Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 57.05 Billion |

| Market Size (2031) | USD 67.02 Billion |

| Growth Rate (2026 - 2031) | 3.28% CAGR |

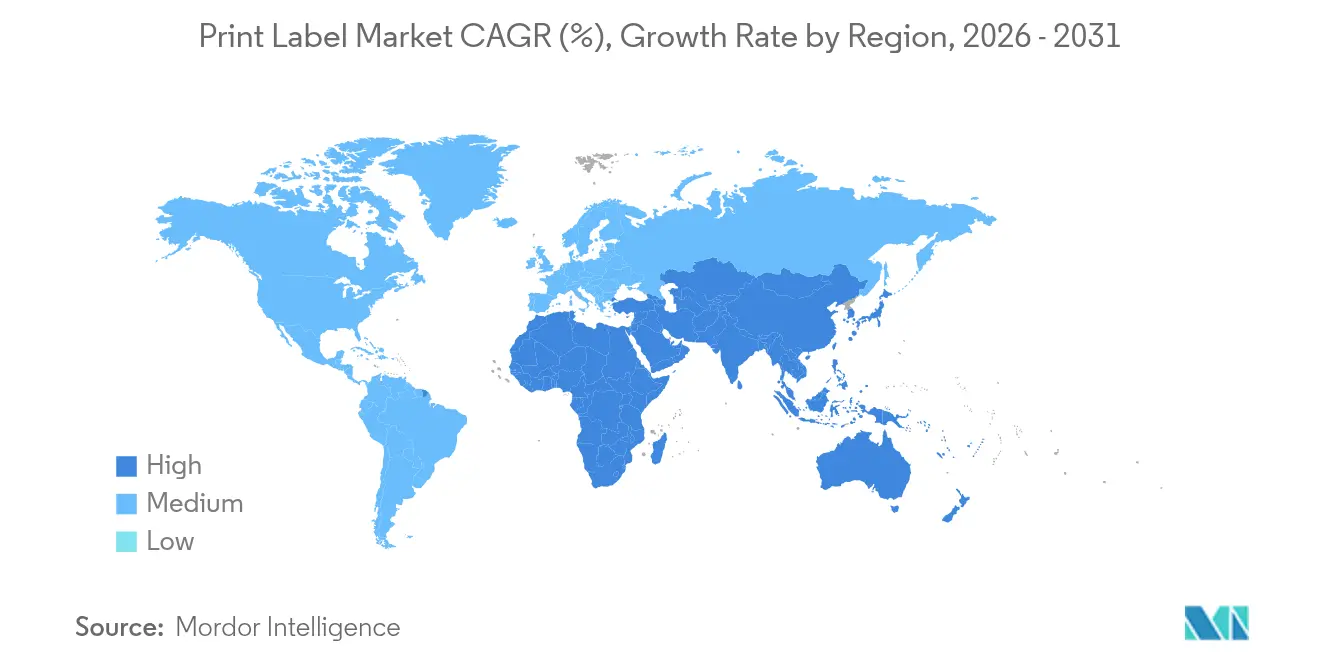

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

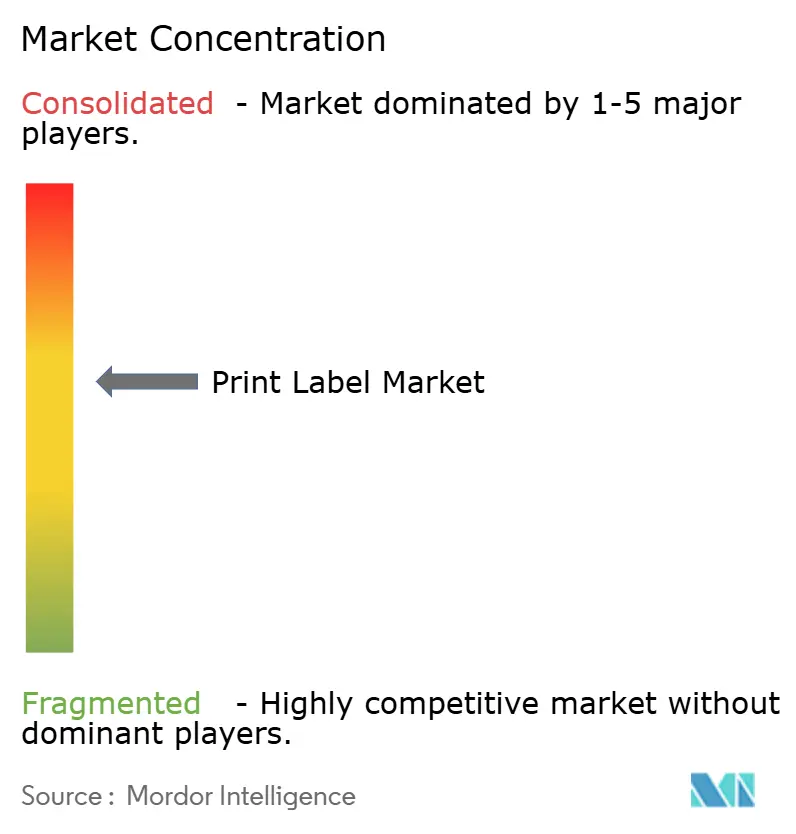

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Print Label Market Analysis by Mordor Intelligence

Print label market size in 2026 is estimated at USD 57.05 billion, growing from 2025 value of USD 55.24 billion with 2031 projections showing USD 67.02 billion, growing at 3.28% CAGR over 2026-2031. Steady expansion reflects the sector’s shift from purely analog processes to digitally enabled, sustainability-focused production frameworks that lower minimum order quantities, compress lead times, and cut material waste. Flexography still controls the largest share of installed capacity, yet inkjet systems are scaling rapidly as converters look to satisfy proliferating SKUs and e-commerce labeling needs. Brand owners’ preference for linerless formats and intelligent identifiers, plus mandated pharmaceutical serialization and food traceability, is reshaping converter investment priorities. Cost pressure from substrate and adhesive volatility continues, but margin resilience hinges on hybrid digital-flexo workflows, supply-chain integration, and circular-economy compliant materials.

Key Report Takeaways

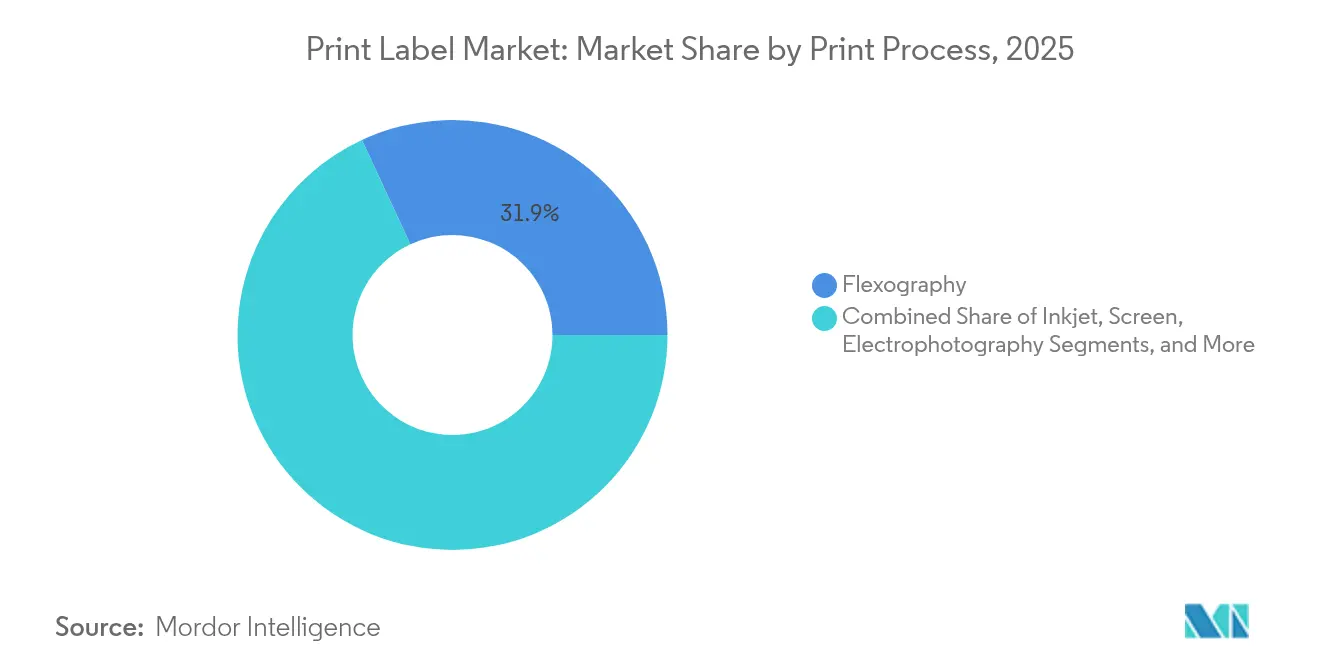

- By print process, flexography captured 31.92% of the print label market share in 2025.

- By label format, the print label market size for linerless labels is projected to grow at a 5.56% CAGR between 2026-2031.

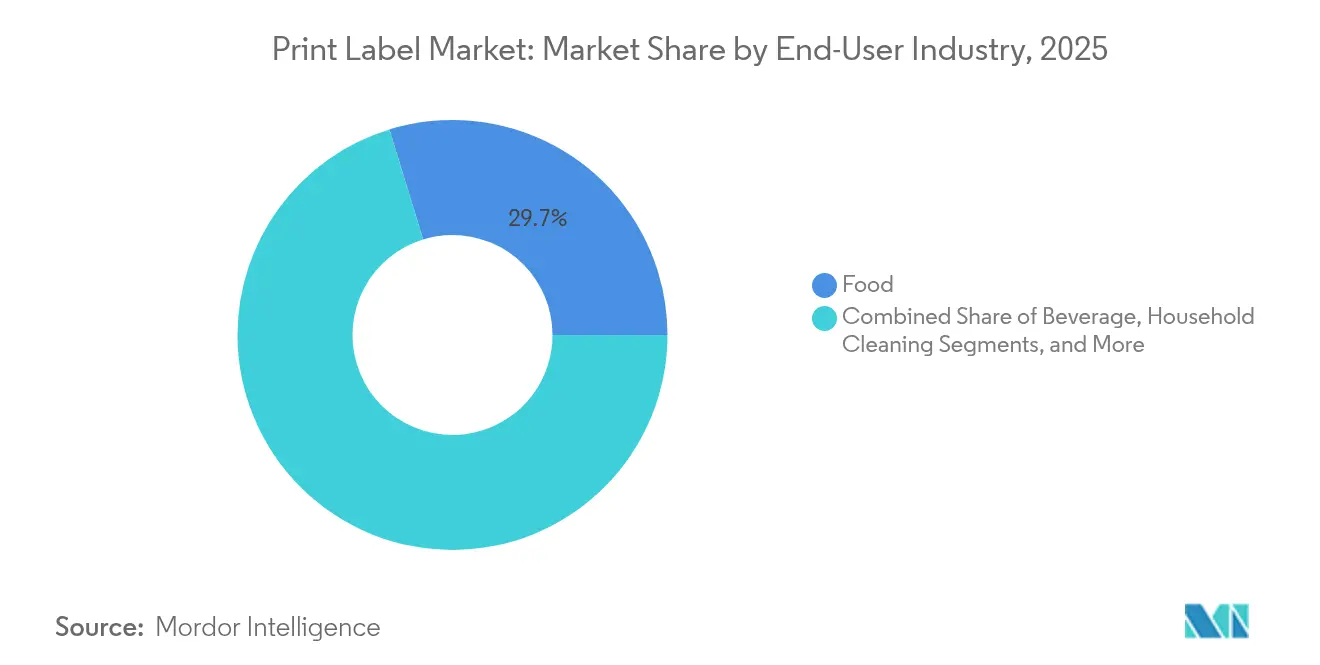

- By end-user industry, food captured 29.74% of the print label market share in 2025.

- By geography, the print label market size for Asia-Pacific is projected to grow at a 4.63% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Print Label Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerated adoption of high-speed digital (inkjet) presses for short-run, SKU-proliferated label jobs | +0.8% | Global, with early adoption in North America and Europe | Medium term (2-4 years) |

| Brand-owner shift toward linerless pressure-sensitive labels to cut waste and logistics costs | +0.6% | Global, strongest in North America and Europe | Medium term (2-4 years) |

| E-commerce boom driving demand for variable-data shipping and return labels | +0.7% | Global, led by North America and Asia-Pacific | Short term (≤ 2 years) |

| Regulatory push for smart/barcode labels enabling end-to-end traceability (EU FMD, U.S. DSCSA) | +0.5% | North America and Europe, expanding to Asia-Pacific | Long term (≥ 4 years) |

| Growth of craft beverage and gourmet foods requiring premium, embellishment-rich labels | +0.3% | North America and Europe, emerging in Asia-Pacific | Medium term (2-4 years) |

| Emerging antimicrobial label coatings for food safety in cold-chain logistics | +0.2% | Global, with regulatory focus in North America and Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Accelerated Adoption of High-Speed Digital Presses for Short-Run Production

Digital inkjet platforms enable profitable runs as low as 500 pieces, contrasting with flexography’s historical 10,000-unit threshold, thereby unlocking new SKU strategies for consumer brands. Capital outlays, such as R.R. Donnelley’s USD 25 million Georgia upgrade, illustrate the scale converters commit to gain throughput and variable-data flexibility. Hybrid lines integrating inkjet and flexo towers streamline changeovers yet create operator-skill gaps that industry groups like the Flexographic Technical Association address through FIRST 5.0 curricula. As high-speed digital productivity converges with analog economics, the print label market will migrate toward mixed-technology production cells that compress lead times and inventory.

Brand-Owner Shift Toward Linerless Labels for Waste Reduction

Eliminating release liners cuts label waste up to 30% and boosts roll density, generating logistics savings that resonate with sustainability scorecards.[1]Avery Dennison, “Company Profile Presentation 2025,” averydennison.com Market leaders report double-digit linerless revenue growth, especially within food retail, where Extended Producer Responsibility fees spur adoption. Transition barriers include specialized applicators and adhesive formulations that must perform across humidity swings, but suppliers are scaling capacity. UPM Raflatac reported 13% quarter-on-quarter growth in Q1 2025, partly on European linerless demand. Converter competitiveness hinges on mastering new coating and slitting techniques that diverge from conventional pressure-sensitive workflows.

E-Commerce Expansion Driving Variable-Data Printing Demand

U.S. Postal Service automation rules effective February 2025 compel shippers to employ machine-readable labels, accelerating variable-data volumes for tracking and returns. Software consolidation Seagull’s merger with Mojix supports more than 100 billion labels annually, signaling infrastructure scale behind omnichannel fulfillment. NIST’s Uniform E-commerce Regulation standardizes label data elements, pushing converters to integrate real-time serialization capabilities. As parcel traffic rises, digital print modules embedded in finishing lines let converters personalize content regionally without extra makeready, strengthening the print label market against direct-to-package alternatives.

Regulatory Traceability Requirements Accelerating Smart-Label Adoption

The U.S. DSCSA and EU FMD mandate item-level serialization, driving demand for 2D codes and RFID-enabled identifiers on every pharmaceutical pack. Smart labels capture EPCIS events to authenticate products and combat counterfeits, creating multi-year technology replacement cycles. Avery Dennison targets 15% organic growth in RFID tags as retailers expand use cases beyond apparel into food and logistics. High-memory inlays and cloud platforms converge, positioning converters that master electronics integration to secure premium margins within the print label market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile paper, film and adhesive prices squeezing converter margins | -0.4% | Global, most severe in North America and Europe | Short term (≤ 2 years) |

| Skill-gap in operating hybrid digital–flexo presses among SME converters | -0.3% | Global, particularly acute in Asia-Pacific SME sector | Medium term (2-4 years) |

| Rising brand-owner preference for direct-to-package digital printing (no label) | -0.2% | North America and Europe, emerging in Asia-Pacific | Long term (≥ 4 years) |

| Difficult recycling of multi-layer shrink and in-mold labels in circular-economy markets | -0.2% | Europe and North America, expanding to Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Raw Material Price Volatility Pressuring Converter Margins

Paper pulp, PET, and acrylic adhesive indices have swung by double digits since 2024, leaving converters exposed because materials account for up to 75% of cost of sales. While global players leverage hedging and scale, Avery Dennison reported a 0.1% sales dip yet preserved EBIT via cost controls, SME converters struggle to pass surcharges to brand owners under annual contracts. Consolidators such as Sonoco channel USD 30 million into adhesive capacity expansions to secure supply and dilute input swings.[2]Sonoco Products Company, “Capital Investment Press Release,” sonoco.com Until substrate markets stabilize, margin compression will temper investment appetite among smaller firms in the print label market.

Technical Skill Gaps in Hybrid Digital-Flexo Operations

OECD analysis confirms SMEs lag in digital upskilling, hampering the adoption of integrated press lines that demand ICC-based color management and variable-data RIP expertise. FIRST 5.0 underscores cross-functional communication between design and press crews, yet many converters lack certified trainers. Brady Corporation’s USD 67.7 million R&D spend highlights talent intensity associated with next-gen labeling solutions. Without structured apprenticeships, waste rates and rework can erode the modest gains digital presses promise, restraining overall print label market efficiency.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Print Process: Digital Inkjet Disrupts Traditional Flexography

Inkjet technology’s 5.3% CAGR underscores its role in reshaping the print label market. Flexography still produces the bulk of long-run SKUs thanks to mature platemaking ecosystems, but inkjet’s substrate versatility and 1-click changeovers let converters secure high-margin micro-runs for promotional campaigns. The print label market size associated with inkjet presses is forecast to grow steadily as equipment costs fall and white ink opacity rivals screen-print quality. Across converters, hybrid architectures that bolt inkjet bars onto flexo lines dominate capex roadmaps, enabling variable data without abandoning proven analog die-cutting workflows.

AstroNova’s TrojanLabel platform, launched at Drupa 2024, typifies the mid-web category aimed at craft beverage and cosmetics converters seeking near-offset registration with minimal setup. Gravure’s niche in ultra-long runs remains secure for large beverage co-packers, yet offset lithography’s footprint narrows as UV-inkjet delivers comparable Pantone coverage. Screen technology survives in electronics durables where film thickness is critical, but its share within the print label market will continue to erode.

By Label Format: Pressure-Sensitive Dominance Challenged by Linerless Innovation

Pressure-sensitive constructions own 43.62% of 2025 volume, benefiting from established dispensing lines and multi-layer constructions that incorporate RFID or NFC inlays. The print label market share for linerless, while low today, is accelerating as brand owners quantify landfill avoidance and logistics savings. Wet-glue labels retain beverage strongholds in Europe due to heritage glass bottling infrastructure, yet retrofitting plants to PSA or shrink-sleeve solutions is gaining traction among new canning facilities.

Intelligent pressure-sensitives under Avery Dennison’s portfolio show 20% growth, demonstrating appetite for dual-frequency RFID tags that marry supply-chain visibility with consumer engagement. Shrink sleeves confront recycling scrutiny because multilayer PET-G structures hinder bottle-to-bottle loops; innovations such as Siegwerk’s washable cPET sleeve inks aim to mitigate these concerns.

By End-User Industry: Food Sector Leadership Faces E-Commerce Challenge

Food manufacturers’ regulatory labeling obligations keep the segment atop revenue rankings, yet e-commerce shipping labels represent the fastest-growing slice of the print label market. Parcel operators now mandate scannable codes resilient to abrasion and condensation, pushing demand for topcoated thermal blanks and durable inks. Beverage labels require scuff resistance and premium finishes sparkling wines, RTDs, and hard seltzers all leverage tactile embellishments, driving higher unit prices. Pharmaceuticals lean on robust security features, including tamper-evident cuts, color-shift inks, and serialized 2D codes compliant with DSCSA, adding complexity and margin potential.

Cosmetics rely on small-format labels that withstand oils and offer high chroma for brand storytelling; the segment benefits from digital micro-runs aligned to influencer collaborations. Industrial and automotive labels call for UL-recognized adhesives and high-heat films, ensuring traceability across extended product lifecycles. Logistics and e-commerce will keep outpacing GDP as consumers habituate to same-day delivery norms, cementing variable-data printing as an engine of print label market expansion.

Geography Analysis

Asia-Pacific dominated the print label market in 2025 with a 35.86% share and is projected to post the highest 4.63% CAGR to 2031. China’s extensive manufacturing base and India’s packaging expansion valued at USD 204.81 billion for 2025 underpin regional momentum. Local converters invest in mid-web digital presses to handle proliferating consumer brands, while government recycling mandates in Japan and South Korea encourage adoption of recyclable facestock and wash-off inks. Southeast Asian nations pivot toward e-commerce fulfillment hubs, stimulating demand for thermal shipping labels and QR-based return tags.

North America remains a technology bellwether, with rapid uptake of cloud-connected RFID labels driven by big-box retail mandates. Margin pressures from resin deflation challenged revenue in 2024, yet converters offset headwinds via automation and high-value applications. The region’s pharma serialization deadline of November 2024 spurred hardware upgrades across U.S. plants, reinforcing smart-label penetration within the print label market.

Europe combines mature demand with stringent circular-economy rules. Extended Producer Responsibility fees in France and Germany favor linerless and mono-material constructions. The UK’s Essential Requirements Regulations guide downgauging and recyclability, stimulating R&D into solvent-free adhesives. Eastern European converters attract contract manufacturing for pan-EU brands seeking cost efficiency without sacrificing regulatory compliance.

Latin America, the Middle East, and Africa account for smaller but rising contributions. Brazil and Mexico scale capacity for beverage shrink sleeves, while Gulf Cooperation Council members diversify into packaged foods, importing technical know-how alongside capital equipment. African markets grapple with trade barriers and infrastructure constraints, yet mobile commerce growth signals long-term potential for variable-data label solutions.

Competitive Landscape

The print label market exhibits moderate consolidation: the top five suppliers control roughly 50% of global revenue, granting them procurement leverage and R&D scale. CCL Industries executed nine acquisitions since January 2023, lifting 2024 sales to USD 7.245 billion and strengthening its automation and RFID capabilities. Avery Dennison’s EUR 60 million (USD 64 million) European expansion adds Industry 4.0 adhesive coaters that raise throughput and lower waste, illustrating how incumbents protect margins through technology investments.

Multi-Color Corporation leverages a global gravure plant network to service premium beverage and personal-care customers, while emerging challengers target digital-first niches. M&A activity is forecast to continue as converters pursue geographic fill-ins and specialty coatings know-how. Patent filings for multi-view beverage label assemblies and antimicrobial coatings signal ongoing innovation pipelines. Competitive advantage increasingly rests on integrating software, automation, and sustainability credentials to satisfy brand and regulatory stakeholders.

Print Label Industry Leaders

CCL Industries Inc.

Avery Dennison Corporation

Multi-Color Corporation

Fuji Seal International, Inc.

Huhtamaki Oyj

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: R.R. Donnelley injected USD 25 million into its Georgia facility, adding HP Indigo 120K and PageWide Advantage 2200 presses alongside autonomous robots to double workforce capacity.

- April 2025: 3M posted USD 6.0 billion GAAP sales and improved operating margin to 20.9%, raising 2025 EPS guidance despite tariff sensitivity.

- February 2025: CCL Industries reported record 2024 results, with sales of USD 7.245 billion and 13% operating income growth, fueled by nine acquisitions.

- January 2025: Dennison recorded USD 2.1 billion Q1 sales, noting strong momentum in Intelligent Labels for apparel and food.

Global Print Label Market Report Scope

The market is defined by the consumption revenues accrued from the sales of print labels offered by various vendors operating in the market.

The print label market is segmented by print process (offset lithography, gravure, flexography, screen, letterpress, electrophotography, and inkjet), label format (wet-glue labels, pressure-sensitive labels, linerless labels, multi-part tracking labels, in-mold labels, and shrink and stretch sleeves), end-user industries (food, beverage, healthcare, cosmetics, household, industrial (automotive, industrial chemicals, and consumer and non-consumer durables), logistics, other end-user industries), and geography (North America (United States and Canada), Europe (United Kingdom, Germany, France, Spain, Italy, Poland, Netherlands, and Rest of Europe), Asia-Pacific (China, India, Japan, Australia, South Korea, and Rest of Asia-Pacific), Latin America (Brazil, Mexico, and Rest of Latin America), and Middle East and Africa). The market sizes and forecasts are provided in terms of value (USD) for the above segments.

By Print Process

| Offset Lithography |

| Gravure |

| Flexography |

| Screen |

| Letterpress |

| Electrophotography |

| Inkjet |

By Label Format

| Wet-Glue Labels |

| Pressure-Sensitive Labels |

| Linerless Labels |

| Multi-Part Tracking Labels |

| In-Mold Labels |

| Shrink and Stretch Sleeves |

By End-User Industry

| Food |

| Beverage |

| Healthcare and Pharmaceuticals |

| Cosmetics and Personal Care |

| Household Cleaning |

| Industrial and Automotive |

| Logistics and E-commerce |

| Electronics and Appliances |

By Geography

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia Pacific | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Print Process | Offset Lithography | ||

| Gravure | |||

| Flexography | |||

| Screen | |||

| Letterpress | |||

| Electrophotography | |||

| Inkjet | |||

| By Label Format | Wet-Glue Labels | ||

| Pressure-Sensitive Labels | |||

| Linerless Labels | |||

| Multi-Part Tracking Labels | |||

| In-Mold Labels | |||

| Shrink and Stretch Sleeves | |||

| By End-User Industry | Food | ||

| Beverage | |||

| Healthcare and Pharmaceuticals | |||

| Cosmetics and Personal Care | |||

| Household Cleaning | |||

| Industrial and Automotive | |||

| Logistics and E-commerce | |||

| Electronics and Appliances | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| Rest of Asia Pacific | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the projected value of the print label market in 2031?

The print label market is expected to reach USD 67.02 billion in 2031 at a 3.28% CAGR.

Which print process is growing fastest within labeling applications?

Inkjet printing leads growth with a 5.3% CAGR through 2031 as converters pursue short-run and variable-data jobs.

Why are linerless labels gaining traction?

They eliminate release liners, cutting up to 30% of label waste and improving roll density for logistics savings.

How are regulations influencing smart-label adoption?

U.S. DSCSA and EU FMD require item-level serialization, driving demand for 2D-code and RFID-enabled labels across pharma and food.

What region commands the largest share of label demand?

Asia-Pacific holds 35.86% of global demand and remains the fastest-expanding geography through 2031.

Which companies dominate the competitive landscape?

CCL Industries, Avery Dennison, and Multi-Color Corporation together account for more than 30% of global label revenue.

Page last updated on: