Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2025) | USD 85.79 Billion |

| Market Size (2031) | USD 117.48 Billion |

| Growth Rate (2026 - 2031) | 6.49% CAGR |

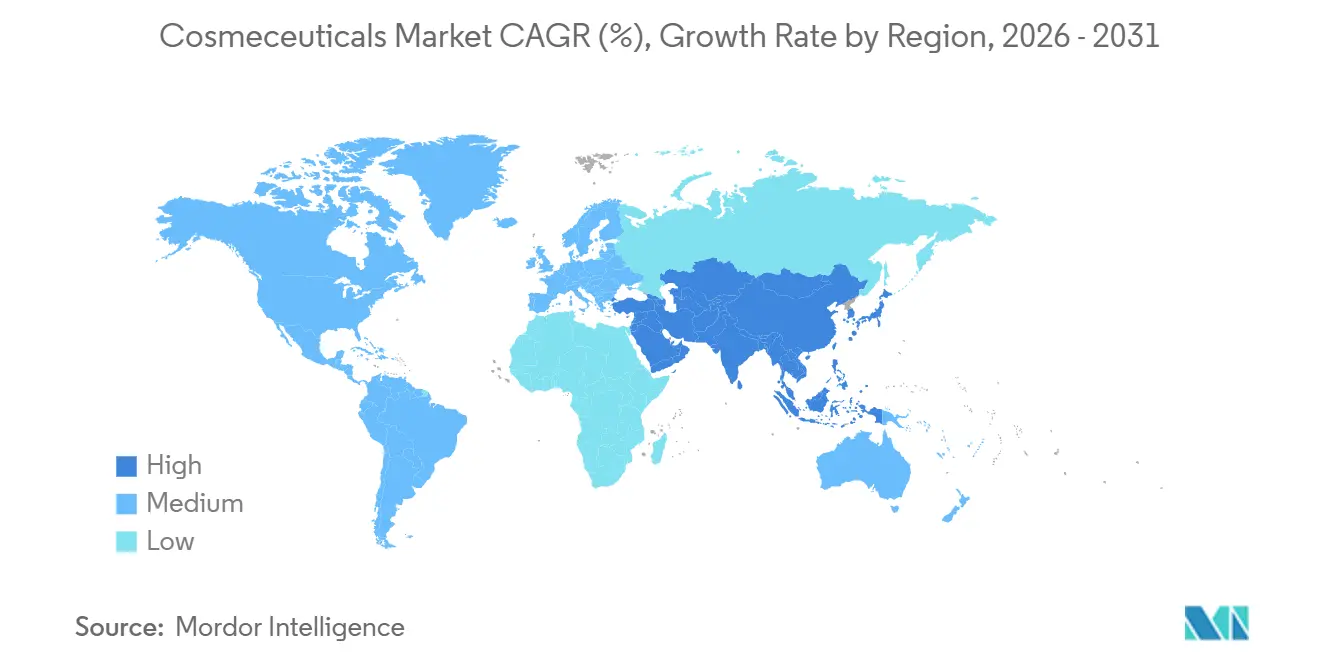

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Cosmeceuticals Market Analysis by Mordor Intelligence

The cosmeceuticals market size is estimated at USD 85.79 billion in 2026 and is projected to reach USD 117.48 billion by 2031, growing at a Compound Annual Growth Rate (CAGR) of 6.49%. This growth is driven by increasing demand for dermatologist-recommended active ingredients, stricter regulatory oversight on efficacy claims, and a rising consumer focus on preventive skin health. Premium pricing is concentrated on formulations containing encapsulated retinoids, collagen-stimulating peptides, and broad-spectrum antioxidants, which deliver visible results within 8 to 12 weeks. Sun protection products combining ultraviolet (UV) filters with free-radical neutralizers are gaining market share, supported by public health campaigns promoting melanoma awareness. Additionally, probiotic and prebiotic blends are expanding the market by appealing to microbiome-conscious consumers. Omnichannel distribution strategies enable brands to capture both in-store consultation traffic and the rapidly growing direct-to-consumer sales. Market consolidation remains moderate, with global conglomerates leveraging patented delivery systems, while prescription-channel specialists maintain pricing by combining pharmaceutical credibility with cosmetic appeal.

Key Report Takeaways

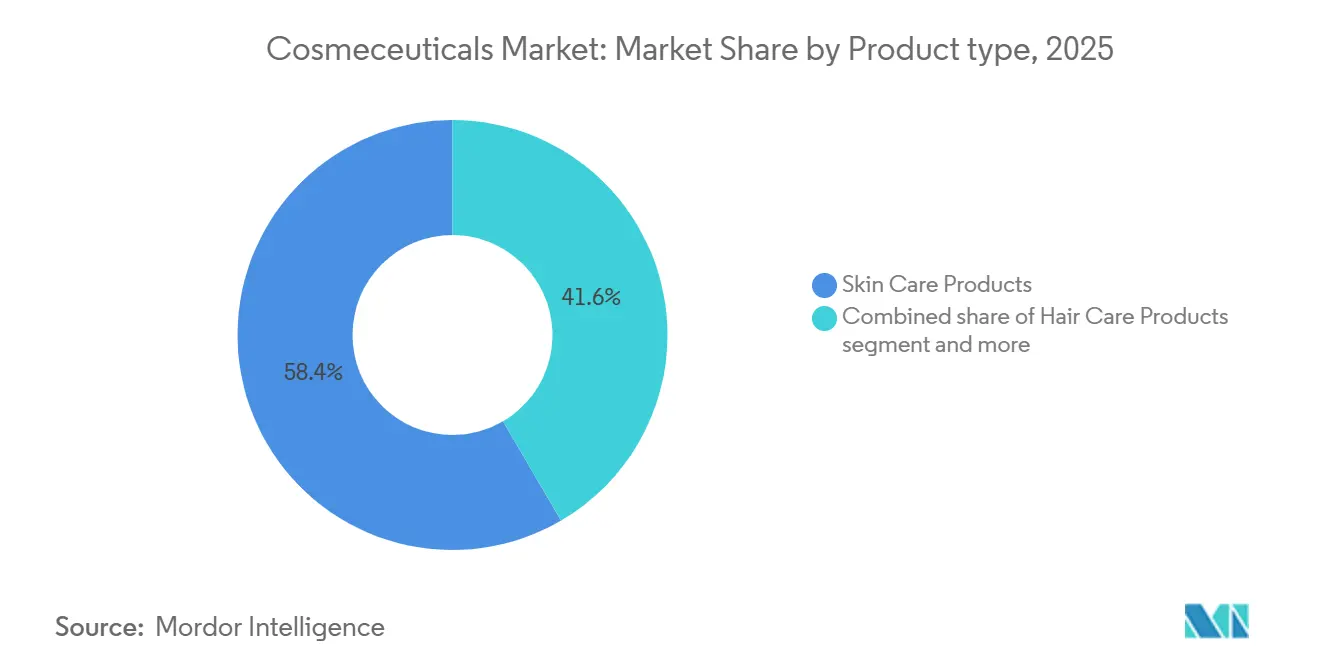

- By product type, skin care captured 58.42% revenue share in 2025; lip care is forecast to expand at a 6.99% CAGR through 2031.

- By category, conventional lines held 71.32% of the cosmeuticals market share in 2025, while natural and organic formulations are advancing at a 7.83% CAGR to 2031.

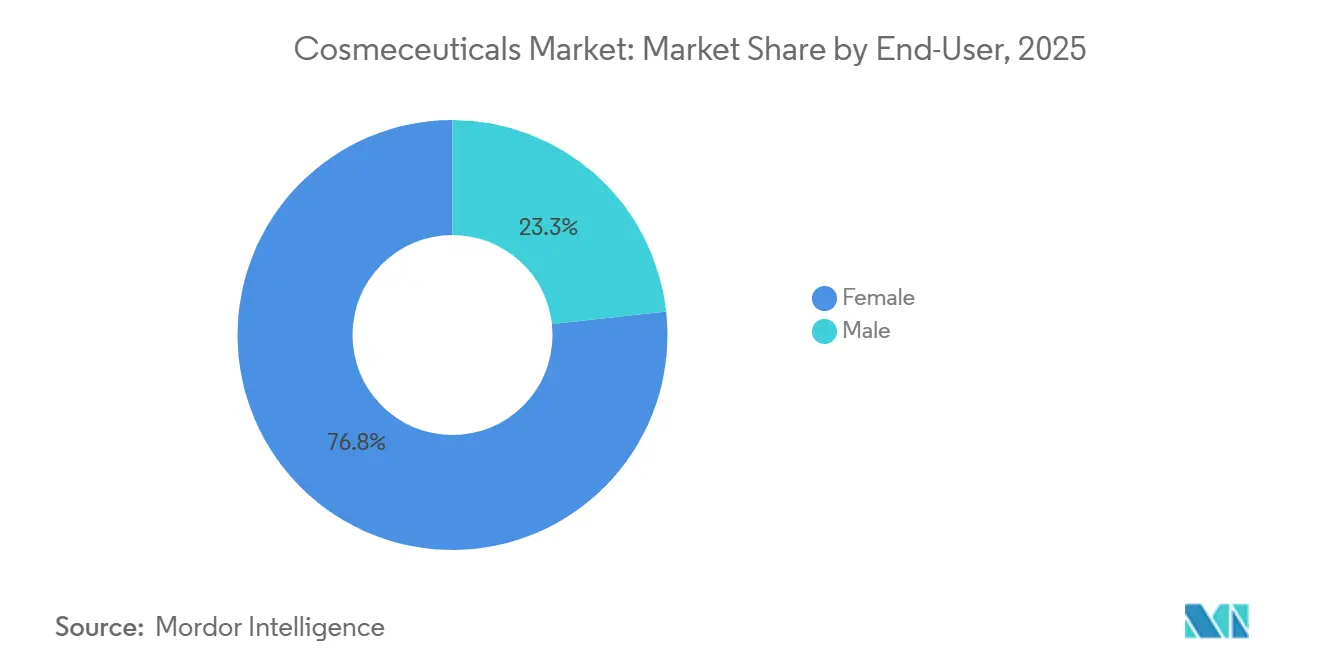

- By end user, female shoppers dominated demand at 72.10% in 2025, whereas male segments are projected to grow at an 8.09% CAGR through 2031.

- By distribution channel, beauty and health stores led with 45.01% of 2025 revenue; online retail is projected to climb at a 7.55% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Cosmeceuticals Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing consumer interest in anti-aging solutions for wrinkles, pigmentation, and firmness using clinically proven actives | +1.8% | Global, with concentrated demand in North America, Europe, and Asia-Pacific | Medium term (2-4 years) |

| Rising awareness of skin cancer, photoaging, and UV damage driving demand for advanced dermocosmetic sun protection | +1.5% | Global, particularly Japan, South Korea, Australia, and Southern Europe | Long term (≥ 4 years) |

| Expansion of dermatologist-recommended and prescription-based skincare boosting credibility of cosmeceutical brands | +1.2% | North America, Europe, and urban Asia-Pacific markets | Medium term (2-4 years) |

| Rapid advancements in active ingredients like peptides, retinoids, antioxidants, and plant stem cells | +1.0% | Global, with R&D hubs in North America and Europe | Short term (≤ 2 years) |

| Growing preference for clean, vegan, and microbiome-friendly formulations with transparent ingredient lists | +0.9% | North America, Europe, and affluent Asia-Pacific segments | Medium term (2-4 years) |

| Increasing adoption of men's grooming and skincare routines featuring anti-aging and anti-acne products | +0.7% | North America, Europe, and emerging Asia-Pacific markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Increasing consumer interest in anti-aging solutions for wrinkles, pigmentation, and firmness using clinically proven actives

The demand for anti-aging cosmeceuticals is evolving as consumers shift from aspirational beauty to results-oriented skincare, expecting visible improvements in fine lines and hyperpigmentation within 8 to 12 weeks. A 2025 Delphi consensus study published in the Journal of the European Academy of Dermatology and Venereology identified retinoids, niacinamide, vitamin C, and azelaic acid as the most dermatologist-recommended ingredients for addressing photoaging. This aligns with consumer preferences for evidence-based formulations over proprietary blends. Clinical validation of these ingredients is driving premiumization, with products containing encapsulated retinol or stabilized L-ascorbic acid priced 30% to 50% higher than conventional moisturizers, while maintaining strong sales in prestige channels. Additionally, the adoption of at-home diagnostic tools, such as AI-powered skin analyzers that measure wrinkle depth and pigment distribution, is accelerating this trend by enabling consumers to objectively track product efficacy. Brands that fail to substantiate anti-aging claims with clinical trial data face potential regulatory scrutiny under the EU's Cosmetics Regulation 1223/2009, which requires efficacy claims to be supported by adequate evidence. This factor is projected to contribute 1.8 percentage points to the overall CAGR, with peak impact expected in the medium term as personalized formulation platforms continue to develop.

Rising awareness of skin cancer, photoaging, and UV damage driving demand for advanced dermocosmetic sun protection

Growing awareness is increasing the demand for hybrid formulations that combine UV filters with antioxidants, such as niacinamide and ferulic acid. These antioxidants help neutralize free radicals generated by UV exposure and provide additional protection beyond Sun Protection Factor (SPF) ratings. In Japan, the quasi-drug classification for sunscreens requires rigorous efficacy testing, creating a regulatory advantage for established companies like Shiseido and Kao. These companies invest in photostable filter technologies, including Tinosorb M and Uvinul A Plus. In Australia, where melanoma rates are among the highest globally, the Therapeutic Goods Administration enforces strict water-resistance standards for sunscreens. This has driven innovation in long-wear formulations that maintain SPF efficacy even after 80 minutes of water immersion [1]Source: Commonwealth of Australia, “Sunscreens,” tga.gov.au. Furthermore, the Centers for Disease Control and Prevention (CDC) 2024 guidelines recommend daily SPF 30+ application for all skin types, including darker phototypes that were previously underserved by cosmetic sunscreens, thereby expanding the addressable market.

Expansion of dermatologist-recommended and prescription-based skincare boosting credibility of cosmeceutical brands

The prescription-to-consumer pathway is becoming an important factor in building credibility, particularly for brands such as La Roche-Posay and CeraVe, which are frequently recommended by dermatologists for post-procedure care and chronic conditions like rosacea and atopic dermatitis. A 2025 survey of 1,200 dermatologists in North America and Europe revealed that 78% recommend specific cosmeceutical brands to their patients, with retinoid serums and ceramide-based moisturizers being the most commonly suggested products. This pattern of endorsement is fostering a perception among consumers that dermatologist-recommended products are quasi-pharmaceutical, which supports premium pricing and drives repeat purchase rates exceeding 60%. Galderma's Cetaphil and Differin product lines capitalize on this trend by maintaining a strong presence in dermatology clinics while simultaneously expanding into mass retail. This dual-channel approach builds consumer trust while ensuring accessibility. Additionally, prescription-based skincare is benefiting from the increasing adoption of telemedicine. Platforms such as Curology and Apostrophe provide personalized tretinoin and niacinamide formulations through virtual consultations, bypassing traditional retail channels and appealing to younger consumers who prefer to avoid in-person dermatology visits.

Rapid advancements in active ingredients like peptides, retinoids, antioxidants, and plant stem cells

Advancements in active delivery systems are addressing challenges related to ingredient stability and skin penetration. Encapsulation technologies now enable time-release formulations that preserve efficacy while reducing irritation. Peptides, such as matrixyl and argireline, are increasingly recognized for their collagen-stimulating properties, with clinical studies indicating a 15% to 20% improvement in skin firmness after 12 weeks of use. Plant stem cell extracts, including those from edelweiss and sea fennel, are being promoted as sustainable alternatives to synthetic active ingredients, appealing to clean-beauty consumers. However, peer-reviewed evidence supporting their anti-aging efficacy remains limited compared to retinoids. Innovations in retinoids are focusing on next-generation derivatives like hydroxypinacolone retinoate (HPR), which provides retinol-like benefits with reduced irritation, an important feature for the 30% to 40% of cosmeceutical consumers with sensitive skin. Antioxidant formulations are also expanding beyond vitamin C to include resveratrol, coenzyme Q10 (ubiquinone), and bakuchiol, a plant-derived retinol alternative that caters to consumers seeking gentler options.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory ambiguity impacts claims and product classification | -0.6% | Global, particularly impacting multinational brands navigating FDA, European Union, and Asia-Pacific frameworks | Medium term (2-4 years) |

| High research and development costs affect profitability | -0.5% | Global, with disproportionate impact on mid-tier brands lacking scale | Short term (≤ 2 years) |

| Short product life cycles drive constant innovation | -0.4% | Global, particularly in fast-moving prestige and mass segments | Short term (≤ 2 years) |

| Adverse reactions limit adoption among sensitive users | -0.3% | Global, with higher incidence in populations with compromised skin barriers | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Regulatory ambiguity impacts claims and product classification

The absence of a unified cosmeceutical category across major markets creates compliance challenges, particularly for smaller brands without dedicated regulatory teams. In the United States, the Food and Drug Administration (FDA) regulates cosmeceuticals under the Federal Food, Drug, and Cosmetic Act. This act defines cosmetics as products intended to cleanse or beautify, while drugs are defined as products intended to treat or prevent disease. Many cosmeceuticals fall between these definitions, often using claims such as "reduce the appearance of wrinkles" instead of "treat wrinkles" to avoid being classified as drugs. In the European Union, Cosmetics Regulation 1223/2009 enforces stricter requirements, such as limiting retinol concentrations to 0.3% in leave-on products and mandating safety assessments for nano-ingredients. These regulations compel brands to reformulate products for regional compliance, increasing inventory complexity[2]Source: United States Food & Drug Administration, “FDA Authority Over Cosmetics: How Cosmetics Are Not FDA-Approved, but Are FDA-Regulated,” fda.gov. Meanwhile, China's 2024 cosmetics supervision regulations require efficacy substantiation for anti-aging and whitening claims. Brands must submit clinical trial data to the National Medical Products Administration, a process that can delay product launches by 6 to 12 months.

High research and development costs affect profitability

Developing a new cosmeceutical formulation with proprietary active ingredients can cost between USD 2 million and USD 5 million. This includes expenses for stability testing, clinical trials, and regulatory submissions, creating a significant barrier to innovation for mid-sized brands that depend on contract manufacturers. For brands aiming to validate anti-aging claims with peer-reviewed clinical data, conducting split-face studies with 50 to 100 participants over a period of 12 to 16 weeks is essential. These studies typically cost between USD 150,000 and USD 300,000 each. However, such investments do not guarantee commercial success if consumer acceptance is low. Furthermore, the growing focus on sustainable sourcing and clean formulations is increasing research and development costs. Plant-derived active ingredients often require more complex extraction and stabilization processes compared to synthetic alternatives. Large companies such as L'Oréal and Estée Lauder can distribute these costs across their global portfolios, but smaller brands face margin pressures, especially when competing in mass retail channels where price sensitivity restricts premium positioning.

Segment Analysis

By Product Type: Skin Care Dominance Masks Lip Care Surge

Skin care products accounted for 58.42% of the global cosmeceuticals market in 2025, driven by multi-step routines that include serums, moisturizers, and sunscreens to address concerns such as photoaging, hyperpigmentation, and barrier dysfunction. Anti-aging formulations containing retinoids and peptides held the largest share within the skin care segment, appealing primarily to consumers aged 35 to 55 who focus on reducing wrinkles and improving skin firmness. Additionally, anti-acne products targeting adult acne in both men and women are gaining traction, supported by increased dermatological prescriptions of adapalene and salicylic acid for persistent breakouts.

Sun protection products are experiencing growth due to rising awareness of melanoma risks, with hybrid formulations that combine broad-spectrum ultraviolet (UV) filters and antioxidants like niacinamide offering enhanced photoprotection beyond sun protection factor (SPF) ratings. This positioning is particularly effective in high-UV regions such as Australia and Southern Europe. Lip care products, while smaller in market size, are projected to grow at an annual rate of 6.99% through 2031, the fastest among product types. This growth is driven by the introduction of peptide-infused balms and hyaluronic acid treatments targeting perioral wrinkles and volume loss, conditions previously addressed primarily through injectable fillers.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Category: Natural and Organic Formulations Accelerate Despite Conventional Dominance

Conventional formulations accounted for 71.32% of the market in 2025, driven by consumer confidence in synthetic active ingredients such as retinoids, niacinamide, and alpha hydroxy acids. These ingredients have a long history of clinical validation and consistent efficacy. Conventional formulations benefit from established supply chains, lower raw material costs, and regulatory precedents. These factors enable brands to scale production efficiently and offer competitive pricing in mass retail channels.

In comparison, natural and organic cosmeceuticals are projected to grow at an annual rate of 7.83% through 2031, exceeding the growth rate of conventional products by 1.34 percentage points. This growth is being driven by increasing consumer demand for microbiome-friendly formulations, vegan certifications, and transparent ingredient sourcing. Younger demographics, particularly Generation Z (Gen Z) and millennials, are leading this trend. They view clean beauty as an extension of sustainability values and are willing to pay 20% to 30% premiums for products certified by organizations such as Ecocert and The Vegan Society.

By End User: Male Grooming Routines Normalize Clinical Actives

Female consumers are projected to account for 72.10% of the cosmeceuticals market in 2025. This reflects years of category development and marketing efforts that have positioned anti-aging and sun protection as essential components of women's skincare routines. This segment benefits from well-established purchasing patterns, with women aged 30 to 55 forming the primary demographic for products such as retinoid serums, peptide moisturizers, and broad-spectrum sunscreens. These consumers exhibit strong brand loyalty when products deliver visible and effective results.

In comparison, male consumers are expected to grow at an annual rate of 8.09% through 2031, representing the fastest growth among end-user segments. This trend is being driven by evolving cultural norms around grooming and an increasing adoption of multi-step skincare routines that include clinically validated ingredients. Younger male consumers, particularly those aged 25 to 40, are leading this growth as they view skincare as a form of preventive health rather than vanity. This perspective is further supported by dermatologists and social media influencers who emphasize sun protection and anti-aging as universal priorities, regardless of gender.

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Distribution Channel: E-Commerce Disrupts Traditional Beauty Retail

Beauty and health stores accounted for 45.01% of cosmeceuticals distribution in 2025, highlighting the continued preference for in-store consultations, product sampling, and immediate product availability. These are advantages that online channels often cannot fully replicate. These specialty retailers, such as Sephora, Ulta, and independent pharmacies, provide curated product selections and employ trained staff who offer recommendations tailored to individual skin types and concerns. This personalized service is particularly valued by consumers managing complex, active ingredient-based skincare routines.

Online retail stores are expected to grow at an annual rate of 7.55% through 2031, driven by direct-to-consumer (DTC) brands such as The Ordinary and Curology, which bypass traditional retail markups and offer personalized formulations at prices 30% to 50% lower than those of prestige brands. The adoption of artificial intelligence (AI)-powered skin diagnostic tools is further accelerating this trend by enabling consumers to assess their skin conditions at home and receive tailored product recommendations, reducing the reliance on in-store consultations. According to the International Trade Association, global B2C e-commerce revenue is projected to grow at a steady compound annual growth rate of approximately 14%[3]Source: International Trade Association, "2024 eCommerce Size & Sales Forecast," trade.gov.

Geography Analysis

In 2025, the Asia-Pacific region led the global cosmeceuticals market, accounting for 35.13% of the total share. This leadership was supported by strict sun protection regulations in countries like Japan and South Korea, where UV filters are classified as quasi-drugs requiring efficacy validation. Additionally, China's 2024 cosmetics supervision regulations require clinical substantiation for anti-aging and whitening claims. Japan's aging population, with 29% of residents over the age of 65, is driving demand for formulations containing firmness-enhancing peptides and retinoids. Meanwhile, South Korea's K-beauty export ecosystem is globalizing innovations such as centella asiatica extracts and fermented ingredients, which combine traditional botanicals with clinical validation. In India, the cosmeceuticals market is expanding as dermatologists increasingly recommend active-based regimens for conditions like hyperpigmentation and melasma, which are common in darker skin phototypes. Brands such as Cipla's Excela and Abbott's Deriva are positioning themselves as cost-effective alternatives to Western premium lines.

The Middle East and Africa, while representing a smaller market share in 2025, are projected to grow at an annual rate of 8.21% through 2031, making it the fastest-growing region. This growth is driven by the increasing demand for halal-certified dermocosmetics, which combine religious compliance with clinical efficacy. Saudi Arabia and the United Arab Emirates are leading this growth, with consumers prioritizing products free from alcohol and animal-derived ingredients. Halal certification is a critical factor in these markets, where it is considered essential for personal care products.

North America maintained a significant market share in 2025, supported by high consumer awareness of dermatologist-recommended skincare products and well-established distribution channels. These include specialty retailers such as Sephora and Ulta, as well as direct-to-consumer platforms offering personalized formulations like tretinoin and niacinamide. The United States Food and Drug Administration's (FDA) regulatory framework, which classifies cosmeceuticals under the Federal Food, Drug, and Cosmetic Act without a distinct category, adds compliance complexity. However, it also allows brands to make structure-function claims that are restricted in other markets.

Get Analysis on Important Geographic Markets

Download PDF

Competitive Landscape

The global cosmeceuticals market shows moderate concentration, with multinational corporations such as L'Oréal, Estée Lauder, and Unilever leading the market through their dermatological brand portfolios, including La Roche-Posay, Clinique, and Dermalogica. At the same time, specialized companies like Galderma and Pierre Fabre leverage their credibility in prescription channels to achieve higher margins in specific segments. Large players are adopting dual strategies by acquiring digitally native brands to tap into direct-to-consumer growth while maintaining a presence in prestige retail to protect brand equity. For example, Estée Lauder's 2021 acquisition of Deciem (The Ordinary) and its subsequent expansion into Sephora illustrate this approach.

Smaller brands are exploring opportunities in areas such as microbiome-friendly formulations and personalized active concentrations. They are utilizing artificial intelligence (AI)-powered skin diagnostics to offer customization that larger, mass-market players find difficult to replicate at scale. Additionally, the rise of telemedicine platforms such as Curology and Hims is disrupting traditional retail channels. These platforms enable brands to capture higher margins by bypassing distributor markups and offering subscription models that enhance customer lifetime value.

Technology adoption is becoming a critical competitive advantage in the market. Brands are investing in encapsulation technologies that allow time-release delivery of retinoids and peptides, reducing irritation while maintaining effectiveness. For instance, L'Oréal holds a patent portfolio with over 500 active filings related to cosmeceutical delivery systems, reflecting its strategic focus on proprietary technologies to establish defensible positions in an otherwise commoditized active-ingredient market. Regulatory compliance expertise is also emerging as a significant barrier to entry. This is particularly evident in regions such as the European Union, where the Cosmetics Regulation 1223/2009 imposes restrictions on retinol concentrations and requires safety assessments for nano-ingredients. These regulatory complexities favor established players with dedicated regulatory teams, further strengthening their market position.

Cosmeceuticals Industry Leaders

-

L’Oréal S.A.

-

Procter & Gamble Co.

-

Unilever PLC

-

Shiseido Co., Ltd.

-

The Estée Lauder Companies Inc.

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- March 2025: Prada Beauty launched its cosmetics line in Canada with a technology-driven product range that combines functionality with innovative design. The collection includes skincare, complexion, eye, and lip products, aiming to offer consumers a new perspective on beauty through a curated selection of essential items.

- February 2025: COSMOS-certified organic skincare brand Puddles has launched a new skincare and haircare range for teenagers. The international product line uses plant-based ingredients with scientific validation to treat common teenage skin concerns, including acne, breakouts, and dandruff, while maintaining gentle and safe formulations.

- January 2025: Kao Corporation introduced its global skincare brand Curél in German pharmacies. This launch aligns with Kao's expansion strategy in the skincare market, emphasizing derma-cosmetics and skin protection products.

- September 2024: Beiersdorf introduced its first epigenetic serum under the Eucerin brand, incorporating the company's patented skin-specific age clock technology. The technology utilizes an algorithm based on epigenetic patterns to measure the skin's biological age.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the global cosmeceuticals market as commercial topical, ingestible, or minimally invasive products that blend cosmetic appeal with bioactive, dermatology-grade ingredients across skin, hair, lip, and oral care lines.

Scope exclusion: professional aesthetic procedures (laser, surgical, or injectable therapeutics administered solely in clinics) and prescription-only pharmaceuticals are outside this report.

Segmentation Overview

-

By Product Type

-

Skin Care Products

- Anti-ageing

- Anti-acne

- Sun Protection

- Other Skin-care Products

-

Hair Care Products

- Shampoos and Conditioners

- Hair Colourants and Dyes

- Other Hair-care Products

- Lip Care Products

- Oral Care Products

-

Skin Care Products

-

By Category

- Conventional

- Natural/Organic

-

By End-User

- Male

- Female

-

By Distribution Channel

- Supermarkets/Hypermarkets

- Beauty and Health Stores

- Online Retail Stores

- Other Distribution Channels

-

By Geography

-

North America

- United States

- Canada

- Mexico

- Rest of North America

-

Europe

- Germany

- United Kingdom

- Italy

- France

- Spain

- Netherlands

- Poland

- Belgium

- Sweden

- Rest of Europe

-

Asia-Pacific

- China

- India

- Japan

- Australia

- Indonesia

- South Korea

- Thailand

- Singapore

- Rest of Asia-Pacific

-

South America

- Brazil

- Argentina

- Colombia

- Chile

- Peru

- Rest of South America

-

Middle East and Africa

- South Africa

- Saudi Arabia

- United Arab Emirates

- Nigeria

- Egypt

- Morocco

- Turkey

- Rest of Middle East and Africa

-

North America

Detailed Research Methodology and Data Validation

Primary Research

Analysts then spoke with contract manufacturers, retail pharmacists, dermatologists, and online beauty merchants in North America, Europe, Asia Pacific, and the Middle East. These interviews clarified average selling prices, ingredient cost pass-through, and the pace at which male grooming and clean label trends are reshaping demand.

Desk Research

We first gathered freely available evidence from tier-1 regulators and statistics bureaus, such as FDA MoCRA filings, EU CosIng ingredient lists, UN Comtrade trade codes, and age-band population tables from the World Bank. Industry context came from dermatology journals and patents accessed via Questel, while company 10-Ks, investor decks, and Factiva news helped benchmark pricing corridors and launch pipelines. Association portals like Cosmetics Europe and the Personal Care Products Council provided compliance and labeling insights. This list is illustrative; many other public and licensed sources informed data collection and validation.

Market-Sizing & Forecasting

We begin with a top-down recreation of retail receipts using country beauty expenditure, derma-cosmetic share, and cosmeceutical penetration. Supplier roll-ups and sampled ASP × volume checks provide bottom-up cross-tests before totals are locked. Key variables tracked include active ingredient launches, dermatologist prescription rates, online premium beauty share, median age shifts, and per capita disposable income movements. Multivariate regression blended with ARIMA frames the outlook, and gaps, such as sparse African channel data, are bridged through calibrated import values reviewed with regional experts. For context, Mordor Intelligence provides insights into the market.

Data Validation & Update Cycle

Outputs pass variance screens against historical series, shipment trackers, and currency movements. A second analyst reviews anomalies, and the dataset is refreshed yearly, with interim updates triggered by material regulatory or M&A events.

Why Our Cosmeceuticals Baseline Commands Reliability

Published estimates often diverge because firms pick dissimilar product mixes, inflate online growth, or freeze exchange rates. Our study includes only retail sold cosmeceuticals, converts revenues with rolling average FX, and refreshes inputs every twelve months, ensuring balanced figures.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 80.56 B | Mordor Intelligence | - |

| USD 70.00 B | Global Consultancy A | Narrower SKU basket and lower ASP ladder |

| USD 74.31 B | Research Publisher B | Includes physician-dispensed sales for three regions only |

| USD 64.68 B | Industry Journal C | Uses constant 2021 FX and static online share |

In sum, while external numbers swing between conservative and aggressive, the disciplined variable selection, dual cross-checks, and annual refresh practiced by Mordor Intelligence give decision makers a transparent, dependable baseline.

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the current global value of the cosmeceuticals market?

The cosmeceuticals market size is USD 85.79 billion in 2026 with a forecast to reach USD 117.48 billion by 2031.

Which product category leads revenue?

Skin care products hold the largest share at 58.42% of 2025 global sales.

Which region commands the highest demand?

Asia-Pacific leads with 35.13% of 2025 revenue, driven by stringent efficacy regulations and aging demographics.

What is the fastest-growing distribution channel?

Online retail is projected to expand at a 7.55% CAGR through 2031 as direct-to-consumer brands scale globally.

Which segment shows the highest growth by end user?

Male consumers are forecast to grow at an 8.09% CAGR as preventive grooming routines normalize clinical actives.