Authentication Services Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 2.88 Billion |

| Market Size (2031) | USD 7.02 Billion |

| Growth Rate (2026 - 2031) | 19.51% CAGR |

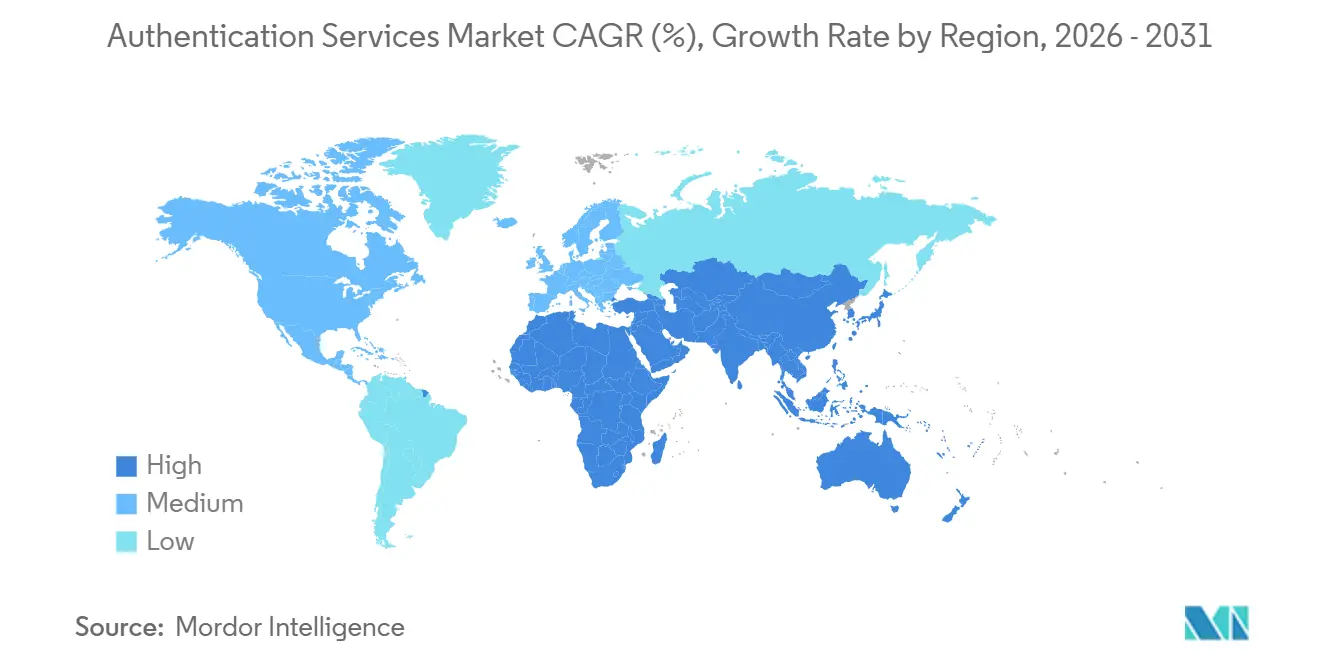

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Authentication Services Market Analysis by Mordor Intelligence

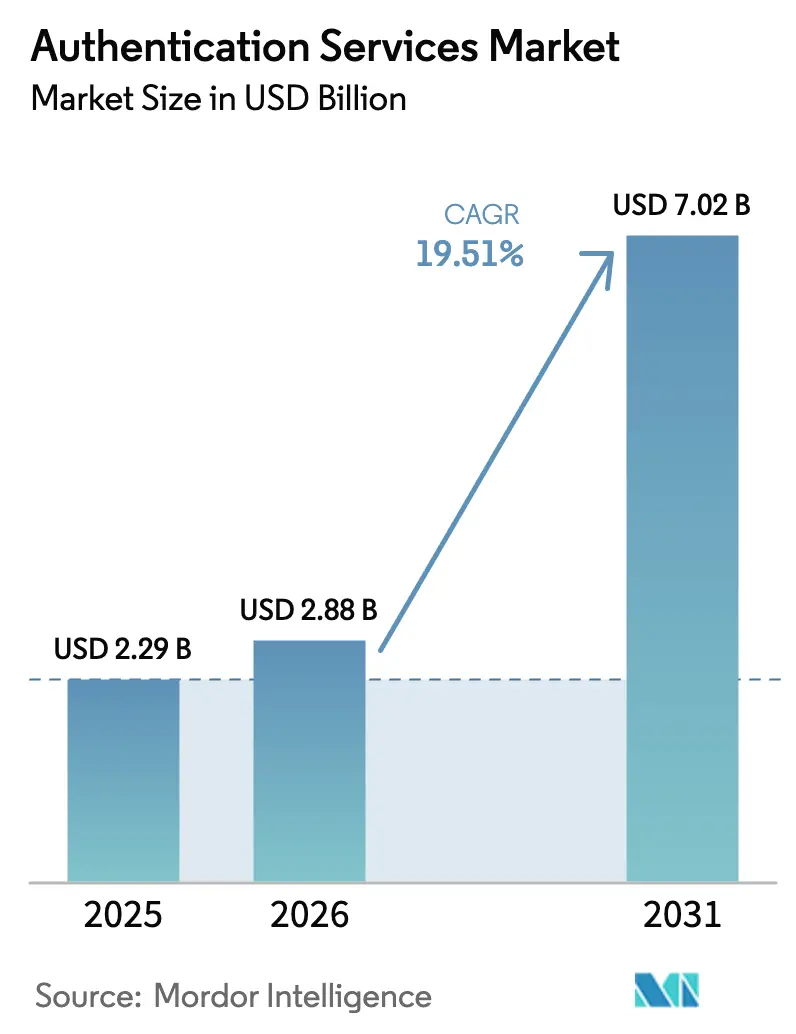

The authentication services market size is expected to grow from USD 2.29 billion in 2025 to USD 2.88 billion in 2026 and is forecast to reach USD 7.02 billion by 2031 at 19.51% CAGR over 2026-2031. Regulators mandate phishing-resistant verification under frameworks such as NIST SP 800-63-4 and the European Union’s eIDAS 2.0, while corporate boards tie revenue targets to friction-free login journeys that lower abandonment rates. These twin forces are shifting spending from passwords and SMS codes toward passkeys, biometrics, and risk-adaptive policy engines that plug directly into application programming interfaces. Cloud platforms accelerate adoption by bundling identity tools into consumption-based subscriptions, and chipmakers embed secure elements into devices at the factory, allowing credentials to be provisioned before shipment. Competition intensifies as hyperscalers undercut standalone vendors on price, and decentralized identity pilots test whether distributed ledgers can further trim recurring license fees.

Key Report Takeaways

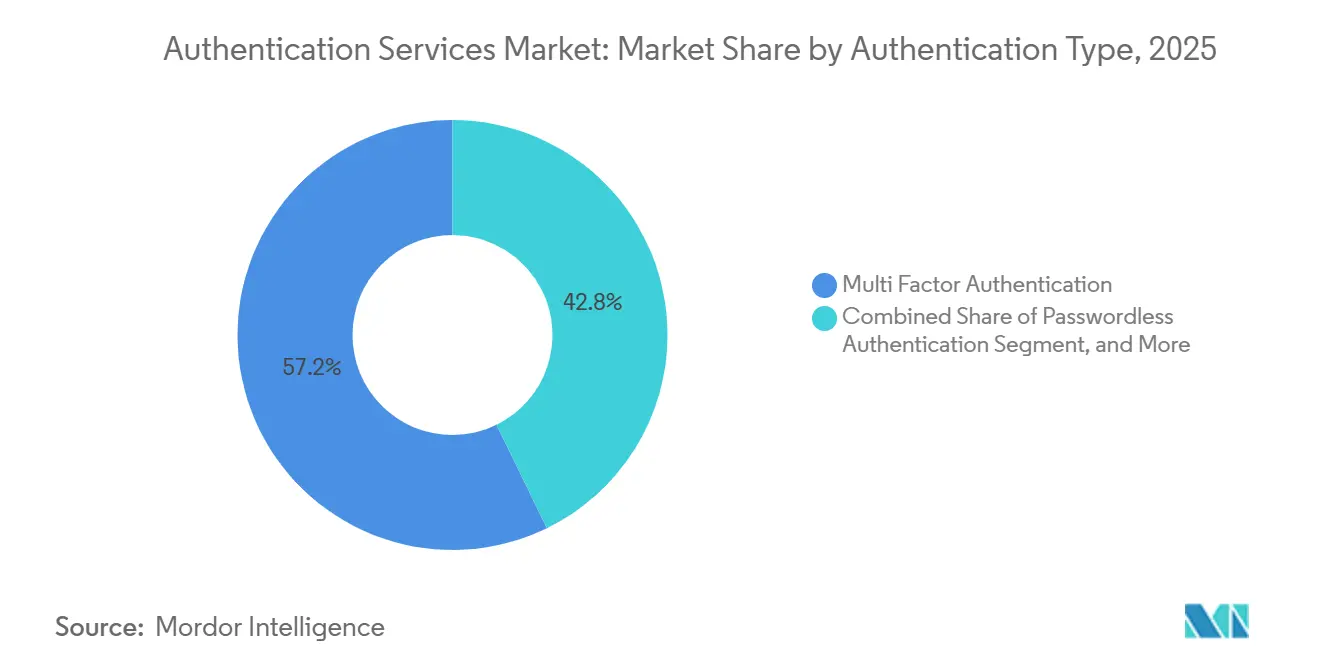

- By authentication type, Multi-Factor Authentication captured 57.24% of authentication services market share in 2025, while Passwordless Authentication is projected to expand at a 20.29% CAGR through 2031.

- By service type, managed public key infrastructure held 39.16% of the authentication services market share in 2025, whereas Risk-Based Authentication Orchestration is poised to post the fastest growth, at a 20.63% CAGR through 2031.

- By deployment mode, public cloud accounted for 63.29% of the revenue in 2025 and is also the fastest-growing segment, with a 20.44% CAGR over the forecast period.

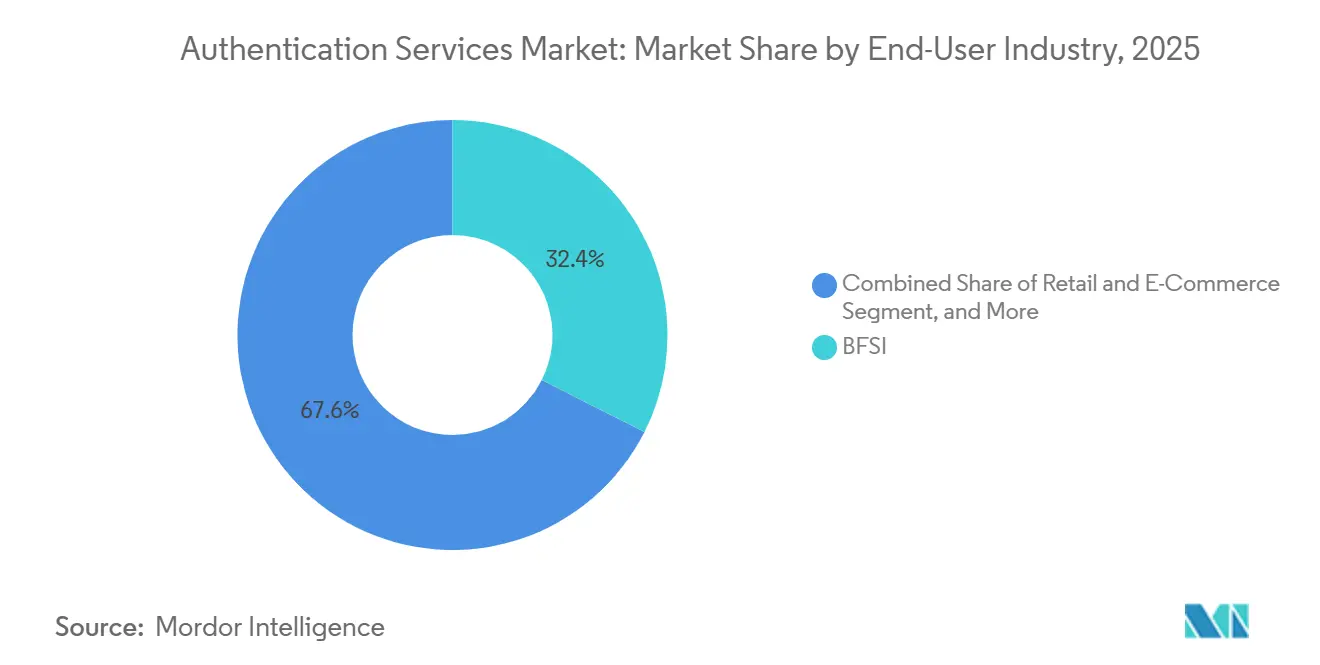

- By end-user industry, banking, financial services, and insurance led with a 32.44% share in 2025; however, Retail and E-Commerce is slated to advance at a 21.36% CAGR by 2031.

- By organization size, large enterprises generated 59.38% of spending in 2025, while Small and medium enterprises are set to register a 20.16% CAGR during the outlook period.

- By geography, North America dominated with a 36.71% share in 2025, whereas the Asia-Pacific region is projected to rise at the highest regional pace of 20.57% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Authentication Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growth in the Number of Digital Identities | +3.2% | Global, with concentration in Asia-Pacific and Europe | Medium term (2-4 years) |

| Authentication Needed for Security Compliance and Regulations | +4.1% | Global, led by North America and Europe, expanding to Asia-Pacific | Short term (≤ 2 years) |

| Growing Adoption of Bring Your Own Device (BYOD) | +2.8% | North America and Europe, emerging in Asia-Pacific urban centers | Medium term (2-4 years) |

| Increasing Cybersecurity Spending by Enterprises for Zero-Trust Initiatives | +4.5% | Global, strongest in North America and Europe | Short term (≤ 2 years) |

| Emergence of Passkeys and FIDO2 Standards Reducing UX Friction | +3.6% | Global, early adoption in North America and Asia-Pacific | Medium term (2-4 years) |

| Integration of Authentication APIs into Embedded IoT Modules Enabling Device-Level Revenue Streams | +2.7% | Global, concentrated in Asia-Pacific manufacturing hubs and North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Increasing Cybersecurity Spending for Zero-Trust Initiatives

Federal directives now require phishing-resistant multi-factor authentication for all United States civilian agencies by fiscal 2027, sparking immediate procurement of FIDO2-certified tokens and risk engines.[1]Office of Management and Budget, “Federal Zero Trust Strategy Memorandum,” whitehouse.gov European banks face oversight under the Digital Operational Resilience Act, which classifies identity systems as critical, driving 2025 budgets toward adaptive controls. Enterprises report sharper visibility into credential misuse as zero-trust rollouts cut mean-time-to-detect compromised accounts by one-third, yet hybrid architectures remain complex because legacy directories lack real-time policy hooks. Vendors respond with cloud gateways that translate Security Assertion Markup Language into modern RESTful calls, thereby lowering the migration risk. The driver adds 4.5 percentage points to forecast growth and peaks through 2028 as multiple regulatory deadlines converge.

Emergence of Passkeys and FIDO2 Standards Reducing UX Friction

Apple, Google, and Microsoft activated passkey support on 2.1 billion devices in 2025, embedding cryptographic authenticators inside operating-system credential managers and erasing password fatigue for everyday logins.[2]FIDO Alliance, “Passkey Adoption Statistics,” fidoalliance.org The WebAuthn Level 3 specification enables cloud-encrypted credential backup, solving the device-loss hurdle that once slowed adoption. E-commerce sites report a 41% decline in cart abandonment after switching from SMS codes to passkeys. Financial regulators in Japan and South Korea now classify passkeys as baseline controls for consumer apps, nudging banks to sunset legacy credentials. The standard’s usability boost translates into a 3.6-point lift in CAGR as enterprises retool help desks and migrate credential stores.

Growth in the Number of Digital Identities

Government programs issued more than 5.2 billion digital IDs in 2025, propelled by India’s Aadhaar, Indonesia’s e-KTP, and Nigeria’s NIN projects.[3]World Bank, “Global Digital Identity Programs,” worldbank.org Aadhaar alone processed 102 billion authentications that year, weaving biometric checks into banking, health, and welfare portals. Europe’s eIDAS 2.0 obliges member states to deploy interoperable wallets by 2026, generating demand for providers that can bridge public and private credentials. Enterprises that tap into pre-verified IDs reduce onboarding costs by more than one-quarter and shorten revenue recognition cycles, resulting in a 3.2-point increase in market CAGR as wallet interoperability matures.

Integration of Authentication APIs into Embedded IoT Modules Enabling Device-Level Revenue Streams

Semiconductor firms shipped 1.4 billion IoT modules with onboard secure elements in 2025, representing a 22% year-over-year increase. Qualcomm’s Snapdragon IoT platform now includes a dedicated secure processing unit that runs FIDO Device Onboard, allowing manufacturers to inject keys during production and reduce supply-chain attack surfaces. European utilities rolled out 18 million smart meters using hardware-rooted credentials to comply with the Network and Information Security Directive. Vendors monetize these modules through subscription plans, bundling key rotation and anomaly detection, which creates annuity streams that lift the CAGR by 2.7 points over the long term.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Cost Involved with Matured Authentication Methods | -1.9% | Global, acute in cost-sensitive SME segments and emerging markets | Medium term (2-4 years) |

| User Fatigue and Login Abandonment due to MFA Complexity | -2.4% | Global, concentrated in consumer-facing applications in North America and Europe | Short term (≤ 2 years) |

| Chip Supply Constraints for Hardware Security Modules Post-2025 Tariffs | -1.6% | Global, most severe in North America and Europe | Short term (≤ 2 years) |

| Fragmentation of National Digital Identity Schemes Hindering Cross-Border Authentication | -2.1% | Global, particularly Europe, Asia-Pacific, and cross-Atlantic corridors | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Cost Involved with Matured Authentication Methods

FIDO2 hardware tokens run USD 25-55 per user, a hurdle for price-sensitive small businesses. Biometric sensors embedded in laptops or smartphones can lower costs over time, but early upgrades still require capital expenditure that competes with payroll and marketing expenses. Emerging-market buyers face import tariffs on security modules, which raise the total cost of ownership by double digits. Vendors respond with per-user subscription models starting at USD 3 monthly, yet budget holders often delay refresh cycles until insurance underwriters or regulators force the issue. The cost headwind reduces the anticipated CAGR by 1.9 points until economies of scale drive unit prices below mass-market thresholds.

User Fatigue and Login Abandonment Due to MFA Complexity

Help desks reported a 31% increase in lockout tickets in 2025, as employees managed an average of 14 credential workflows, leading to dissatisfaction and shadow IT workarounds. The United Kingdom’s National Cyber Security Centre found that 42% of users who faced delayed SMS codes abandoned online transactions, reverting to lower-security channels. Banks in the United States reported a 19% opt-out rate from mobile biometrics following repeat false rejections, which inflated password use and increased credential-stuffing risk. Adaptive risk engines can silence prompts for low-value transactions, but tuning errors either annoy customers or invite fraud. This friction reduces growth by 2.4 points until biometrics and passkeys replace step-up factors entirely.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Authentication Type: Passwordless Momentum Builds on MFA Foundation

Multi-Factor Authentication retained 57.24% of the authentication services market share in 2025, underscoring its role as the regulatory minimum for high-value workflows. Passwordless approaches, however, are projected to outpace every other category at a 20.29% CAGR to 2031, signaling management’s drive to cut reset tickets and phishing exposure. The authentication services market is expected to benefit from 340 million passkeys registered in 2025, following Google Workspace's introduction of passwordless accounts for 180 million users.

Passwordless growth is not uniform. Healthcare pilots in the United States shaved 18 seconds off each clinician's login time, freeing almost 2.3 hours weekly for patient care. European banks exploit exemptions in the revised Payment Services Directive that allow biometric-only flows below EUR 500, provided devices bind credentials and behavioral analytics confirm identity. Retailers that deploy passkeys have seen a 29% increase in repeat purchases, as smoother checkout experiences foster loyalty. Manufacturing and energy firms still rely on hardware tokens because air-gapped operational technology cannot support frequent firmware updates, thereby delaying widespread passwordless adoption in these verticals.

By Service Type: Risk-Based Orchestration Becomes the Differentiator

Managed Public Key Infrastructure generated 39.16% of 2025 revenue, indicating enterprises' desire to outsource certificate lifecycle tasks subject to WebTrust and ETSI audits. Yet Risk-Based Authentication Orchestration is forecast to deliver a 20.63% CAGR, riding insurer and bank appetite for context-aware trust decisions. Adaptive engines now score device health, geolocation anomalies, and micro-behavioral inputs such as keystroke cadence, stepping up verification only when risk indicators spike.

Subscription key management reduces manual rotation time for secrets stored in microservices, a task that consumed 14 engineering hours per month in 2025. Reporting and analytics modules integrate evidence into SOC 2 and ISO 27001 packages, reducing audit preparation by 40%. Financial regulators in Singapore and Hong Kong direct institutions to monitor anomalies in real time, pushing the authentication services market toward SaaS dashboards that expose risk metrics by user, device, and geography. U.S. energy utilities incorporate adaptive controls into their supervisory control and data acquisition (SCADA) layers to meet CISA’s cross-sector performance goals.

By Deployment Mode: Public Cloud Sets the Pace

Public Cloud captured 63.29% of spending in 2025 and is expected to rise at a 20.44% CAGR as Azure, AWS, and Google Cloud integrate identity APIs into their platform subscriptions. Microsoft Entra now handles 300 million enterprise seats with sub-100 millisecond latency via 60 sovereign cloud regions. The authentication services market size for on-premises deployments continues to shrink in commercial segments but persists in defense, where the Cybersecurity Maturity Model Certification demands locally hosted token stores.

Private Cloud appeals to banks and hospitals that require single-tenant setups to meet PCI DSS and HIPAA requirements, yet 31% of such workloads are slated for managed migrations by 2027. Hybrid patterns, accounting for 18% of 2025 spending, enable firms to modernize gradually while preserving sunk infrastructure costs. European telcos employ hybrids to ensure biometric templates never exit national borders, aligning with GDPR minimization clauses. Markets in China and Russia remain fragmented due to the complexity of cross-border data rules, which complicates vendor consolidation.

By End-User Industry: Retail Surge Outstrips Incumbents

The Banking, Financial Services, and Insurance sector held 32.44% of the revenue in 2025, reflecting high-value transactions that justify layered risk scoring. Retail and E-Commerce is, however, projected to lead growth at 21.36% as card-not-present fraud climbed to USD 9.3 billion in 2025, forcing merchants to adopt tokenized checkout and passkey sign-in. E-commerce sites in Southeast Asia introduced passkeys to 140 million shoppers, cutting takeover fraud by 38%.

Healthcare providers devoted 12% of IT budgets to identity controls after enforcement actions citing compromised clinician accounts escalated. Government agencies moved to phishing-resistant factors ahead of 2027 deadlines. Energy utilities validated firmware updates through hardware-rooted keys to meet IEC 62443 mandates. Education institutions adopted single sign-on for 280 million learners, slashing reset calls by 44%. Manufacturing extended API-based identity to suppliers, cementing secure data exchange without exposing internal directories.

By Organization Size: Cloud Economics Pulls SMEs Into the Fold

Large Enterprises generated 59.38% of 2025 revenue, a nod to sprawling application estates and regulatory exposure. Yet Small and Medium Enterprises are forecast to post a 20.16% CAGR as cloud subscriptions remove capital barriers. Okta’s Workforce Identity Cloud serves 18,500 SMBs that have switched from on-premises Active Directory to SaaS login, consolidating credentials under one roof.

European SMEs face the GDPR’s accountability principle, which no longer offers leniency based on headcount, driving the uptake of managed authentication bundles. Cyber-insurance underwriters in North America now require multi-factor authentication as a baseline, prompting smaller firms to adopt pay-as-you-go identity management. Australia’s Digital Transformation Agency curates vendor panels that pre-approve solutions for public contracts, accelerating SME procurement cycles. Talent shortages remain a hurdle, but turnkey cloud consoles that automate policy updates narrow the skills gap enough to sustain rapid growth.

Geography Analysis

North America accounted for 36.71% of 2025 revenue, as an executive order mandated zero-trust adoption across federal agencies, unlocking USD 420 million for phishing-resistant authenticators. Canada’s Treasury Board Secretariat synchronized federal guidance with the Pan-Canadian Trust Framework, creating a common credential backbone across provinces. Mexico’s National Digital Strategy emphasized identity for financial inclusion, yet slow backend modernization capped quick wins.

The Asia-Pacific region is forecast to deliver a 20.57% CAGR through 2031, driven by India’s Unified Payments Interface, which logged 102 billion authentication calls in 2025, and China’s directive that IoT gateways in critical infrastructure be shipped with hardware security modules. Japan and South Korea now require passkey support in mobile banking, and Singapore aligns risk guidelines with real-time scoring. ASEAN’s interoperability pilot, involving Singapore, Thailand, and Malaysia, aims for a region-wide credential federation but must still refine attribute schemas.

Europe advances on eIDAS 2.0, aiming to equip digital wallets for 80% of citizens by 2030. Germany’s BSI requires providers to host data within the European Economic Area and undergo annual audits. The United Kingdom’s exit from the mutual recognition framework forces companies to maintain separate customer flows, which increases costs. Adoption in the Middle East and Africa is mixed: Gulf states are rolling out national IDs linked to banking, while sub-Saharan countries struggle with patchy connectivity. Latin America experiences a moderate uptake as Brazil enforces strong customer authentication for Pix payments, although currency volatility elsewhere moderates spending.

Competitive Landscape

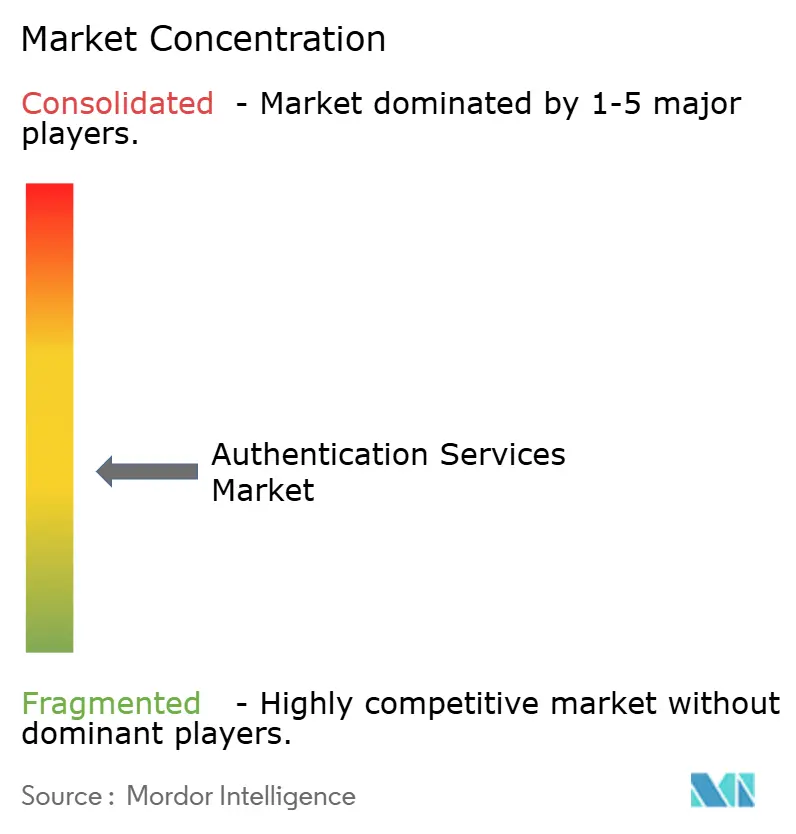

The authentication services market exhibits moderate concentration, with the top five vendors accounting for roughly 42% of the 2025 revenue, resulting in a score of 6 on a 10-point scale. Microsoft anchors its Entra suite across Azure, productivity, and security stacks, leveraging account ubiquity to upsell unified identity. Okta targets developer and workforce needs in one console, following its earlier Auth0 integration, and then strengthened adaptive capabilities by acquiring Spera Security in November 2025.

Thales appeals to banks with FIPS 140-3 Level 3 hardware security modules and Common Criteria certifications. Ping Identity partners with AWS Control Tower, enabling cloud administrators to quickly enforce federation. Cisco folds Duo Passwordless into its secure access edge, pitching a single vendor for identity and network controls. IBM Verify SaaS layers AI risk scoring over contextual signals to curb false positives.

Disruptors chase niches: Beyond Identity and Stytch champion developer-friendly, passwordless kits. Hardware makers such as Yubico embed biometrics on-device, avoiding cloud storage of templates. Hyperscalers bundle identity in platform fees, shrinking standalone addressable spend but enlarging total deployments. Decentralized identity pilots run on distributed ledgers but await clearer policy stances before scaling.

Authentication Services Industry Leaders

Entrust Datacard Corporation

IBM Corporation

Microsoft Corporation

Google LLC

Tata Communications Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Microsoft released passkey support to all Entra ID tenants, reducing password reset tickets by 47% during pilots.

- November 2025: Okta acquired Spera Security for USD 280 million to fold behavioral biometrics into Workforce Identity Cloud.

- October 2025: Thales won a EUR 150 million (USD 165 million) contract supplying hardware security modules for the eIDAS 2.0 wallet pilot.

- September 2025: Google extended passkeys to Google Workspace, reporting a 52% drop in account-takeover incidents.

Global Authentication Services Market Report Scope

The Authentication Services Market Report is Segmented by Authentication Type (Single Factor Authentication, Multi Factor Authentication, Passwordless Authentication), Service Type (Compliance Management, Managed Public Key Infrastructure, Subscription Keys Management, Reporting and Analytics, Risk-Based Authentication Orchestration), Deployment Mode (On-Premises, Public Cloud, Private Cloud, Hybrid), End-User Industry (IT and Telecommunications, BFSI, Government and Defense, Healthcare, Retail and E-Commerce, Energy and Utilities, Manufacturing, Education, Other End-User Industries), Organization Size (Small and Medium Enterprises, and Large Enterprises), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, South America). Market Forecasts are Provided in Terms of Value (USD).

| Single Factor Authentication |

| Multi Factor Authentication |

| Passwordless Authentication |

| Compliance Management |

| Managed Public Key Infrastructure |

| Subscription Keys Management |

| Reporting and Analytics |

| Risk-Based Authentication Orchestration |

| On-Premises |

| Public Cloud |

| Private Cloud |

| Hybrid |

| IT and Telecommunications |

| BFSI |

| Government and Defense |

| Healthcare |

| Retail and E-Commerce |

| Energy and Utilities |

| Manufacturing |

| Education |

| Other End-User Industries |

| Small and Medium Enterprises |

| Large Enterprises |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| By Authentication Type | Single Factor Authentication | ||

| Multi Factor Authentication | |||

| Passwordless Authentication | |||

| By Service Type | Compliance Management | ||

| Managed Public Key Infrastructure | |||

| Subscription Keys Management | |||

| Reporting and Analytics | |||

| Risk-Based Authentication Orchestration | |||

| By Deployment Mode | On-Premises | ||

| Public Cloud | |||

| Private Cloud | |||

| Hybrid | |||

| By End-User Industry | IT and Telecommunications | ||

| BFSI | |||

| Government and Defense | |||

| Healthcare | |||

| Retail and E-Commerce | |||

| Energy and Utilities | |||

| Manufacturing | |||

| Education | |||

| Other End-User Industries | |||

| By Organization Size | Small and Medium Enterprises | ||

| Large Enterprises | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

Key Questions Answered in the Report

What CAGR is predicted for the authentication services market through 2031?

The market is forecast to grow at 19.51% annually between 2026 and 2031.

Which authentication method is expanding the fastest?

Passwordless authentication is projected to advance at a 20.29% CAGR as enterprises retire passwords and SMS codes in favor of passkeys and biometrics.

How large is public cloud’s share of spending?

Public cloud deployments accounted for 63.29% of global revenue in 2025 and are expected to rise further.

Which region will see the quickest growth?

Asia-Pacific is set to register a 20.57% CAGR, driven by large-scale digital-identity and mobile-payment ecosystems.

Why are SMEs accelerating adoption?

Subscription-based identity platforms remove upfront capital costs, and cyber-insurance policies increasingly require multi-factor authentication.

How is user fatigue being addressed?

Vendors deploy adaptive risk engines that suppress challenges for low-risk actions and promote passkeys to eliminate code fatigue altogether.

Page last updated on: