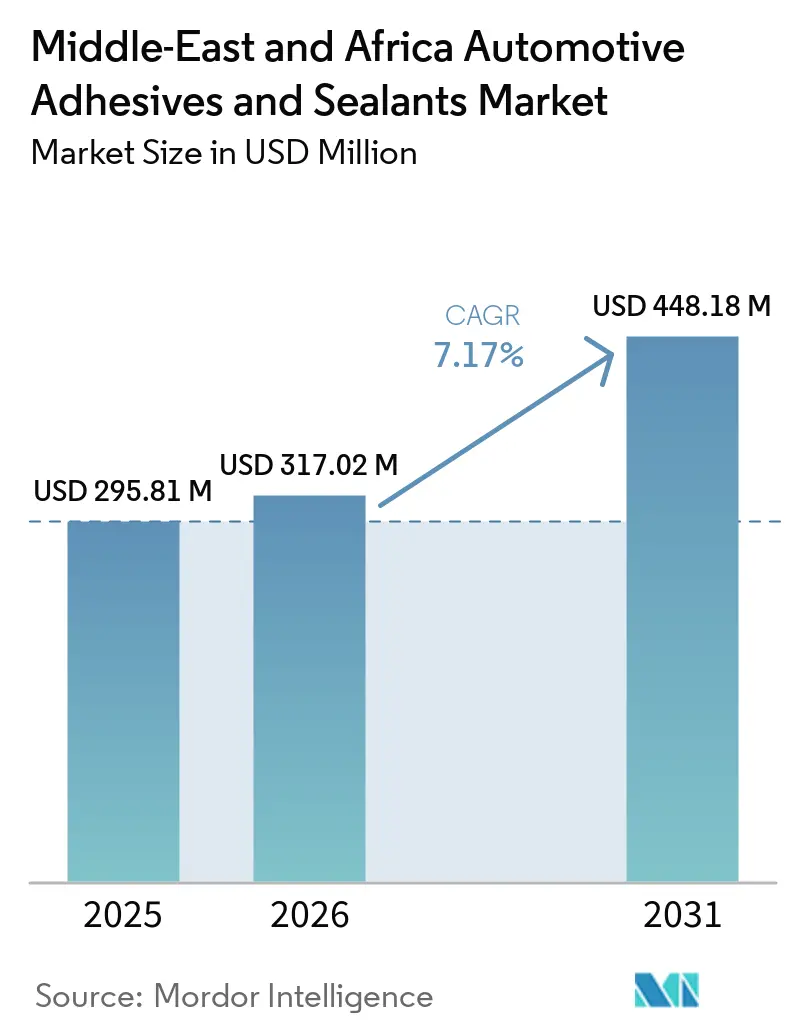

| Base Year Market Size (2025) | USD 295.81 Million |

| Market Size (2026) | USD 317.02 Million |

| Market Size (2031) | USD 448.18 Million |

| Growth Rate (2026 - 2031) | 7.17% CAGR |

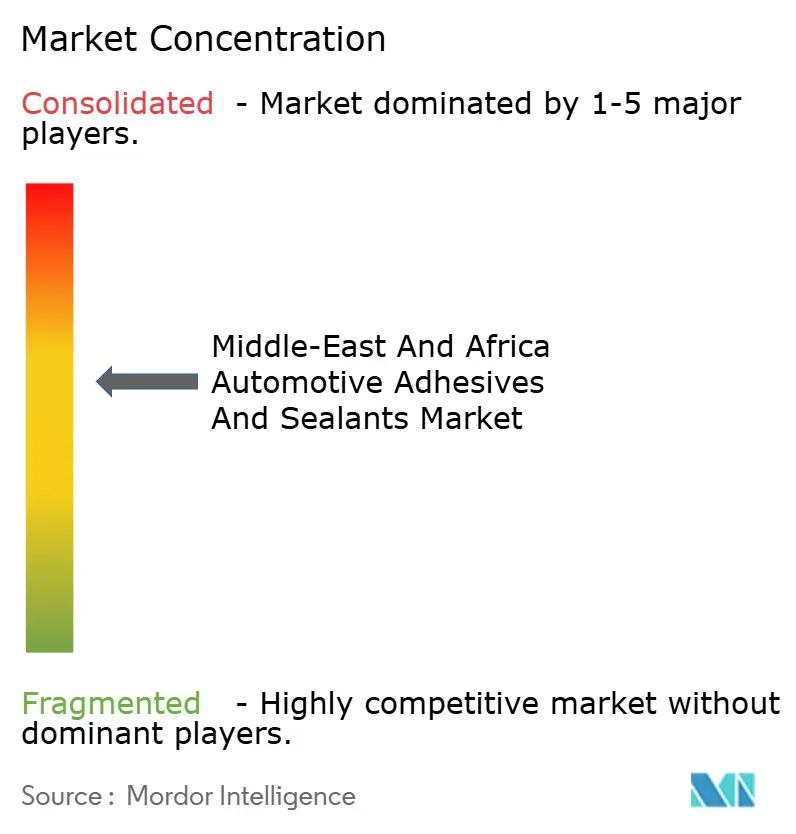

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Middle-East And Africa Automotive Adhesives And Sealants Market Analysis by Mordor Intelligence

The Middle-East And Africa Automotive Adhesives And Sealants Market size is expected to grow from USD 295.81 million in 2025 to USD 317.02 million in 2026 and is forecast to reach USD 448.18 million by 2031 at 7.17% CAGR over 2026-2031. Rising localization mandates above 45% in Saudi Arabia, Egypt, and Morocco are altering tier-1 sourcing strategies and driving the establishment of new blending plants near assembly lines. Stricter volatile-organic-compound (VOC) limits below 100 g/L in the UAE and South Africa are accelerating the shift from solvent-borne to water-borne and hot-melt chemistries. Additionally, the rapid electrification of vehicles is increasing demand for thermally conductive gap fillers that can withstand battery-pack temperatures above 85 °C. Lightweight, multi-material body structures are also driving higher epoxy usage as a replacement for spot welds. While multinational companies dominate OEM contracts, local formulators are gaining market share in the expanding collision-repair segment.

Key Report Takeaways

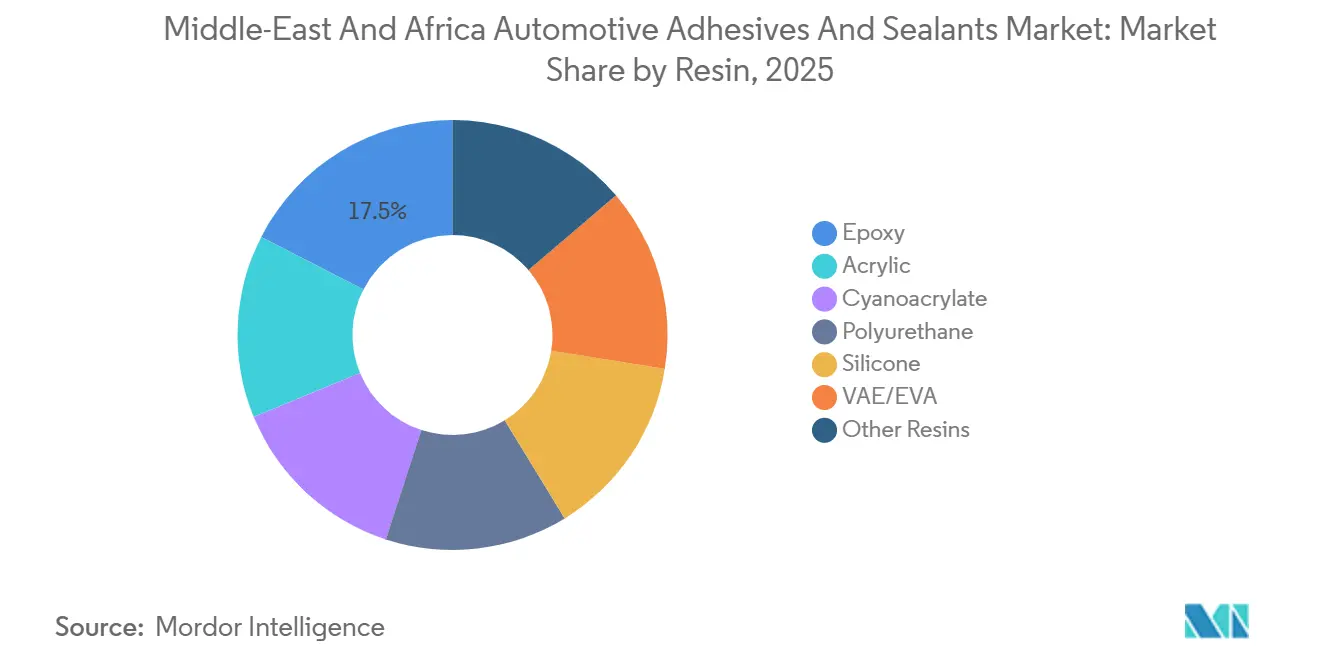

- By resin, epoxy led with 17.46% of the Middle-East and Africa automotive adhesives and sealants market share in 2025, while VAE/EVA resins are forecast to post the fastest 7.31% CAGR through 2031.

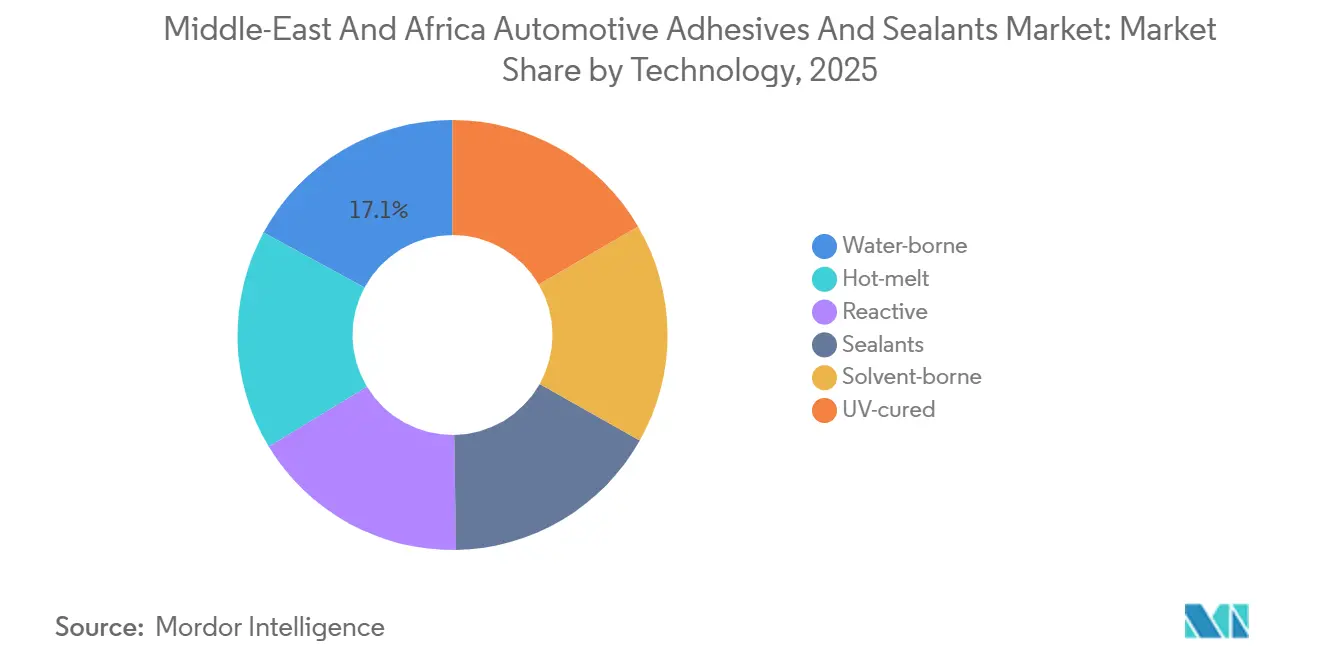

- By technology, water-borne accounted for 17.10% of the Middle-East and Africa automotive adhesives and sealants market share in 2025, while hot-melt is advancing at an 8.38% CAGR through 2031.

- By geography, South Africa held 20.66% of the Middle-East and Africa automotive adhesives and sealants market share in 2025; Saudi Arabia is projected to log the quickest 7.33% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Middle-East And Africa Automotive Adhesives And Sealants Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Lightweighting drive to meet regional CAFÉ-equivalent standards | +1.2% | Saudi Arabia, UAE, South Africa | Medium term (2–4 years) |

| EV battery-pack bonding requirements in hot climates | +1.5% | GCC (Saudi Arabia, UAE, Kuwait), Egypt | Long term (≥4 years) |

| OEM localization policies boosting Tier-1 adhesive sourcing | +1.8% | Saudi Arabia, Egypt, Morocco, South Africa | Short term (≤2 years) |

| Aftermarket collision-repair boom in GCC | +0.9% | GCC (Saudi Arabia, UAE, Kuwait, Qatar) | Short term (≤2 years) |

| Surge in aluminum and multi-material car bodies | +1.1% | Morocco, Saudi Arabia, South Africa | Medium term (2–4 years) |

| Growth of MEA gigafactories for e-mobility | +0.7% | Morocco (Gotion), Egypt (MG, VW), Saudi Arabia (Ceer, Lucid) | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Lightweighting Drive to Meet Regional CAFÉ-Equivalent Standards

Increasing Corporate Average Fuel Economy targets are pushing OEMs to reduce vehicle weight, leading to the substitution of welds with structural epoxies and polyurethanes. These materials provide up to 15% weight savings while maintaining crash energy absorption. For example, a 62% aluminum body-in-white bonded with 180 meters of epoxy reduced curb weight by 100 kg, highlighting the adhesive requirements for mixed-material constructions[1]Henkel, “Lightweighting in Aluminum-Intensive Vehicles,” henkel.com. Regional suppliers co-locating formulation lines near Ceer’s and MG’s new plants secure long-term volumes but must manage higher capital investments to meet local-content thresholds.

EV Battery-Pack Bonding Requirements in Hot Climates

Lithium-ion battery packs operating in ambient temperatures above 50 °C require adhesives with thermal conductivity up to 3.4 W/mK and UL 94 V-0 flame ratings. Two-part polyurethane gap fillers meet these requirements but face challenges such as reduced pot life in non-air-conditioned warehouses. To address this, formulators are extending working times using latent-cure catalysts. Morocco’s 20 GWh LFP cell line alone is expected to consume approximately 2,000 tons of such materials annually, encouraging the setup of on-site mixing stations within the gigafactory premises.

OEM Localization Policies Boosting Tier-1 Adhesive Sourcing

Tax-rebate programs in Egypt and Saudi Arabia provide benefits only if the local content exceeds 45%, prompting five global adhesive manufacturers to establish blending and packaging facilities in King Abdullah Economic City. Contracts mandate 48-hour just-in-time delivery, leading to fragmented production footprints across three countries. This approach helps suppliers mitigate risks related to tariff fluctuations and shipping delays.

Aftermarket Collision-Repair Boom in GCC

The growing vehicle parc and high accident rates are driving demand for OEM-approved structural adhesives in GCC body shops. These adhesives ensure crash-test integrity, and insurance underwriters are increasingly auditing repair procedures. This trend is encouraging workshops to adopt cyanoacrylate instant-bond products with 10-second fixture times, optimizing the use of premium floor space.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile MDI and epoxy raw-material costs | -1.3% | Global, acute in Middle-East and North Africa | Short term (≤2 years) |

| Stringent VOC limits on solvent-borne chemistries | -0.8% | UAE, South Africa, Egypt (emerging) | Medium term (2–4 years) |

| Limited cold-chain logistics for two-part systems | -0.5% | Nigeria, Egypt, Rest of Middle-East and Africa | Medium term (2–4 years) |

| Skilled-labor shortages for automated dispensing | -0.6% | Egypt, Nigeria, Saudi Arabia | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Volatile MDI and Epoxy Raw-Material Costs

Spot prices for methylene diphenyl di-isocyanate (MDI) rose by 5.86% week-on-week in Q1 2026 after a regional force majeure reduced supply by 15%. Epoxy resin prices increased to USD 3.18 per kg, marking a 38.9% year-on-year rise. These cost increases are squeezing formulator margins on fixed-price OEM contracts and accelerating the transition to more cost-effective acrylic and VAE/EVA chemistries.

Stringent VOC Limits on Solvent-Borne Chemistries

UAE regulations capping VOC emissions at 50–100 g/L for primers are driving the need for plant retrofits and reformulations. Smaller regional players are struggling to finance the spray-booth upgrades required to adopt compliant water-borne systems[2]Ministry of Energy & Infrastructure UAE, “VOC Emission Standards,” moei.gov.ae.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Resin: Structural Epoxy Dominance and VAE/EVA Momentum

Epoxy resins held 17.46% of the Middle-East and Africa automotive adhesives and sealants market share in 2025, attributed to their 25 MPa lap-shear strength and 180 °C service temperature, which are essential for aluminum-steel assemblies in new EV platforms. Meanwhile, polyurethane and silicone chemistries continue to serve specific applications such as glazing and under-hood gaskets, where elastic recovery or continuous exposure to 150 °C is required.

VAE/EVA resins are projected to grow at the fastest CAGR of 7.31% through 2031, driven by their sub-3-second set times and zero-VOC emissions, making them suitable for hot-melt headliner and carpet-backing applications. Enhanced hydrolysis resistance in advanced VAE grades supports their use in humid coastal regions while meeting interior-odor standards, creating opportunities in door-panel lamination and pillar trims.

By Technology: Water-Borne Compliance and Hot-Melt Acceleration

Water-borne accounted for 17.10% of 2025 revenue due to their compliance with VOC regulations in the UAE and South Africa, while also eliminating flammability risks. Emerging styrene-acrylic and VAE emulsions are replacing solvent-based systems in applications such as seat-foam fabric lamination and acoustic felt bonding. In contrast, hot-melt technology is expected to grow at an 8.38% CAGR through 2031, as OEMs prioritize faster production speeds. UV-curable hot-melt adhesives achieve full bond strength in 10 seconds, enabling immediate module removal from fixtures. Reactive two-part epoxies and polyurethanes remain essential for battery modules, offering 1,000-cycle thermal-fatigue resistance. However, suppliers are reformulating these adhesives with latent catalysts to extend pot life in uncooled storage environments.

Geography Analysis

South Africa contributed 20.66% of 2025 sales, supported by its established supplier base and a vehicle output of 599,754 units, despite a slight decline. Local content stagnated at 39%, providing opportunities for adhesive manufacturers to secure design-in slots before model platforms finalize specifications for the 2030 cycle. New-energy vehicle penetration reached 3% in 2024, driving demand for battery-pack gap fillers and flame-retardant potting materials in Gauteng and Eastern Cape production facilities.

Saudi Arabia will achieve the region’s fastest CAGR of 7.33% through 2031, as Ceer and Lucid scale their combined production capacity to 50,000 vehicles annually by 2026. TASARU Supplier Hub agreements require five major adhesive manufacturers to blend locally and deliver within 48 hours, supporting a just-in-time supply chain aligned with CAFE-driven lightweighting initiatives. These efforts are expected to increase material intensity from 8 kg to as much as 15 kg per vehicle. Feasibility studies by Hyundai and Stellantis could potentially double assembly volumes and adhesive demand by 2028.

Egypt, the UAE, and Nigeria represent the next wave. Egypt’s Automotive Industry Development Program secured USD 135 million for the MG plant, set to begin operations in Q2 2026, and Volkswagen’s East Port Said body shop. These facilities will require local sealant and masking-tape suppliers but face a 12-month skills gap in robot programming. In Nigeria, the Kaduna line relaunch highlights policy risks, as multiple-tax regimes and grid instability deter larger OEM investments despite strong domestic vehicle demand. Morocco, with a production capacity of 1 million units, benefits from Stellantis Kenitra and Tesla’s announced plans, positioning the Kenitra-Rabat corridor as a hub for battery-pack bonding chemistries.

Competitive Landscape

The market is moderately concentrated. Major players include Henkel, Sika, Arkema, H.B. Fuller Company, and Dow. Regional players such as ACC Gulf, Pidilite, and Mapei dominate the aftermarket segment through extensive distributor networks. BASF’s Durban reactor expansion, scheduled for March 2026, includes a climate-simulation lab to customize dispersions for tropical humidity, reflecting the localization strategies of major players. Sika’s pumpable baffle adhesive integrates bonding, acoustic damping, and corrosion protection, reducing assembly steps and enhancing lightweighting benefits.

Innovative solutions are focusing on recyclability. Arkema’s debond-on-command primer allows heat-triggered separation at end-of-life, aligning with emerging take-back regulations in South Africa. Suppliers are also incorporating robotics into their technology roadmaps, co-developing vision-guided applicators with ABB and KUKA to secure line integrations 18 months before start-of-production. Portfolio consolidation continues, as evidenced by Arkema’s acquisition of Dow’s laminating-adhesive unit for USD 150 million, leveraging shared blending lines across automotive, industrial, and flexible-packaging applications.

Middle-East And Africa Automotive Adhesives And Sealants Industry Leaders

Dow

H.B. Fuller Company

Henkel AG & Co. KGaA

Sika AG

Arkema

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Sika AG acquired Akkim, a Turkey-based manufacturer of adhesives and sealants, to enhance its distribution network and production capacity in high-growth markets. The acquisition integrated Akkim’s extensive manufacturing capabilities with Sika AG’s global operations to serve regions including the Middle-East and Africa.

- May 2025: H.B. Fuller Company inaugurated a new manufacturing facility in Cairo, Egypt, located within the CPC Industrial Park in the 6th of October Industrial City. The two-story facility, spanning 37,000 m², doubled the company’s production capacity in the region and featured both pressure-sensitive adhesive (PSA) and non-PSA hot melt adhesive production capabilities.

Middle-East And Africa Automotive Adhesives And Sealants Market Report Scope

Adhesives and sealants are substances used to join surfaces, but they serve distinct purposes and possess different physical properties. Adhesives are formulated to bond two materials permanently, creating a high-strength connection capable of withstanding mechanical loads such as shear and tensile forces. They are typically applied in liquid form and cure into a rigid or semi-rigid solid. Sealants, on the other hand, are primarily used to fill gaps, joints, or seams, forming a barrier against moisture, air, dust, and sound. They are generally more viscous and remain highly flexible after curing, enabling them to accommodate movement and thermal expansion between substrates.

The Middle-East And Africa Automotive Adhesives And Sealants Market is segmented into resin, technology, and geography. By resin, the market is segmented into epoxy, acrylic, cyanoacrylate, polyurethane, silicone, VAE/EVA, and other resins. By technology, the market is segmented into water-borne, hot-melt, reactive, sealants, solvent-borne, and UV-cured. The report also covers the market size and forecasts for automotive adhesives and sealants in 5 countries across the region. For each segment, the market sizing and forecasts have been done on the basis of value (USD).

By Resin

| Epoxy |

| Acrylic |

| Cyanoacrylate |

| Polyurethane |

| Silicone |

| VAE/EVA |

| Other Resins |

By Technology

| Water-borne |

| Hot-melt |

| Reactive |

| Sealants |

| Solvent-borne |

| UV-cured |

By Geography

| Saudi Arabia |

| South Africa |

| United Arab Emirates |

| Egypt |

| Nigeria |

| Rest of Middle-East and Africa |

| By Resin | Epoxy |

| Acrylic | |

| Cyanoacrylate | |

| Polyurethane | |

| Silicone | |

| VAE/EVA | |

| Other Resins | |

| By Technology | Water-borne |

| Hot-melt | |

| Reactive | |

| Sealants | |

| Solvent-borne | |

| UV-cured | |

| By Geography | Saudi Arabia |

| South Africa | |

| United Arab Emirates | |

| Egypt | |

| Nigeria | |

| Rest of Middle-East and Africa |

Market Definition

- End-user Industry - In the automotive industry, both the OEM and after market adhesive and sealants applications are considered under the scope.

- Product - All adhesive and sealant products used in automotive industry are considered in the market studied

- Resin - Under the scope of the study, resins like Polyurethane, Epoxy, Acrylic, Cyanoacrylate, VAE/EVA, and Silicone are considered

- Technology - For the purpose of this study, Water-borne, Solvent-borne, Reactive, Hot Melt, UV Cured Adhesives, and Sealants technologies are taken into consideration.

| Keyword | Definition |

|---|---|

| Hot-melt Adhesive | Hot melt adhesives are generally 100% solid formulations, based on thermoplastic polymers. They are solid at room temperature and are activated upon heating above their softening point, at which stage they are liquid, and hence, can be processed. |

| Reactive Adhesive | A reactive adhesive is made up of monomers that react in the adhesive curing process and do not evaporate from the film during use. Instead, these volatile components become chemically incorporated into the adhesive. |

| Solvent-borne Adhesive | Solvent-borne adhesives are mixtures of solvents and thermoplastic, or slightly cross-linked polymers, such as polychloroprene, polyurethane, acrylic, silicone, and natural and synthetic rubbers (elastomers). |

| Water-borne Adhesive | Water-borne adhesives use water as a carrier or diluting medium to disperse a resin. They are set by allowing the water to evaporate or be absorbed by the substrate. These adhesives are compounded with water as a diluent, rather than a volatile organic solvent. |

| UV Cured Adhesive | UV curing adhesives induce curing and create a permanent bond without heating by using ultraviolet (UV) light or other radiation sources. An aggregation of monomers and oligomers is cured or polymerized by ultraviolet (UV) or visible light in a UV adhesive. Because UV is a radiating energy source, UV adhesives are often referred to as radiation curing or rad-cure adhesives. |

| Heat-resistant Adhesive | Heat-resistant Adhesives refer to those that do not break down under high temperatures. One aspect of a complicated system of circumstances is the adhesive's capacity to withstand disintegration brought on by high temperatures. As the temperature rises, adhesives may liquefy. They can withstand stresses resulting from differing coefficients of expansion and contraction, which might be an additional advantage. |

| Reshoring | Reshoring is the practice of moving commodity production and manufacturing back to the nation where the business was founded. Onshoring, inshoring, and back shoring are further terms used. Offshoring, the practice of producing items abroad to lower labor and manufacturing costs, is the opposite of this. |

| Oleochemicals | Oleochemicals are compounds produced from biological oils or fats. They resemble petrochemicals, which are substances made from petroleum. The oleochemical business is built on the hydrolysis of oils or fats. |

| Nonporous Materials | Nonporous materials are substances that do not permit the passage of liquid or air. Nonporous materials are those that are not porous, such as glass, plastic, metal, and varnished wood. Since no air can get through, less airflow is required to raise these materials, negating the requirement for high airflow. |

| EU-Vietnam Free Trade Agreement | A trade agreement and an investment protection agreement were concluded between the European Union and Vietnam on June 30, 2019. |

| VOC content | Compounds with limited solubility in water and high vapor pressure are known as Volatile Organic Compounds (VOCs). Many VOCs are human-made chemicals that are used and produced in the manufacture of paints, pharmaceuticals, and refrigerants. |

| Emulsion Polymerization | Emulsion polymerization is a method of producing polymers or connected groups of smaller chemical chains known as monomers, in a water solution. The method is often used to make water-based paints, adhesives, and varnishes, in which the water stays with the polymer and is marketed as a liquid product. |

| 2025 National Packaging Targets | In 2018, the Australian Environment Ministry set the following 2025 National Packaging Targets: 100% of the packaging must be reusable, recyclable, or compostable by 2025, 70% of plastic packaging must be recycled or composted by 2025, 50% of average recycled content must be included in packaging by 2025, and problematic and unnecessary single-use plastic packaging must be phased out by 2025. |

| Russian Government’s Import Substitution Policy | The Western sanctions suspended the distribution of several high-tech items to Russia, including those required by the raw material export sectors and the military-industrial complex. In response, the government launched an "import substitution" scheme, appointing a special commission to oversee its implementation in early 2015. |

| Paper Substrate | Paper substrates are paper sheets, reels, or boards with a base weight of up to 400 g/m2 that has not been converted, printed or otherwise altered. |

| Insulation Material | A material that inhibits or blocks heat, sound, or electrical transmission is known as Insulation Material. The variety of insulation materials includes thick fibers like fiberglass, rock and slag wool, cellulose, and natural fibers as well as stiff foam boards and sleek foils. |

| Thermal Shock | A temperature change known as thermal shock generates stress in a material. It commonly results in material breakdown and is especially prevalent in brittle materials like ceramics. When there is a quick temperature change, either from hot to cold or vice versa, this process occurs abruptly. It occurs more frequently in materials with poor heat conductivity and insufficient structural integrity. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: The quantifiable key variables (industry and extraneous) pertaining to the specific product segment and country are selected from a group of relevant variables & factors based on desk research & literature review; along with primary expert inputs. These variables are further confirmed through regression modeling (wherever required).

- Step-2: Build a Market Model: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms