Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

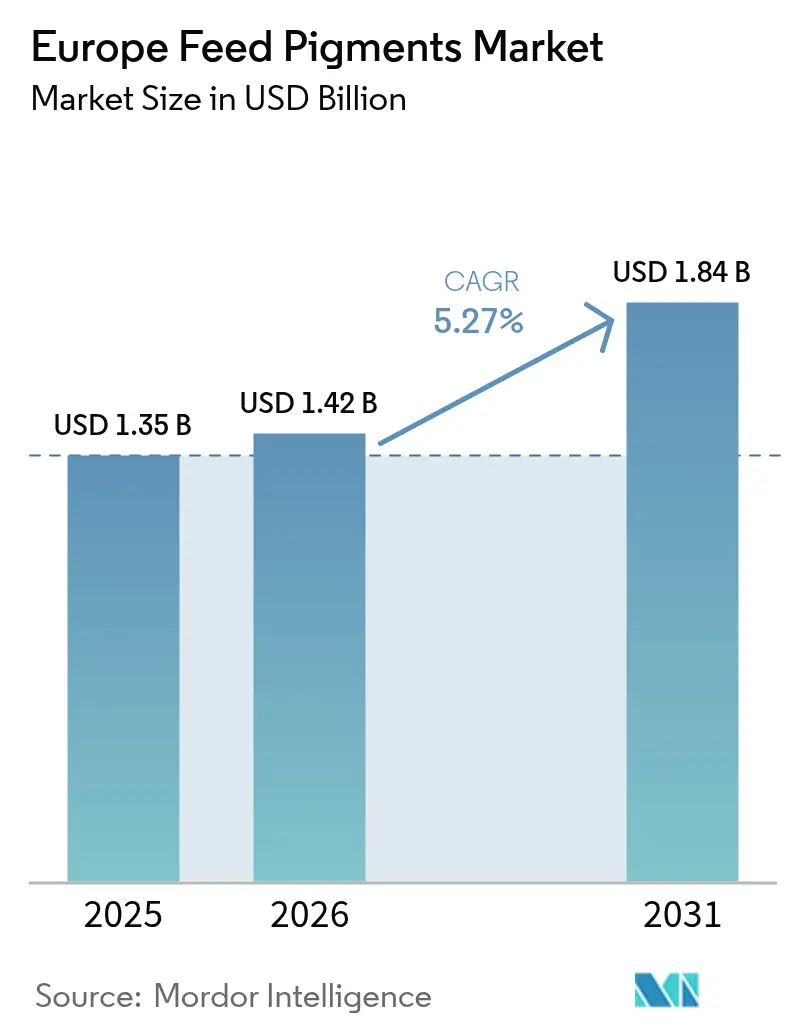

| Base Year Market Size (2025) | USD 1.35 Billion |

| Market Size (2026) | USD 1.42 Billion |

| Market Size (2031) | USD 1.84 Billion |

| Growth Rate (2026 - 2031) | 5.27% CAGR |

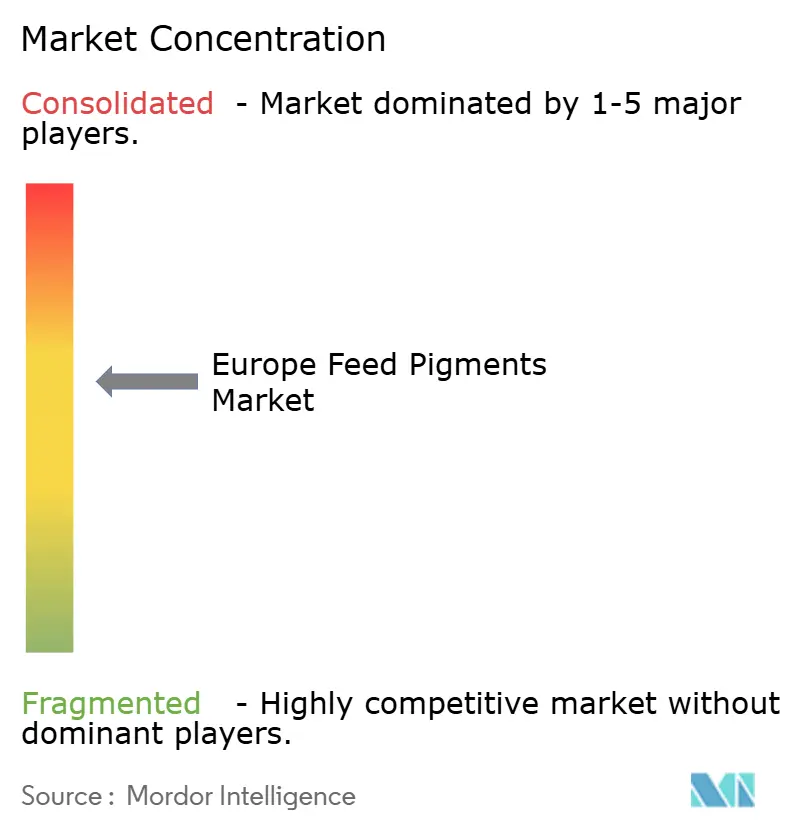

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Feed Pigments Market Analysis by Mordor Intelligence

The Europe feed pigments market size was valued at USD 1.35 billion in 2025 and estimated to grow from USD 1.42 billion in 2026 to reach USD 1.84 billion by 2031, at a CAGR of 5.27% during the forecast period (2026-2031). Growth is propelled by retailer demand for vivid yolk and flesh coloration, a regulatory tilt toward natural carotenoids, and expanding aquaculture production. Carotenoids dominate due to their dual role in pigmentation and immune support, while spirulina outpaces all other ingredients as algae cultivation scales up. Poultry integrators continue to represent the bulk of demand, and salmonid producers are modernizing their feed recipes to comply with the European Food Safety Authority's inclusion caps. Germany anchors regional revenue because its large layer flock supports widespread carotenoid use, whereas Russia shows the quickest growth as import-substitution policies stimulate domestic pigment blending.

Key Report Takeaways

- By type, carotenoids captured 61.45% of the Europe feed pigments market share in 2025, while spirulina is projected to grow at a 9.25% CAGR through 2031.

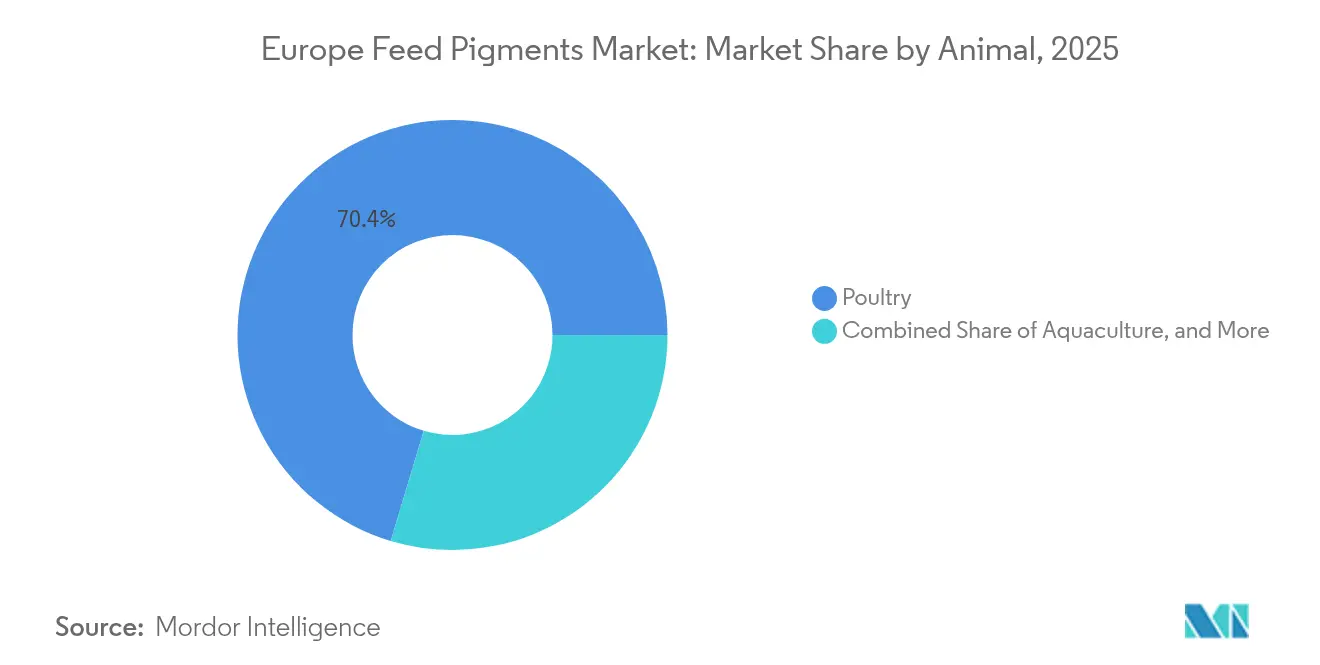

- By animal, poultry applications held 70.36% of the Europe feed pigments market share in 2025, and aquaculture is projected to grow at an 8.05% CAGR through 2031.

- By geography, Germany accounted for 18.32% of the Europe feed pigments market share in 2025, whereas Russia is the fastest-growing region, with a 7.22% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Feed Pigments Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for carotenoid-enriched poultry products | +1.2% | Germany, France, Spain, and United Kingdom | Medium term (2-4 years) |

| Shift toward natural pigment sources | +1.0% | Germany, Spain, France, Italy, and United Kingdom | Long term (≥ 4 years) |

| Technological advances in microencapsulation for stability | +0.6% | Germany, France, and United Kingdom | Medium term (2-4 years) |

| Regulatory easing on algal pigment approvals | +0.5% | Germany, France, Spain, Italy, United Kingdom, and Russia | Short term (≤ 2 years) |

| Consumer preference for clean-label meat and eggs | +0.9% | Germany, France, United Kingdom, and Spain | Medium term (2-4 years) |

| Growth of antibiotic-free feed driving functional pigments | +0.4% | Germany, France, Spain, Italy, and United Kingdom | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Carotenoid-Enriched Poultry Products

Retailers across Germany, France, and Spain are mandating deeper yolk colors to signal freshness and nutritional density, with supermarket chains specifying Roche scores of 14 or higher for premium egg lines. This visual benchmark translates directly into lutein and zeaxanthin inclusion rates of 20 to 30 milligrams per kilogram of layer feed, which is projected to increase carotenoid demand by an 8% year-over-year in 2024. DSM-Firmenich's trial data, published in 2024, showed that apocarotenoid-ester formulations achieved 46.2% deposition efficiency in egg yolks, compared with 31.9% for canthaxanthin [1]Source: DSM-Firmenich, “Apocarotenoid Ester Deposition Trials,” DSM-Firmenich.com. This enabled formulators to reduce inclusion rates while maintaining target color scores and lowering feed costs by 3%. Consumer surveys in Germany indicate that 68% of shoppers associate darker yolks with higher omega-3 content, even though yolk color is unrelated to fatty-acid profile, creating a perception gap that drives premiumization strategies across the egg value chain.

Shift Toward Natural Pigment Sources

The European Union's de facto ban on synthetic azo dyes, including Red 2G, has accelerated adoption of plant- and algae-derived pigments, with spirulina and paprika oleoresin capturing share from chemically synthesized alternatives. Spirulina's phycocyanin and carotenoid content make it a dual-function ingredient for aquaculture, providing both blue-green hues for ornamental fish and red-orange tones for salmonids when combined with astaxanthin. The European Food Safety Authority (EFSA) fast-tracked approvals for several algal extracts in 2024, reducing the regulatory timeline from 18 months to under 12 months for dossiers with robust safety data. This has emboldened ingredient suppliers to invest in European cultivation capacity. Spain's paprika-growing regions experienced a 12% decline in yield in 2024 due to drought and elevated summer temperatures, which tightened the oleoresin supply and pushed spot prices up 18% year-over-year. This, in turn, prompted poultry integrators in France and Italy to lock in forward contracts or reformulate with synthetic canthaxanthin blends.

Technological Advances in Microencapsulation for Stability

Microencapsulation technology has emerged as a critical enabler for pigment bioavailability, with patented beadlet formulations protecting carotenoids from oxidative degradation during feed pelleting and storage. DSM-Firmenich's Carophyll beadlets utilize a lipid-matrix coating that maintains 95% pigment potency after six months of ambient storage, compared with 70% retention for uncoated powders, thereby reducing the need for over-formulation and lowering raw material waste. Kemin's ORO GLO product line incorporates a proprietary encapsulation process that increases lutein deposition in egg yolks by approximately 25% compared to standard marigold extracts, enabling layer operations to achieve Roche 14 scores with 15% lower inclusion rates and reducing feed costs by an estimated USD 0.02 per dozen eggs. Germany and France lead the adoption due to their concentration of large-scale compound-feed producers, which possess the capital and technical expertise to validate encapsulated ingredients through controlled feeding trials.

Regulatory Easing on Algal Pigment Approvals

The European Food Safety Authority (EFSA) has streamlined its approval pathway for algae-derived additives, reducing dossier review times by one-third since 2024. This reflects the agency's recognition that spirulina and Haematococcus extracts pose a lower toxicological risk profile than novel synthetic compounds. EW Nutrition GmbH secured approval for a lutein-rich Tagetes extract for turkeys in October 2024, with a maximum inclusion of 80 milligrams per kilogram, which is double the limit for broilers. This approval opens a differentiated segment for producers targeting skin pigmentation in heavy tom lines. Long-term supply certainty for integrators planning multi-year genetics programs, as per the European Food Safety Authority (EFSA). Russia has adopted a parallel fast-track process for feed additives that mirrors Europe Union approvals, reducing the lag time for ingredient availability in the Russian market from 24 months to under 12 months and supporting the country's pigment consumption as domestic aquafeed mills ramp up production.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile raw-material costs | -0.8% | Germany, France, Spain, Italy, and United Kingdom | Short term (≤ 2 years) |

| Stringent maximum inclusion limits by European Food Safety Authority (EFSA) | -0.5% | Germany, France, Spain, Italy, United Kingdom, and Russia | Long term (≥ 4 years) |

| Slow farmer adoption in Central and Eastern Europe | -0.3% | Russia, and Rest of Europe | Medium term (2-4 years) |

| Supply constraints of natural pigment biomass | -0.4% | Spain, France, and Italy | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Volatile Raw-Material Costs

Natural astaxanthin derived from Haematococcus algae was traded between USD 6,000 and USD 7,150 per kilogram in 2024, roughly six times the cost of synthetic astaxanthin at USD 1,000 per kilogram, creating margin pressure for aquafeed mills that market premium, all-natural salmon diets [2]Source: Food and Agriculture Organization, “Price Trends for Natural Astaxanthin,” Fao.org. Marigold oleoresin prices surged 18% year-over-year in 2024, driven by reduced harvests in India and Mexico, the two largest exporters, as well as a tightening European paprika supply following Spain's 12% yield decline due to drought. Aquaculture operators in Norway and Scotland have responded by blending natural and synthetic astaxanthin at ratios of 30:70 or 40:60, preserving the label claims of containing natural pigments while managing input costs, though this strategy risks consumer backlash if ingredient transparency becomes a competitive battleground.

Stringent Maximum Inclusion limits by European Food Safety Authority (EFSA)

European Food Safety Authority (EFSA) enforces maximum inclusion caps for several carotenoids, most notably a 25-milligram-per-kilogram limit for canthaxanthin in layer and broiler diets and a 100-parts-per-million ceiling for astaxanthin in salmonid feeds, which constrain formulators' ability to achieve target pigmentation scores in high-performance genetics. BioMar's technical guidance, published in 2024, recommends a 50-parts-per-million astaxanthin inclusion to optimize flesh-color retention economics. The guidance notes that exceeding 80 parts per million delivers diminishing returns on SalmoFan scores while increasing feed costs by USD 0.15 per kilogram. These regulatory ceilings create a structural demand ceiling for high-potency pigments, redirecting innovation toward bioavailability enhancement and encapsulation rather than higher-dose applications.

*Our updated forecasts treat driver/restraint impacts as directional, not additive. The revised impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Carotenoids Anchor Market, Spirulina Gains Aquaculture Traction

Carotenoids captured 61.45% of the Europe feed pigments market size in 2025, underpinned by their versatility across poultry, aquaculture, and swine applications, where lutein, zeaxanthin, astaxanthin, and canthaxanthin serve both pigmentation and immune-support functions. Curcumin remains a niche segment, primarily deployed in organic poultry systems, where turmeric's antioxidant properties complement its mild yellow pigmentation. Although the Europe Food Safety Authority (EFSA) has not issued specific inclusion guidelines, formulators rely on Generally Recognized as Safe (GRAS) precedents from the food sector. Caramel colorants capture a minimal share in feed applications, primarily used in specialty pet-food formulations where the visual appeal to human purchasers outweighs the ingredient's negligible nutritional contribution.

Spirulina is projected to grow at a 9.25% CAGR through 2031, driven by European aquaculture's pivot toward algae-derived pigments that align with clean-label positioning and the Europe Food Safety Authority (EFSA) streamlined approval pathway for botanical extracts. Spirulina's dual functionality as a protein source and pigment positions it for incremental share gains in aquaculture, particularly as Norwegian and Scottish salmon farms seek to differentiate from Chilean competitors that rely on synthetic astaxanthin, though European cultivation capacity remains below 2,000 metric tons annually and forces mills to import dried biomass from Asia at a 25 to 30% cost premium .

By Animal: Poultry Dominates, Aquaculture Expands Fastest

Poultry applications held 70.36% of the Europe feed pigments market size in 2025, reflecting the sector's scale and the direct link between yolk color and consumer purchasing decisions in Germany, France, and Spain, where retailers specify Roche scores of 14 or higher for premium egg lines. Swine applications capture a single-digit share, concentrated in Spain and Italy, where producers use paprika oleoresin to enhance cured-ham color and appeal to premium export markets, though this remains a low-volume niche relative to poultry and aquaculture. Ruminant pigment use is negligible, as beef and dairy products derive color from endogenous myoglobin and beta-carotene metabolism rather than dietary supplementation, leaving carotenoids relevant only in specialty veal operations targeting pale-pink flesh for Continental European buyers.

Aquaculture is set to grow at an 8.05% CAGR through 2031, propelled by rising European salmon and trout production and the need to meet retailer color specifications under Europe Food Safety Authority (EFSA) 100-parts-per-million astaxanthin cap, which has forced mills to optimize blended carotenoid strategies pairing astaxanthin with canthaxanthin or lutein. Russia's 50,000 metric tons aquafeed plant, which opened in 2024, signals the country's intention to scale domestic salmon farming. Pigment inclusion rates remain 20 to 30% below Norwegian benchmarks due to limited technical support and a fragmented distribution network.

Geography Analysis

Germany accounted for 18.32% of the revenue in 2025, anchored by its 50-million-layer flock and consumer willingness to pay premiums for Roche-scale 14 yolks, which translate into lutein and zeaxanthin inclusion rates of 20 to 30 milligrams per kilogram in layer diets. The country's large-scale compound-feed producers, including Deutsche Tiernahrung Cremer and Agravis Raiffeisen, have adopted microencapsulated carotenoids that maintain 95% potency after six months of ambient storage, thereby reducing over-formulation waste and lowering raw material costs by an estimated 3%. Italy accounts for a significant share, supported by its aquaculture sector and niche demand for paprika in cured-ham production. The United Kingdom holds a significant share, with ForFarmers' June 2025 launch of an organic paprika yolk colorant targeting free-range producers supplying Waitrose and Marks and Spencer.

Russia is forecast to deliver the fastest growth, with a 7.22% CAGR through 2031, propelled by new aquafeed capacity and import-substitution policies that favor domestic pigment blending. Adoption rates remain 20 to 30% below Western European benchmarks due to limited technical support and a fragmented distribution network. The country's 50,000 metric tons aquafeed plant, which opened in 2024, signals intent to scale domestic salmon farming, yet pigment inclusion rates lag Norwegian standards, creating a latent opportunity for ingredient suppliers willing to invest in local technical service teams.

Poland, Romania, and smaller markets contribute a significant share in 2025 but grow at below-average rates due to slower adoption of natural pigments and a historical focus on least-cost feed formulations. Poland's egg sector remains 70% reliant on synthetic canthaxanthin, compared with 40% in Germany, because Polish retailers have not imposed the same Roche-score specifications as their Western counterparts. This adoption gap constrains near-term growth but represents a structural opportunity as retail consolidation and export-market access drive quality standardization across Central and Eastern Europe over the next five years.

Competitive Landscape

The Europe feed pigments market demonstrates moderate concentration, with leading players holding the largest market share in 2024. This leaves opportunities for regional specialists and botanical-extract suppliers to target niche segments. Technology plays a critical role, with advancements such as microencapsulation patents enabling suppliers to enhance bioavailability and shelf stability. For instance, DSM-Firmenich's lipid-matrix beadlets retain 95% of their pigment potency after six months, compared to 70% for uncoated powders, thereby reducing over-formulation waste and lowering raw material costs by around 3%.

Major players in the European feed pigment market prioritize product innovation, focusing on bio-based and fermentation-derived pigments to align with European Union sustainability requirements. Significant investments are directed toward encapsulation and stabilization technologies to improve pigment effectiveness during feed processing. Strategic collaborations with aquaculture and poultry integrators enable the co-development of tailored solutions. Additionally, companies are expanding regional manufacturing capabilities to strengthen supply chains and reduce dependence on imports. Efforts also include participation in regulatory advocacy and certification initiatives to accelerate the approval of natural alternatives and enhance consumer confidence in pigment-based animal products.

Opportunities in the market include the cultivation of spirulina within Europe, where current annual production remains below 2,000 metric tons. This shortfall forces aquafeed mills to import dried biomass from Asia at a 25–30% cost premium, presenting an opportunity for vertically integrated players willing to invest in photobioreactor infrastructure. A notable example is EW Nutrition GmbH's October 2024 approval by the European Food Safety Authority (EFSA) for a lutein-rich Tagetes extract for turkeys, allowing for the inclusion of up to 80 milligrams per kilogram. This highlights how expertise in regulatory dossiers can unlock differentiated market segments. Smaller players, such as Nutrex and Impextraco, leverage regional distribution networks and technical services to compete by offering formulation support, targeting mid-sized integrators that lack in-house nutrition expertise.

Europe Feed Pigments Industry Leaders

DSM-Firmenich AG

BASF SE

Kemin Industries Inc.

EW Nutrition GmbH

Nutrex N.V.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2024: ADM completed the acquisition of NutraColor, a leading Spanish manufacturer of natural feed pigments, strengthening ADM’s position in the European animal nutrition market.

- September 2022: DSM acquired Prodap, a Brazilian animal nutrition and technology company that combines technology offerings, consulting services, and specialized nutritional solutions, including animal feed pigments to enhance animal farming efficiency and sustainability.

- July 2022: Impextraco, a Belgium-based manufacturer of animal feed pigments and feed solutions, expanded its Mexico facility to increase product storage capacity and enhance business opportunities.

Europe Feed Pigments Market Report Scope

Feed pigments are compounds that are added to feed and are responsible for the color of products. The market is segmented by Type (Carotenoids, Curcumin, Caramel, Spirulina, and Others), Animal (Ruminant, Poultry, Swine, and Aquaculture), and Geography (Spain, United Kingdom, Germany, France, Italy, Russia, and Rest of Europe). The report offers the market size and forecasts in value (USD) for all the above segments.

By Type

| Carotenoids |

| Curcumin |

| Caramel |

| Spirulina |

| Others |

By Animal

| Poultry |

| Swine |

| Ruminant |

| Aquaculture |

By Geography

| Germany |

| Spain |

| France |

| Italy |

| United Kingdom |

| Russia |

| Rest of Europe |

| By Type | Carotenoids |

| Curcumin | |

| Caramel | |

| Spirulina | |

| Others | |

| By Animal | Poultry |

| Swine | |

| Ruminant | |

| Aquaculture | |

| By Geography | Germany |

| Spain | |

| France | |

| Italy | |

| United Kingdom | |

| Russia | |

| Rest of Europe |

Key Questions Answered in the Report

What is the projected value of the Europe feed pigments market by 2031?

The market is forecast to reach USD 1.84 billion by 2031.

Which ingredient type leads demand across Europe?

Carotenoids held 61.45% of 2025 revenue, making them the dominant pigment group.

Why is spirulina growing faster than other pigment sources?

Spirulina aligns with clean-label trends and delivers dual protein and pigment benefits, supporting a 9.25% CAGR through 2031.

Which animal segment shows the fastest pigment adoption?

Aquaculture is advancing at an 8.05% CAGR as salmon farms tailor carotenoid blends to meet retailer flesh-color standards.

Page last updated on: