Market Overview

| Study Period | 2020 - 2031 |

|---|---|

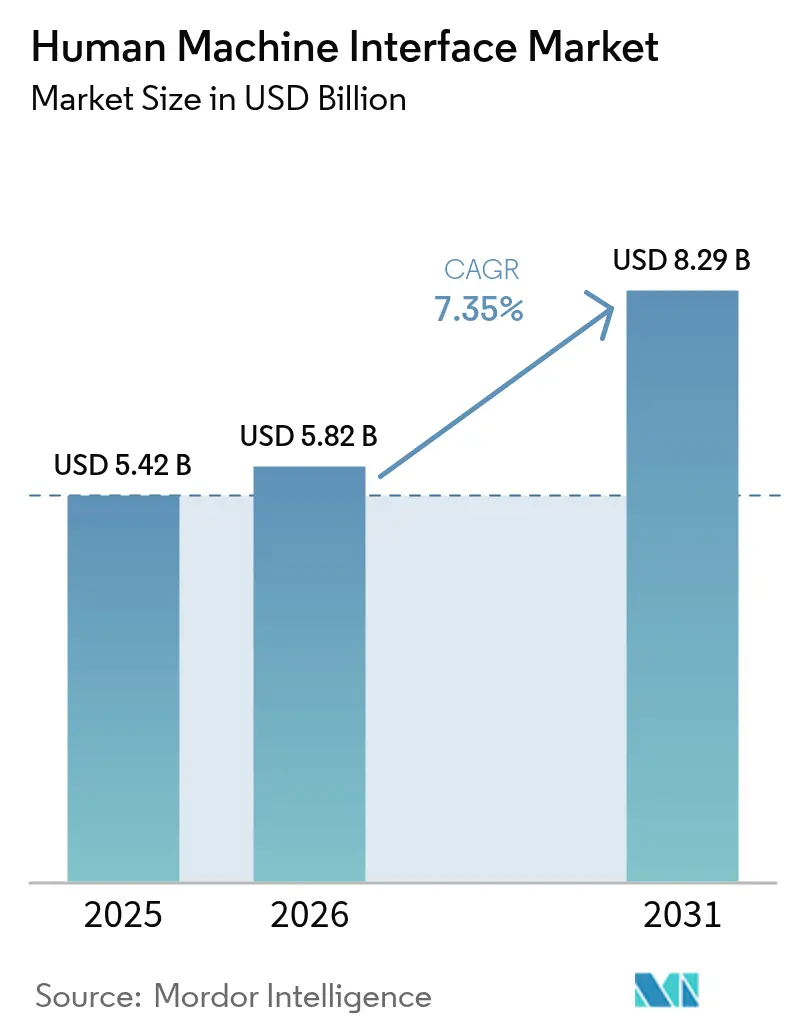

| Market Size (2026) | USD 5.82 Billion |

| Market Size (2031) | USD 8.29 Billion |

| Growth Rate (2026 - 2031) | 7.35% CAGR |

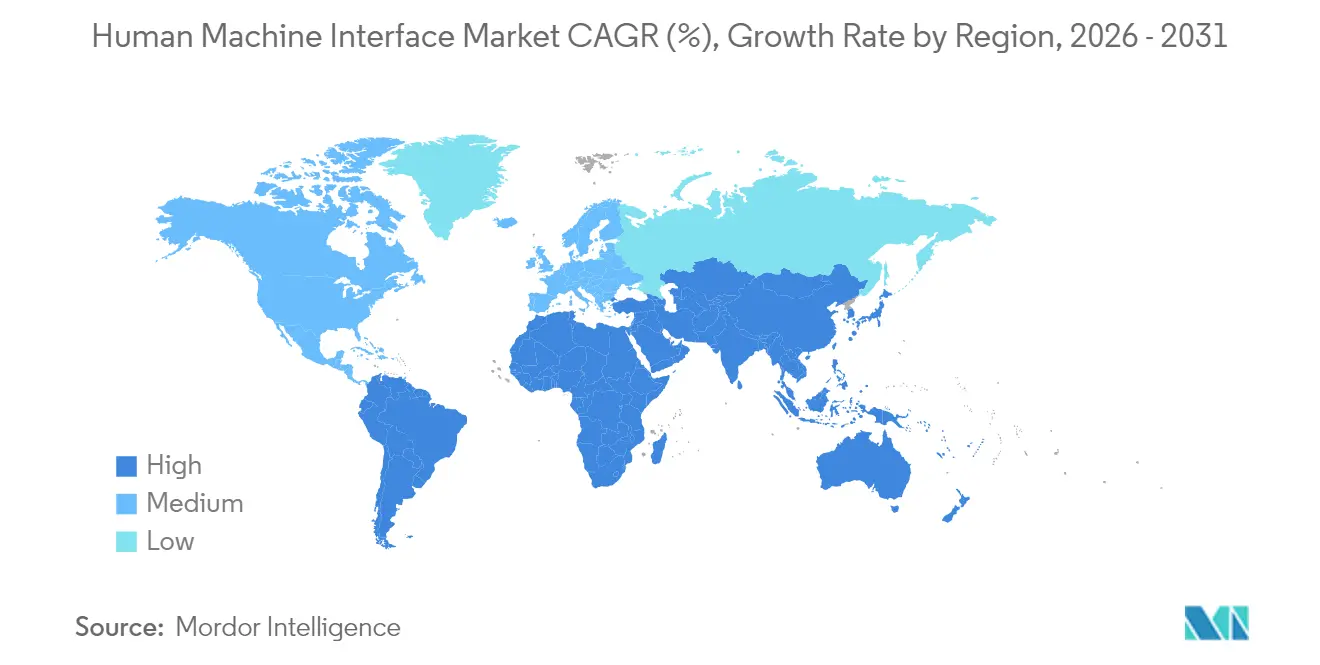

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

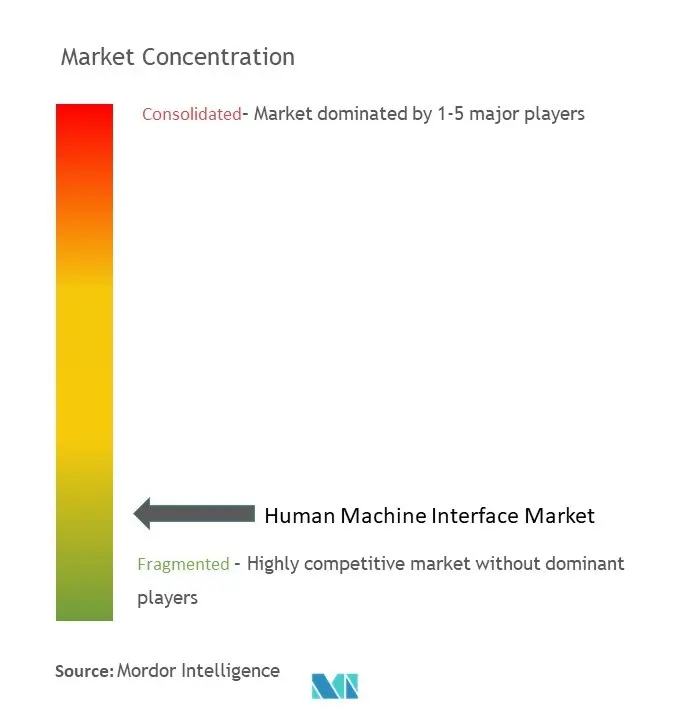

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Human Machine Interface Market Analysis by Mordor Intelligence

HMI market size in 2026 is estimated at USD 5.82 billion, growing from 2025 value of USD 5.42 billion with 2031 projections showing USD 8.29 billion, growing at 7.35% CAGR over 2026-2031. Strong factory digitalization programs, expanding OT-IT integration, and the shift toward human-centric Industry 5.0 production models are the core demand catalysts. Investments in edge-connected panels, immersive visualization, and secure-by-design architectures continue to rise as manufacturers prioritize real-time insight, lower downtime, and workforce productivity. Hardware retains a clear lead thanks to purpose-built industrial PCs and panels, yet software-defined HMIs and low-code configuration tools are accelerating adoption among smaller plants. Regionally, the HMI market benefits most from large-scale automation in Asia-Pacific and rapid modernization programs in the Middle East & Africa, while North America and Europe focus on cybersecurity compliance and advanced analytics integration. [1]Siemens, “Senseye Predictive Maintenance,” siemens.com

Key Report Takeaways

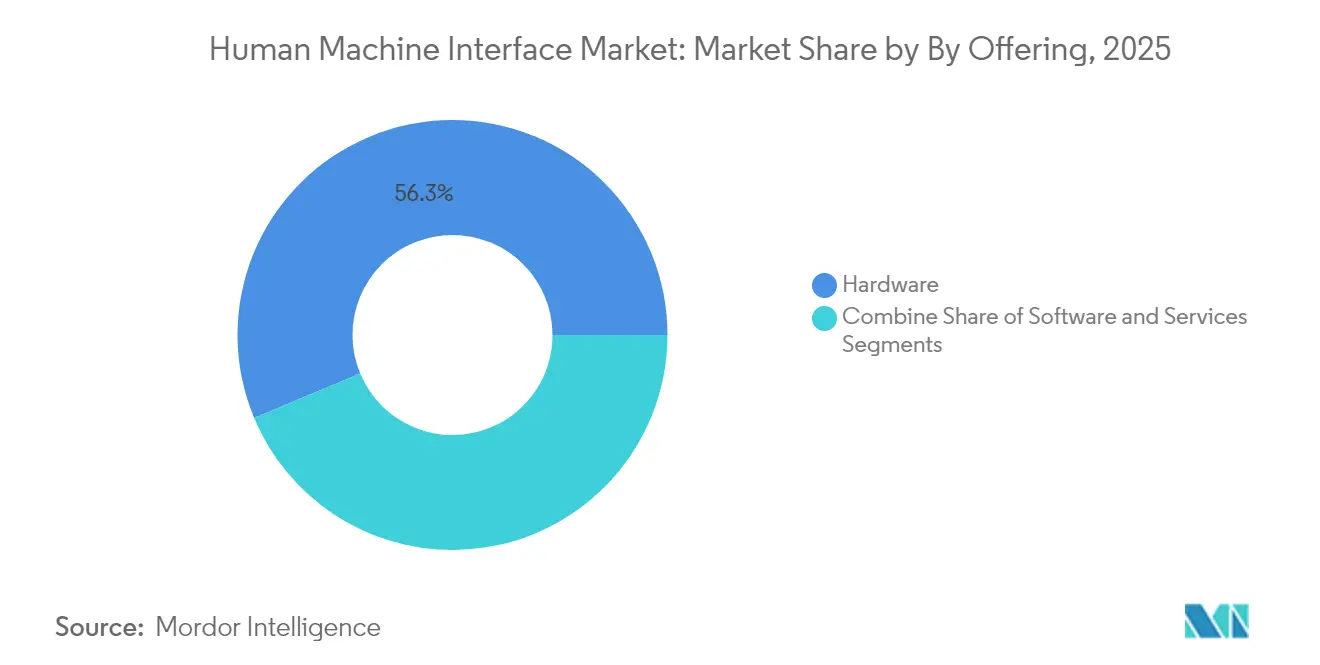

- By offering, hardware commanded 56.30% of the HMI market share in 2025, while services are projected to expand at an 10.94% CAGR to 2031.

- By interface technology, touchscreens held 70.40% revenue share in 2025; AR/VR-assisted interfaces are advancing at an 17.62% CAGR through 2031.

- By configuration, embedded solutions accounted for 45.30% of the HMI market size in 2025; distributed or remote HMIs are growing at a 11.85% CAGR to 2031.

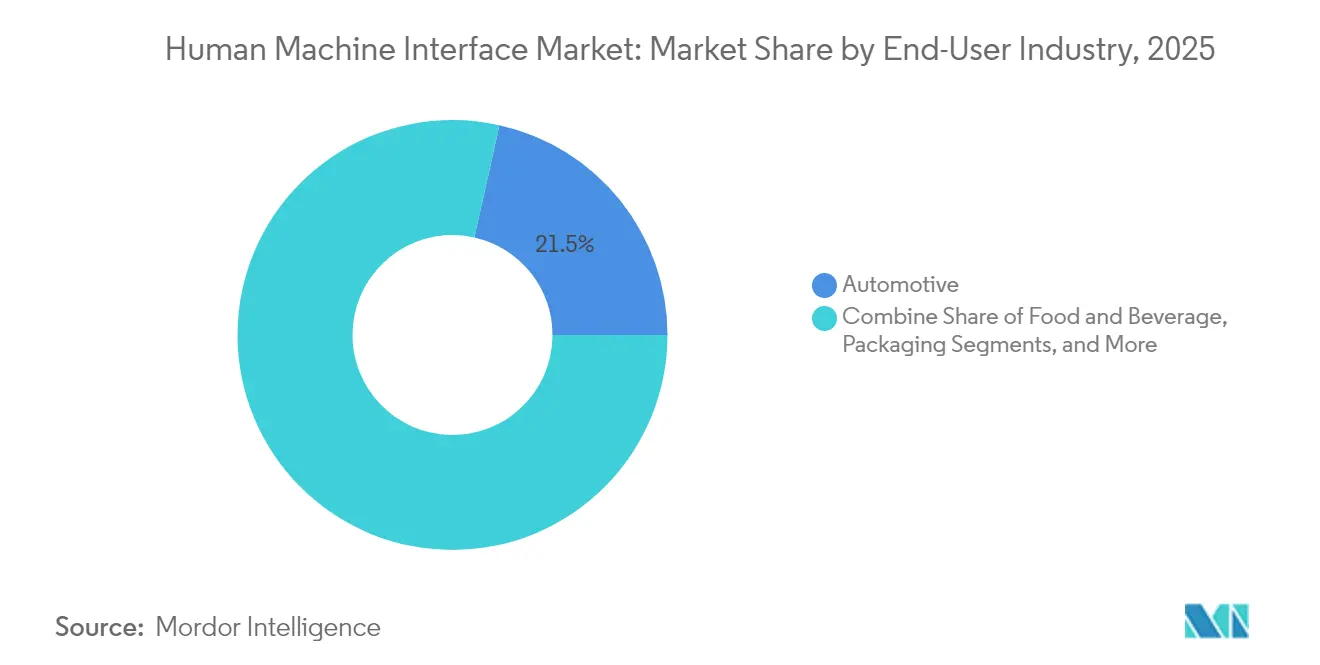

- By end-user, automotive led with 21.50% share of the HMI market size in 2025, while semiconductor & electronics is forecast to grow at a 10.15% CAGR.

- By region, Asia-Pacific captured 37.60% of the HMI market share in 2025; the Middle East & Africa region records the highest CAGR at 9.25% to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Human Machine Interface Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerated Industry 4.0 adoption | +2.1% | APAC, Europe, North America | Medium term (2-4 years) |

| Convergence of OT-IT cybersecurity demands | +1.8% | North America, Europe, expanding APAC | Medium term (2-4 years) |

| Edge-AI enabling predictive UX | +1.6% | North America, Europe, advanced APAC economies | Long term (≥ 4 years) |

| Low-code or no-code HMI configuration tools | +1.3% | Early adoption in North America, spreading globally | Short term (≤ 2 years) |

| Energy-efficient industrial displays | +0.7% | Europe, North America, Japan | Medium term (2-4 years) |

| 5G-enabled ultra-low-latency remote HMI | +0.5% | North America, Europe, China, South Korea | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Accelerated Industry 4.0 adoption

Industry 4.0 programs transform HMIs from passive displays into data-driven command hubs that aggregate sensor, MES, and ERP feeds into context-aware dashboards. In many plants, operators now use HMIs to orchestrate co-bots, coordinate batch changes, and launch predictive maintenance workflows. A 2025 MDPI study highlights Industry 5.0’s emphasis on collaborative robots, noting that intuitive HMIs are essential for seamless human-machine teamwork. Siemens reported its Senseye platform prevented costly downtime at a dairy facility through AI-enabled anomaly alerts, demonstrating tangible ROI for connected HMIs.

Convergence of OT-IT cybersecurity requirements

Remote connectivity and enterprise cloud links expose legacy panels to modern attack surfaces, prompting a move toward Zero Trust Architecture. The European Union’s NIS2 directive compels critical-infrastructure operators to adopt strict authentication and role-based controls on every HMI node. Telefónica Tech underscores that multi-factor authentication and continuous verification are quickly becoming baseline interface functions. Vendors now embed secure boot, signed firmware, and encrypted protocols to satisfy these mandates.

Edge-AI enabling predictive UX

Local inference engines running on AI-focused microprocessors adjust screen layouts, prioritize alerts, and even enable hands-free voice or gesture commands. A 2025 ScienceDirect paper showed a wearable AR interface powered by edge analytics cut error rates by 22.3% and lifted task speed by 31.1%. Texas Instruments’ AM6x family integrates dedicated AI accelerators that support such adaptive capabilities with industrial temperature tolerances. [2]Texas Instruments, “AM6x Processors for Industrial HMI,” ti.com

Low-code/no-code HMI configuration tools

Drag-and-drop builders allow subject-matter experts to customize dashboards, reducing coding cycles and boosting agility. Rockwell Automation’s FactoryTalk Optix lets engineers assemble browser-based screens and push updates across plants without recompiling binaries.

Persistent legacy PLC installed base

Older controllers lack modern protocols, creating integration hurdles. Plants hesitate to rip and replace mature assets, instead layering protocol gateways that add cost and complexity. Food Engineering notes version-control headaches when proprietary buses clash with modern OPC UA or MQTT frameworks.

Supply-chain volatility for specialty semiconductors

New import tariffs and limited foundry capacity have extended lead times for industrial-grade touch controllers to 12–16 weeks in early 2025. Rugged HMI vendors redesign boards around commodity chipsets, yet those swaps sometimes raise power draw or cut display refresh rates.

*Our updated forecasts treat driver/restraint impacts as directional, not additive. The revised impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Offering: Hardware dominance meets service-led growth

Hardware generated 56.30% of the HMI market in 2025 as rugged panels, industrial PCs, and edge gateways remain mission critical. Texas Instruments confirms a pivot toward embedded AI to balance deterministic control with predictive analytics. The services segment, advancing at 10.94% CAGR, reflects mounting demand for integration, cybersecurity hardening, and continuous training. Control Global observes suppliers shifting from one-off projects to lifecycle partnerships with subscription models for interface optimization.

Hardware evolution now favours modular boards, and high brightness displays certified for Class I, Division 2 zones. Vendors integrate hot-swap SSD bays and field-upgradeable CPUs to extend lifespan. Meanwhile, managed services teams conduct remote UX audits, patch critical vulnerabilities, and retrain operators to exploit new features, a dynamic expected to lift service revenues to nearly one third of overall HMI market size by 2031.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Interface Technology: Touchscreens lead, AR/VR accelerates

Touchscreens retained 70.40% of the HMI market in 2025 because glove-friendly capacitive layers and chemically strengthened glass satisfy harsh-plant demands. Multi-touch gestures shorten navigation time and cut error rates, especially in batch changeovers. Yet AR/VR interfaces are scaling fastest at 17.62% CAGR, reshaping operator interaction paradigms. An MDPI study on XR-based robot programming reported faster commissioning and lower downtime than traditional pendant methods.

AR-equipped headsets provide spatial overlays, letting technicians visualize hidden piping, torque targets, or live analytics. Automotive OEMs run immersive design reviews that replace clay modelling and shorten concept loops. This cross-pollination of gaming engines and industrial data paves the way for spatial computing control rooms, potentially capturing an expanded share of HMI market size through 2031.

By End-User Industry: Automotive scale, semiconductor precision

Automotive plants held 21.50% of the HMI market size in 2025 because of high robot density and weekly model changeovers. XR walk-throughs help engineers optimize line ergonomics and quality gates before physical tooling is complete. Aquent highlights immersive visualization’s role in trimming prototyping costs by double-digit percentages.

Semiconductor & electronics fabrication is the fastest-growing end user at 10.15% CAGR. ASML’s multibeam eScan1000 wafer-inspection tool marries sub-nanometre precision with advanced HMI surfaces that allow engineers to analyse 3D defect maps in near real time. Cleanroom regulations demand fangless, low-outgassing panels with sealed USB-C service ports. These specialized requirements explain the segment’s outsized momentum in capturing additional HMI market share through 2031.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Configuration: Embedded cohesion to distributed agility

Embedded HMIs held 45.30% of the HMI market size in 2025 due to tight PLC integration and deterministic response. Panel-mounted units typically boot from flash in under five seconds and maintain IP65-rated enclosures. Research in modular industrial PCs reveals a clear trend toward separating display and compute elements, simplifying on-site upgrades while retaining environmental seals.

Distributed architectures are advancing at 11.85% CAGR. PlantPAx implementations demonstrate that browser-rendered graphics delivered over secured Ethernet allow centralized experts to guide multiple facilities. Private 5G backbones unlock remote machinery control for mines and oil platforms, redefining disaster-recovery strategies and cutting travel costs. This transition underscores how the HMI market balances latency constraints with workforce distribution.

Geography Analysis

Asia-Pacific led the HMI market with 37.60% share in 2025. Chinese installations surpassed 18.25 million units, generating revenue of CNY 9.28 billion (USD 1.39 billion) amid a climb in smart-factory rollouts. Japan and South Korea continue to commercialize next-gen OLED panels, while India’s production-linked incentives propel automation uptake in pharmaceuticals and consumer durables. Regional suppliers such as Delta Electronics are scaling local manufacturing, widening access to cost-competitive panels.

The Middle East and Africa registers the highest growth at 9.25% CAGR. Vision 2030 initiatives in Saudi Arabia and the UAE’s Operation 300bn plan are investing in digital plants for petrochemicals, logistics, and renewables. The Future Manufacturing Africa Conference spotlights AI-driven quality control and workforce upskilling for automation, signalling sustained large-project pipelines.

North America benefits from reshoring incentives and an established industrial-software ecosystem. Platforms like Ignition by Inductive Automation employ unlimited licensing to cut total cost of ownership for multi-site rollouts. Cybersecurity regulations such as CISA guidelines fuel adoption of secure-boot HMIs, further solidifying market demand across defence and critical-infrastructure verticals.

Europe maintains a sizeable slice of the HMI market on the back of regulatory rigor and sustainability leadership. Compliance with NIS2 and eco-design mandates drives preference for energy-efficient, IEC 62443-certified panels. Siemens’ USD 2 billion European investment into digital-center expansions underscores the continent’s determination to lead in human-centric, low-carbon industry.

Get Analysis on Important Geographic Markets

Download PDF

Competitive Landscape

The five largest vendors control roughly 45% of global revenue, confirming a fragmented yet contestable HMI market. Siemens is infusing artificial-intelligence co-pilots into engineering suites, positioning HMIs as agents that execute tasks autonomously and learn continuously. Rockwell Automation promotes an open, modular FactoryTalk Optix portfolio that decouples graphics, data models, and deployment targets, offering users cloud, edge, or panel options.

ABB plans to float its robotics unit to sharpen focus and speed investments in next-generation interfaces that blend robot path editing with real-time production analytics. GE Vernova’s Proficy update brings native HTML5 and cloud-ready deployment to 20,000 clients across oil and gas, food and beverage, and pharmaceuticals. Honeywell’s annual HUG conference centers on AI and autonomous operations, underscoring heightened service-led differentiation.

White-space opportunities include vertical-specific dashboards for battery gigafactories, hydrogen hubs, and offshore wind assets. Disruptors such as Mitsubishi Electric Iconics GENESIS emphasize low-code SCADA that scales from edge gateways to enterprise historians, shrinking deployment cycles for SMEs. Established players counter by bundling unlimited tags, flexible licensing, and containerized run times to retain share in the evolving HMI market.

Human Machine Interface Industry Leaders

Honeywell International Inc.

Siemens AG

Rockwell Automation Inc.

Schneider Electric SE

ABB Ltd

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- May 2025: Siemens introduced AI agents for its Industrial Copilot ecosystem, enabling autonomous execution and cross-system interoperability.

- April 2025: BB announced plans to spin off its robotics division to accelerate dedicated robotics growth and deepen integration with HMIs.

- March 2025: Rockwell Automation launched FactoryTalk DataMosaix, a cloud Industrial DataOps suite with a low-code visualization builder.

- January 2025: Honeywell unveiled the agenda for the 2025 Honeywell Users Group, focusing on AI integration, cybersecurity, and digital services.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the global human-machine interface (HMI) market as all industrial, automotive, and process automation solutions, hardware panels, embedded PCs, visualization software, and configuration services that let an operator monitor, control, or optimize a machine or production line through a digital display, touch, voice, or gesture input. The valuation covers original equipment sales and licensed software, reported in USD, across discrete and process industries plus aftermarket upgrades.

Scope Exclusion: Consumer smartphones, tablets, smartwatches, and other personal electronics interfaces are not counted.

Segmentation Overview

- By Offering

- Hardware

- HMI Panels

- Industrial PCs

- Software

- Configuration / Programming

- Services

- Hardware

- By Interface Technology

- Touchscreen

- Push-button / Keypad

- Gesture-based

- Voice-controlled

- AR / VR-assisted

- By End-User Industry

- Automotive

- Food and Beverage

- Packaging

- Pharmaceutical

- Oil and Gas

- Metal and Mining

- Energy and Utilities

- Aerospace and Defense

- Semiconductors and Electronics

- Other End Users

- By Configuration

- Embedded HMI

- Stand-alone HMI

- Distributed / Remote HMI

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Russia

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- Saudi Arabia

- United Arab Emirates

- Turkey

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts next interview panel builders, MES integrators, line supervisors, and OT cybersecurity leads across North America, Europe, and Asia-Pacific. Conversations refine average selling prices, screen size preferences, and retrofit rates, and survey feedback weights the relative uptick expected from Industry 4.0 stimulus programs.

Desk Research

We start with structured desk work pulling shipment, production, and trade series from sources such as the United Nations Comtrade database, U.S. Census Machinery Orders, Eurostat PRODCOM, and the International Federation of Robotics. Safety and performance rules from IEC-61131 and OSHA guides anchor compliance breakpoints, while patent trends from Questel highlight emergent modalities like AR-enabled HMIs. Company 10-Ks, investor decks, and news wires in Dow Jones Factiva add pricing color. These examples are illustrative; many additional references inform our evidence stack.

Market-Sizing & Forecasting

We employ a top-down build that reconstructs HMI demand from factory automation capex logs and vehicle production datasets, then corroborate totals with sampled supplier roll-ups (panel shipments × blended ASP). Key variables feeding the model include global robot installations, PLC stock growth, automotive light vehicle output, touchscreen glass pricing, and industrial software license penetration. Forecasts are generated through multivariate regression with scenario checks; missing bottom-up points, such as private label panel volumes, are bridged using regional penetration ratios confirmed in primary calls.

Data Validation & Update Cycle

Outputs pass three-layer variance checks, peer review, and anomaly resolution before sign-off. Reports refresh annually, and we trigger interim updates when material events, large plant closures, component shortages, or currency swings shift the baseline. An analyst revalidates every number before delivery.

Why Mordor's Human Machine Interface Baseline Earns Reliability

Published numbers often diverge because firms pick dissimilar device sets, price stacks, and refresh cadences. We disclose scope choices, refresh yearly, and align ASP curves to verifiable contract data, which competitors rarely reveal.

Key gap drivers include whether consumer touchscreens are bundled, if SCADA licenses are merged with HMI totals, the aggressiveness of future ASP lifts, and currency translation timing.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 5.42 B (2025) | Mordor Intelligence | - |

| USD 6.70 B (2024) | Regional Consultancy A | Includes consumer tablets and SCADA bundles |

| USD 7.41 B (2025) | Global Consultancy B | Uses uniform 7 % ASP uplift, ignores chip shortages |

| USD 5.48 B (2024) | Industry Association C | Relies on headline trade codes, omits software revenue |

Taken together, the comparison shows that Mordor's disciplined device boundary, reality-checked ASP path, and yearly refresh give decision-makers a transparent, balanced baseline they can readily trace and replicate.

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the current size of the HMI market?

The HMI market stands at USD 5.82 billion in 2026 and is projected to reach USD 8.29 billion by 2031.

Which segment is expanding fastest within the HMI market?

AR/VR-assisted interfaces are the fastest-growing segment, posting an 17.62% CAGR between 2026 and 2031.

Why are services gaining momentum in the HMI market?

Services grow at an 10.94% CAGR because plants need integration, cybersecurity hardening, and continuous UX optimization beyond initial hardware deployments.

Which region shows the highest HMI market growth?

The Middle East & Africa region leads with a 9.25% CAGR as governments fund large-scale industrial modernization projects.

How does edge-AI improve HMI performance?

Edge-AI engines predict operator needs, reorganize screen content, and enable voice or gesture input, cutting error rates and boosting task speed according to recent peer-reviewed studies.

What are the main cybersecurity measures adopted in modern HMI systems?

Zero Trust frameworks, multi-factor authentication, secure boot, and encrypted protocols are rapidly becoming standard to meet mandates like the EU’s NIS2 directive.