| Study Period | 2019 - 2030 |

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

| Market Size (2025) | USD 428.37 Million |

| Market Size (2030) | USD 531.28 Million |

| CAGR (2025 - 2030) | 4.40 % |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order |

Brazil Forage Seed Market Analysis

The Brazil Forage Seed Market size is estimated at USD 428.37 million in 2025, and is expected to reach USD 531.28 million by 2030, at a CAGR of 4.4% during the forecast period (2025-2030).

The Brazilian forage seed industry operates within one of the world's largest agricultural landscapes, with pastures totaling 162.5 million hectares according to recent ABIEC data. The country's continental dimensions and favorable climate for grass seed plant growth have enabled Brazil to achieve a prominent position in the global scenario. This vast agricultural foundation has led to Brazil maintaining its position as the world's largest commercial beef cattle herd owner, accounting for approximately 14.7% of the global total. The industry's structure is characterized by a mix of traditional farming practices and modern agricultural technologies, with increasing emphasis on sustainable and efficient forage seed production methods.

The market landscape is dominated by specific grass varieties, with cultivated fodder seed grasses of exotic species introduced from the African continent occupying 60-70% of the total pasture seed area. Notably, Brachiaria and Panicum varieties have emerged as the predominant choices, covering over 60 million hectares and accounting for more than 70% of marketed seeds in the country. This concentration in specific varieties has led to increased focus on genetic diversity and research initiatives to prevent vulnerability to diseases and pest attacks. The industry has witnessed significant technological advancements in seed treatment and coating technologies, with a growing trend toward the use of incrusted seeds over the past five years.

The Brazilian Agricultural Research Corporation (EMBRAPA) has been at the forefront of innovation in the sector, exemplified by the introduction of BRS Integra in 2022, a new forage seed plant specifically developed for Brazilian soil and climate conditions. This development represents a significant advancement in integrated crop-livestock-forestry systems (ICLFS), offering increased fodder production between harvests and improved nutritional value. The research landscape continues to evolve through partnerships between public and private entities, with organizations like the Association for the Promotion of forage seed Breeding Research collaborating with EMBRAPA to develop new grassland seed cultivars.

The industry is experiencing a notable shift in quality standards and production practices, particularly in the export market versus domestic consumption. While seeds destined for export markets maintain higher purity standards, the domestic market is gradually adapting to improved quality requirements. The introduction of hybrid seeds, although currently limited in scale, represents a significant technological advancement in the sector. This development is accompanied by increasing investment in research and development activities focused on genetic improvements and climate change adaptation, indicating a progressive transformation in the industry's approach to seed development and production.

Brazil Forage Seed Market Trends

INCREASE IN DEMAND FOR ANIMAL PRODUCTS

Brazil's consumption of animal products, particularly milk and meat, has been experiencing substantial growth due to increasing awareness of health benefits and rising protein demand. The country currently maintains 1,822 dairies, with the state of Minas Gerais hosting the largest concentration of dairy operations, featuring farm sizes averaging up to 100 hectares. The dairy industry has shown remarkable progress in productivity, achieving 6.0 liters per cow per day in 2022 through the implementation of advanced forage grass silage techniques, which has directly contributed to the escalating demand for quality forage seed.

The dairy production landscape across Brazil shows significant regional variation, with approximately 70% of production concentrated in the South and Southeast regions. The South region alone produces 9.9 million liters of cow milk, representing 33% of national production, while the Southeast contributes 11.1 million liters, accounting for 36.9% of the total production. The industry has witnessed growing production costs but maintained steady growth in the production of cheese, butter, and milk powder, particularly driven by the revival of the food service industry and the end of market restrictions. This sustained growth in dairy production has created a robust demand for high-quality fodder seed, as farmers increasingly recognize the direct correlation between feed quality and dairy product excellence.

Understand The Key Trends Shaping This Market

Download PDF

RISE IN DEMAND FOR FORAGE CROPS

The Brazilian agricultural landscape has witnessed a significant transformation in forage crop cultivation, with 60-70% of the area now occupied by cultivated pasture grass seed of exotic species introduced from the African continent. These crops, particularly Panicum and Brachiaria varieties, cover over 60 million hectares of pasture and account for more than 70% of the marketed seeds. The industry has shown a clear northward movement toward Mato Grosso and Goiás states, where economic, agricultural, and social conditions are more conducive to pasture seed production activities.

The corn production sector, particularly in the Midwestern states of Brazil, has experienced substantial growth, with Mato Grosso leading production at 43.8%, followed by Paraná (16.3%), Mato Grosso do Sul (13.4%), Goiás (12.8%), and Minas Gerais (4.5%). The tropical climate in these regions enables the innovative practice of planting soybeans in summer followed by corn in winter on the same land, maximizing land utilization and creating additional opportunities for the grass seed industry. This agricultural intensification, combined with the crops' contribution to improving water quality, rotation benefits, and wildlife habitat enhancement, has significantly boosted the demand for legume seed across the country.

GROWING LIVESTOCK POPULATION

Brazil's livestock sector has experienced substantial growth, with approximately 60% of the country's cattle herd concentrated in the Center-West and northern regions, primarily in the states of Mato Grosso, Mato Grosso do Sul, and Pará, with significant production in the pre-Amazon area. The livestock industry has shown remarkable advancement in production efficiency through long-term programs aimed at improving sector efficiency and government credit programs, estimated at USD 1.1 billion, which support increased cattle productivity, herd quality enhancement through pasture improvement, and acquisition of high-quality seed stock.

The country's livestock production landscape has evolved significantly, with hog producers concentrated in the three southern states of Santa Catarina, Paraná, and Rio Grande do Sul. The Brazilian Agricultural Research Company has reported significant developments in production costs and efficiency metrics, with nutrition costs accounting for 76.3% of the total cost of hog production in Santa Catarina. This increasing focus on production efficiency and quality has created a strong demand for better grass seed, as producers become increasingly concerned about the quality of meat they produce, driving the need for higher-quality legume seed to support the growing livestock population.

Segment Analysis: Crop Type

Grasses Segment in Brazil Forage Seed Market

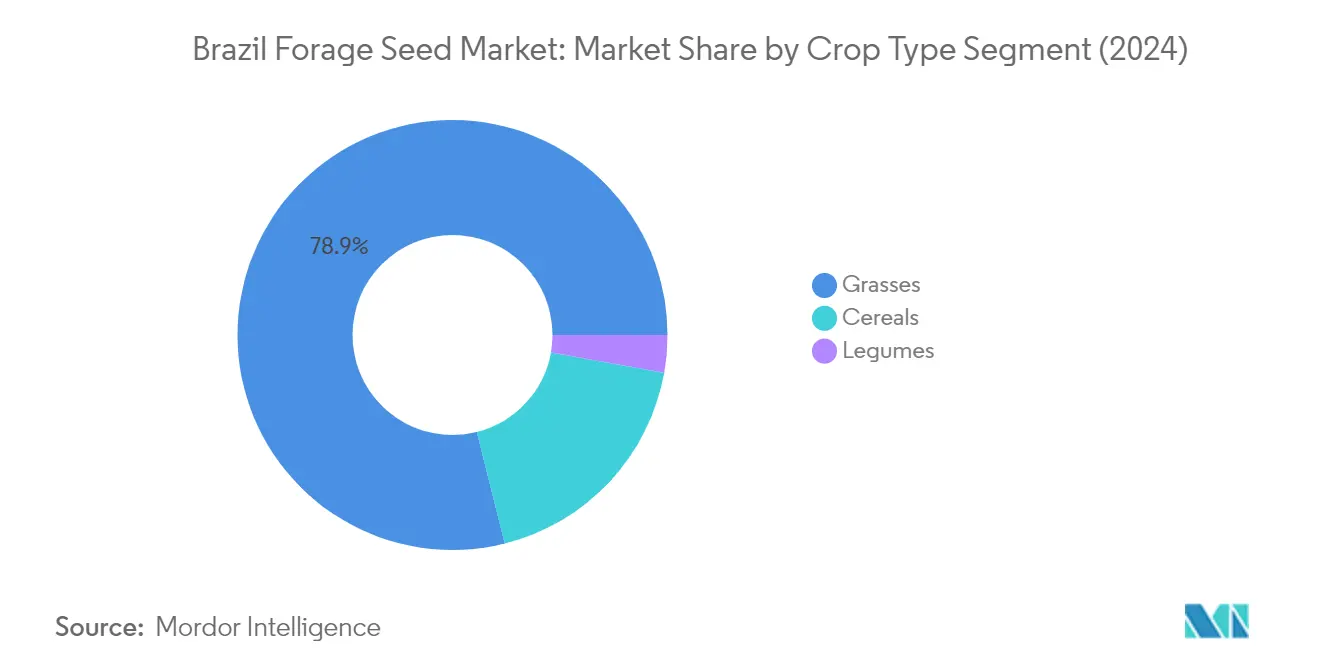

The grass seed segment continues to dominate the Brazil forage seed market, accounting for approximately 79% of the total market value in 2024. This substantial market share is primarily attributed to the development of new forage plants specifically designed for Brazilian soil and climate conditions. The segment's growth is further supported by tailored integrated crop-livestock-forestry systems such as BRS Integra, which provide increased fodder production between harvests. Grasses like ryegrass, cultivated from March to May with around 20 to 30 kilograms of grass seed spread per hectare, contribute significantly to the segment's dominance. Additionally, the introduction of Sudangrass, known for its drought resilience and suitability for rotational grazing in Brazil, has strengthened the segment's position in the market.

Legumes Segment in Brazil Forage Seed Market

The legume seed segment is projected to experience the highest growth rate of approximately 9% during the forecast period 2024-2029. This accelerated growth is primarily driven by the increasing recognition of legume seed as a sustainable alternative for animal feeding, owing to their high nutritional value and ability to form symbiotic relationships with nitrogen-fixing bacteria. The segment's growth is further supported by the rising adoption of alfalfa seed, particularly in the southern states of Rio Grande do Sul and Paraná, where it demonstrates impressive crude protein content ranging from 18% to 26%. The segment is also benefiting from the increasing utilization of various clover seed varieties, including white clover, Persian clover, and red clover, which are typically used in combination with oats and ryegrass to enhance pasture quality.

Remaining Segments in Crop Type

The cereals segment plays a crucial role in the Brazil forage seed market, offering essential options for livestock feed through crops like forage corn and forage sorghum. This segment is particularly significant in supporting the dairy and poultry industries, especially in southern Brazil. Forage corn has gained prominence due to its high capacity for dry matter production and ease of harvesting, while sorghum has become increasingly important for managing farmlands with varying elevations and climates. The segment's impact is further enhanced by the development of small grain cereal grasses, such as rye, oats, triticale, and wheat, which provide valuable complements to other winter annual grasses and help extend the grazing season.

Brazil Forage Seed Industry Overview

Top Companies in Brazil Forage Seed Market

The Brazil forage seed market is characterized by a mix of global agricultural giants and local specialists, with companies like DLF Seeds & Science, Corteva Agriscience, and KWS SAAT SE leading the innovation curve. Product development has been primarily focused on creating climate-resilient varieties and improving nutritional content for livestock feed, with companies investing heavily in research and development capabilities. Strategic partnerships and acquisitions have been relatively limited, with companies instead focusing on expanding their distribution networks and strengthening their local presence through direct engagement with farmers. The emphasis has been on developing specialized seed varieties suited to Brazilian soil and climate conditions, particularly in the areas of Brachiaria and Panicum seeds. Companies are increasingly integrating digital technologies and precision agriculture solutions into their product offerings to provide comprehensive solutions to farmers.

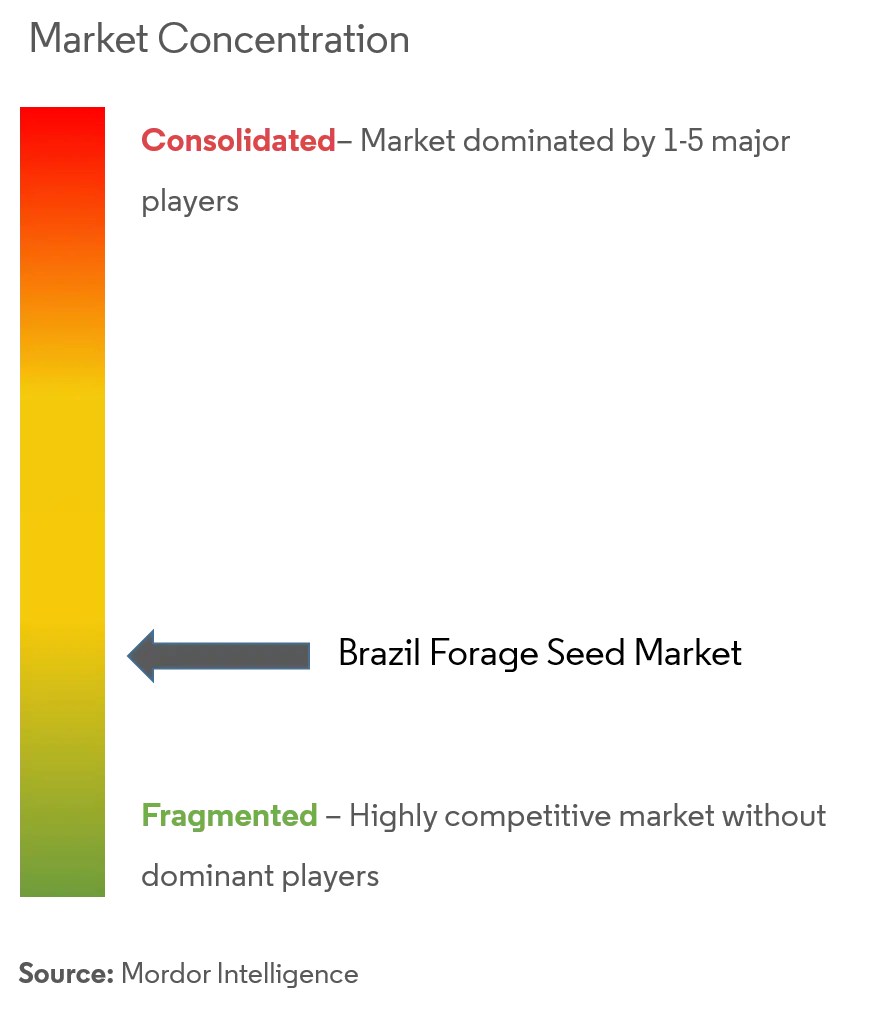

Fragmented Market with Strong Local Players

The Brazilian forage seed market exhibits a highly fragmented structure, with numerous regional players maintaining significant market presence alongside multinational corporations. Local companies like Agroquima, Wolf Sementes, and Safrasul Sementes have carved out strong niches through their deep understanding of regional farming practices and close relationships with local distributors. The market's fragmentation is further reinforced by the diverse geographical requirements across Brazil's various agricultural regions, leading to specialized product offerings tailored to specific climatic zones. The competitive dynamics are shaped by companies' ability to maintain robust research and development capabilities while simultaneously building strong distribution networks across the country's vast agricultural landscape.

The market has witnessed limited consolidation activity, with most companies focusing on organic growth rather than acquisitions. Global players have primarily entered the market through establishing local subsidiaries or forming partnerships with established Brazilian companies rather than through direct acquisitions. The competitive landscape is characterized by companies focusing on developing specialized product portfolios and building strong technical support networks to assist farmers in optimizing their pasture seed production. This approach has led to a market structure where success is determined by a combination of product quality, local market knowledge, and after-sales support capabilities.

Innovation and Distribution Drive Market Success

For established players to maintain and expand their market share, the focus needs to be on developing innovative seed varieties that address specific challenges faced by Brazilian farmers, particularly in terms of climate resilience and productivity. Companies must invest in building comprehensive research and development capabilities while simultaneously strengthening their distribution networks to ensure widespread product availability. Success in the market increasingly depends on the ability to provide integrated solutions that combine high-quality seeds with technical support and digital farming tools. The development of strong relationships with key agricultural institutions and research organizations has become crucial for maintaining competitive advantage.

New entrants and smaller players can gain ground by focusing on specialized market segments and developing products tailored to specific regional requirements. The key to success lies in building a strong local presence through partnerships with distributors and agricultural cooperatives, while also investing in technical support capabilities. Companies need to consider the growing importance of sustainability and environmental concerns in agricultural practices, adapting their product development and marketing strategies accordingly. The regulatory environment, particularly regarding seed certification and quality standards, continues to play a crucial role in shaping market dynamics, making compliance capabilities a critical success factor for all market participants. Additionally, the integration of grass seed and legume seed varieties into product offerings can further enhance market competitiveness.

Brazil Forage Seed Market Leaders

-

Agria Corporation

-

Advanta Seeds (UPL)

-

Wolf Sementes

-

Germisul Seeds Ltd

-

MN Agro Consulting In Seeds & Agribusiness

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competiters?

Download PDF

Brazil Forage Seed Market News

July 2022: Corteva Agriscience introduced Bovalta BMR (brown midrib) corn silage product designed to meet the highest standards for yield and milk production.

Brazil Forage Seed Market Report - Table of Contents

1. INTRODUCTION

- 1.1 Study Deliverables and Market Definition

- 1.2 Study Assumptions

- 1.3 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.3 Market Restraints

-

4.4 Porters five Force Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5. MARKET SEGMENTATION

-

5.1 By Crop Type

- 5.1.1 Cereals

- 5.1.1.1 Forage Corn

- 5.1.1.2 Forage Sorghum

- 5.1.1.3 Other Cereals

- 5.1.2 Legumes

- 5.1.2.1 Alfalfa

- 5.1.2.2 Other Legumes

- 5.1.3 Grasses

-

5.2 By Product Type

- 5.2.1 Stored Forage

- 5.2.2 Fresh Forage

-

5.3 By Animal Type

- 5.3.1 Ruminant

- 5.3.2 Swine

- 5.3.3 Poultry

- 5.3.4 Other Animal Types

6. COMPETITIVE LANDSCAPE

- 6.1 Market Share Analysis

- 6.2 Most Adopted Strategies

-

6.3 Company Profiles

- 6.3.1 Agria Corporation

- 6.3.2 Advanta Seeds (UPL)

- 6.3.3 Wolf Sementes

- 6.3.4 Germisul Seeds Ltd

- 6.3.5 MN Agro Consulting In Seeds & Agribusiness

- 6.3.6 DLF Seeds and Science

- 6.3.7 Deutsche Saatveredelung AG

- 6.3.8 Corteva Agriscience

- 6.3.9 SGM Group

- *List Not Exhaustive

7. MARKET OPPORTUNITIES AND FUTURE TRENDS

You Can Purchase Parts Of This Report. Check Out Prices For Specific Sections

Get Price Break-up Now

Brazil Forage Seed Industry Segmentation

Forages are plants or parts of plants eaten by herbivorous animals. The report covers the seed market of forage crops and the analysis of different types of forages. The information regarding market overview, especially in terms of maturity provided in the study, is essential towards developing apt growth strategies suitable for Brazil considered in the study. Profiles of major players active in countries studied will provide decisive information towards developing a competitive strategy.

| By Crop Type | Cereals | Forage Corn | |

| Forage Sorghum | |||

| Other Cereals | |||

| Legumes | Alfalfa | ||

| Other Legumes | |||

| Grasses | |||

| By Product Type | Stored Forage | ||

| Fresh Forage | |||

| By Animal Type | Ruminant | ||

| Swine | |||

| Poultry | |||

| Other Animal Types | |||

Need A Different Region or Segment?

Customize Now

Brazil Forage Seed Market Research FAQs

How big is the Brazil Forage Seed Market?

The Brazil Forage Seed Market size is expected to reach USD 428.37 million in 2025 and grow at a CAGR of 4.40% to reach USD 531.28 million by 2030.

What is the current Brazil Forage Seed Market size?

In 2025, the Brazil Forage Seed Market size is expected to reach USD 428.37 million.

Who are the key players in Brazil Forage Seed Market?

Agria Corporation, Advanta Seeds (UPL), Wolf Sementes, Germisul Seeds Ltd and MN Agro Consulting In Seeds & Agribusiness are the major companies operating in the Brazil Forage Seed Market.

What years does this Brazil Forage Seed Market cover, and what was the market size in 2024?

In 2024, the Brazil Forage Seed Market size was estimated at USD 409.52 million. The report covers the Brazil Forage Seed Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Brazil Forage Seed Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Our Best Selling Reports

Brazil Forage Seed Market Research

Mordor Intelligence offers a comprehensive analysis of the Brazilian forage seed and fodder seed industry. With decades of agricultural research expertise, our report provides valuable insights. Available as an easy-to-download report PDF, it covers the complete spectrum of grass seed varieties, including clover seed, alfalfa seed, and legume seed segments. The analysis examines both traditional and emerging cultivation methods across Brazil's diverse agricultural regions.

The report provides detailed insights into pasture seed market dynamics. It includes production trends for pasture grass seed varieties and seeds for permanent pasture applications. Stakeholders gain a valuable understanding of grassland seed development and implementation strategies. This is supported by comprehensive data on cultivation patterns, regional demand variations, and technological innovations. This thorough analysis enables agricultural businesses, seed producers, and investors to make informed decisions. They can rely on reliable market intelligence and future growth projections.